Brexit, Fed’s Lending Programs, Young Adults Come Home

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSUMMARY

- Brexit Brinksmanship Returns

- Low Plateau for Fed Lending Programs

- Young Adults and the Comforts of Home

Brinkmanship is a situation in which competitors flirt with disaster in order to get the most positive outcome for themselves. A poker player will sometimes go all-in to intimidate other players into folding, despite holding a relatively weak hand. This approach can work, but only until another player calls the bluff.

The U.K. has engaged in brinkmanship for much of the four-year-old Brexit saga. With less than four months to go in the transition period that followed its departure from the European Union (EU), the U.K. is still banking on this strategy. The EU has shown no signs of folding, raising the risk of a disastrous outcome.

Britain left the EU in January after signing a Withdrawal Agreement requiring it to follow EU rules during this year’s transition period. The two sides were to invest the 12 months negotiating and agreeing the outline of a new economic relationship. But instead of building on the base of the Withdrawal Agreement, the U.K. government recently stunned the EU and some British citizens by seeking to break it down. This has raised the risk of departure on December 31 without a new economic treaty with the EU; this risk is being priced into the markets for British assets and the pound.

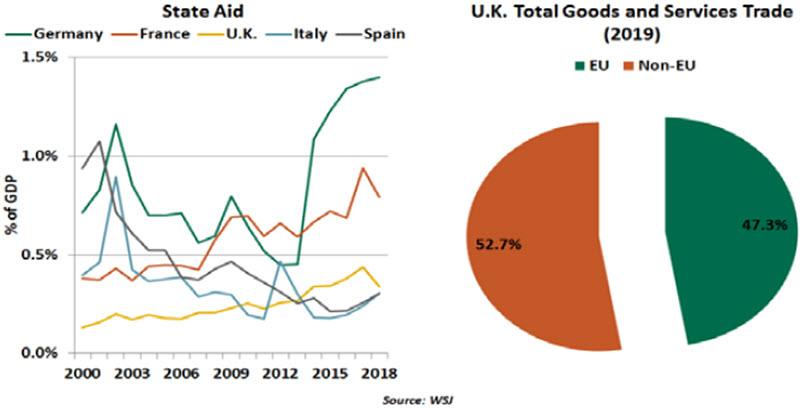

Britain wants to set many of its own rules, particularly on state aid to industry, the biggest roadblock in Brexit negotiations. Instead of following the European regime, which would have provided better market access to British businesses, the U.K. intends to follow World Trade Organization (WTO) state aid rules to create its own national champions.

The U.K. Parliament is currently considering a bill that suggests it would not implement the dual customs regime for Northern Ireland that was central to the Withdrawal Agreement. Retreat from this commitment would lead to customs checks and a hard border between Northern Ireland and the Republic of Ireland, something both sides seemed anxious to avoid a year ago.

A Brexit outcome that undermines the Good Friday Agreement of 1998, which ended decades of violence in Northern Ireland, would be a political and economic nightmare. People and goods flow freely across the border between the two in significant numbers. Northern Ireland trades mostly with the EU, but is particularly reliant on the Republic of Ireland’s market. More than one-third of Northern Ireland’s goods are exported to the Republic, while a little less than one-third are imported from that source. There are close supply chain linkages between the two sides, reflected in the high share of intermediate inputs in the trade structure.

In addition, reneging on the Withdrawal Agreement would imperil the U.K.’s stance as a reliable negotiator in future trade deals with other nations. Even the suggestion of it has undermined the U.K.’s image globally, and could dampen hope of a U.S.-U.K. trade deal. (U.S. presidential candidate Joe Biden has suggested he would not agree to such a treaty if the border issue is not satisfactorily solved.) Furthermore, a messy departure from the EU could embolden Scotland, currently part of the U.K., to press for a new referendum on independence.

“Bringing the Irish border back into question is a dangerous step.”

Europe, unsurprisingly, doesn’t want the U.K. subsidizing its businesses and getting tariff-free access to European markets. As we wrote in our last weekly commentary, the EU wants Britain to comply with European state aid rules regardless of the fact that the U.K. spends less on state aid than its European counterparts. On the contrary, the U.K.’s commitment to stricter state aid rules in its recent trade deal with Japan could weaken its stance against the EU.

A deal is in the political and economic interests of all parties. Under a no-deal Brexit, U.K.-EU trade would be subjected to a broad range of new tariffs and non-tariff barriers. WTO rules would apply in concept, but the weakness of the WTO impairs its enforcement power. In that scenario, the U.K. would likely face a bigger economic hit, as the EU is its single largest trading partner.

