The month of March brought an onslaught of news requiring a daily reassessment of risks. The signs of recession are spreading: empty roads, closed stores, cancelled flights, postponed events and idled workers.

Today’s circumstances defy comparison to any recent experience. The spread of COVID-19 has not yet reached its peak in the U.S. As long as the rate of diagnoses continues to increase, commerce will be impaired, markets will be volatile and forecasting will be hazardous.

So, an economic outlook hinges critically on bending the contagion curve, and we expect this to be achieved in the second quarter. Decisive measures taken today, including social distancing, near-zero interest rates, and $1,200 checks distributed to eligible recipients, should help to keep the crisis from causing prolonged damage.

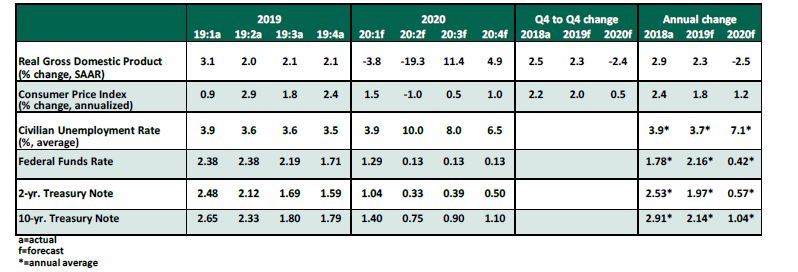

As our forecast table shows, we will see wide swings in the coming quarters. Scary readings should eventually fade as normal patterns of life are re-established.

Key Economic Indicators

Influences on the Forecast

- The Federal Reserve acted quickly and decisively to the emerging COVID-19 threat, in many respects returning to the playbook it created during the 2008 financial crisis:

- The overnight federal funds rate returned to its crisis low of 0%-0.25%, accompanied by forward guidance that the Fed will “maintain this target range until it is confident the economy has weathered recent events.”

- U.S. dollar swap lines with foreign central banks were re-opened to keep an ample supply of dollars available to the rest of the world.

- A commercial paper funding facility was announced to unlock the market for short-term corporate debt, as it was among the first to show stress. Credit facilities to support money market funds, primary dealers and bond issuers will also help keep financial markets functioning smoothly.

- Details are forthcoming as to how the Fed will “lever up” a portion of the fiscal response to generate up to an estimated $4 trillion of new credit for businesses.

- To address the economic effects of the coronavirus, the U.S. government has passed three rounds of spending totaling over $2 trillion, about 10% of U.S. annual gross domestic product (GDP). These measures are appropriately sized to combat this massive risk.

- U.S. residents will benefit from paid leave for COVID-19 patients, protections for parents taking care of children whose schools are closed and direct cash payments to help keep household budgets balanced during lean times.

- Businesses will qualify for loans and grants to maintain payrolls and rent payments as well as targeted support for severely impacted industries like airlines.

- Weekly initial jobless claims set the stage for a severe increase in unemployment. The March 26 reading of 3.3 million initial claims was unprecedented. Expect elevated levels ahead as state unemployment offices work through a backlog of claims. Monthly unemployment rates may exceed the record of 10.8% set in 1982. However, once consumers regain the ability and confidence to gather in public places, service sector jobs will recover quickly.

- U.S. GDP will likely show the beginnings of contraction in the first quarter of 2020, a jaw-dropping decline in the second quarter, and a sharp return to growth in the third quarter as recovery takes hold. The U.S. convention of reporting GDP growth at an annualized rate will make these changes appear especially steep; in total, we expect a full-year loss of 2.4%, to be followed by a year of growth in 2021.

- U.S. Treasury debt yields have fallen across all tenors, with 1-month and 3-month bills occasionally pushed into slightly negative yields. Investors currently value safety over returns, and demand is likely to keep yields suppressed in the year ahead. The ten-year yield will recover only gradually from its current record low.

- An ill-timed conflict among oil producers has sparked a price war, with energy markets flooded with crude oil supply. This will hinder U.S. producers, while low gasoline prices will provide limited benefit to home-bound consumers. Inflation, already below its targeted level, is likely to fall further.

© Northern Trust

© Northern Trust

Read more commentaries by Northern Trust