Value (investing) is dead. Long live value investing. Such certainly seems to be the mantra as investors continue to pile into growth stocks while rationalizing valuations using methodologies which historically have not worked well.

However, as with all things when it comes to investing, be careful when declaring any asset or investment strategy dead. Such was a point made recently by Research Affiliates. The media has a long history of declaring sectors, markets, or strategies “dead” based on past performance. From August 1979 — when Business Week declared the “death of equities” — to July 2019, when the Financial Times questioned whether emerging markets investments make sense anymore.

In most cases, those were pivotal periods when what was believed to be “dead,” came roaring back to life.

Looks Like 1999

In late 1999, the media suggested that “investing like Warren Buffett was the same as driving ‘Dad’s ole’ Pontiac.” The suggestion, of course, was that “value” investing was no longer a viable investment strategy in the new “dot.com” economy where “growth” was all that mattered. After all, in the “new world,” it was indeed “different this time.”

Less than a year later, investors wished they had adhered to Warren Buffett’s buying value strategy as the “Dot.com dream” emerged as a nightmare for many unwitting individuals.

However, it wasn’t just stocks either. In 2007, individuals were chasing the “momentum” in the real estate market. Individuals left their jobs to pursue riches in housing. They were willing to “pay any price” under the assumption they would be able to sell higher. Of course, it was not long after Ben Bernanke uttered the words “the subprime market is contained,” the dreams of riches evaporated like a “morning mist.”

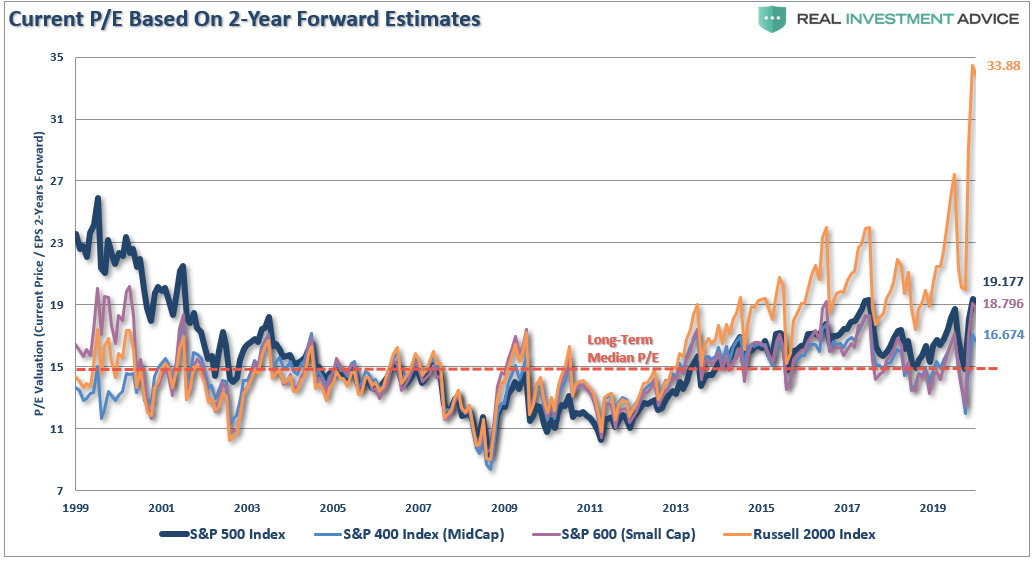

In 2020, investors are again chasing “growth at any price” and rationalizing overpaying for growth. As we discussed just recently:

“Such makes the mantra of using 24-month estimates to justify paying exceedingly high valuations today, even riskier.”

