SUMMARY

- Inflation: More or Less?

- EU Seeking to Create National Champions?

- More Unemployment Than Meets The Eye

Five months into the COVID-19 crisis, I still venture out only occasionally. The local pool has reopened, allowing me to swim laps a couple of times each week. I’ll make the occasional trip to the home improvement store, to address a long list of repair and gardening projects. On Saturday night, we’ll take out food from a local restaurant, in an effort to keep our favorite eateries in business.

The biggest thrill I have each week is my Saturday trip to the grocery store. What used to be routine has become exhilarating: the freedom of being out, interacting with other people, and enjoying the colorful arrays at the market provides the lion’s share of my week’s excitement. I traverse each and every aisle slowly, and I always end up purchasing more than I need.

I have noticed that food prices seem quite a bit higher than they used to be. That is understandable; as more people are eating at home more often with restaurants restricted, supply chains have struggled to adapt. But I do not understand the frequent concerns I hear among investors about the risk of inflation. If anything, the pandemic will push the price level in the opposite direction.

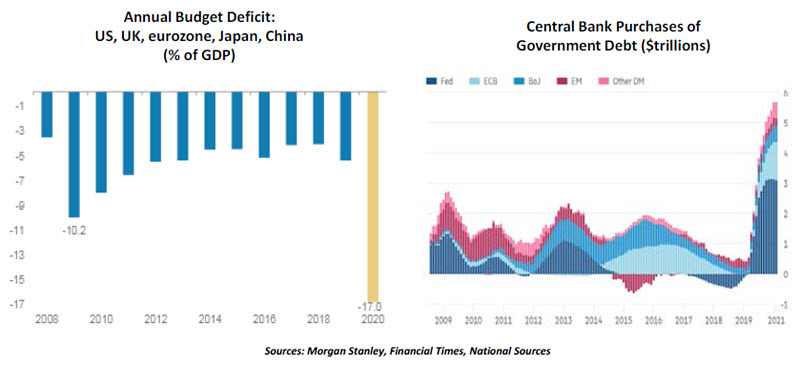

Today’s inflation fears stem from the immense amount of policy support that has been implemented around the world in an effort to counteract the economic consequences of the pandemic. Deficits and debt have surged, and central banks have run the virtual printing presses to help finance the effort. This combination, which some have likened to Modern Monetary Theory, can be a precursor to higher inflation. Concern over this outcome led the price of gold to over $2,000 per ounce recently, an all-time high.

But as we noted earlier this month, rapid increases in the money supply are not translating into an excess of credit or demand. A majority of the new reserves remains on bank balance sheets, as lenders exercise care in extending credit during these uncertain times. Bank regulators have encouraged financial companies to conserve capital, putting a further brake on credit creation.

Relief distributed directly to consumers in the form of stipends or unemployment support has kept spending from slumping. But households in many countries have increased their saving rates significantly in preparation for potential financial challenges ahead. The expiration of government support programs will limit consumption and entrench a conservative mind-set.

After strong initial gains as reopening commenced, high-frequency data suggests economic growth has slowed considerably. Renewed outbreaks have forced the restoration of restrictions in a number of countries; this kind of stop/start pattern will likely persist into next year. Commerce is therefore likely to remain impaired for some time to come, which will keep unemployment elevated.

“Powerful secular forces have kept inflation below targeted levels.”

It has been gratifying to see unemployment rates fall from their peaks. But levels of joblessness remain much higher than they were at the depth of the last recession. (Europe’s unemployment rates have been stable, but only because those who would otherwise be laid off are kept on the payrolls and receive government support to offset salary reductions.). There is immense slack in labor markets, making it unlikely that wages will start to grow more rapidly.

