Still Bullish

New Models

Jet Fuel Market

Market sentiment reflects human sentiment, which lately has been quite negative—understandably so, given the great uncertainty surrounding the coronavirus pandemic. A month ago, we didn’t know where all this was going but it was potentially serious.

I can almost begin to sense sentiment changing. New drug therapies are being announced and dozens of vaccines are in development. There is a high probability one or more will work by the end of the year. Deployment will be difficult, but doable. This change in sentiment, combined with generous fiscal support and liquidity injections, gives investors more confidence, so we see stocks rising.

I am not generally one to “fight the tape,” but I really wonder how long this can last.

Looking at it not as an investor, but as an entrepreneur and small business owner, I think some are greatly overestimating how fast the economy can recover. Entire industries, no longer viable in their current forms, must now figure out new ways to do business.

They will figure it out, too, because that’s what entrepreneurs do. But they don’t do it overnight, or even in a few months, nor do they take direct paths from here to there. I am bullish on the American entrepreneur. Betting against not only the American entrepreneur but entrepreneurs worldwide in relatively free-market societies has always been a losing proposition. That doesn’t mean it will be easy or fast.

The rules have changed. As I wrote two weeks ago, we are in the process of Repricing the World. And I mean everything will get repriced. It is not clear how this will happen. Will landlords be forced (by the market) to take lower rents from restaurants? Will the cost of our restaurant food go up? Haircuts? A thousand other things we buy?

Today we’ll look at how this may work, and what it means for stock investors. For an even deeper discussion, register for my upcoming Virtual Strategic Investment Conference, an online event running over five days between May 11–21 for 4–5 hours a day. You can watch it live and ask questions, or watch the presentations at your leisure and personal time frame from your home or office. You’ll get written transcripts, too.

I can honestly say we have never had a lineup as powerful as this SIC. I have personally constructed it to answer the questions on our minds.

- How deep a shock is the current recession going to be, and what will recovery look like in the near term?

- What is the longer-term impact on the economy, the markets, and society?

- What profit opportunities will emerge from the rubble, and how do we seize them?

What will the impact be on the post-vaccine society? We will be talking geopolitics, lots of technology, specific investment ideas from some of the world’s greatest investment minds, the inside baseball of politics coming up, looking at China, Europe, and emerging markets, the fallout in the energy industry, and so much more.

This crisis has given me a chance to bring together almost twice as many speakers as I normally do, and bring them to you in the comfort of your own home or office, at a price that is a fraction of normal. Look at just a few of the names of the faculty:

Ian Bremmer, Leon Cooperman, Peter Diamandis, Niall Ferguson, George Friedman, Louis and Charles Gave (from France), Neil Howe, Lacy Hunt, Michael Pettis from China, Matt Ridley, Felix Zulauf from Switzerland, and last but not least, Ross Beaty, one of the world’s most successful gold miners.

There will be lots of short presentations combined with lots of panels and discussion. This conference is intended to give you the answers you need.

I have designed this conference to be the best roadmap I can possibly imagine for our journey into the future. I’ve tried to hit all the high points to make sure you walk away with specific, investable ideas. It will be inspirational and at times a little troubling. But that is what our future will bring. Better to have a roadmap with an idea of where to go than simply to walk into the future without a plan.

Join me. You know you not only want to, but you need to. This will be a once-in-a-lifetime event, and you don’t want to miss it.

I have written a very personal letter about this conference, outlining not just its purpose but giving you the details of every speaker and why they’re there. I am giving you the opportunity to see the “why” of every speaker. There are some famous names but also some less famous but brilliant thinkers you need to hear from right now. You can read that letter here. I think you will find it extraordinarily helpful as you make your own personal plans for the future, for your investments, your family, and your business.

I can almost guarantee you will be like the thousands of conference attendees who have over the years told me, “This has been the best conference ever.” I can tell you there will never be another one like this. Be there!

Still Bullish

The US economy contracted an annualized 4.8% in Q1, according to the first estimate released Wednesday. This same economy was growing (slowly) as of early March. For two or three weeks to pull the entire quarter down that far is unprecedented.

Fans of symmetrical bell curves will point out an economy that falls so fast can bounce back equally fast, particularly when monetary and fiscal authorities are injecting so much rocket fuel. We see this in the latest Barron’s Big Money Poll of 107 top money managers. Asked to forecast the stock market this year, 39% were bullish, 20% bearish, and 41% neutral.

So adding together the bullish and neutral, 8 out of 10 money managers see at least some chance of positive equity returns between now and year end. They are even more confident for 2021, with 82% bullish and only 4% bearish.

The Barron’s panel has tons of bullish quotes, arguing that things will go back to normal and now is the time to buy. Which is the same thing people said in 2007–2008.

My friend Ed Yardeni is similarly bullish, largely due to Federal Reserve actions. He also thinks analysts will probably overshoot their revenue and earnings estimates to the downside, then revise them upward later in a grandly bullish surprise.

