SUMMARY

- Pandemic Policy Hasn’t Always Seized The Moment

- China Sets Its Priorities

- Some Reports of Progress Are Greatly Exaggerated

Timing is everything. We want to hit the road just ahead of rush hour. We enjoy perfectly ripe fruit, and a perfectly cooked steak. (And a perfectly aged wine to go with it.) We seek to deliver jokes with just the right cadence so that a gathered group stops to laugh out loud. Getting the timing right is not always easy, but the rewards can be ample. The poor pacing of some recent economic interventions, however, is no laughing matter.

Vast tracts of the global economy came to a stop during the month of March. Large numbers of people were forced to work from home (if they could) alongside children engaged in distance learning. Many were furloughed from their jobs, with no certainty about when (or if) they would be called back. Fortunately, policymakers tried to gear their actions to match the rapid and massive downturn in activity. Legislatures passed emergency spending measures with impressive speed, at an impressive scale.

Two months later, however, some of those bold initiatives have yet to reach their intended beneficiaries.

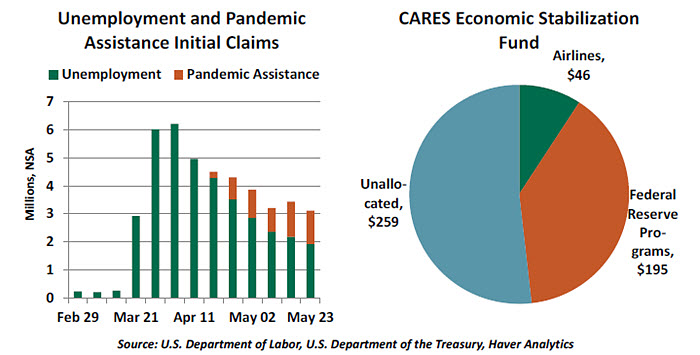

Among the more effective measures has been the direct Economic Impact Payments called for in the Coronavirus Aid, Relief, and Economic Security (CARES) Act. The undertaking was ambitious; wide-scale disbursements are a rarity, and stimulus checks in past crises took months to reach households. Five weeks after the program was announced, more than 130 million payments had been disbursed. But 20% of those eligible are still waiting for their money.

The recent surge of initial unemployment insurance (UI) claims has been shocking. More than 40 million Americans, or about one-quarter of the total labor force, have filed for benefits. As a result, most state unemployment systems have struggled to keep pace with new cases. Adding to the challenge, the CARES Act also created Pandemic Unemployment Assistance (PUA), allowing millions of self-employed and gig workers to qualify for jobless benefits. To this day, from Oregon to Wisconsin to North Carolina, frustration continues as states’ employment security systems groan under unprecedented workloads. At this point, only about 60% of Americans who have filed for unemployment benefits have actually received them.

“There has been a lot of red tape holding back crisis-related benefits.”

The CARES Act featured a supplement of $600 per week on top of state UI benefits. Bringing that program online across all 50 states took a month, and it is up to each state to disburse any of these payments due in arrears. States were already working to catch up to the backlog of new claims, and this change to the process complicates their existing workflows.

One of the CARES Act’s more contentious points was its $500 billion Economic Stabilization Fund (ESF) to support larger businesses. Careful negotiations were required to ensure it had sufficient oversight. While $46 billion of this fund was earmarked to support airlines and industries essential for national security, no payments have actually been made.

Of the remaining $454 billion, the Treasury has committed up to $195 billion to capitalize the Federal Reserve’s interventions (of which only $37.5 billion has actually been disbursed). In testimony before the Senate Banking Committee last week, Treasury Secretary Steven Mnuchin committed the “remaining $259 billion to create or expand programs as needed.” The ESF may have served its role as a stabilizing signal of emergency fiscal support, but very few of the funds have actually been deployed.

