On Wednesday, the Federal Reserve concluded their January “FOMC” meeting and released their statement. Overall, there was not much to get excited about, as it was virtually the same statement they released at the last meeting.

However, Jerome Powell made a comment which caught our attention:

“We do see asset valuations as being somewhat elevated”

It is an interesting comment because he compares it to equity yields.

“One way to think about equity prices is what’s the premium you’re getting paid to own equities rather than risk-free debt.”

As we have discussed previously, looking at equity yield, which is the inverse of the price-earnings ratio, versus owning bonds is a flawed and ultimately dangerous premise. To wit:

“Earnings yield has been the cornerstone of the ‘Fed Model’ since the early ’80s. The Fed Model states that when the earnings yield on stocks (earnings divided by price) is higher than the Treasury yield, you should invest in stocks and vice-versa.”

The problem here is two-fold.

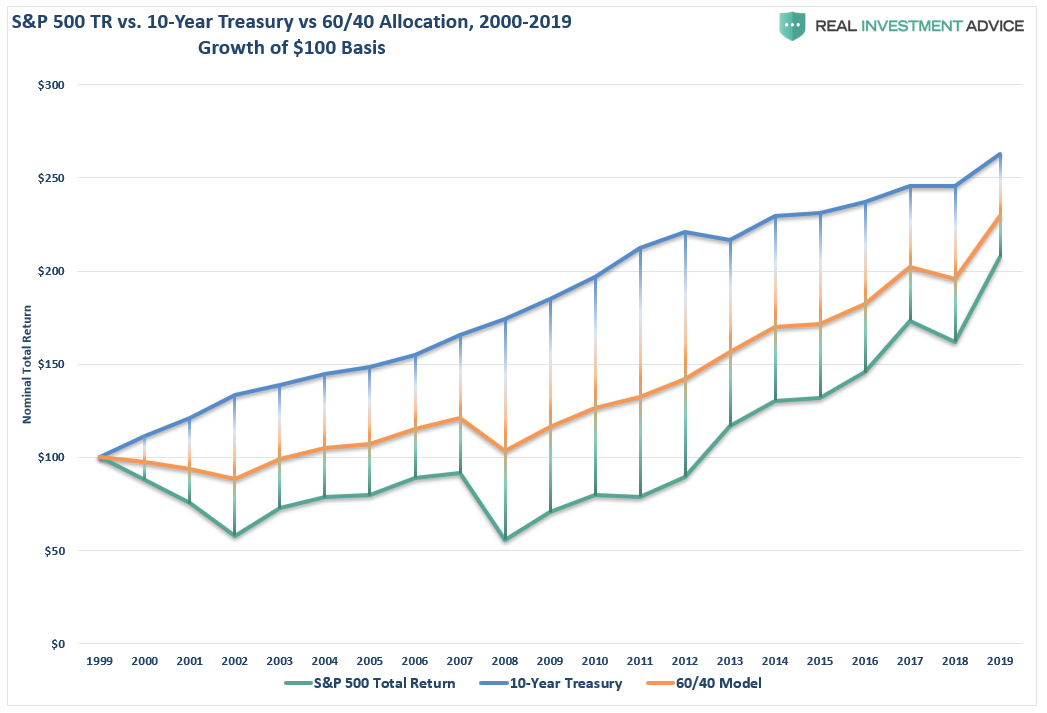

1. You receive the income from owning a Treasury bond, whereas there is no tangible return from an earnings yield. For example, if we purchase a Treasury bond with a 5% yield and stock with an 8% earnings yield, if the price of both assets remains stable for one year, the net return on the bond is 5% while the return on the stock is 0%. Which one had the better return? Furthermore, this has been especially true over the last two decades where owning bonds has outperformed owning stocks. (Data is total real return via Aswath Damodaran, NYU)

2. Unlike stocks, bonds have a finite value. At maturity, the principal is returned to the holder along with the final interest payment. However, while stocks may have an “earnings yield,” which is never received, stocks have price risk, no maturity, and no repayment of principal feature. The risk of owning a stock is exponentially more significant than owning a “risk-free” bond.

This flawed concept of risk, as promoted by the Federal Reserve, also undermines their view of current valuations.

