Climate Considerations, Regulatory Shifts, and Debt Investment in China

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefitssummary

- Climate risks go beyond any one country or election.

- The election may put an end to a wave of deregulation.

- China’s fixed income markets are attracting foreign investors.

Editor’s Note: This is the third in a series of pieces that will examine key economic issues surrounding the 2020 U.S. election.

The adage “That government is best which governs least,” is taken from Henry David Thoreau’s “Civil Disobedience.” This has long been the credo of conservative economic thinkers, who view government interventions in markets with disdain. Regulation changes incentives and equilibria, and often not for the better. But others counter that intelligent regulation can improve individual and collective outcomes.

When the consequences of problems and the remedies offered by regulation are surrounded by uncertainty, designing intelligent controls becomes very challenging. When complying with those controls is costly, the contention surrounding them is especially intense.

Environmental regulation, therefore, represents a perfect storm. (Pun intended.) Natural conditions change gradually, and are difficult to project very far into the future. Steps to address environmental concerns involve costly sacrifices by firms and individuals. And because no one county, state or country owns the world’s atmosphere, governments must put their self-interests aside and collaborate with one another.

These are the challenges that surround proposals to address climate change. The differences of opinion on this front between the two presidential candidates could not be starker, and the stakes surrounding the issue couldn’t be higher.