20/20 In 2020

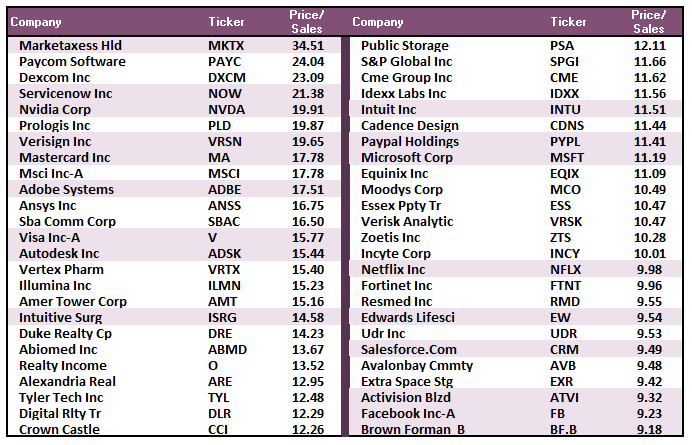

“Earnings per share” have been heavily manipulated over the last decade through a variety of gimmicks from “cookie jarring reserves,” to massive “share buybacks.” However, “revenue” is a different matter.

Unfortunately, investors are vastly overpaying for sales as well. Scott McNeely discussed the irrationality of paying 10x sales for a company, then CEO of Sun Microsystems, in 1999 in a Bloomberg interview. To wit:

“At 10-times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10-straight years in dividends. That assumes I can get that by my shareholders. It also assumes I have zero cost of goods sold, which is very hard for a computer company.

That assumes zero expenses, which is hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that expects you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10-years, I can maintain the current revenue run rate.

Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those underlying assumptions are? You don’t need any transparency. You don’t need any footnotes.

What were you thinking?”

Many of the most popular “growth” stocks fit this insanity.

A History Of Value

In hindsight, we know the dangers of overpaying for the “estimated growth” of Dot.com companies. In 2020, investors are doing it again, expecting a different result.

As Warren Buffett once quipped, “price is what you pay, value is what you get.”

Throughout market history, investors have repeatedly abandoned this simple principle during periods where bull market advances seemed to defy logic. Ultimately, those investors paid a dear price for their speculation as the reality of “overpaying for value” led to poor financial outcomes.

As we have noted in a series of articles posted at RIAPRO.net we believe the market is on the precipice of another monumental shift from “growth” to “value.” As always, such a transition will blindside most investors.