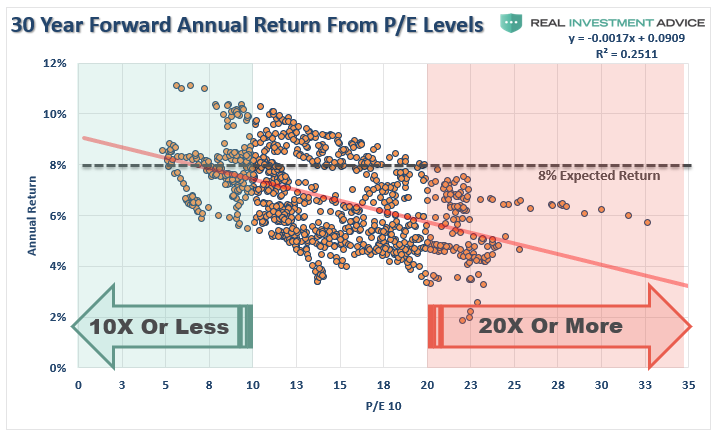

I have spilled an enormous amount of “digital ink” discussing the importance of valuations on future returns for investors, and most recently, why high starting valuations are critically important to individuals at, or near, retirement.

“Over any 30-year period, beginning valuation levels have a tremendous impact on future returns. As valuations rise, future rates of annualized returns fall. This should not be a surprise as simple logic states that if you overpay for an asset today, the future returns must, and will, be lower.”

Not surprisingly, valuations are often dismissed in the short-term because there is not an immediate impact on price returns. Valuations, by their very nature, are not strong predictors of 12-month returns. This was a point made by Janet Yellen in 2017:

“The fact that [stock market] valuations are high doesn’t mean that they’re necessarily overvalued. For starters, high valuations don’t portend lackluster returns in the near term. History shows that valuations provide no reliable signal as to what will happen in the next 12 months.”

That is correct. However, over long periods, valuations are strong predictors of expected returns, which is what matters for investors.

As my friends over at Crescat Capital, Kevin Smith and Tavi Costa, recently penned:

“The problem is that P/E, even Shiller’s cyclically adjusted P/E ratio (CAPE), is a potential value-trap measure in the current economy because of three issues:

- Profit margins are unsustainably high today, not only within this business cycle but compared to other business cycles making P/E ratios understated;

- The P/E ratio completely ignores debt in its valuation, not a good idea at a time when corporations have record leverage; and

- The most common measures of total market P/E use the mean rather than median company valuation which understates the average company’s multiple today by putting more weight on bigger, more profitable companies – the median better captures the valuation of the breadth of the market.