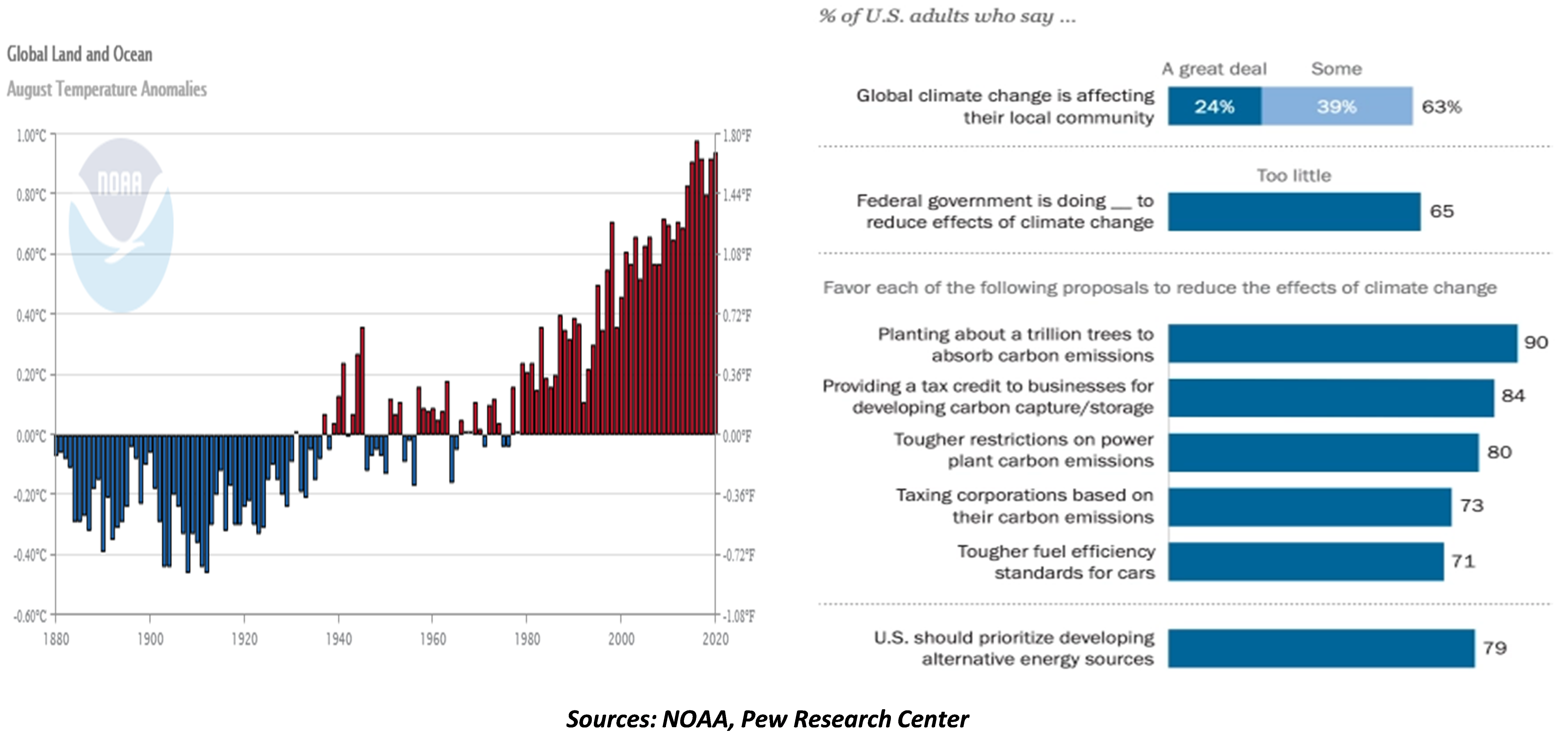

Global Land and Ocean: August Temperature Anomalies

The debate over climate change is taking place against a dramatic backdrop. Fires have consumed more than five million acres of forest in western states, and there have been 28 named tropical storms and hurricanes so far in 2020. (The average is 12 per year.) The human and financial costs of these events are immense.

The data shows that air and water temperatures have been increasing persistently for 40 years. Seas are rising and acidifying; polar ice is dissipating. The frequency and severity of weather-related disasters have escalated in recent decades. Insurers, investors and central bankers are taking account of climate risk in their policy setting.

“2020 has been a particularly difficult year for climate-related disasters.”

A broad scientific consensus finds that global warming is real, and anticipates severe consequences if temperatures continue to rise at their recent pace. The consensus further holds that global warming is linked to human activity, specifically to the burning of fossil fuels.