As a natural optimist myself, I admire people who show confidence in tough situations. But I also think recovery will take more than a year or two. I talk to small business owners and corporate leaders all the time, and they all say it will be a long, hard climb out of this hole.

New Models

Last week I noted Woody Brock’s observation that the service sector drives growth and employment. The coronavirus closures, though necessary, were a kind of laser-guided missile into the service economy’s core. The numbers understate how much destruction occurred.

In 1920, 26% of the US population worked in the service sector of the economy. Today it is 86%. That is the primary reason for the extraordinary reduction in economic volatility. The manufacturing/inventory tail no longer wagged the dog. It was seemingly impervious, until this pandemic struck. Now, 30 million people have filed for unemployment in the last few weeks and potentially 10 million more in the gig economy have lost their income.

Unlike manufacturing, retailing, or agriculture, service businesses can’t hold inventory. They can’t just close for a few weeks and then make up the lost time. There is no second chance to sell that hotel room night, plane seat, restaurant meal, haircut, Uber ride, or cocktail. Revenue has been vaporized, not deferred. So, having permanently lost weeks or months of revenue while many fixed expenses continued, service businesses are deeply in the red.

There will be no return to business as usual as long as the virus remains a health threat. Service business can’t simply open their doors again. They have to reengineer everything they do. Processes that took years or even decades to design and optimize are now unworkable. Replacing them isn’t going to happen in a few weeks. And making processes efficient enough to match previous profit margins will take even longer.

Restaurants and other service businesses make money by filling a defined number of chairs with a defined number of people who spend a defined amount of money in a defined length of time. Interrupt any part of that formula and everything falls apart. That is what these businesses will return to when they’re allowed to reopen.

South Korea is a few weeks ahead of the US and the picture there is grim, according to this WSJ report.

When meeting in an office, people will wear masks. At meals, diners will sit next to each other or in a zigzag pattern, not directly across. Hotel rooms will be ventilated for 15 minutes after travelers check out. Visitors at zoos and aquariums must stand 6 feet apart. Shouting and hugging will be discouraged at sporting events. So will high-fives…

…Kwon Sae-min, 29 years old, who works at a bakery in Seoul, is now taking shoppers’ temperatures at the entrance and asking them to sanitize their hands and swipe their credit cards themselves.

“It’s a lot of extra work to manage customers now,” Ms. Kwon said.

Ms. Kwon puts her finger on the problem. Everything will be a lot of extra work now. The US may give businesses more flexibility than South Korea’s government is, but it’s not the only constraint. Customers have to feel safe. Governors can lift their lockdown orders but they can’t make people shop, nor can they make businesses open.

It’s not just Korea. Here is what Simon Hunt tells us from his sources in China:

A friend of ours left Shanghai for his home town in Hunan province. Shanghai airport was empty as was the airport in his home town in contrast to the usual hubbub at this time of year. Taxis were non-existent in his home town because there were so few visitors. Moreover, the taxi driver, who eventually appeared after an hour’s wait, told him that the high-speed train station was empty as well.

This example of life across China confirms our thesis that the average household will keep their hands in their pockets to rebuild savings and regain confidence. It thus won’t be until the 4th quarter that consumer spending will become the third driving force behind the economy’s recovery, the other two being infrastructure and building.

That is echoed in John Browning’s Letter from Shanghai #451:

But as here in Shanghai we are perhaps in week 15 of the pandemic and the US in week 7 or 8 perhaps we can discuss the challenges that lay ahead. I note online grocery shopping has taken off in a big way, and one of my local supermarkets has closed seemingly for good. But the small local shops are thriving, and there is a genuine sense of localism, as throughout the pandemic they have earnt the gratitude and goodwill of the community, a change I suspect that will be permanent. Indeed, I have no desire to travel across town, anywhere I cannot walk is too far. Which also means for my bigger ticket items, online shopping is the way to go.

The lesson of China is that fear of a second wave of infection and nagging job insecurity encourages people to stay at home and save. Mr. Powell already recognizes the Fed-engineered recovery is unlikely to bring the US economy “quickly back to pre-crisis levels” and “there will still be a level of caution… that might remain for some time.” If I can paraphrase for a moment, if we are wearing masks, consumption will not be as it was before.

I hear the same from other sources in China. Businesses are coming back but consumers remain cautious.

In parts of the US, restaurants are being allowed to reopen at lower capacity, usually 25% or 50%. They can’t turn a profit that way, even without all the extra costs. So often the financially smartest thing they can do is stay closed, and many are. Maybe they will open in a few weeks, if the virus and associated restrictions ease. But meanwhile, workers stay unemployed and everyone’s spending remains muted.

The same applies in retail. Macy’s is beginning to reopen its stores but one executive told WSJ he expects less than a fifth of normal sales volume at first.

There are multiple problems:

- Customers are reluctant to return

- Those who do return will spend less

- Serving them as now required and/or expected will cost more.

