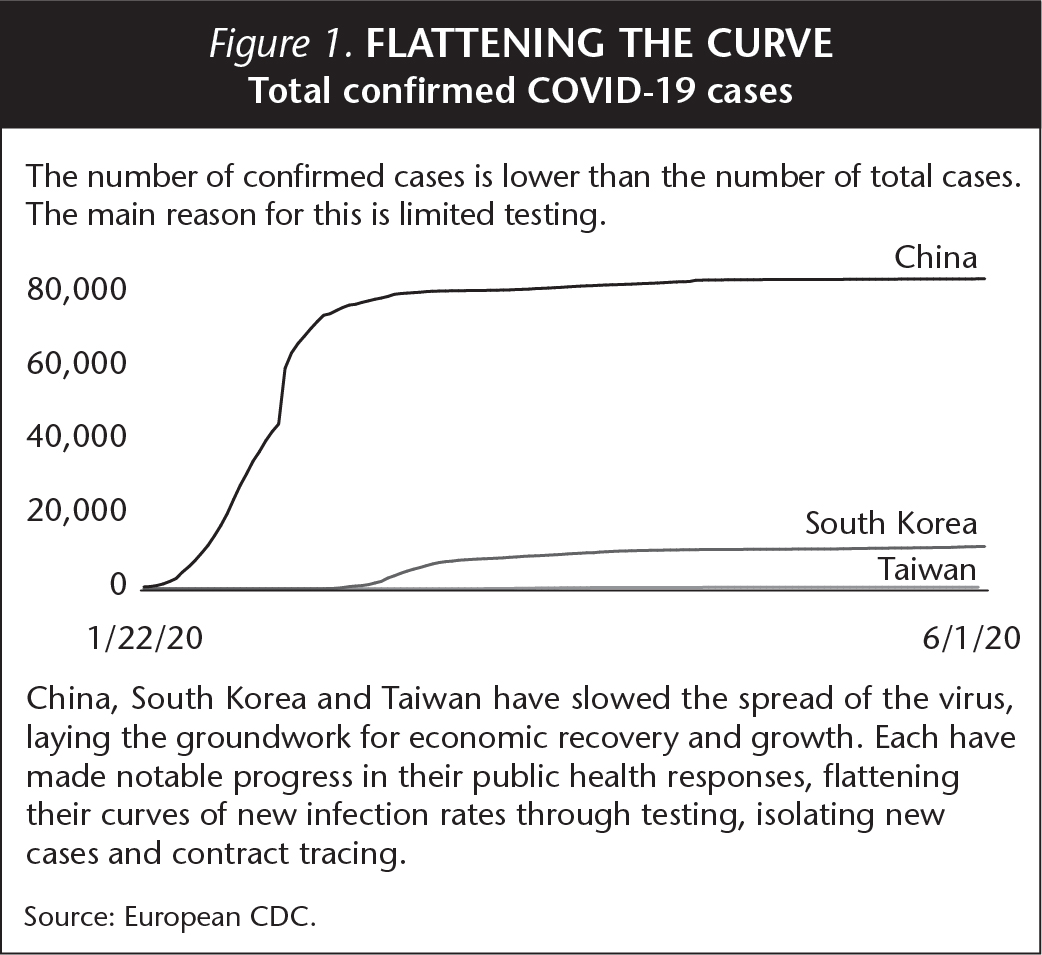

As the global economy slows, we remain optimistic about the long-term growth potential of Chinese equities. From a public health perspective, China has flattened its curve of new cases COVID-19. Fiscal and monetary stimulus, while incremental, remains supportive. Interest rates remain positive, giving China's central bank room to maneuver. Turning to the private sector, many innovative sectors within China continue to experience rapid growth. Reflecting both the health of China's economy and a faster resumption of daily activities, local sentiment has been more optimistic than global sentiment. In this roundtable, Matthews Asia portfolio managers Andrew Mattock, CFA, Winnie Chwang, Tiffany Hsiao, CFA, and Michael Oh, CFA, discuss their outlook for China and trends they are following.

Q. What was the initial impact of the global pandemic on China's markets?

Andrew Mattock: When the coronavirus emerged in China, Chinese equities experienced a brief market correction, following by a rapid rebound in stock prices. China was the first country to experience broad spread of the corona virus and the first to begin its economic recovery. Looking back to January, stocks fell as investors feared fallout from the virus. A longer than normal incubation period for the virus combined with the mass people movement associated with Chinese New Year complicated the control of the virus early on. Chinese authorities limited internal travel and controlled its borders while working with world health organizations to control the outbreak. In February, a slowdown in the percentage rise in new virus cases, along with comprehensive policy, action helped stabilize sentiment within Chinese markets, especially A-shares. In April, Chinese equity prices rebounded as the economy began to reopen. The pandemic accelerated some global trends but China was already ahead of the game in many respects. For example, many businesses globally are shifting to digital payments over cash to reduce virus transmission amid the pandemic. In China, cash has been virtually nonexistent for a while, with consumers across all income brackets paying for purchases via mobile phones and digital wallets.