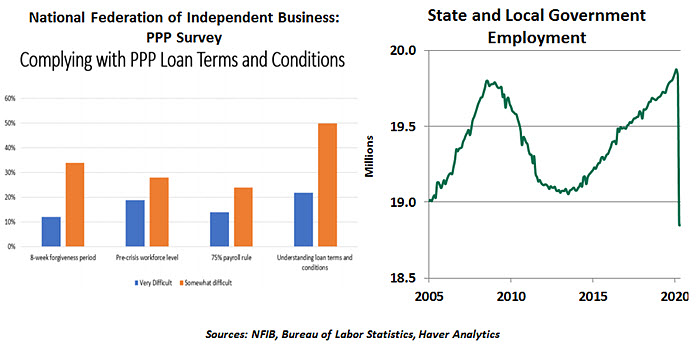

Another program that was originated with great fanfare has struggled to benefit its intended audience. The Paycheck Protection Program (PPP) was celebrated upon its launch. But processing applications proved to be a nightmare. Then questions arose as to whether its forgiveness requirements were achievable for many businesses, and the Fed’s commitment to disclosing loan details put off many potential applicants. As shown in the survey below, small business owners reported great difficulty understanding the terms and conditions of PPP loans.

Favor quickly turned against PPP. After the first tranche of funding ran out in two weeks, the second tranche remains open five weeks after it was approved. Congress is now considering broadening the group of expenses that quality for PPP forgiveness and lengthening the time over which these can accrue. But uncertainty and delays will undoubtedly cost some small businesses their lives.

State and local governments are another area witnessing a slow fiscal policy response. These public bodies are stretched; their reliance on sales and income taxes has pinched their revenue, while expenses for UI payments and public health are only increasing. States have limits on their capacity to borrow to survive a recession. This has led to staffing cuts for many non-essential services at a more extreme pace than past downturns.

“Without additional aid, states will have to cut payrolls and services.”

The CARES Act included only token amounts for states to use in their medical responses, but much more direct aid will be required. Just as the PPP sought to preserve employment by incenting small companies to maintain headcount, help for state and local governments aims to prevent further job losses among entities that account for one-in-eight jobs in the U.S.

The policy response still has room to run. If any further programs are to be passed, they are not coming with any urgency. The House of Representatives passed a large but partisan spending package, and the Senate is adjourned until next week.

While aspects of the U.S. response have been slow, it could be worse. Just this week, the European Union passed its first joint fiscal response. Its member nations have been left to their own devices to support their economies, fighting against a virus that does not recognize borders. But this aid will come slowly, too, and will likely not be operational until the forthcoming fiscal year.

Standing up new programs in short time frames is bound to be challenging; some frictions are to be expected. But while the U.S. Congress deserves an “A” for effort, its grade for execution is an “incomplete” at best. Unless relief begins to arrive in a more timely way, the economic recovery may be late to arrive.

‘Two Sessions’, Two Messages

After a two-month delay owing to the COVID-19 outbreak, China concluded its most important political event, the annual Two Sessions meetings. Its top leadership had convened to outline the country’s domestic and foreign policy agendas.

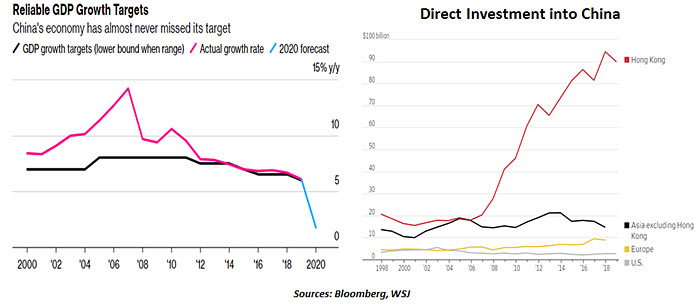

For decades, China has set a growth target, and those targets have never been missed. However, this year, economic activity in China has suffered due to COVID-19 lockdown measures. GDP contracted by 6.8% year-over-year in the first quarter, while unemployment climbed near historic highs. At the Two Sessions meeting, China opted to shelve its growth target for this year. This is the first time since records began in 1990 that authorities have not set a numeric objective for total output. Uncertainty amid the COVID-19 pandemic was one reason behind this move; another was a desire to obscure the depth of the Chinese downturn.

While some would argue that the absence of a growth target could weaken investor confidence in policy measures, others like us are of the view that a target close to the previous level would have been difficult to achieve. As we wrote last year, an unrealistic target would only provide an incentive to inflate output data and undertake short-term stimulus that might not be in China’s best long-term interests.