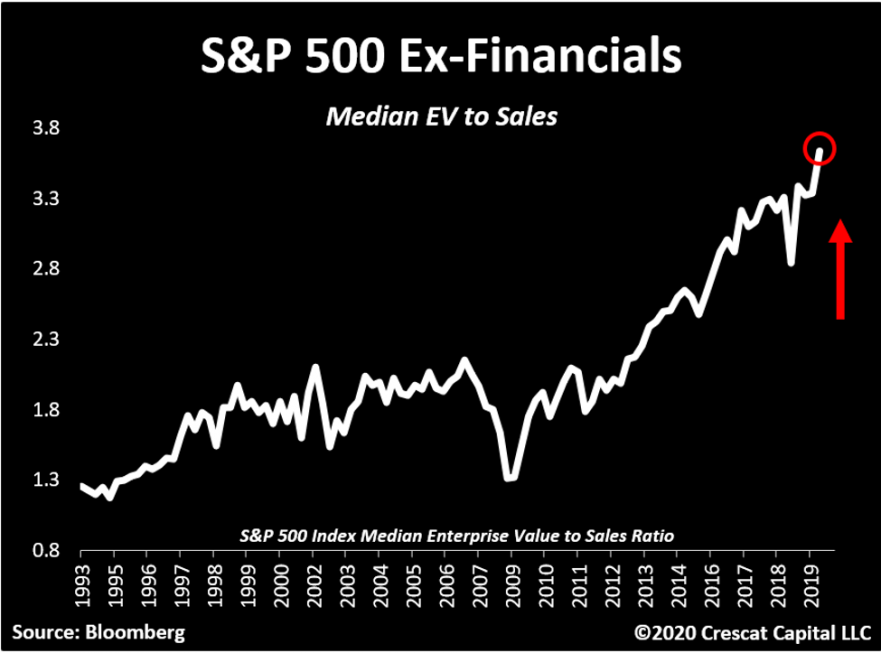

We believe median enterprise value to sales is one of the best measures to understand the extent of the bubble in the stock market today compared to history. By looking at sales and not earnings, we control for today’s likely fleeting, record-high profit margins. And because EV includes debt as well as equity in the total valuation of the company, it properly reflects the valuation of the business. Finally, our focus on the median company’s valuation illustrates the breadth of the valuation extreme in the market today.”

Let’s break down Crescat’s important points visually.

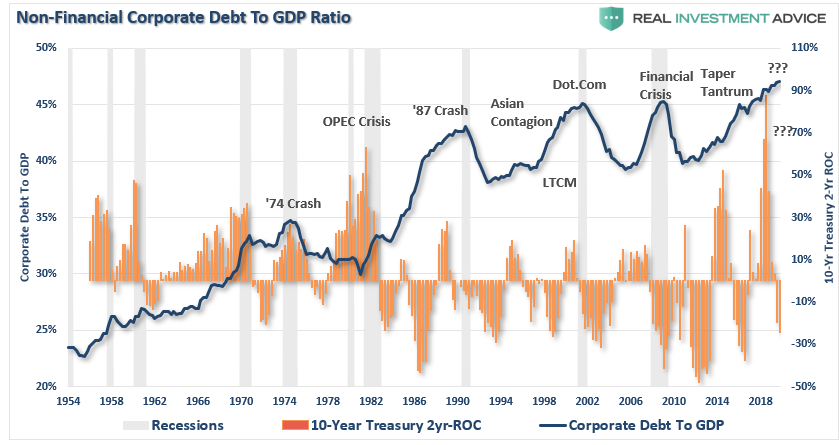

Since the economy is driven by consumption, and theoretically, companies should be taking on debt for productive purposes to meet rising demand, analyzing corporate debt relative to underlying economic growth gives us a view on leverage levels.

As Scott Minerd, CIO of Guggenheim Investments tweeted on Friday:

Scott Minerd ✔@ScottMinerd

There is no doubt that we are in the “everything bubble.” Pick your asset class and prices are up. But the heavily indebted corporate sector is vulnerable if the #economy begins to slow.