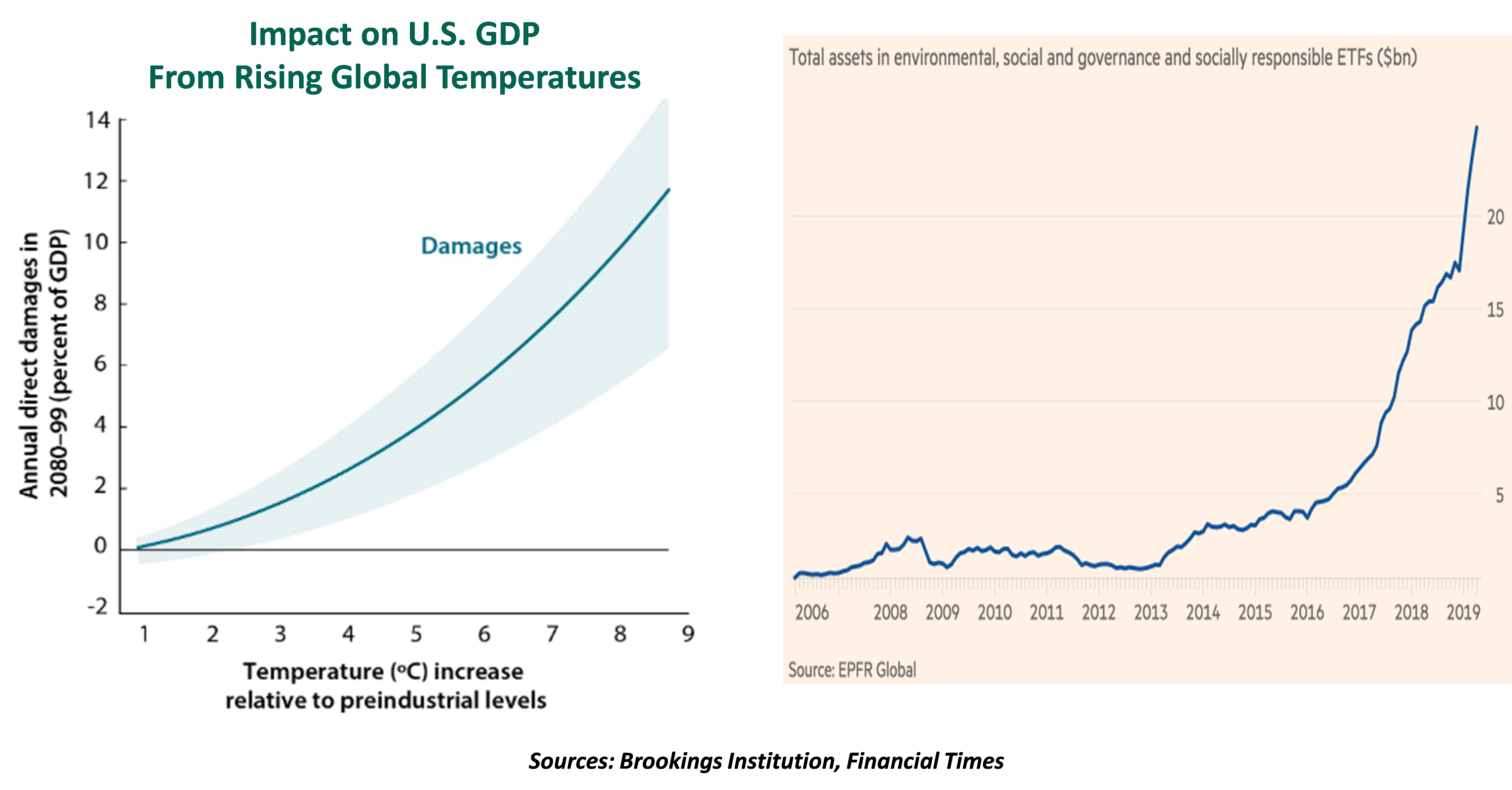

We’ve discussed the economic issues related to climate change on several occasions; major work can be found here and here. Studies show that economic output around the world could shrink by 15% in the coming decades if warming is not arrested. The human costs could be immense.

The current administration does not agree with the consensus. It has downplayed the science surrounding climate change and has rolled back environmental regulation. The White House plans to withdraw the United States from the Paris Climate Accord next month, and the Brookings Institution counts 74 further actions taken by the administration to weaken environmental protection. Controls on emissions from power plants and automobiles have been relaxed, and vast tracts of federal territory have been opened to oil and gas exploration.

Impact on U.S. GDP from Rising Global Temperatures

The Biden platform is diametrically opposed to the president’s. It supports a series of measures aimed at tackling climate change: the goal of zero net greenhouse gas emissions by 2050 has been proposed. To meet that target, methane emissions would be limited, fuel economy standards for vehicles would be raised, and development of fossil fuel sources on public land would be prohibited. Additional investment in clean energy technology would be sponsored and encouraged. And (needless to say) a Biden administration would rejoin the Paris Climate Accord.

The evolution to a greener future will not come without cost. Oil and gas production in the United States has mushroomed over the last 20 years, reducing dependence on unstable foreign providers. According to PwC, the industry accounts for just over 5% of American employment, and is even more prominent in key energy-producing states. Migration to a greener future will lead this sector to shrink.

“The investment community will continue to push for a greener future.”

There is also legitimate concern about being a first mover. No country wants to make the investments or sacrifices needed to reduce global warming if others aren’t doing the same. Any asymmetry of international commitment would leave industries in some countries facing tighter regulation, creating a competitive disadvantage.

Finally, there is a good debate to be had over whether a carrot or a stick would be the best way to achieve environmental outcomes. Carbon taxes and exchanges would use market mechanisms to allocate emissions capacity efficiently, causing firms and individuals to internalize the impacts they have on the planet. Regulation is more rigid and potentially punitive.

Whatever the outcome of the election, the path forward for the financial markets is clear. Environmentally sensitive investing continues to gain strength as leading asset managers shift allocations away from firms and industries with poor carbon footprints and cast proxies in favor of corporate resolutions aiming at a greener future.

Throughout history, industrial transitions have caused difficulty. Paradigm shifts can be disruptive and disorienting, but they also present new opportunities. When it comes to climate policy, the question facing the U.S. electorate is whether to warm to these opportunities or risk getting even warmer by turning away from them.

Oversight Options

Environmental policy is far from the only regulatory topic being debated this campaign season. Government guidelines cover a range of products and practices.

Well-structured regulations can play an important role in keeping people safe and in ensuring fair access to markets. But the cost of compliance slows down business initiatives and consumes capital. As a result, deregulation is generally viewed as a business-friendly stance.

“Too much regulation is a burden, but too little is a risk.”