Q. Year to date, both U.S. and Chinese equity markets have shown considerable resilience. What accounts for the relative strength of Chinese equity prices?

Winnie Chwang: Over the past decade, China's equity markets have undergone a significant transformation, deepening and expanding. Consider the example of the health care sector. There was a time when we could only invest in a handful of health care product distributors. Now we can invest in a broad range of different types of health care companies. Increasingly, innovative drug makers, contract research organizations (CROs) and high-end medical equipment manufacturers and suppliers are also represented in our investment opportunity set. As China's economy has changed and evolved, we find the quality of earnings streams coming out of publicly listed company improving. We also find that sentiment towards Chinese equity is generally more positive because business activity has resumed more quickly in China than in other parts of the world.

Q. Can Chinese equities continue to generate attractive growth amid a slowing macro environment?

Michael Oh: In slower growth and recessionary environments, innovation often continues strong. New players have the opportunity to invent entirely new business paradigms, while some incumbents may continue to gain market share. Many innovative companies are thriving by competing on intellectual property, brand loyalty and providing superior products and services. The pandemic is speeding up consumer behavior changes in China, as well as developing parts of Asia. Notably, companies with strong organic structural growth tailwinds behind them have performed well year to date. We believe that the same type of companies have the potential to continue to outperform coming out of the crisis, and active security selection is key during periods of disruption and change.

Q. What is the impact of the pandemic on China's small companies?

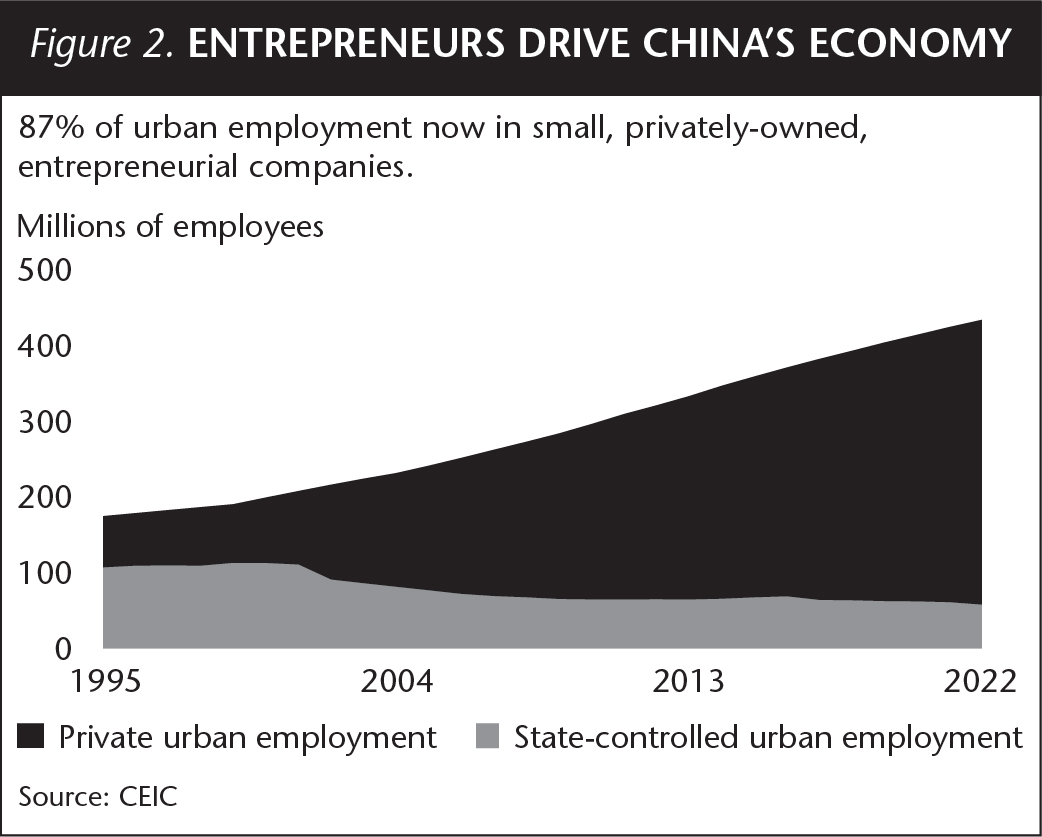

Tiffany Hsiao: We believe the pandemic has created tailwinds for China's small companies competing on innovation. For example, facing rising wages and an aging work force, China's economy continues to require increased labor productivity to sustain its growth. Software, AI and automation—many of the same forces boosting productivity in the U.S. and Japan—are also in play in China. Small companies are powering these productivity gains. Small businesses make up the bulk of companies of China's private sector today, with entrepreneurs at the helm. Small- and medium-size businesses (SMEs) now make up over 87% of urban employment in China. Yet only about 2% of the MSCI China Index consists of small businesses. For global investors, in my view this means that China small companies remain an untapped universe that can offer genuine diversification benefits.