Value vs. Growth

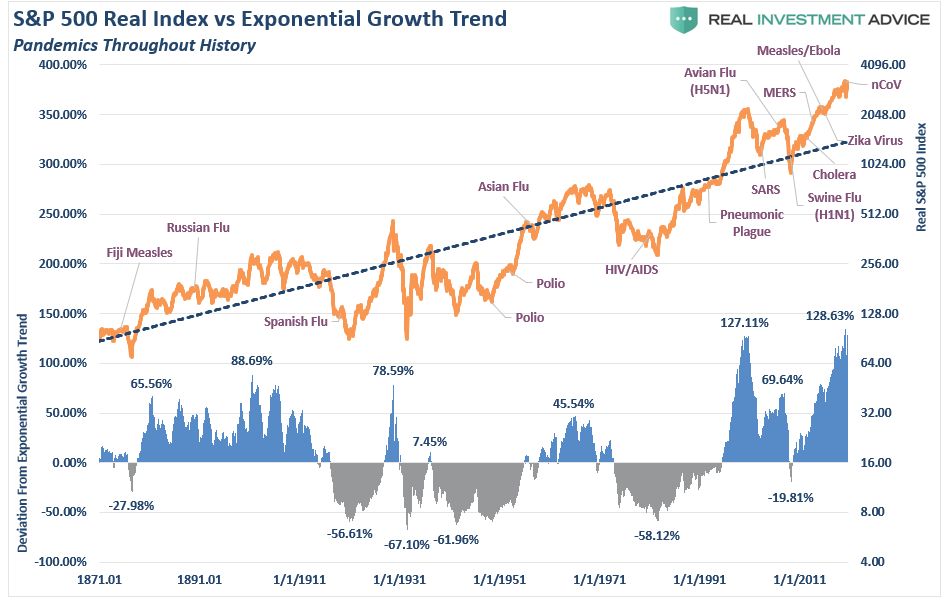

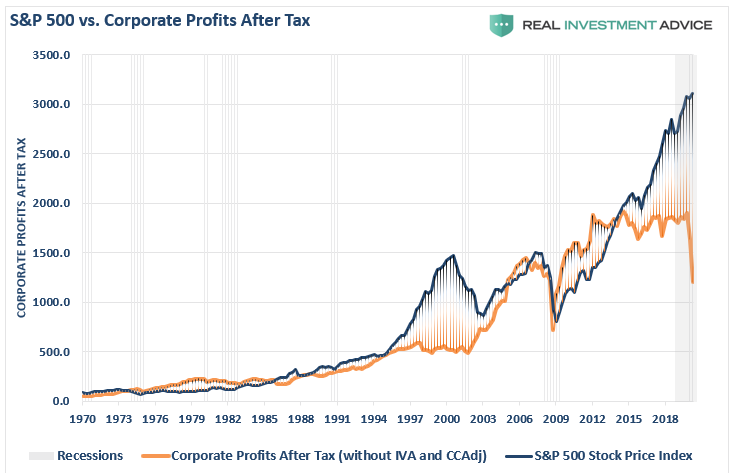

The market’s surge higher since the financial crisis, driven by massive fiscal and monetary policies, has been nothing short of extraordinary. Currently, the S&P 500 is trading at the highest deviation from its long-term exponential growth trend in history.

Such is occurring at a time where market prices are advancing. At the same time, corporate profitability has remained flat for the majority of the decade. The gap is even more problematic given the recent plunge in corporate profits due to the economic shutdown.

However, this is the very consequence, dangerous at it may be, of the unparalleled use of monetary policy to push asset prices higher. In this case, the shift to “growth,” or should I say “speculative momentum,” over “value.” That shift was a function of corporations’ misallocation of capital. By shunning future growth for the short-term incentive of “share repurchases,”they eroded shareholder value.

Stunning Underperformance

As Michael Lebowitz, CFA previously noted:

“As a result of these behaviors, we have witnessed a divergence in what has historically spelled success for investors. Stronger companies with predictable income generation and solid balance sheets have grossly underperformed companies with unreliable earnings and over-burdened balance sheets. The prospect of majestic future growth has trumped dependable growth. Companies with little to no income and massive debts have been the winners.”

Such also occurred in late 1999 as companies with no earnings, no revenue, and no real growth strategy exploded higher in a speculative fueled buying frenzy.

This underperformance of “value” relative to “growth” is not unique. What is unusual is the current duration and magnitude of that underperformance. To say unprecedented is almost an understatement.

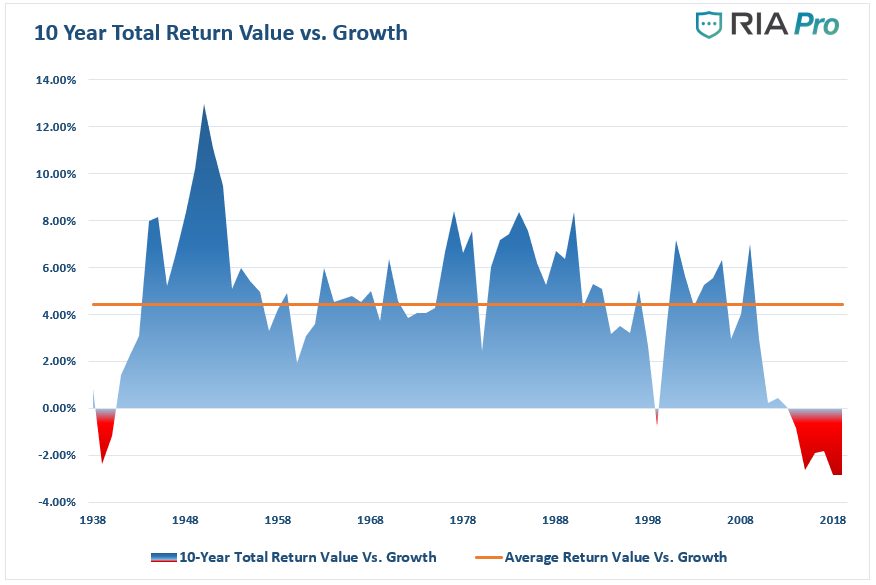

10-Year Total-Return Failure

The graph below charts ten-year annualized total returns (dividends included) for value stocks versus growth stocks. The most recent data point representing 2019, covering the years 2009 through 201-, stands at negative 2.86%. Such indicates value stocks have underperformed growth stocks by 2.86% on average in each of the last ten years.