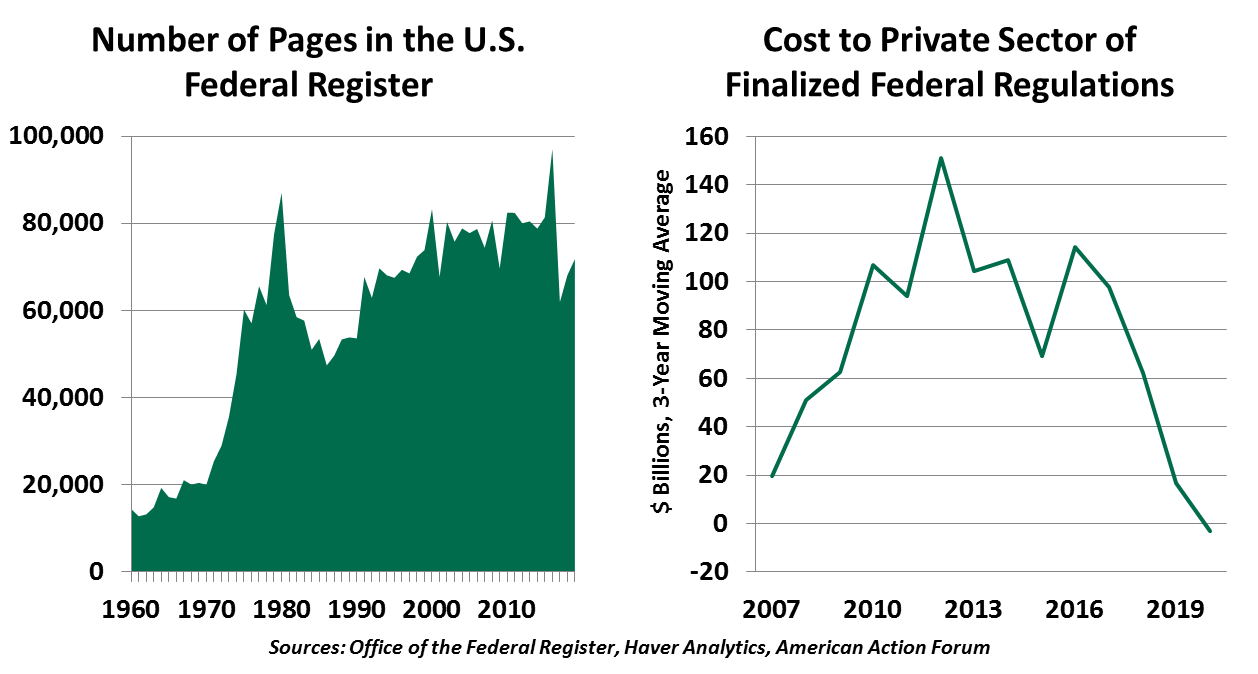

The current administration has a mixed record on this front. The Brookings Institution has tracked more than 150 de-regulatory proposals passed since the president took office. The size of the Federal Register, which records regulations passed by Congress, has fallen by almost 25,000 pages since 2016. The American Action Forum estimates the resulting savings for businesses to be over $100 billion annually.

But the last four years have not entirely been a bonanza of shredded red tape. The Trump administration has intervened in markets when it deems necessary, as shown by the Justice Department’s objection to certain international acquisitions. Technology transfer is almost certainly going to be the focus of considerable regulatory attention in the years ahead.

The Democratic Party, on the other hand, is more willing to advance new regulations. Joe Biden’s healthcare plan would add to the regulatory framework of the Affordable Care Act. His proposals for promoting racial equity, improving access for people with disabilities, auditing recipients of small business support and raising safety requirements for frontline workers seek to correct business practices deemed to be misaligned with the public interest.

Financial services regulation is a point of considerable speculation, especially under the scenario of a Democratic sweep. Other candidates in the Democratic presidential primary called for even greater regulation and reinforcement of the Consumer Financial Protection Bureau, which has languished under the current administration. Biden’s platform does not single out the financial sector, but in this case, personnel is policy. If he wins, Biden’s appointees to roles like Secretary of the Treasury and Chair of the Federal Reserve (in 2022) will be closely watched.

Both parties are considering additional regulation around the technology sector. Much debate centers on section 230 of the Communications Decency Act of 1996, which provides liability protection to online publishers for content shared on their platforms. The law has already required amendments to require removal of content that supports illegal activity, and its durability remains in question. Republicans believe social media companies do too much to suppress conservative views, while Democrats argue social media companies must do more to crack down on hate speech and misinformation.

Number of Pages in the U.S. Federal Register

Online technology firms may also face antitrust scrutiny. Just this week, the House Judiciary Committee published an investigation into competition in digital platforms. The report found that major tech firms have a high degree of power in online retail, app development and advertising markets, and it recommended remedies as drastic as breaking the firms apart to restore competition. Republican members of the committee did not sign on to these conclusions, but released a separate recommendation calling for more targeted antitrust enforcement. Expect investigations to continue regardless of who takes power.

