A vote for stocks. After solid summer gains came September volatility. The question now is what’s priced into markets as investors zero in on COVID-19 developments and the November election. Highlights of our Q4 outlook:

- Market volatility is likely to remain elevated through year-end.

- Elections bring uncertainty but little long-term bearing on stock performance.

- Stocks’ favorable valuations vs. bonds should prevail as rates stay low.

Market overview and outlook

U.S. stocks have made up significant ground since their March lows. We see COVID-19 vaccines and therapeutics as a key driver moving forward. Positive vaccine progress this fall could further boost stocks, particularly those at the epicenter of coronavirus pain. Examples include travel and leisure broadly, and select retailers. While the unprecedented vaccine effort has required significant government outlay, the money spent pales relative to expected economic losses. The COVID-induced slowdown will cost the economy $7.9 trillion over the next decade, according to the Congressional Budget Office. Vaccine investment in the area of $4 billion is money well spent.

Alongside the ongoing battle with the pandemic and its economic fallout is a pivotal U.S. election. Volatility historically has trended higher as elections near, and this year is likely to be more pronounced. It wouldn’t surprise us to see a contested election that drags on, exacerbating volatility through December. Our view leading into year-end: balanced.

Perspective on election risks

Elections are notoriously peppered with angst, anticipation and speculation. As investors, we believe they should also be approached with humility — and a grain of salt. We offer three reasons why this is still true in this most unusual year — one in which the coronavirus pandemic and its economic fallout have upset lives and livelihoods and reset the priorities of Americans and politicians alike:

-

Things aren’t always as they appear

Promises and proposals made on the campaign trail offer an indication of a candidate’s intentions, but bureaucracy, compromise, lobbying and politics help shape the reality once in office. At the same time, markets don’t always behave as conventionally expected. One example: Defense and so-called “sin” stocks were widely expected to suffer under President Barack Obama. But over those eight years, defense as a sector outperformed, with one top name outpacing the S&P 500 by 400% and another by 100%. The leading tobacco stock bested the index by more than 250%.

Key takeaway: Politics and its impact on markets are hard to predict and rarely play exactly to script. This is all the more reason to focus on bottom-up company fundamentals as the key driver of returns.

-

Many “popular" scenarios are priced early

As an election nears, the rhetoric and investor attention to it increase — and markets begin to discount the outcomes and implications. Case in point: Many of the clean energy companies might be expected to benefit under a Joe Biden win, but we see prices already building this in. We prefer to target the overlooked opportunities. Utility companies, for example, have been laggards but could be winners with strides toward investing in renewable energy projects. They are also resilient to tax rate changes given a regulatory structure that generally provides for an after-tax return on equity.

Key takeaway: Markets are anticipatory, and investment opportunities must be framed relative to current pricing. Gaining an edge requires looking beyond the obvious to the nuance and potential that may lie beneath the headline.

-

Politics have had little long-term market impact

The stock market has advanced regardless of the party in the White House: A hypothetical $1,000 investment in U.S. equities in 1926 would have grown to nearly $9 million as of June 30, 2020, according to data from Morningstar.* It’s important to stay invested, yet the uncertainty of election years causes many investors to retreat to cash while waiting out the volatility. COVID-19 has exponentially increased uncertainty — and cash balances.

Key takeaway: Increased cash on the sidelines could make a return to stocks as election and coronavirus-related uncertainty abates — and as stock valuations appear attractive relative to bonds.

It’s all relative

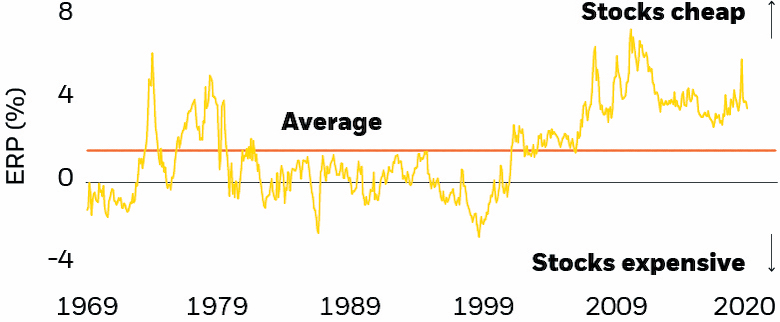

A glance at price/earnings (P/E) ratios might suggest U.S. stocks are expensive. But this paints an incomplete picture of the current opportunities and risks in financial assets. With interest rates at historic lows, and poised to stay there for some time, we believe equities are a relative bargain and can be a compelling option for growth, value and income seekers.

The equity risk premium (ERP) compares stocks to bonds by taking a simple P/E ratio of the S&P 500, inverting it to arrive at the earnings yield, and subtracting the 10-year Treasury yield. The gap is the equity risk premium. As shown in the chart below, the ERP is near the highs of the past 50 years, suggesting stocks are very attractive relative to bonds.

Stock valuations attractive vs. bonds

Equity risk premium, 1969-2020

© BlackRock

Read more commentaries by BlackRock