Coronavirus Clouds the Outlook

COVID-19 has brought a complete turnabout in U.S. risk sentiment. Markets cannot be calmed: safe-haven assets like U.S. Treasuries have fallen to record-low yields while equity market volatility has been substantial. The U.S. Federal Reserve executed a large, out-of-cycle interest rate cut, its first such action since October 2008.

While this has been the most challenging interval for the U.S. economy since the last recession, analogies to the global financial crisis are inappropriate. That was an era defined by bank failures, nationalization of the auto industry and consumers losing their homes. Outcomes thus far are nowhere near that severe, and are unlikely to be.

Current dour sentiments are driven by uncertainty. As long as new infections continue to be reported, fear will persist. Other countries’ experiences suggest news in the U.S. will get worse before it gets better. However, we are encouraged by the high worldwide survival rates of COVID-19 and by China’s return to production after its serious slowdown. Recession is not our base case, and we expect a return to trend growth in the second half of the year. But the situation is fluid, and downside risks are certainly present.

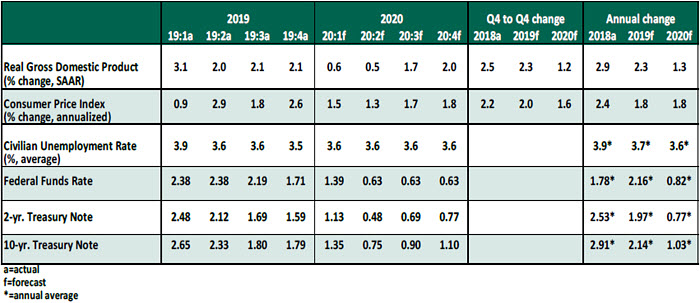

Key Economic Indicators

Influences on the Forecast

-

The Fed’s surprise rate cut of 50 basis points was a strong signal. While monetary policy is not a vaccine, easier financial conditions may help prevent layoffs and defaults as the economy endures turbulence.

- With uncertainty growing and risk sentiment declining, the Fed will likely cut by another 50 basis points at its March 18 meeting. Monetary policy consensus has evolved toward acting before a crisis is at its peak, and the Fed is unlikely to wait for developments to become worse.

- On the fiscal front, bipartisan authorization of $8.3 billion to support vaccine development and other response measures is a good start, but measures of a much larger scale are needed. We expect more government interventions in the weeks ahead, but the specifics are unclear. The most straightforward policies to implement, like a payroll tax reduction, would not help the unemployed or workers who are losing hours. More comprehensive social support, like paid sick leave, is complex and politically tenuous.