Biden and Trump also share an emphasis on restoring America’s domestic manufacturing sector. A reelected Trump may go beyond his signature tariff policies to actively reduce U.S. business involvement with other nations, especially China. Biden’s plan calls for a strategic review of supply chains to identify and change points that put U.S. supplies at risk. Either approach is additive to the rules that businesses must follow.

History suggests that regulation increases and falls in cycles. November’s outcome may mark the end of a deregulatory wave.

China’s Capital Gains

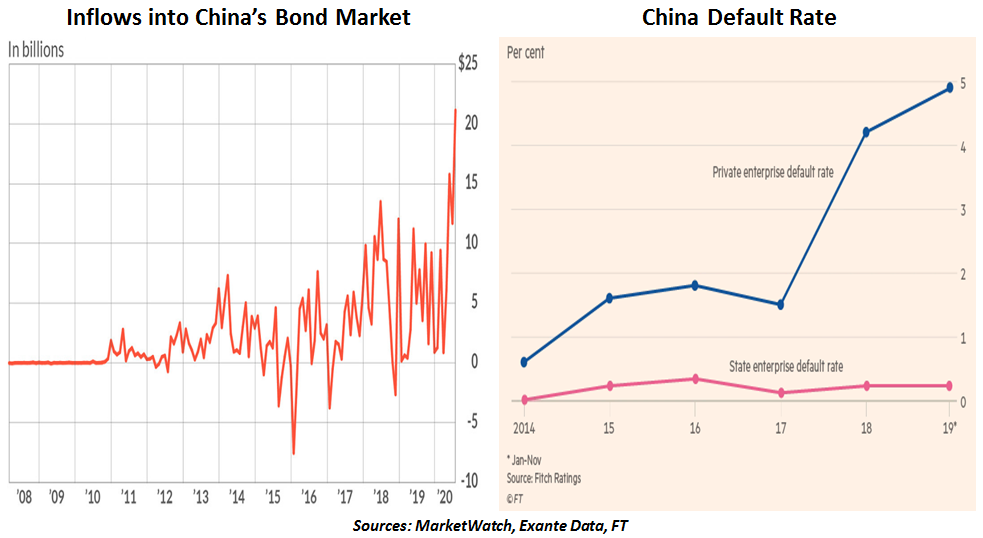

As we wrote recently, China has emerged as a global investor, but its outbound investments are being met with increased scrutiny. But capital flows in both directions, and international investors are buying into China’s $15 trillion bond market in increasing numbers.

Despite its massive size, the Chinese domestic debt market was opaque to overseas investors only a few years ago. Chinese efforts to open its bond market to foreign investors have included launching the Bond Connect program, ending foreign investment limits and expanding the range of investment options.

“Index investing is driving foreign capital into Chinese bonds.”

Bloomberg, JP Morgan and FTSE Russell began including Chinese assets in their benchmark bond indices in early 2019. This was an important milestone for China, as inclusion prompted record inflows into China’s fixed income markets. Foreign institutional holdings of Chinese bonds have risen from $100 billion in 2016 to over $400 billion this year. This total could rise by another $140 billion as index allocations to Chinese debt fully phase in over the next 20 months.

While record inflows reflect the favorable reaction to Beijing’s efforts to liberalize its capital markets, stronger performance and the hunt for higher yields have also motivated investors. The yield on the 10-year Chinese government bond is over 3%, compared to less than 1% on 10-year U.S. Treasury bonds and just above 0% on the Japanese benchmark. The FTSE Chinese Government Bond Index returned an annual 4.2% in the 12 months to July 2020, compared with a 3.7% return for JP Morgan’s dollar-denominated Emerging Market Bond Index.

Inflows into China's Bond Market

China may not carry the economic risks generally associated with many emerging markets, but it is not riskless. China’s high corporate debt and rising defaults in domestic bond markets are a key concern. And the transparency around some obligors is still not the best, which is one reason why the proportion of Chinese securities in benchmark indices remains small relative to China’s share of global debt or gross domestic product.

The situation surrounding bond indices and Chinese debt illustrates the power and potential pitfalls of passive investing. Global capital flows are heavily driven by the efficiency and low fees of indexing, but the automatic nature of the process may not fully account for inherent risks. Index inclusion has been great for China; time will tell whether it’s great for investors.

© Northern Trust

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All