U.S. Economic Outlook, August 2020: Healing

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe outlook for the economy and the outlook for COVID-19 are fusing. As long as the virus is spreading, the recovery will be incomplete and uneven. Many sectors, like restaurants, airlines and sports leagues, will remain disrupted until the virus is in the past. Those parts of the economy that have reopened are functioning at the mercy of public health policy, disrupted value chains and consumers’ willingness to leave their homes.

But an uneven recovery is still a recovery. The second quarter brought us economic readings that broke records for the speed and severity of their declines, but that is in the past. Even a limited return to normal activity will bring high growth readings in the near term: quarter-over-quarter growth is poised to show significant improvement from a depressed base. However, a full recovery will take time.

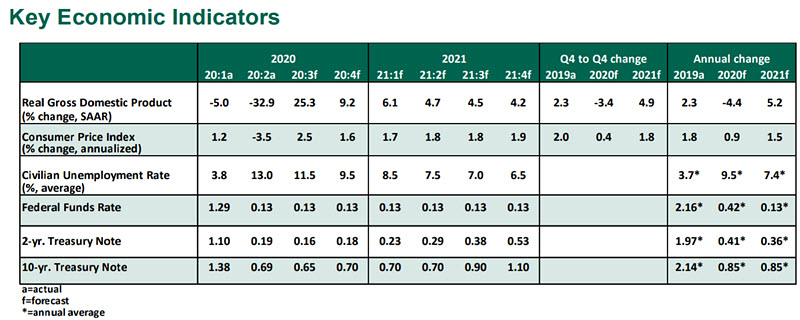

Key Economic Indicators

Influences on the Forecast

- U.S. economic activity declined at an annualized rate of 32.9% in the second quarter, translating into a simple loss of 9.5% quarter-over-quarter. Though such a large reading is shocking, it was expected. In the midst of a global pandemic, most other developed markets reported losses of a similar (or larger) magnitude. The American economy is functioning at about 90% of its prior peak; recovering that last 10% of output will be slow going.

- Recovery from COVID-19 remains incomplete. Most regions that experienced the worst outbreaks earlier in 2020 have avoided resurgence, but the virus continues to spread elsewhere. The recent spate of infections, such as in Texas, California and Florida, appears to have peaked. A sustained recovery will require vigilance. Nearly all states have some business restrictions in force, typically focused on bars, restaurants, nightclubs and concert venues.

- The unemployment rate continued to decline from its peak of 14.7% in April to 10.2% in July. Past cycle peaks were 10.8% in 1982 and 10.0% in 2009; while the July reading is high, it has at least returned to the range of past precedent. The recovery will continue at a slower rate from here: the boost from reopening has passed, and jobs lost in the most severely affected sectors will take the longest to return.

- After acting decisively to support the economy in March, Congress has failed to agree on a subsequent round of spending. Key economic supports like the $600 supplement to unemployment insurance payouts and a moratorium on evictions were allowed to expire at the end of July. Presidential executive orders to continue certain protections are not likely to be very effective; there remains a need for a more comprehensive legislative response.

- Since the crisis took hold, the saving rate has been elevated. Saving constituted 19.0% of disposable income in June after peaking at 33.5% in April. (The saving rate hovered around 7% before the pandemic hit.) Persistently elevated saving suggests consumers are braced for stressful conditions ahead.

- At its July meeting, the Federal Open Market Committee modified its routine statement to include the phrase: “the path of the economy will depend significantly on the course of the virus.” We regard this statement as self-evident, but its inclusion is significant as an indicator of how the Fed will gauge economic progress. The Fed has extended its temporary crisis response programs, such as its liquidity facilities for money market funds and short-term commercial paper, through the end of the year.

- Large-scale fiscal spending and monetary interventions stoked fear of inflation, but it has not yet materialized. Indicators like the consumer price index (CPI) and personal consumption expenditure (PCE) deflator each had at least one negative month-over-month reading in the second quarter. They remain low, with CPI growing 0.6% and the core PCE deflator growing 0.9% year-over-year in June.

- Low interest rates, limited housing supply and a movement toward working from home have buoyed the residential real estate market. The federal forbearance initiative should prevent a repeat of the correction and wave of foreclosures seen in the 2008-09 global financial crisis.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All