summary

- The Jobs Data Doesn’t Add Up

- Yes, Brexit Is Still An Issue

- Frustration For Food Producers

Some dieters have experienced something called “sugar shock.” Certain weight loss plans recommend abstaining from any sweetened food for weeks at a time. When the dieter tries a dessert after the long break, the sweet taste feels overwhelming.

So it was with last week’s U.S. employment report. After a long series of record low economic reports and downward forecast revisions, it was sweet to see positive job creation and a decline in the unemployment rate. Once the shock wore off, we turned to digesting the results. Our initial impressions follow.

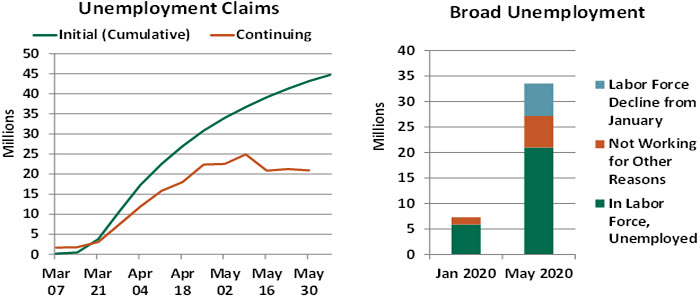

Dour expectations for the job situation had been driven, in part, by the weekly flood of initial claims for unemployment benefits. A total of 44 million initial claims have been filed since mid-March, equivalent to 28% of the labor force.

The unemployment rate is obviously not that high. The link between unemployment insurance claims and the unemployment rate is not straightforward. Claimants frustrated by processing delays (state unemployment systems have been overwhelmed) may have applied more than once, while others may have been found ineligible. The number of continuing claims, people actually receiving unemployment, stood at 20.9 million as of the week of May 25. This represents only about 13% of the labor force.

But this latter figure may be a low estimate of unemployment, because many states remain behind in their processing. A recent Bloomberg study estimated that state governments have yet to grant unemployment benefits to more than one-third of claimants.

Some who have filed for claims over the past three months may already be back at work. That was the source of the surprise. Through the early weeks of May, COVID-related restrictions were relaxed and businesses began to reopen. Consumers cautiously (and in some cases, carelessly) returned to shops, bars and restaurants. High-frequency indicators like airport security screenings and gasoline sales suggest the peak of the slowdown passed in April. The return to employment began earlier than anticipated.

“Good news is welcome, but employment remains deeply depressed.”

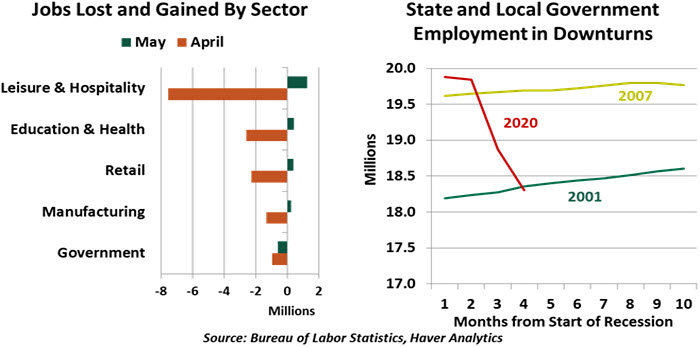

A view of the sectors that surprised most significantly in May confirms this hypothesis. Workers in retail, hospitality and healthcare led the re-hiring. These discretionary sectors slowed the most in the lockdown, and they have been the first to bounce back. This surge may count as an early win for the Paycheck Protection Program (PPP). Small businesses that received PPP loans needed to return to their pre-crisis staffing levels by June in order for their loans to be forgiven. While data specific to PPP borrowers is still forthcoming, it may help to explain some of the gains.

Less encouragingly, government employment saw a substantial decline last month. Most state and local budgets were thin entering the crisis, and the precipitous drop in sales and income tax revenue has damaged public finances. Many local governments have responded by cutting headcount with a severity not seen in past downturns. This comes just as demand for local government services is rising, especially amid a public health crisis and pockets of civil unrest. Support for state governments will need to be a priority in upcoming fiscal policy debates.

May’s unemployment rate, while improved, remains an understatement. The jobless rate emerges from a survey filled out by households; the response options can sometimes be confusing. There has been a surge of nearly five million workers who were reported as employed but absent from work for “other reasons.” Those in this category are not counted as unemployed.