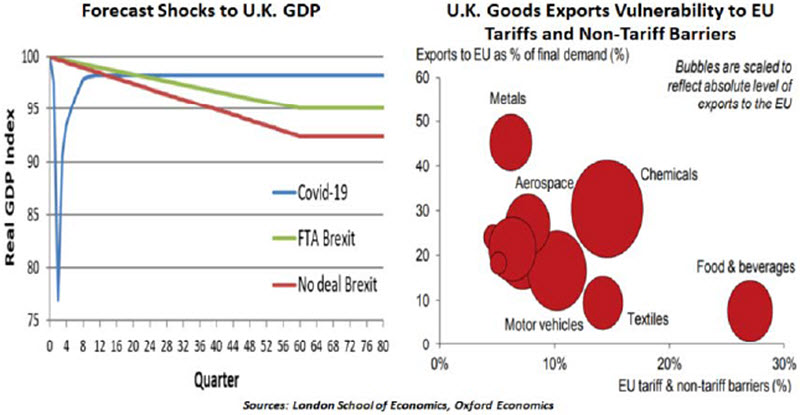

British and European car manufacturers are already struggling amid the pandemic and have warned against a no-deal Brexit. Under WTO terms, car and truck exports would be subjected to 10% and 22% tariffs respectively, translating to a combined £100 billion loss by 2025 for the automakers. The British farming industry, which accounts for two-thirds of British exports to the EU, will face even higher tariffs. On average, dairy products will be subjected to 35% tariffs. British firms would be forced to initiate the costly task of re-aligning supply chains.

Under a no-deal scenario, Oxford Economics estimates that the U.K. will experience a slower recovery from the current slump, with real gross domestic product (GDP) 0.9% below its baseline at the end of 2022. The U.K. government’s analysis showed that a no-deal Brexit would reduce U.K. GDP by 7.6% after 15 years compared to a 4.9% decline should a free trade agreement be reached with the EU.

The U.K. government is already under pressure for its handling of the pandemic. A no-deal Brexit would compound the grim economic outlook just as the government prepares to wind down its stimulus measures. (Many Brexiteers believe, strangely, that the pandemic will obscure the costs of a disorderly divorce, and somehow make them more palatable.) Although the immediate shock from Brexit will likely be lower than that from the pandemic, it will have a lasting impact on the economy.

“Hopes for a trade agreement between Britain and the EU are fading.”

It is said that one nation’s loss is another nation’s gain. Ireland, a country at the center of the Brexit deadlock and one likely to suffer significantly from a no-deal, has been among the biggest beneficiaries of the Brexit-led corporate exodus. While the U.K. enjoys a clear dominance in financial services (London clearing houses handle over 90% of all euro-denominated derivative transactions), more firms have been relocating their businesses to the EU. Dublin has emerged as a popular choice for financial services firms seeking to relocate their operations. Germany, France and the Netherlands are not far behind.

While we are still hopeful that Britain and the EU will agree to a free trade deal this year, our confidence is fading. It is going to be an extremely close call. Recent history tells us that these matters are rarely resolved before the eleventh hour, but the clock is ticking.

It is not wise to go all-in with weak hands, especially when the stakes are so high. If the EU chooses not to fold, the U.K.’s current Brexit strategy could prove to be an expensive bust.

Borrowers Wanted

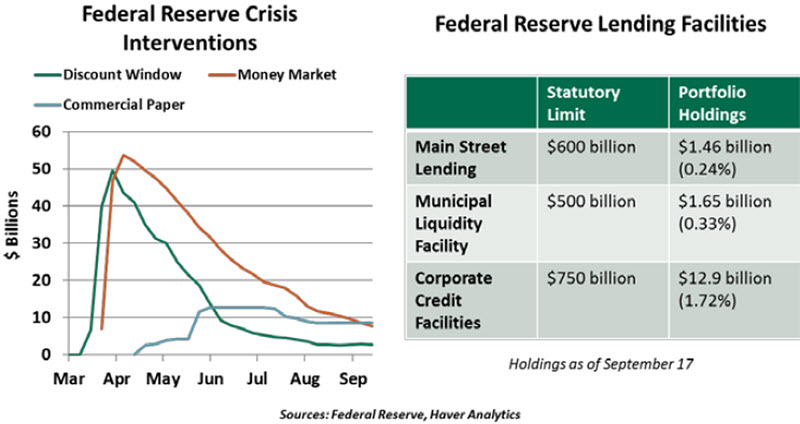

As fear took hold across markets in March, we celebrated the decisive actions the U.S. Federal Reserve undertook to restore order. Fed leaders wasted no time cutting interest rates and increasing asset purchases. They rapidly launched special programs to support financial sectors that were under acute stress and announced additional facilities that supported the market more broadly. Six months later, these interventions have seen widely varied outcomes.

The Fed’s immediate responses were effective. Funding facilities added liquidity to markets for commercial paper and money market funds, while expanded use of the Fed’s discount window ensured that banks had sufficient capital to continue lending. In short order, these programs reached their peaks, and then receded as financial markets returned to normalcy.

The Fed’s broader lending programs launched later. The Main Street Lending Program contained three vehicles to support bank lending for medium- to large-sized businesses. The Corporate Credit Facility aimed to purchase corporate bonds. The Municipal Liquidity Facility launched to support state and local bond issuance. While announced with great fanfare, all of these programs are far short of their potential.

This shortcoming can be viewed optimistically. Low take-up of the Fed’s programs means that markets are functioning well without intervention. The signaling effect of the Fed’s commitment to market support can help to soothe investors without the Fed ever actually buying an asset.

Still, we are surprised to see potentially trillions of dollars of lending capacity go unclaimed. The Fed’s programs have been challenged by eligibility: Risky borrowers found little support from these new programs. Banks that lend under the Main Street program must keep a portion of each loan on their books, limiting their future risk appetite. And municipal issuers must be investment grade to partake in the Municipal facility, with pricing adjusted by credit rating. Most potential borrowers have not found the Fed’s programs to offer any savings relative to market rates.

The Fed has not given up on these programs. All of their interventions have been extended beyond their initial deadline dates of September 30. Several programs have evolved to include a wider range of borrowers: the Main Street program lowered its minimum loan amounts and expanded to include nonprofits, while the Municipal facility grew to welcome more issuers. But to spur adoption, the Fed needs to make the harder decision to lower prices or take on greater credit risks.

“Fed lending programs have improved credit conditions, but have resulted in very few new loans.”

Far in its past, the Fed made direct loans. Starting in 1934, to promote the recovery from the Great Depression that curtailed bank lending, regional reserve banks issued commercial loans directly. Early loans had an estimated 3% loss rate. This power was struck from the Federal Reserve Act in a 1958 amendment, leading to the Fed’s current risk-averse posture. The Fed’s mandate now allows it only to support bank lending, which slows underwriting and adds costs to loans.

The Main Street program contrasts starkly with the Paycheck Protection Program (PPP), administered by the Small Business Administration (SBA). PPP loans were eligible for forgiveness, making them highly desirable, and were priced at only 1% if they weren’t forgiven. The Main Street program, however, has less to compel a borrower to seek a loan or a bank to promote it.

Ultimately, these programs demonstrate the limits of the Fed’s ability to stimulate the economy. Short-term financial interventions were helpful; more complex arrangements were not. These slow-moving programs received seed funding from the CARES Act’s allocation to support larger businesses. Proposals for future fiscal stimulus have contemplated taking back this unused capital. To support important sectors, Congress and the Treasury may need to take more direct action than this partnership with the Fed.

Failure To Launch

School is back in session. Some students are in the classroom, some are at home, and some are shifting between the two locations. Many parents of children in primary school have added the title of tutor to their other responsibilities, adding another challenge to their daily balancing act.

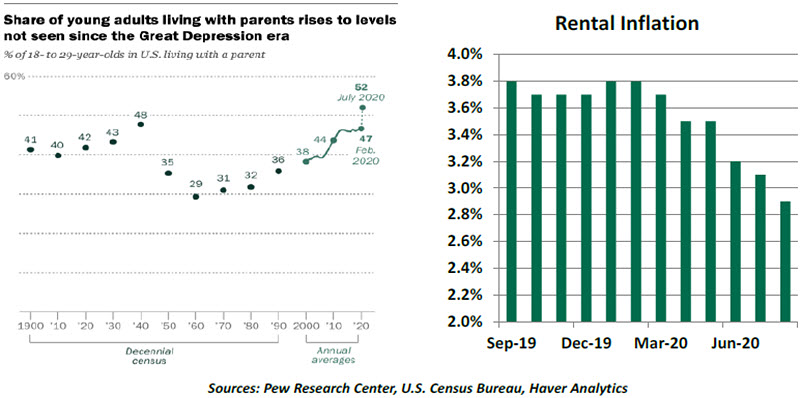

Parents in other American households are dealing with the challenge of having young adults in the house. For the first time in at least 80 years, a majority of 18- to 29-year-olds are not living independently. These young people don’t need tutoring, but their presence at home is both a sign of the times and a potential warning for the economy.

At the younger end of the range, many collegians have either been instructed to or chosen to remain home, as virtual instruction covers the majority of classes at many schools. Their return to student apartments will depend on how well COVID-19 can be contained in campus settings, allowing more in-person instruction.

For recent graduates, unemployment rates are quite a bit higher than those of the overall economy. As of June 2020, more than one-quarter of 16- to 24-year-old Americans are neither enrolled in school nor employed, more than double the February level. With incomes uncertain and student debt high, the economic benefits of living at home are very attractive.

“The pandemic has been especially hard on students and younger members of the labor force.”

Those able to live with their parents are fortunate to have that alternative, but their continued presence at home has a number of broad economic consequences. Rates for rental properties have stagnated, pressuring owners of multi-family properties (especially those in urban centers). Postponed independence delays marriage and child-bearing, perpetuating demographic imbalances in the population. Parents who support their children well into adulthood often have to deplete savings and delay retirement.

Some who have returned home recently will move out again as the economic and public health consequences of COVID-19 ease. But the downward trend in the fortunes and finances of young people predates the pandemic, and will likely continue after it passes. This means that many families are going to be spending a lot more time together in the years ahead, for better or worse.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2020 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit our terms and conditions page.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All