452Twitter Ads info and privacy

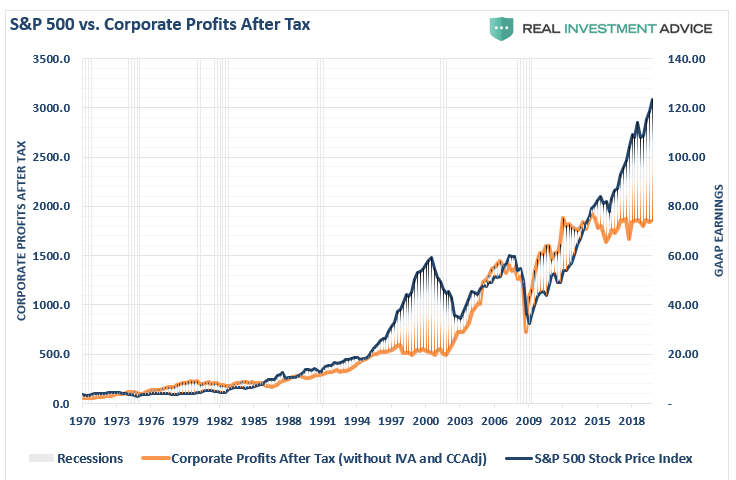

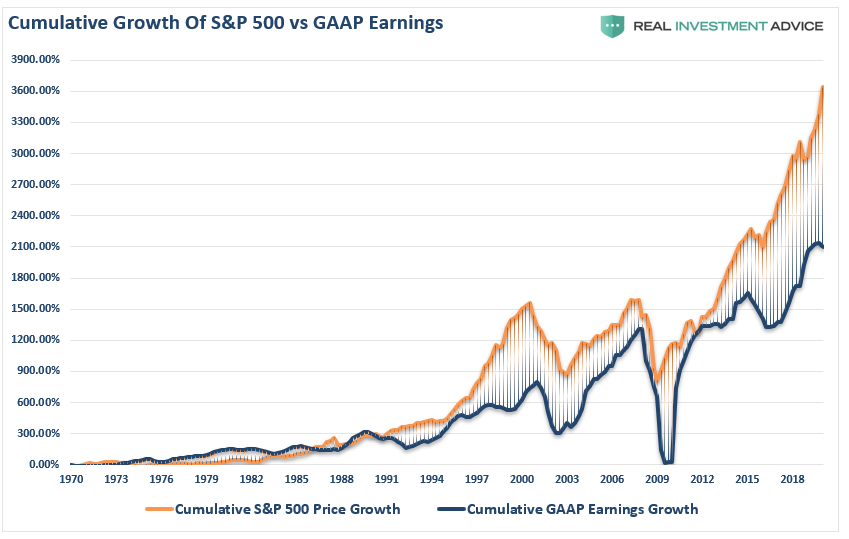

The problem with debt, of course, is it is leverage that has to be serviced by underlying cash flows of the business. While asset prices have surged to historic highs, corporate profits for the entirety of U.S. business have remained flat since 2014. Such doesn’t suggest the addition of leverage is being done to “grow” profits, but rather to “sustain” them.

However, when it comes to GAAP earnings per share, which have been heavily manipulated by massive levels of “share buybacks,” the deviation between what investors are paying for earnings is the largest on record, far surpassing the “Dot.com” bubble era.

“The average investor does not need an advanced finance degree to understand these valuation points. It is a worthy endeavor to avoid getting caught up in the popular delusions associated with late-cycle market euphoria. We believe investors will need a good grounding in valuation and business cycle analysis to reject the common buy-the-dip advice that is soon to become prevalent in the still early stages of what is likely to become a brutal bear market.” – Crescat Capital

As I stated above, what price-to-earnings (P/E) ratios tell us is that high valuations lead to lower future returns over time. However, what Jerome Powell misses in comments that valuations are elevated, but not concerning, is that it isn’t just P/E’s which are elevated.

