Value, Margin Of Safety, & The Art Of Doing Nothing

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOver the last several months, we have discussed the remarkable underperformance of value versus growth. While many investors quickly dismiss the performance gap under the guise of “this time is different,” it has important longer-term implications. In today’s missive, we want to discuss value, the margin of safety, and the real art of “doing nothing.”

This Time Is Different

A recent MarketWatch article made an argument for why this time is different than previous cycles.

“Investors seem to want to embrace a value tilt – stocks that will do well as the economic recovery gathers steam. However, they continue to fall back on the tried-and-true growth stocks that have done well so far, through more uncertain times. But what if those old ‘value’ and ‘growth’ frameworks are the wrong way to measure market moves?”

If you re-read the statement closely, there are a couple of issues that stand out.

- If “individuals” continue to “fall back” into the stocks that are rising with the market, then they are “speculating” by chasing prices rather than “buying value.”

- There is nothing wrong with the “growth” and “value” frameworks, expect in periods where they don’t fit the speculative fervor of the market.

Investing Versus Speculation

Currently, the majority of investors are simply chasing performance. However, why would you NOT expect this to be the case. On a daily basis the media, and WallStreet, continually press investors to chase prices higher by deeming “this time to be different.”

However, this is where we can begin to understand the difference between investing based on value versus speculating for short-term gains.

Let me give you an example:

You are playing a hand of stud poker, and the dealer deals you this hand:

How would you bet? A lot, a little, or would you fold?

Even a cursory understanding of the game of poker suggests other players are probably holding better hands than you. Instinctively, you know this and you would tend to “fold” and wait for the next hand.

Now, is this operation “investing” or “speculation?”

The answer should be obvious. When you engage in an operation where the outcome is primarily derived from “luck,” more than “skill,” it is speculation.

Phillip Carret, who wrote The Art of Speculation (1930), defined this more elegantly:

“Speculation, may be defined as the purchase or sale of securities or commodities in expectation of profiting by fluctuations in their prices.”

Chasing markets is the purest form of speculation. It is merely a bet on prices going higher rather than determining if the price paid for those assets is at a discount to fair value.

The Discounting Of Value

What the quote from MarketWatch espouses is that of the “Greater Fool Theory.”

“The greater fool theory states that it is possible to make money buying securities, whether or not they are overvalued, and sell them for a profit at a later date. Such is because there will always be someone (i.e. a bigger or greater fool) else willing to pay a higher price.”

Such is also the purest definition of market speculation.

Benjamin Graham, along with David Dodd, attempted a precise definition of investing and speculation in their seminal work Security Analysis (1934).

“An investment operation is one which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.”

Graham also noted why individuals should be concerned when they read articles espousing “this time is different.”

“The distinction between investment and speculation in common stocks has always been a useful one and its disappearance is a cause for concern.” – The Intelligent Investor

Given the sharp rise in markets since March, it is not surprising the media pushes a host of excuses to justify overpaying for assets. However, as Graham goes on to note, the media should take a different track.

We have often said that Wall Street as an institution would be well advised to reinstate this distinction and to emphasize it in all its dealings with the public. Otherwise the stock exchanges may some day be blamed for heavy speculative losses, which those who suffered them had not been properly warned against.” – Ben Graham, The Intelligent Investor

Why Value Investing Wins The Long-Game

Throughout market history, investors repeatedly abandon the principles of value investing and maintaining a “margin of safety” during periods of exuberance. Ultimately, those investors paid a dear price for their speculation. “Overpaying for value” has repeatedly led to poor financial outcomes.

What Is A “Margin Of Safety”

Ben Graham heavily espoused the importance of a “margin of safety” in the investment operation. The margin of safety suggests an investor only purchases securities when their market price is significantly below their intrinsic value.

“Confronted with a challenge to distill the secret of sound investment into three words, we venture the motto, Margin of Safety” – Ben Graham

Followers of Ben Graham’s teachings have a deep history of long-term investing success from Warren Buffett to Seth Klarman:

“The best investments have a considerable margin of safety. This is Benjamin Graham’s concept of buying at a sufficient discount that even bad luck or the vicissitudes of the business cycle won’t derail an investment. As when you build a bridge that can hold 30-ton trucks but only drive ten-ton trucks across it, you would never want your investment fortunes to be dependent on everything going perfectly, every assumption proving accurate, every break going your way.” – Seth Klarman

The reality of investing is that rarely does everything “break” the right way. Having a “margin of safety” provides a cushion against the unexpected when it occurs.