Chinese authorities did announce support measures for the economy. The fiscal deficit target has been raised from 2.8% of GDP in 2019 to at least 3.6% of GDP this year, the highest in recent decades. National and local governments will issue a total of CNY3.75 trillion ($528 billion) in additional debt to support stimulus programs. Although Chinese data is showing signs of recovery, these fiscal measures reflect the concerns on policymakers’ minds that the recovery could be slower than desired.

China’s congress outlined the country’s foreign policy plans, too. The main focus was on Hong Kong: China’s leadership has opted to impose a new national security law to deal with pro-democracy protests. This has raised concerns over Hong Kong’s status as one of the world’s leading financial centers and trade hubs, which was already under stress from political events of last year and recent travel restrictions amid the pandemic.

Hong Kong enjoys a special status globally, allowing it to negotiate trade and investment pacts independently. For instance, U.S. tariffs on Chinese imports are not applied to imports from Hong Kong. However, this might be at risk. The U.S. administration has declared that Hong Kong is no longer sufficiently distinct from the mainland, which could cause a reconsideration of the special status.

Reappraisal of Hong Kong’s status by businesses and investors could lead to the flight of individuals, capital and multinational corporations, which would harm both sides. Hong Kong is one of the world’s biggest markets for equity and debt financing. China relies on liquidity and financial markets conducted through Hong Kong, with several Chinese firms listing shares on its exchange. Hong Kong is Beijing’s major source of foreign direct investment and a global hub for internationalization of its currency.

“Troubling news from the Far East.”

Economic issues remain a priority for Beijing as the economy remains under massive strain, but its stance on foreign policy, particularly Hong Kong, is raising anxieties among market participants. How China deals with Hong Kong will not only have implications for the latter, but for U.S.-China trade and investment relations as well. The Two Sessions gathering and the situation in the Far East are sending troubling messages to the markets.

Too Rosy

We are as anxious as you are to begin seeing firm signs that the economy has bottomed. But recent headlines trumpeting rapid advances must be taken with considerable caution.

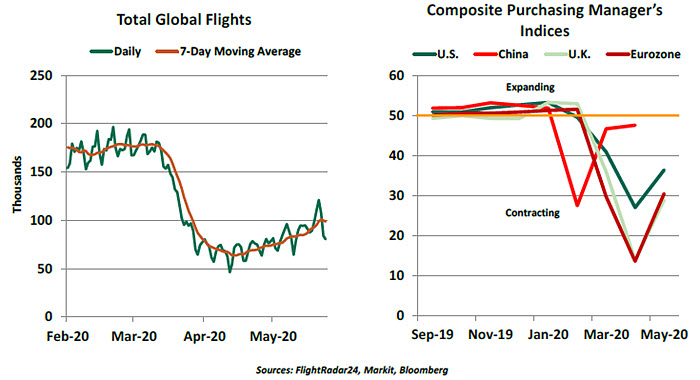

In some cases, math can be misleading. Take, for example, a recent upbeat report stating that global airline traffic had increased by 162% between April 12 and May 21. While the calculation is correct, it compares a Sunday (when traffic is typically light) with a Thursday. Using a seven-day moving average, the rate of increase during that same interval slowed to 50%. Further, the number of flights (on a seven-day average basis) fell 65% from the beginning of the year through mid-April; gaining 50% from that low base still leaves traffic down 46% from January levels. And that does not account for the fact that passenger loads on many flights are a small fraction of what they had been before COVID-19.

Another example centers on the closely watched purchasing managers indices (PMIs) that are computed for a broad range of countries. PMIs are derived from a simple survey in which respondents are asked whether conditions have gotten worse, stayed the same, or improved. The index takes the fraction of those who reported improvement and adds half of those who reported that things stayed the same. Readings above 50% are presumed to signal economic advance.

“It’s easier to show progress from a low base.”

But if conditions descend sharply and then stabilize, you will see rising PMIs as more survey respondents report no change in their outlooks. We are seeing improvement in these measures for May, but activity is still deeply depressed.

Data can be viewed in a variety of ways, but conclusions can be shaped by the perspective of the analyst. While we would be delighted to embrace truly upbeat trends, we must remain as objective as we can in our interpretations.

A friend once observed that if you dig yourself a deep hole, and emerge partially, you are still in a deep hole. It will be a while before we are back on level ground.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2020 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit our terms and conditions page.

© Northern Trust

Read more commentaries by Northern Trust