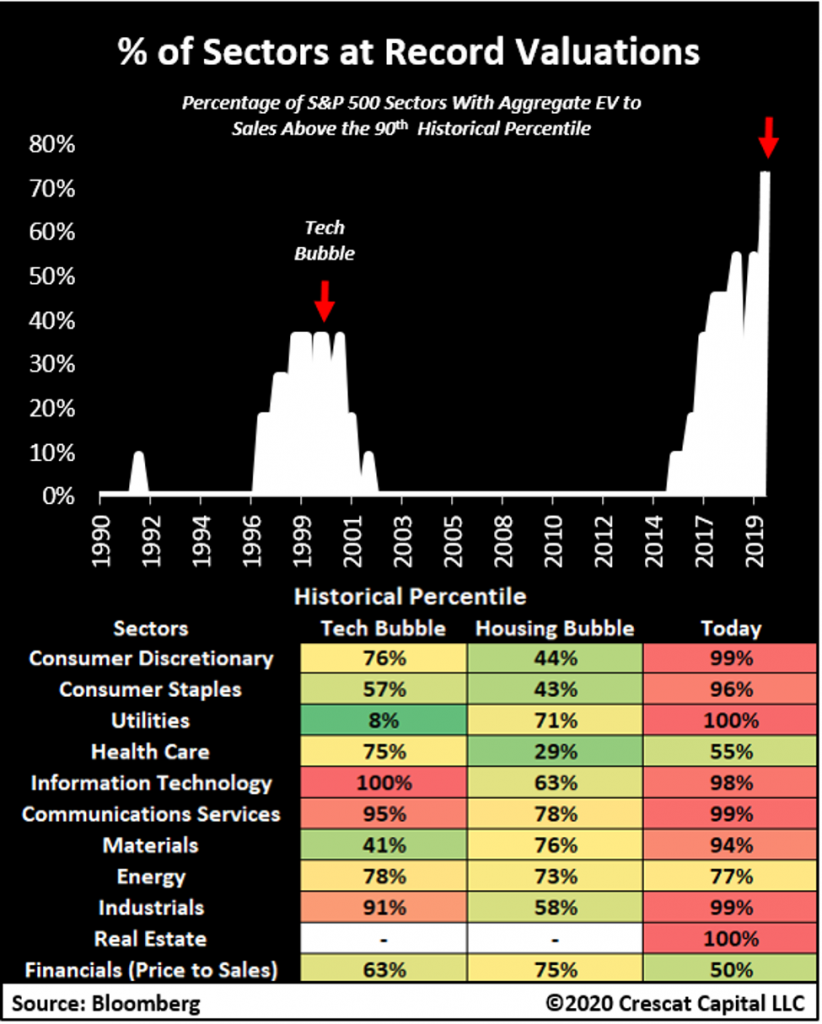

“Below is another way to visualize the current market valuation extremes to understand the risks of a severe market downturn ahead. Here we look at each sector of the S&P 500 and compare its valuation today to compared to prior market peaks in the tech and housing bubbles in 2000 and 2007. We can see that an unprecedented 8 out of 11 sectors are at top-decile, historical valuations illustrating the breadth of the current market excess.” – Crescat Capital

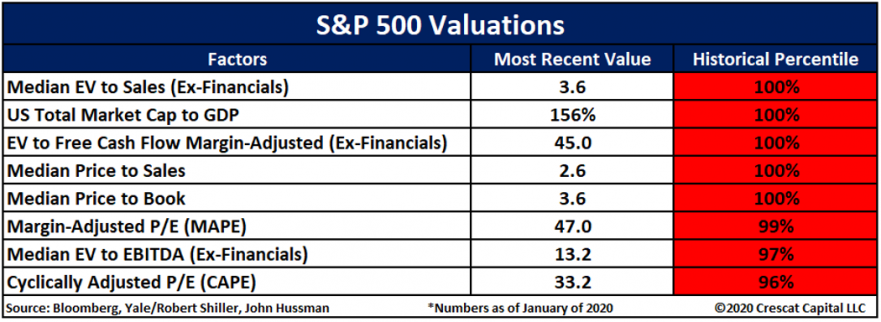

“Below we show the gamut of measures currently at record high fundamental valuation for the market at large based on their historical percentile ranking. Data for MAPE and CAPE ratios go back prior to 1929! The other measures are based on the entire history of available data which goes back at least two and half business cycles:” – Crescat Capital

Low Interest Rates Support Higher Valuations

This is where we generally hear a common refrain from the mainstream media:

“Low levels of interest rates justify higher valuations.”