That math is not consistent with a V-shaped recovery, even with all the stimulus funding. You don’t have to search long to realize that the money supposedly flowing to Main Street isn’t getting down to the smallest businesses. Even if they represent only 10 or 15% of the economy, that is enough to spark a severe, prolonged recession.

Do we come back? Absolutely. The question is when and how?

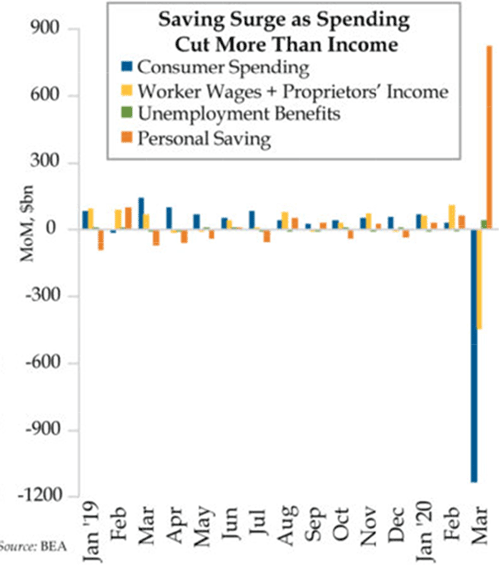

Let me pull out this snippet from Danielle DiMartino Booth of Quill Intelligence (one of my daily must-reads). Notice the chart. American consumers are behaving exactly like the Chinese consumers described above. Human beings react to uncertainty the same all over the world. They become cautious.

Spending cuts exceeded income gains in March, generating a moonshot for personal savings; the backlog of unemployment filings signals a sustained improvement in consumption will elude absent a labor market recovery as unapproved claimants are deprived of any income.

Jet Fuel Market

I think businesses will figure this out, given time. The problem is that losses keep accumulating and the hole gets deeper. That isn’t good for corporate earnings, and not just at service businesses. A kind of reverse trickle-down effect will affect almost every consumer and business.

Many stock market bulls recognize this but think it won’t matter as the Fed keeps injecting more jet fuel. I am not sure that’s a good assumption. The Fed has done quite a lot and pledges even more, but Main Street needs customers. The Fed can’t create them.

Nonetheless, the jet fuel has succeeded in pushing stock benchmarks and valuations back near their old highs. Clearly, and probably rightly, investors are willing to look past the second- and possibly even third-quarter earnings, which everyone acknowledges will be dismal.

But what happens when earnings are dismal in the fourth quarter?

With the Fed in the mix, I suppose new market highs are possible this year or next, but I can’t imagine it lasting long. The animal spirits that drove well-known names higher are seriously weaker than they were in February, and I don’t foresee them coming back.

Two big points:

- Some businesses, both small and large, are going to do extremely well in this environment. Their earnings will rise. They will help pull the indexes up. Likewise, we are going to lose more businesses than most currently think. They will have the opposite effect. This is going to be a stock picker’s market. Index investors, as I have been saying for several years, will get their heads and their 401(k)s handed to them.

- Again, I readily grant that the market is looking past the next two quarters. But are investors going to look past the fourth quarter? Even if we get a vaccine by year-end, it will be a miracle if we all get it by the end of 2021’s first quarter. And balance sheets have been destroyed for so many businesses. There will be opportunities for startups everywhere, as seasoned management will need capital.

It is entirely possible that investors simply become disillusioned with looking past the next few quarters’ earnings. At some point, the attitude will change to, “Show me the money!” Then again, who knows what the Fed will do. If the market starts turning down will they start buying stock ETFs like Japan is? Dear gods, I hope not. But right now, there is simply no way to predict what they will do.

- A bonus point. The big indexes are composed of the biggest companies. I will bet that over 100 companies currently in the S&P 500 will not be there 12 to 15 months from now.

Just a reminder: Bull markets like this one don’t just retreat to reasonable valuations. They usually overshoot to the downside just as they did on the upside. The lower bound is probably lower than many “worst-case” scenarios suggest. That will not be good for Baby Boomer retirement plans.

But in any case, this experience is going to leave deep scars on the economy, and on consumer/investor/business sentiment. This is going to scar a generation just as deeply as the Great Depression scarred our parents and grandparents. Things we once took for granted—a leisurely restaurant meal, catching a movie, sharing a concert or a ballgame with other fans—are gone now and will come back in a different form.

But they will come back. We’re moving from one world to the next—an Age of Transformation—whether we want to or not.

The letter is already running a little long, and frankly, feels as personal as my usual personal ending, so I think I will just hit the send button and wish you a great week! And sign up for the SIC. We are all going to need that roadmap, and I want you on the journey with me!

Your still optimistic for the long run analyst,

John Mauldin

© Mauldin Economics

www.mauldineconomics.com

© Mauldin Economics

Read more commentaries by Mauldin Economics