An Example Of Intrinsic Value

Investing using a “margin of safety” is not as easy as it sounds. The vast majority of retail investors today do “no research” on the companies in which they invest. They look to the financial media, websites, and tweets to tell them what to buy. Or worse yet, they just buy what is “winning” in the short-term.

The reality is that the concept of a margin of safety is found only by researching to discover the company’s qualitative and quantitative factors. Such work includes understanding the firm’s management, governance, industry performance, assets, and earnings. From there, the investor must derive the security’s intrinsic value.

The following is a report on CVS Health. We regularly provide such reports to our RIAPRO Subscribers (30-day Risk-Free Trial). The report is a condensed version of analysis we use to determine the intrinsic value of a potential investment opportunity.

Once you have done your homework, the market price is then used as the point of comparison to calculate the margin of safety. As noted in the CVS report:

“CVS is currently priced at a deep discount to its intrinsic value. We forecast that roughly 47.1% of upside remains on the stock.”

Such is why Warren Buffett declares the “margin of safety” as one of his “cornerstones of investing.” He, like us, applies as much as a 50% discount to the intrinsic value of a stock to determine price targets.

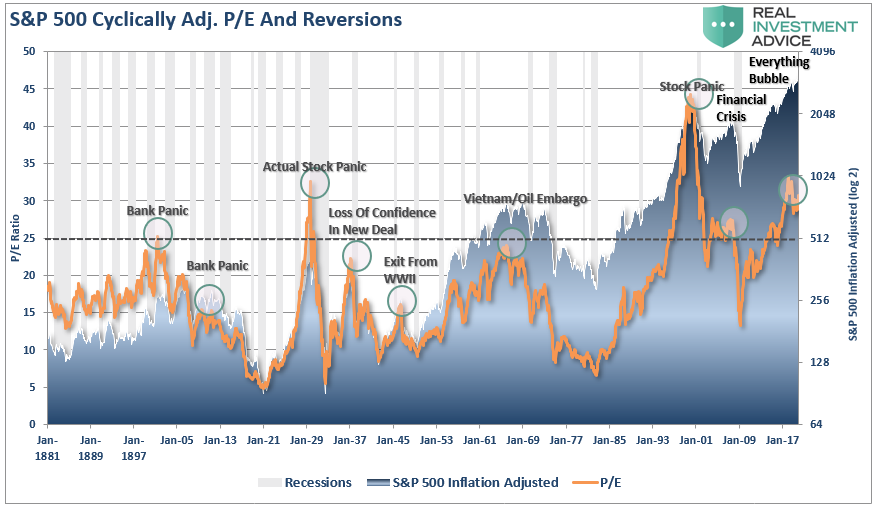

However, in a market that is overvalued on many metrics, finding value becomes difficult. Furthermore, holding value when it is underperforming the “hot stocks” in the market, is even more challenging.

Art Of Doing Nothing

Currently, value investing is clearly out of favor. It hasn’t worked well for so long it is not surprising the media has declared “value investing dead.” As we showed in that article:

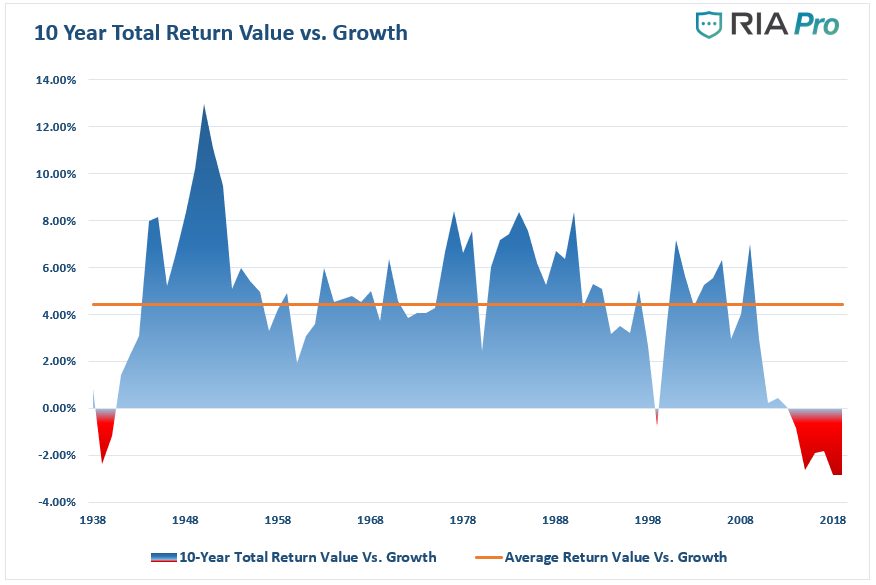

“The graph below charts ten-year annualized total returns (dividends included) for value stocks versus growth stocks. The most recent data point representing 2019, covering the years 2009 through 201-, stands at negative 2.86%. Such indicates value stocks have underperformed growth stocks by 2.86% on average in each of the last ten years.”

There are two critical takeaways from the graph above:

- Over the last 90 years, value stocks have outperformed growth stocks by an average of 4.44% per year (orange line).

- There have only been eight ten-year periods over the last 90 years (total of 90 ten-year periods) when value stocks underperformed growth stocks. Two of these occurred during the Great Depression, and one spanned the 1990s leading into the Tech bust of 2001. The other five are recent, representing the years 2014 through 2019.

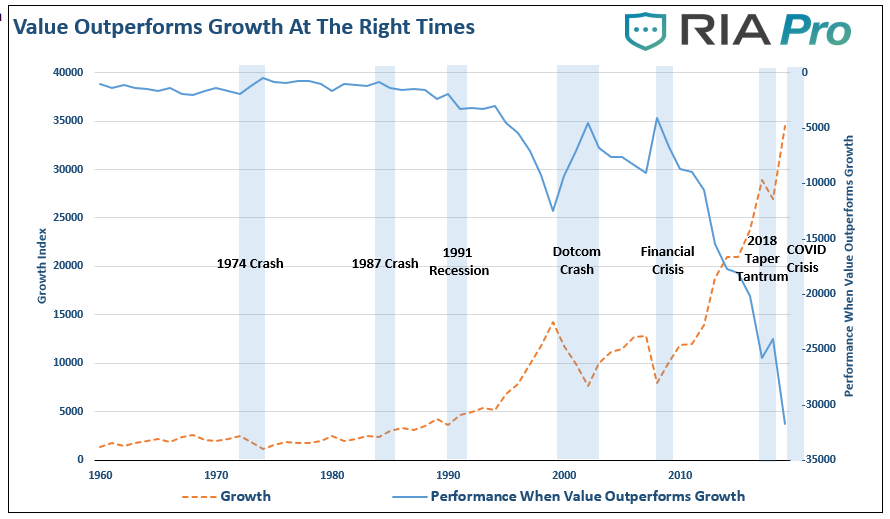

Mirror Opposites

“The chart shows the difference in the performance of the “value vs growth” index. That index is compared to a pure growth index with each based on a $100 investment. While value investing has always provided consistent returns, there are times when growth outperforms value. The periods when “value investing” has the greatest outperformance, as noted by the “blue shaded” areas, are notable.”

So, what should investors do when they can’t find real value in which to invest? While the media says you must always remain invested regardless of the outcome, there is an option. Do nothing.

The Art Of Doing Nothing

Such was a point Jesse Felder recently noted:

Perhaps the most important lesson about investing I’ve learned is when there is nothing to do, do nothing. The problem is nothing may actually be the hardest thing to do. We all want to feel like we are being proactive and that requires doing something even when there’s nothing to be done. So it takes a great deal of discipline to resist the urge to do something and commit to doing nothing. In that way, however, committing to doing nothing is probably the most proactive thing to do.

His comment defines “investment” versus “speculation.”

When investing, we seek to deploy capital in an operation with potential to deliver a high return on that investment. Therefore, logically, if no such opportunity with the required “margin of safety” exists, then the best operation is to “do nothing.”

You wouldn’t overpay for a piece of real estate. You shop for the best price on everything from televisions to autos. Yet, when it comes to investing, why would you pay any price for a future stream of cashflows?

Conclusion

Another way to think about this is to realize that the vast majority of mistakes investors make come out of a feeling of needing to do something, of being proactive, rather than simply waiting patiently to react to a truly fantastic opportunity. Rather than react only to true opportunity, they react to social pressure or envy when they see their neighbor making a “killing” in dot-com stocks, ala 2000, or residential real estate, ala 2005, or in call options today.” – Jesse Felder

As is always the case, it may seem for a while that investors are making money “hand over fist” while the market is rising. However, the stories are just as plentiful about what happens as the inevitable downturn vaporizes capital in an instant.

I agree with Jesse’s conclusion:

Right now, due to the extraordinary circumstances in the world, politics, the economy, monetary policy, and more, the urge to do something is greater than normal. However, the opportunity to put money to work is simply not there. At least not yet. But it’s coming. And until it does, the most proactive thing an investor can do is simply commit to doing nothing. Understanding that that is not a passive decision, but a very proactive one, indeed.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All