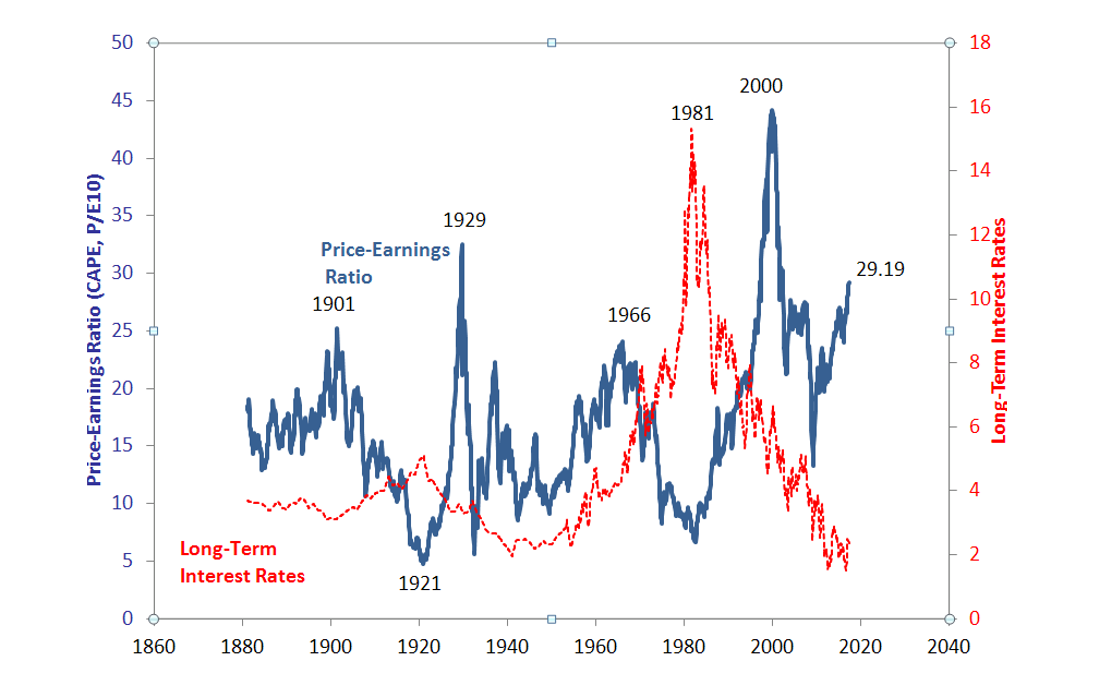

To analyze the relative value argument, let’s look at the interaction of interest rates and stock valuations over the broad sweep of time. As shown, extremely high stock market valuations occurred in 1929, 2000, and recently. However, interest rates were extremely low only once (recently) during those three occurrences. If low interest rates coincide with extremely high stock valuations only one time out of three, then it is obvious that low interest rates do not cause, or justify, high stock valuations. Yet “low interest rates justify high stock valuations” is one of the certainties of the current mainstream narrative.

Source: Robert Shiller, multipl.com. Data through June 2017.

If we isolate the times when interest rates were extremely low, the 1940s and currently, we find in the 1940s stock valuations were low. So, the statement that low interest rates justify high stock valuations is only supported by one event….now.

A better understanding is achieved by the relative value argument that extremely high interest rates coincide with extremely low stock market valuations, which occurred in 1921 and 1981. Although a sample size of two observations is not enough to draw a statistically-significant conclusion, at least it is two events with the same outcome.

The historical relationship between extremes in stock market valuations with extremes in interest rates is as follows:

- Extremely high interest rates, which have occurred twice, coincided with low stock market valuations.

- Extremely low interest rates, which have occurred twice, have coincided with high stock market valuations only once; today.

- Extremely high stock valuations have occurred three times. Only once (1/3 probability) did high stock valuations coincide with low interest rates; today.

- If extremely low interest rates do not justify extremely high stock market valuations, then a rise in rates should not necessarily cause a decline in stocks, but rising rates do lead to market corrections and bear markets.

Crescat Capital also weighed in on this point as well:

“A common argument today is that low interest rates justify today’s high equity valuations. That is not true at all. When low interest rates are due to low growth and excessive debt, as is the case today, no valuation premium is justified.”

Make No Mistake

Jerome Powell clearly understands that a decade of monetary infusions and low interest rates has created an asset bubble larger than any other in history. However, they are trapped by their own policies as any reversal leads to the one outcome they can’t afford – a broad market correction.

“In the U.S., the Federal Reserve has been the catalyst behind every preceding financial event since they became ‘active,’ monetarily policy-wise, in the late 70’s.”

This is the problem facing the Fed.

Currently, investors have been led to believe that no matter what happens, the Fed can bail out the markets and keep the bull market going for a while longer. Or rather, as Dr. Irving Fisher once uttered:

“Stocks have reached a permanently high plateau.”

Interestingly, the Fed is dependent on both market participants, and consumers, believing in this idea. With the entirety of the financial ecosystem now more heavily levered than ever, due to the Fed’s profligate measures of suppressing interest rates and flooding the system with excessive levels of liquidity, the “instability of stability” is now the most significant risk.

The “stability/instability paradox” assumes that all players are rational, and such rationality implies avoidance of complete destruction. In other words, all players will act rationally, and no one will push “the big red button.”

The Fed is highly dependent on this assumption as it provides the “room” needed, after more than 10-years of the most unprecedented monetary policy program in U.S. history, to try and navigate the risks that have built up in the system.

Simply, the Fed is dependent on “everyone acting rationally.”

The problem comes when they don’t.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube