Investments in the Future: Infrastructure and Education

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSUMMARY

- Infrastructure Indigestion

- Making More Of American Minds

Editor’s Note: This week’s edition concludes our series examining key economic issues surrounding the 2020 U.S. election.

As the pandemic continues, we reflect on fond memories of experiences not available to us at the moment. Restaurant patrons may recall the challenge of visiting an eatery and finding the menu to be too long. Page after page of appetizers, entrees, desserts and drinks all sound tempting, but there is only so much room on the table. The longer the menu runs, the harder it is to choose.

That same feeling of paralysis has held back investment in infrastructure. A wide range of elements falls under the umbrella of “infrastructure,” including the water supply, waste management, electrical generation, transportation and telecommunications. Each has scores of subcategories underneath. It’s quite a menu, which is why it has been hard to design a way forward for America’s infrastructure. The next administration will be forced to choose among a range of interesting alternatives.

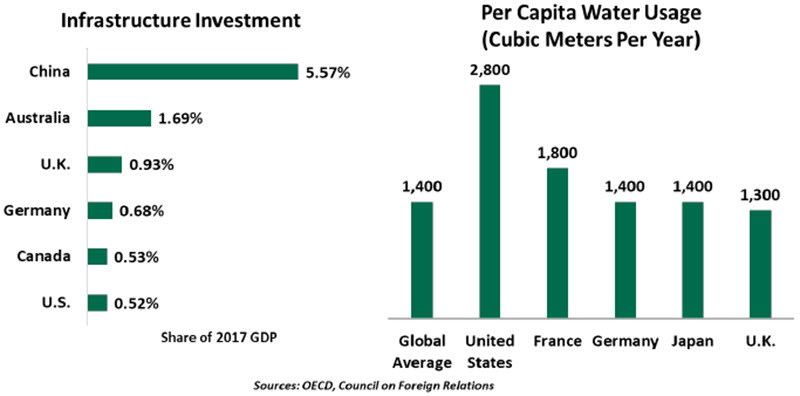

The benefits of infrastructure investment are clear. Maintenance of existing facilities reduces the risk of unfortunate occurrences that range from the inconvenient (like heavy traffic and electric brownouts) to the catastrophic (like collapsed bridges). Spending on infrastructure accrues directly to local employment and economic growth. And well-designed infrastructure can boost productivity, which has grown sluggishly in recent years. The Economic Policy Institute estimates that each $100 spent on infrastructure increases private sector output by $17.

Given its broad benefits, wide scope, and essential nature, infrastructure investment sounds like a slam-dunk proposition for government investment. Yet substantial progress on this front has been elusive for the current administration, as with many before it. Infrastructure programs are not cheap, and this may have dissuaded some members of Congress from supporting them. The president’s first term priority was a tax reduction that will significantly increase the size of the federal deficit over time.

But delaying infrastructure investment risks decay and obsolescence. The American Society of Civil Engineers publishes an annual Infrastructure Report Card that most recently gave overall U.S. infrastructure a barely-passing D+ grade. The World Economic Forum ranked the U.S. as having just the 13th best infrastructure in the world. The cost of required maintenance currently runs in the trillions of dollars, and deferral comes at a cost; as an example, around 18% of the treated water supply is currently wasted due to broken water supply pipes.

“The U.S. infrastructure gap has grown to a shocking magnitude.”

Motorists can feel the infrastructure gap. Aversion to tax increases has kept federal gasoline taxes at 18.4 cents per gallon since 1993. States and municipalities add their own taxes, but the overall low level of funding for road maintenance is evident in rough streets and aging bridges.

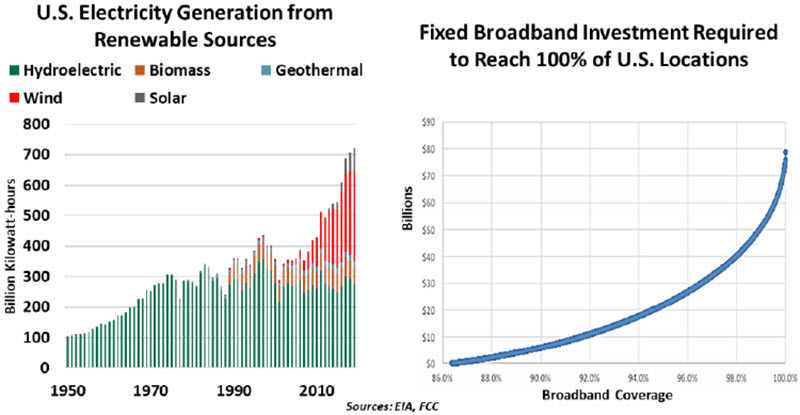

Filling potholes is important, but new infrastructure deserves increased attention. The pandemic has laid bare the need for broadband: now that our jobs, education and some medical care have moved online, it is clear that every household should have access to high-speed internet. 5G wireless service is becoming available, bringing high speed and high potential. And with each passing year, sustainable energy generation becomes more cost-effective, justifying investments in the transmission grid.

Infrastructure investment is also a great opportunity for government to stimulate a struggling economy. The Depression-era Works Progress Administration ran thousands of projects to create jobs. The American Recovery and Reinvestment Act of 2009 funded “shovel-ready” projects to fight high unemployment. We could use that kind of economic stimulus now, as permanent job losses accrue and labor force participation falls. And with government bond yields at historic lows, the cost of financing an infrastructure package would not be too burdensome.

Presidential candidate Joe Biden’s campaign has stressed the potential of infrastructure investment, prominently featuring the candidate’s history of commuting from his home in Delaware to Washington, D.C. on an Amtrak train. But Biden’s agenda impractically includes nearly every possible investment. It gives little direction as to which projects will be the highest priorities, and contains only vague funding proposals. Much recent commentary has contemplated the consequences of a “blue wave” that would lead to more expansive government spending. But that spending must first focus on addressing COVID-19, with further advancements competing with a crowded field of priorities, like healthcare, in a challenging fiscal context.

President Donald Trump’s first-term infrastructure priority was to encourage public-private partnerships (P3s). P3s build, operate and maintain infrastructure assets and collect the revenue they generate. P3s are a worthwhile approach to funding revenue-generating assets, such as toll roads, airports and university facilities. They have been successful around the world, but their adoption has been slow in the U.S. Some P3s have shown poor results, giving investors and communities pause about entering new ones.

“Public-private partnerships can help finance infrastructure, but they are not a panacea.”

Even when executed well, P3s are not a panacea. The 2019 White House budget proposal called for $1.3 trillion in private infrastructure investment on top of only $200 billion of public spending, a modest sum. Many necessary projects will not generate fee income, limiting the potential for P3s.

In the long run, the U.S. would do well to create a national fund to invest in domestic priorities, like the European Investment Bank or the Australian Future Fund. Infrastructure projects have lifecycles far exceeding the tenure of most politicians, and long-term development needs are not matters of political debate. A national infrastructure bank would separate decisions about federally funded infrastructure projects from the pork barrel politics of congressional earmarking. It would also spur job creation in manufacturing and construction. But for the United States, this is likely to be a bridge too far.

When confronted with too many options, such as an oversized restaurant menu, we will often fall back on our old favorites. In the U.S., the default option has been to defer our spending. Sooner or later, we will need to change course and make the necessary investment in our nation.

Hard Lessons

Carl makes the case for human capital investment.

Our daughter calls periodically from college to share a video chat. It’s always nice to see her and know that she is well, as COVID-19 has been active on her campus.

The interactions often find her curled comfortably on her bed. This is understandable; the vast majority of her classes are held virtually. But on occasion, we can hear a lecture taking place on her computer while she is talking to us on the phone. Given the tuition we are paying, we are less sympathetic to this; we advise her to hang up and focus on her studies.

The pandemic has been especially disruptive for students and their families. But American education was facing important challenges prior to COVID-19, challenges that may become more difficult after the virus is contained. Well-crafted policies to bolster the formation of human capital will be critical to sustaining U.S. economic growth in the years ahead.

Learning from home is not going well. Pupils were sent away from school last spring as a safety measure, leaving educators at all levels scrambling to provide lessons online. Technology hasn’t always been cooperative, and many students lack access to reliable internet connections. The interaction of the classroom has been difficult to reproduce. Parents, many of whom have been dealing with their own professional dislocations, have struggled to provide oversight and tutoring.

We’re now beginning to understand the costs of distance instruction. Primary and secondary school achievement has slipped, and the difference between those doing well and those doing poorly has grown. The long-term consequences of the lost class time could be substantial. As it appears restrictions on indoor gatherings will continue for some time, society will need to up its distance learning game…quickly. Unfortunately, budget constraints at the state and local levels threaten to hinder progress.

As we wrote last spring, the pandemic has been disastrous for U.S. colleges and universities, which have been starved for revenue. They have responded with increasingly severe rounds of cost cutting. Some observers will certainly note that a rationalization of the costs of higher education was long overdue. But the abruptness and scale of the austerity has caught students and faculty members off guard.

“Less than 40% of Americans have a college degree.”

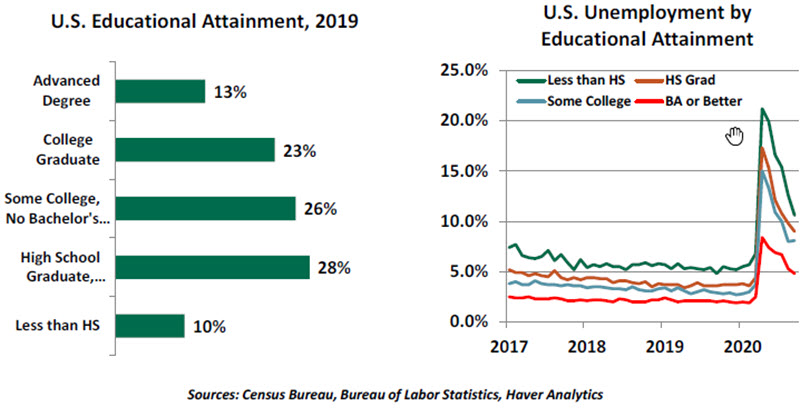

It is hard to overstate the importance of education to society. Learning deepens specific skill sets, enhances problem solving, and makes the labor force more adaptable to change. It is a key ingredient in productivity, which fosters economic growth and competitiveness. Schooling offers students opportunities to advance, and a well-educated population makes good political and policy choices.

The data consistently illustrate the importance of education to economic outcomes. U.S. college graduates can expect to earn hundreds of thousands of dollars more than high school graduates during their working lifetimes, and they are about half as likely to be unemployed at any given time. Yet less than 40% of Americans hold college degrees.

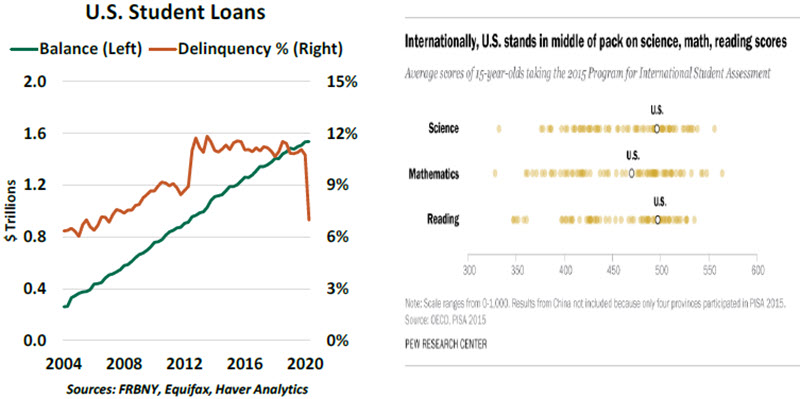

One reason is that the cost of getting a degree has become prohibitive for many families. Tuition rates have routinely risen by twice the rate of inflation over the past generation; while aid defrays some of that expense, completing college leaves many students deeply in debt. Forty-five million Americans owe a total of $1.6 trillion on student loans.

We’ve written about student debt on a number of occasions (our most recent exposition can be found here). Potential reforms include tighter licensing for for-profit colleges, many of which have poor graduation rates and high loan default rates. About 35 million Americans have some college but no degree; they have debt, but no diploma. Counseling these students before they enter school and helping them complete college if they start would make debt levels more manageable. Tying loan payments more closely to a student’s ability to repay (the practice in many other countries) would be another strategy.

The issue of who should pay for college has been actively debated this campaign season. U.S. taxpayers have financed public education through grade 12 for over a century. When the practice started, a high school education was enough to prepare young people for a wide range of occupations; today, it is barely sufficient. In recent decades, Congress has passed a series of aid programs to help students foot the bill for college, but the current administration has proposed cutting them back.

On the other end of the spectrum is the progressive proposal to make college free for anyone who might want to go. Critics of this approach note that some occupations do not require a baccalaureate; for some technical professions, apprenticeship programs are more effective. The effort would certainly be costly, although the introduction of a single-payer system might contain the cost of college.

“Budget troubles at all levels of government will challenge funding for education.”

Space does not allow for a fulsome discussion of issues related to primary and secondary education in America, which also requires careful attention. U.S. student achievement has fallen behind that of other countries, and educational outcomes have become more uneven. The proper formula for school funding remains a point of policy debate, as is the best way to reinforce accountability for educational attainment among administrations, teachers and households.

The near-term challenges presented by COVID-19 will add to the significant long-term challenges facing American education. The pandemic is forcing cuts in learning budgets at a time when learning is becoming more important. The pandemic is also accelerating the advance of technology in many areas, which will create opportunities and risks for the U.S. labor force. If workers are not educated and adaptable, economic dislocation could ensue.

Our daughter hopes to eventually get a doctorate in physical therapy, to work in the field of rehabilitation. Our educational system is in dire need of some rehabilitation; its recovery will be essential to the nation’s long-run health.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2020 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit our terms and conditions page.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All