The data for this analysis comes from Kenneth French and Dartmouth University.

There are two critical takeaways from the graph above:

Over the last 90 years, value stocks have outperformed growth stocks by an average of 4.44% per year (orange line).

There have only been eight ten-year periods over the last 90 years (total of 90 ten-year periods) when value stocks underperformed growth stocks. Two of these occurred during the Great Depression and one spanned the 1990s leading into the Tech bust of 2001. The other five are recent, representing the years 2014 through 2019.

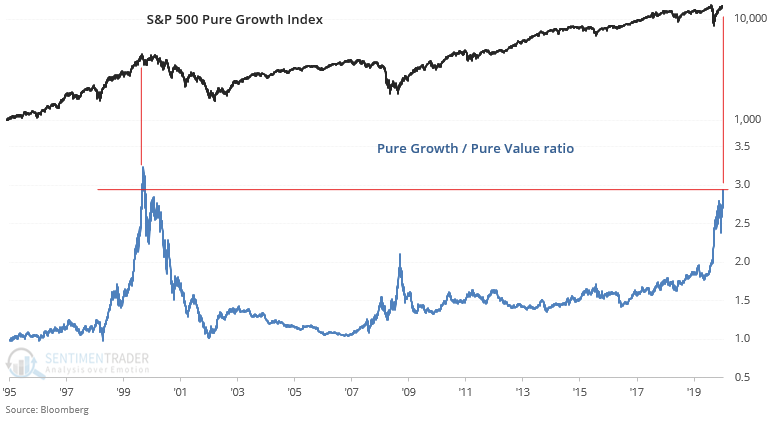

Mirror Opposites

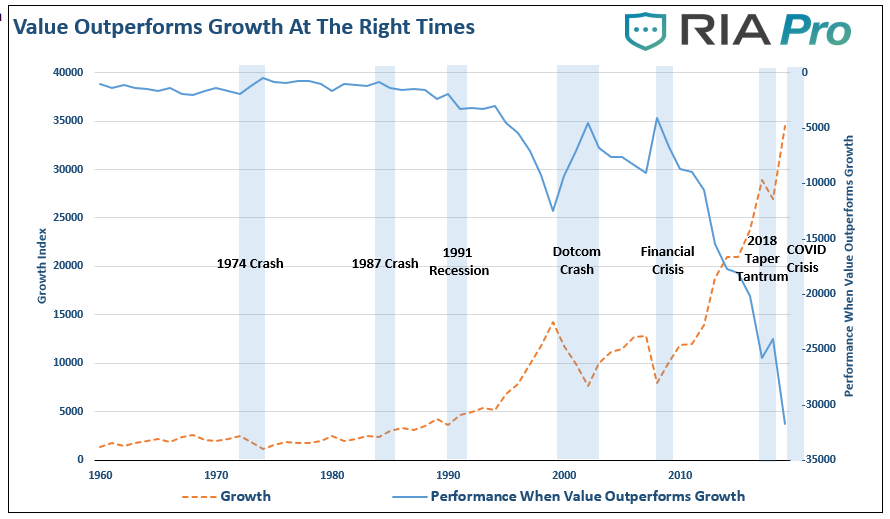

The chart shows the difference in the performance of the “value vs growth” index. That index is compared to a pure growth index with each based on a $100 investment. While value investing always provides consistent returns, there are times when growth outperforms value. The periods when “value investing” has the greatest outperformance, as noted by the “blue shaded” areas, is notable.

The question is what are the causes of this underperformance.

“The Fama–French value factor, and value investing in general, has suffered an extraordinarily long 13.3 years of underperformance relative to the growth investing style. The current drawdown has been by far the longest as well as the largest since July 1963.