Most of these respondents must be facing disruption due to COVID-19. Survey takers should have marked these workers as being on a temporary layoff, which would increase the unemployment rate by about 3%. This issue was also present in March and April, and the Bureau of Labor Statistics (BLS) made the discrepancy clear in their press release.

Further, more than six million people have left the labor force since the start of the year. This may also be a product of classification problems related to the survey, as many of these workers remain in need of employment. While the American unemployment rate fell at all levels last month, functional joblessness is still dangerously close to 20%.

We must acknowledge the complexity of performing a survey in a pandemic. In its past three employment reports, the BLS has included a special note of its difficulties collecting data. Its surveys require interaction between a survey taker and a respondent. Response rates are falling as more respondents work from home or are dealing with job losses.

“Temporary layoffs may become permanent job losses without more fiscal support.”

The primary focus of the recent employment report was on transient shifts, assessing the extent of temporary layoffs and their recovery. These passing movements take attention away from more troubling permanent shifts. The May report showed an increase to 2.3 million workers who reported that their job loss was permanent; in 2019, that figure averaged only 1.3 million. This is exactly the outcome that fiscal and monetary interventions aimed to prevent: permanent job losses due to business closures or reductions in force. In the Federal Open Market Committee press conference this week, Chair Jerome Powell shared his fear that “well into the millions of people may be out of work for some time.”

In sum, the May employment report was better, on almost all levels, than the previous edition. With continued easing of restrictions (and, hopefully, no material increase in coronavirus cases), payrolls should continue to increase. However, today’s unemployment rate of 13.3% is still decidedly poor, even as it understates the depth of the labor market retreat.

With some key worker support programs due to expire in the coming months, and PPP funding running out, the improvement seen in May could turn out to be temporary. Additional government support for those out of work will be required to prevent a bitter outcome.

It’s The Pits

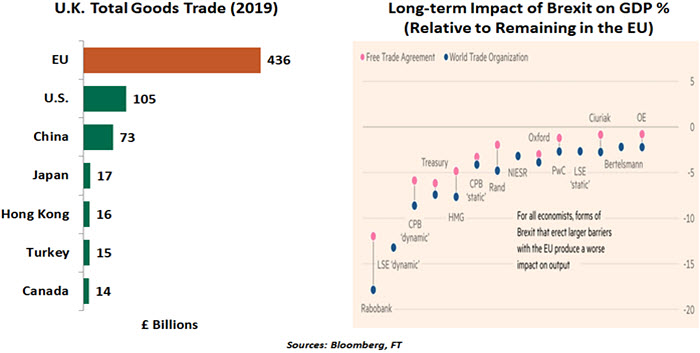

The law of holes states that when you are in hole, stop digging. The deeper the hole, the harder it is to climb out. The U.K. appears to be doing exactly the opposite by hardening its stance on Brexit, even as its economy gazes at an unprecedented contraction this year. Despite the shock to economic activity from the pandemic and growing calls from its constituents and businesses, the British government has so far ruled out an extension to the December 31, 2020 transition deadline.

Negotiations between the European Union (EU) and the U.K. stalled in recent weeks, with no real progress on crucial areas like labor, environmental and competitive standards. As a result, a no-trade deal Brexit looks quite plausible now.

The EU is the U.K.’s largest trading partner. The two sides remain far apart as they seek common ground on tariffs. The U.K. government has unveiled a new tariff regime called the U.K. Global Tariff, aimed at increasing its competitiveness. Under the regime, the U.K. would apply an average tariff of 5.7% on goods compared to EU’s 7.2%, with 47% of products attracting zero tariffs compared to 27% under the EU’s tariff rules. These differences will have to be closed if a new free trade deal is to emerge.

Without such a deal, the British farming industry, which accounts for two-thirds of British exports to the EU, will face tariffs and non-tariff barriers. The services sector, comprising 80% of the U.K. economy, will face disruptions. British manufacturers of goods like cars and pharmaceuticals will likely face new costs and significant disruptions to their just-in-time supply chains in Europe.

When one talks about the possibility of a disorderly Brexit, Northern Ireland cannot be overlooked. It would suffer a double setback from a no-deal outcome. Tariffs would be implemented on goods crossing from the rest of the U.K. to Northern Ireland, which is part of the U.K. Businesses could then reclaim these tariffs through a rebate system if the product remained in Northern Ireland without entering into the Republic of Ireland, which is part of the EU. Administration of this tariff would be as complicated as it sounds.