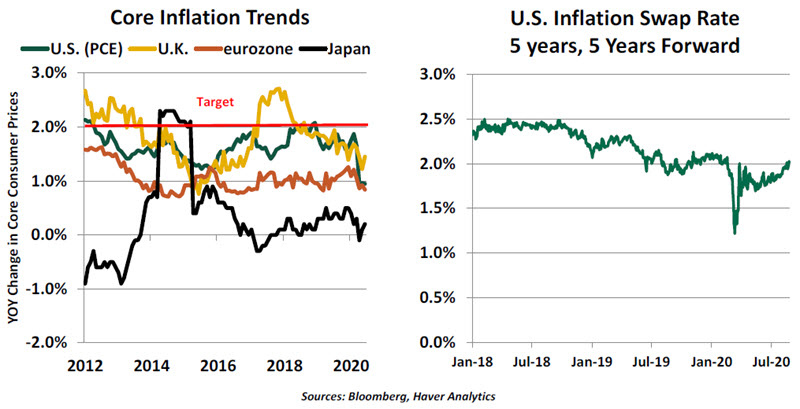

Prior to the onset of COVID-19, the world’s major economies were struggling mightily to get inflation up to targeted levels. Since the beginning of the pandemic, price levels in developed countries have progressed even more slowly. Inflation expectations dropped suddenly earlier this quarter when oil prices slumped. (The two are closely correlated.). Since then, expectations have normalized at levels that remain about the same as they were a year ago.

Last year, we enumerated the top reasons that inflation remained low. A series of secular forces has been bearing down on prices, e-commerce and process automation among them. As we wrote in our piece on Life After COVID, the pandemic will likely accelerate these trends.

Some will counter with the observation that globalization, which has been in retreat for the past several years, may devolve more rapidly in the years ahead. Issues of economic security are leading companies and countries to keep production closer to home. Altering supply chains and building redundancy is difficult and expensive, and may result in higher consumer prices. Further, the tech giants who are in the vanguard of facilitating business productivity are also in the cross-hairs of international regulators. Their ability to disrupt and bend cost curves may be curtailed going forward.

But in our view, the bigger risk is that there will be too little inflation in coming years, not too much. This presents two problems for policy makers.

“The problem going forward might be too little inflation, not too much.”

Firstly, the possibility of deflation has risen. Deflation can be pernicious for economic growth and difficult to dislodge. Central banks can always raise interest rates to choke off high inflation, but have yet to perfect a strategy that addresses negative inflation.

Secondly, governments around the world have gone deeply into debt to finance the current recovery. Inflation can make debt easier to manage; income typically rises by the rate of inflation while debt payments are fixed. Extremely low inflation makes debt harder to handle.

The optimal level of inflation has engendered scholarly debate for decades. Many central banks have targets of around 2%, which has been deemed neither too high nor too low. In the wake of the pandemic, central bankers are re-thinking their inflation targets; the U.S. Federal Reserve announced an update to its policy framework recently. The main message: a little more inflation, if it can be achieved, would not be a bad thing.

I do worry about rising inflation, though. If prices go up faster, I may have to limit the duration of my weekly shopping trips. There goes my main source of entertainment...

The Challenge of Champions

The term “national champions” often refers to top sports achievers who represent their countries in international arenas. In the business arena, national champions are corporate powerhouses that seek victory in global competition. While technically private entities, they are explicitly or implicitly backed by their national governments with an aim of achieving a dominant position internationally.

Europe has typically frowned on designating national or regional champions. State aid for domestic industries is all but barred by the European Union (EU), to ensure a level playing field for firms across the continent. But during these unprecedented times, those rules have been shelved. The European Commission (EC) used to take about six months to review a member state’s request to deviate from the state aid rules; nowadays, the approval takes less than a day.

The pandemic has forced several European governments to deliver aid packages to businesses, including corporate giants. France announced an €8 billion package to support its carmakers while the German government agreed to a €9 billion bailout of a major airline, in return for a sizeable stake.

European state-aid rules were eased during the 2008 financial crisis, but reverted swiftly. This time, amid dwindling support for stringent competition rules, relaxations could endure beyond the COVID-19 crisis. The crisis merited extraordinary steps, but even before it began, sentiment was already shifting toward creating national champions.

Through its state-supported capitalism, China is the world leader in creating corporate champions. Most European nations have been vocal advocates of free-market policies and critics of Chinese business practices. But the current calls to fight “unfair” competition from China are changing sentiment surrounding state support.

The European debate about industrial policy has also been triggered by the actions of the United States, linking economic and geopolitical interests. Europe, a crucial player in global value chains, appears to have become a hostage to the ongoing strategic competition between China and the U.S. America has been upping the ante on protecting its steel, auto and technology industries in the name of national security, which serves to promote America’s champion companies.