An investment strategy, style, or factor can suffer a period of underperformance for many reasons.

First, the style may have been a product of data mining, only working during its backtest because of overfitting.

Second, structural changes in the market could render the factor newly irrelevant.

Third, the trade can get crowded, leading to distorted prices and low or negative expected returns.

Fourth, recent performance may disappoint because the style or factor is becoming cheaper as it plumbs new lows in relative valuation.

Finally, flagging performance might be a result of a left-tail outlier or pure bad luck.

If the first three reasons imply the style no longer works, and will not likely benefit investors in the future, the last two reasons have no such implications.

With today’s value vs. growth valuation gap at an extreme (the 100th percentile of historical relative valuations), it sets the stage for a potentially historic outperformance of value relative to growth over the coming decade.”

When things ultimately go “pear-shaped,” the return to value tends to be a swift event. For investors it is crucial to grasp what decades of investment experience tells us about the future. When the cycle turns, we have little doubt the value-growth relationship will revert to its long-term mean.

History Doesn’t Repeat

“History Doesn’t Repeat Itself, but It Often Rhymes” – Mark Twain.

Such is particularly true when it comes to financial markets. It is not a question if the rotation to value will occur, it is only a question of when.

However, this is the risk investors are currently taking in the market.

Ultimately, it is a pure bet on prices going higher than determining if the price paid for those assets is selling at a discount to fair value.

Along with David Dodd, Benjamin Graham attempted a precise definition of investing and speculation in their seminal work Security Analysis (1934).

“An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.”

There is also an essential passage in Graham’s The Intelligent Investor:

“The distinction between investment and speculation in common stocks has always been a useful one. Its disappearance is a cause for concern. We have often said that Wall Street, as an institution, would be well advised to reinstate this distinction and to emphasize it in all its dealings with the public. Otherwise, the stock exchanges may someday be blamed for heavy speculative losses, which those who suffered them had not been properly warned against.”

Be Careful Declaring Value Dead

While the current market advance seems to be unstoppable, investors’ attitude is seen at every prior market in history. As Howard Marks once stated:

“Rule No. 1: Most things will prove to be cyclical.

Rule No. 2: Some of the most exceptional opportunities for gain and loss come when other people forget Rule No. 1.”

The realization that nothing lasts forever is crucial to long term investing. To “buy low,” one must have first “sold high.” Understanding that all things are cyclical suggests that after significant price increases, investments become more prone to declines than further advances.

The rotation from “growth” to “value” is inevitable. It will occur against a backdrop of devastation for the majority of investors quietly lulled into the extreme sense of complacency years of monetary interventions have provided.

As Research Affiliates concludes:

“Overall, relative valuations are in the far tail of the historical distribution. If, as history suggests, there is any tendency for mean reversion, the expected future returns for value are elevated by almost any definition.”

The only question is whether you will be the buyer of “value” when everyone else is selling “growth?”

Real Investment Advice is powered by RIA Advisors, an investment advisory firm located in Houston, Texas with more than $800 million under management. As a team of certified and experienced professionals, we seek to provide our clients with educational services and the necessary information and tools to educate you in the field of finance, investing and economics. To this end, you can use the Real Investment Advice Platform to avail yourself of various video, audio and proprietary collections of information at your leisure to learn and gather the necessary information that you may need in the fields of investment news, investment opinion, financial news, financial opinion, economic news and economic opinion, finance, investing and economics. Utilizing the functionality and tools provided by Real Investment Advice, you can access this information in a variety of ways, including via video and audio programming, audio and visual media content streaming services, downloadable audio-visual media, uploaded, posted or tagged third-party videos, receiving or viewing audio and video clips, blogs, podcasts, and YouTube videos, all of which are accessible on the Real Investment Advice media platform and/or various Internet and communications links that are accessible via the Real Investment Advice Platform and allow for the broadcasting, transmission and streaming of the information and audio-visual content to your media devices and other communications platforms for your viewing and listening pleasure. All of these tools and sources of information are made available to you so that you can utilize the same to make the right financial, economic and investment decisions.