Q. Where are you finding opportunity amid market dislocations?

Andrew Mattock: We expect the pandemic may benefit companies that enjoy dominant positions, strong brand equity and participate in industries with significant barriers to entry. Companies with stronger business models and healthier balance sheets are more likely to weather the crisis, in our view. The crisis also presents an opportunity for stronger companies to weed out less effective competitors, enabling them to gain market share. Online shopping continues to be a growth sector. The pandemic is speeding up adoption of online shopping, but growth in the sector is fundamentally just a continuation of a longer trend. E-commerce platforms continue to broaden their reach into less developed urban centers, often referred to as lower tier cities, tapping into the next large cohort of consumers entering the middle class. We also expect to see pent-up demand for domestic travel during China's economic recovery phase. Following the initial two months of lockdowns and travel restrictions, people want to see family again and enjoy vacations. We also expect to see an increase in business travel activity.

Tiffany Hsiao: The pandemic has exploded the need for B2B software and online services in China. With over 40 million SMEs already migrating to the cloud, demand for enterprise software is accelerating. When we conduct bottom-up research on companies in innovative driven sectors, people tend to be a company's most important assets. Getting better productivity from each worker requires better software, the ability to customize software to the needs of end users and adoption of subscription-based purchasing models—all of which creates stickier client relationships and revenue. Over the past two decades, many of China's most promising students and coders went into the Internet space, creating a big supply and demand imbalance for software. Today, there are few top-quality softwarecompanies, creating a sector still in its infancy benefiting from high demand.

Michael Oh: The pandemic is also pulling more consumers into using online services. Even consumers who were not likely to use online services before, such as older generations, are engaging in faster adoption of various online services. We see the trend as especially likely to benefit online gaming companies, with many consumers are playing online games for the first time. Gaming companies and entertainment companies always face competition from new entrants, but strength of user communities can create competitive moats. Education is another consumer services area that has done well amid the pandemic. We expect that parents will continue to invest in their children's education after the pandemic. Companies with clear secular tailwinds and long growth duration seem to enjoy greater immunity in this particular downturn.

Tiffany Hsiao: Biotech is another innovation-driven sector where we see tremendous growth opportunities for China's small companies. Every year, doctors diagnose more than 4 million new cancer patients in China. China scientists have a huge opportunity to come up with innovative treatments for their unique patient community, especially as cancer treatments become increasingly customized and based on a patient's personal DNA. Developing therapies, drugs and devices that work better on Chinese patients presents an opportunity for Chinese biotech companies with a long runway for growth.

Michael Oh: Many companies in the health care sector have been obvious beneficiaries of the pandemic. China, as well as many other countries in Asia, will need to upgrade their health care systems and infrastructure. Against this backdrop, medical equipment companies and innovative drug companies have performed quite well. In addition to the health care issues related to the pandemic, China also needs to continue to address the chronic health care issues associated with its aging population. Cardiovascular diseases and treatments, diabetes and weight management, lung and other kinds of cancers all require homegrown medical solutions.