The EU’s biggest economies, Germany and France, have been rallying for easing competition and foreign takeover rules, which are perceived as a roadblock in the creation of European champions. Company leaders are also calling for permanent state aid rules that favor European industries. Italy has gone a step further by calling for an overhaul of the region’s competition policy.

State aid is also a roadblock in Brexit negotiations; in general, the U.K. has been less prone to using state aid than other EU nations have been. While the EU wants the U.K. to respect the European state aid rules, the British side has been critical of Germany’s own large-scale subsidies.

“Calls for creating national champions in Europe are growing louder.”

Beyond nationalist sentiments, there are a few economic reasons why EU rules should be changed. Most notably, among the top 10 startups in the world by valuation, not even one is from Europe; six are from the U.S. and three from China. Secondly, the COVID-19 crisis has exposed the vulnerability of supply chains, many of which could be repatriated to Europe. Subsidies would assist the move.

Finally, national champions from abroad are posing tough competition for European corporations.

That said, there are risks to the strategy of developing a national or regional industrial policy centered on leading corporations. The post-World War II period (when national champions became popular) suggests large protected corporations with regular political interventions are often not good at adapting or innovating.

In sports, we cheer for our home teams in global markets. That practice may become more common in industrial competition during the coming decade.

Curb Your Enthusiasm

This year has conditioned us to be nervous any time our devices signal a breaking news alert. But last Friday, a pleasant surprise started our day: The U.S. unemployment rate improved from 10.2% in July to 8.4% in August. Unemployment’s decline since its peak of 14.7% in April has exceeded most forecasters’ expectations, but the streak of good news may be near an end.

The Bureau of Labor Statistics’ (BLS) monthly Employment Situation Summary reflects surveys of both households and employers. Its August household survey showed a jump of 3.8 million people working, which pushed down the unemployment rate. But its establishment survey showed an increase of only 1.4 million jobs. Measurement problems may have contributed to the difference; the response rate to the household survey is still well below its pre-pandemic level, while the establishment survey’s collection rate has returned to normal. This suggests that the lower figure is more accurate and that the unemployment rate could retrace some of last month’s decline.

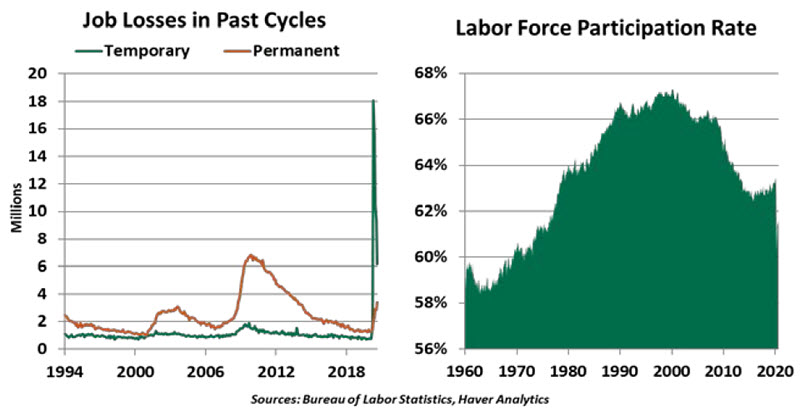

Classifying workers who are laid off due to COVID-19 is a persistent challenge; the BLS still estimates that the unemployment rate would be 0.7% higher if all affected workers were treated consistently. The labor force participation rate stands at a level last seen in 1976, suggesting a high degree of shadow unemployment.

“How long can temporary layoffs be considered temporary?”

Also hard to reconcile with last Friday’s news is the fact that 29 million Americans are drawing some form of unemployment benefits. This figure represents 18% of the U.S. labor force.

The August job count also showed a surge in government hiring for the decennial census. These hires are well-timed, but the jobs are temporary. Workers returning from layoffs are also helping: From a peak of 18 million in April, we are down to six million workers on temporary layoff. That is a great reduction, but still a total far beyond any past cycle peak. Six months into a recession, it is fair to speculate that many of these layoffs are no longer temporary. Permanent job losses have risen to 3.4 million, a sign of damage accumulating. Until labor-intensive sectors like restaurants and hospitality can safely return to their prior business volumes, workers will be sidelined.

We will celebrate good news where we can find it, but there is no reason to throw a party over recent employment news.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2020 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit our terms and conditions page.

© Northern Trust

Read more commentaries by Northern Trust