Beyond Europe, the U.K. is also faced with having to secure free trade arrangements with major economies like the U.S. and Japan. It is already in talks with the U.S. and others, but the British government is driving a hard bargain. The first major free trade agreement they sign will likely set the tone for others.

“Causing a self-inflicted injury when you are already wounded isn’t a great idea.”

The Bank of England has asked British banks to prepare for a no-deal outcome. Apart from the risk of deteriorating credit, U.K. financial companies could lose their ability to operate fluidly in Europe. Again, insult would be added to injury.

In the absence of new trade agreements, British trade would be governed by World Trade Organization (WTO) rules, which would leave British products vulnerable to escalating tariffs from other countries. Losing trade competitiveness would be exceptionally hard on businesses, many of which are struggling to pull through the impact of the pandemic. And a no-deal scenario would initiate the laborious and costly task of re-aligning supply chains.

As things stand, the U.K. has the following options: seek an extension of the transition deadline, rush to get a deal by October, or prepare for no-deal. Recently, a Financial Times writer quipped, “only a fool would put a probability on whether the EU and the U.K. will agree a trade deal.” While we don’t entirely disagree with that viewpoint, we are still hopeful that rational economic minds will be applied to avoid the worst-case outcome.

Brexiteers are arguing that the cost of leaving the EU without a trade deal will be obscured by the unprecedented economic damage inflicted by COVID-19. That is like saying that you are less likely to notice a broken toe while undergoing dental surgery. Once the pandemic policy anesthetic wears off, the economic pain that the U.K. would face in a no-deal scenario will be unbearable.

Bitter Harvest

During the first weeks of the pandemic, the frenzy at grocery stores was remarkable. It wasn’t just paper products and sanitizer that were absent from the shelves; pasta aisles and freezer cases were also picked clean. It was clear that families were dining at home more often.

At the same time, stories emerged of farmers ditching crops in their fields to rot. How can we simultaneously have a glut and a scarcity of food? The answer lies in logistics…and eating habits.

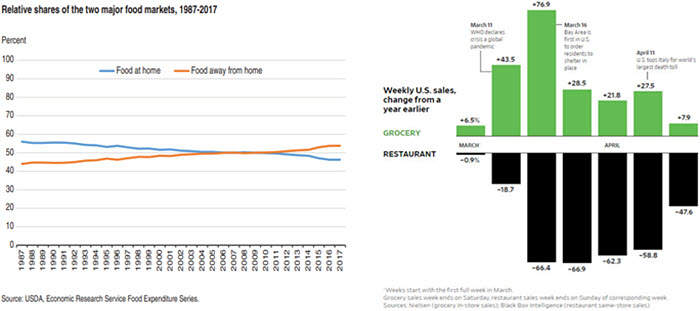

Before social distancing became the term of the year, the average American ate out almost six times per week. Spending on meals eaten away from home eclipsed spending on home cooking about a decade ago, and the gap had been growing. The pandemic threw almost everyone back into their kitchens, an environment that can be intimidating. Basic cooking videos have been popular quarantine viewing.

While there is some humor to be found in recent stories of novices burning dinner, there was nothing funny about the disruption visited upon the food service industry. Households consume many more prepared foods and use fewer fresh ingredients than restaurants. This created a mismatch between what was ready for harvest and what was being eaten.

“We eat different things at home than we do at restaurants.”

Restaurants and groceries have very different supply chains, so the cook-at-home trend threw these configurations into chaos. There simply wasn’t enough time or logistical bandwidth to send fresh food to processors instead of professional kitchens, resulting in a huge spike in prices at the grocery. There also wasn’t time to ship perishable items economically to the many food banks that have seen heavy traffic over the last two months.

And so we witnessed the sad sight of vegetables being plowed under and milk being poured down the drain at a time that some citizens were struggling to feed their families. The juxtaposition of bounty and privation will be a lasting image of the spring.

Over time, a new equilibrium will emerge. Restaurants have slowly begun to reopen, albeit with significantly reduced capacity. And some new home chefs are discovering the joys of cooking from scratch. But we are unlikely to return to our former eating patterns anytime soon. The pandemic may have a lasting impact on the food industry, and on our diets.

© Mauldin Economics

www.mauldineconomics.com

© Northern Trust

Read more commentaries by Northern Trust