Q. What risks should investors keep in mind in today's markets?

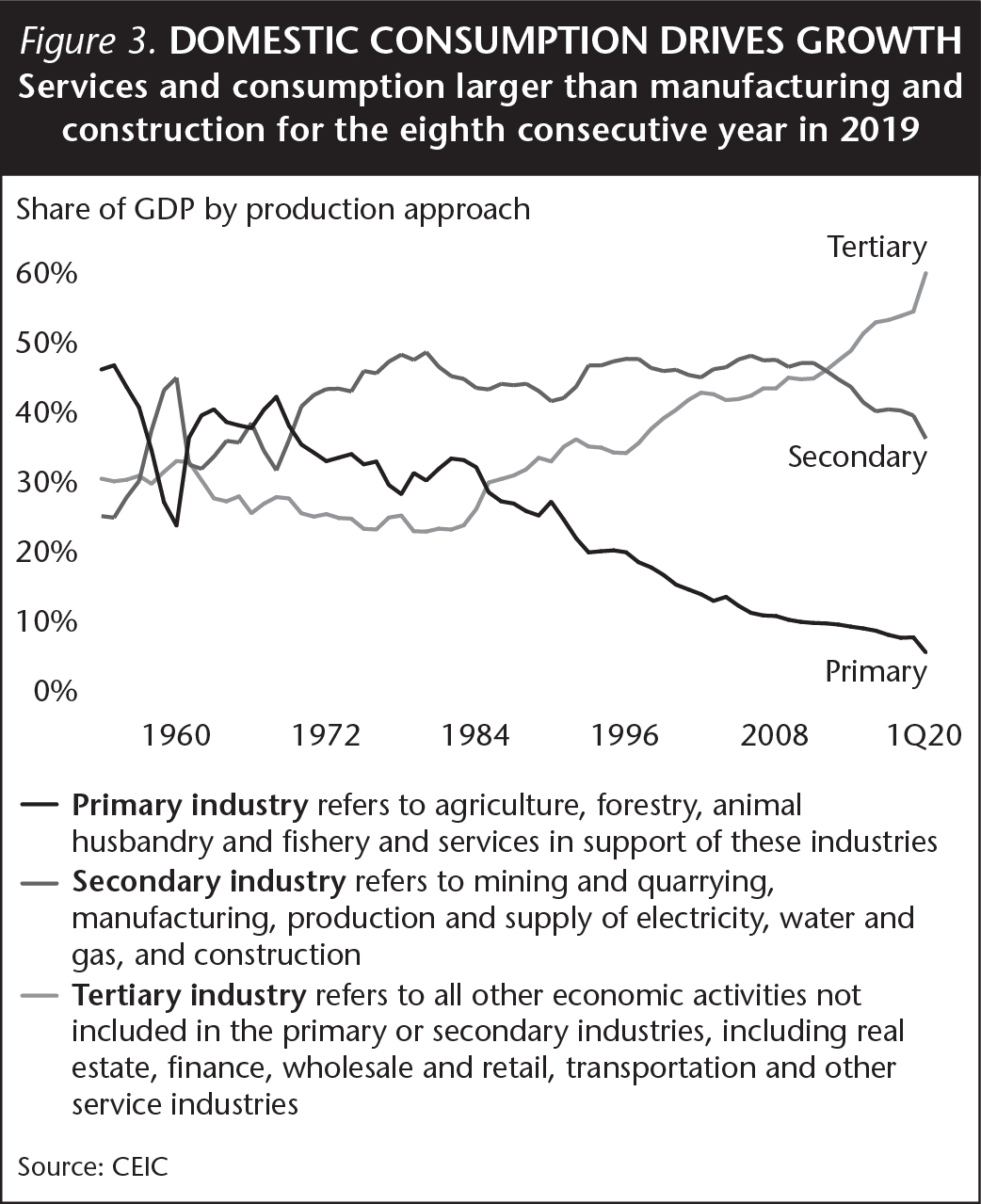

Winnie Chwang: Near-term risks to China's economy remain. While domestic consumption primarily drives China's economy, China is also part of the global economy and maintains a global export presence. Thus, the pace of global recovery affects China's growth in the near term may pose a risk to shorter term economic developments in the country. Taking a longer-term view, we remain optimistic about China's ability to grow its economy over the next three to five years, especially in those sectors driven by services and innovation.

Q. What risks should investors keep in mind in today's markets?

Winnie Chwang: Near-term risks to China's economy remain. While domestic consumption primarily drives China's economy, China is also part of the global economy and maintains a global export presence. Thus, the pace of global recovery affects China's growth in the near term may pose a risk to shorter term economic developments in the country. Taking a longer-term view, we remain optimistic about China's ability to grow its economy over the next three to five years, especially in those sectors driven by services and innovation.

Tiffany Hsiao: For investors who may be considering investing in China small companies, it is important to understand both the risks and opportunities. Small businesses in China tend to serve domestic consumers, which provides a degree of insulation from external trade tensions. At the same time, any slowdown in China's domestic economy would likely trickle down to China's small companies. On balance, though, we remain optimistic about the long-term growth of China's small companies. Management teams of small companies in China in our view tend to be good capital allocators because many of these business grew up starved of capital. Entrepreneurs tend to start with their own hard-earned savings and design businesses that are asset light. Small companies also gravitate toward industries where there is a long runway for growth and generate higher return on capital. We believe the keys to unlocking the growth potential of China's small companies are investing with a long-term horizon, focusing on market leaders and maintaining a carefully curated, concentrated portfolio. As the global economy slows, we believe the universe of China's small companies represents the potential for attractive, uncorrelated growth.

Michael Oh: We could continue to see potential for additional volatility over the short term. Whether investing in China-specific strategies or regional strategies that include significant exposure to China, I believe it is important to have a long-term time horizon.

Q. What makes you optimistic about the investment opportunity set in China today?

Michael Oh: With a focus on the Asian consumer, innovative companies in China are capturing the buying power of a new, powerful middle class. These companies may offer global investors seeking diversification with exposures that are genuinely differentiated. Better companies with quality management teams and innovative business models tend to come out stronger. Looking ahead, we will continue to look for the most attractive growth ideas for long-term investors.

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.

© Matthews Asia

© Matthews Asia

Read more commentaries by Matthews Asia