Red, Blue or Both? Still A Bullish Scenario For Stocks

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs I write this, former vice president Joe Biden has not yet been named president-elect, but with him leading in the crucial battleground states of Pennsylvania and Georgia, it looks more and more likely that he will be sworn in this January.

The market seems to have predicted this outcome. If the S&P 500 is up between July 31 and October 31 before an election, it has historically favored the incumbent party. And if it’s down, it has favored the challenger. Following a loss of 5.6% last week, the S&P was underwater about 4 basis points from the end of July.

Many of you reading this are no doubt disappointed. In a poll I ran back in August, 76% of you said you believed President Donald Trump would be better for the stock market than Biden.

I’m here to tell you there’s probably no need for handwringing at this point, especially since projections of a “blue wave” did not materialize. The Democrats were not able to flip the Senate, managing only to keep control of the House.

|

Investors were strongly in favor of this development, with the S&P ending the week up 7.3%. This is a very good sign for stocks for the rest of the month and year. According to my good friend Pimm Fox, “the direction of the S&P 500 did not change from the period beginning the day after the election for the remainder of November, nor for the rest of the year.”

If history is any indication, a Biden presidency and divided Congress may very well end up being the most favorable outcome for equities. With Republicans controlling the Senate, we’re less likely to see hugely consequential legislation passed such as massive tax hikes, drug pricing limits, nationalized health care and spending for the Green New Deal. Both chambers will need to compromise to pass another stimulus package. Other policy may continue to be made mostly by presidential executive order, which can easily be rolled back by the next president.

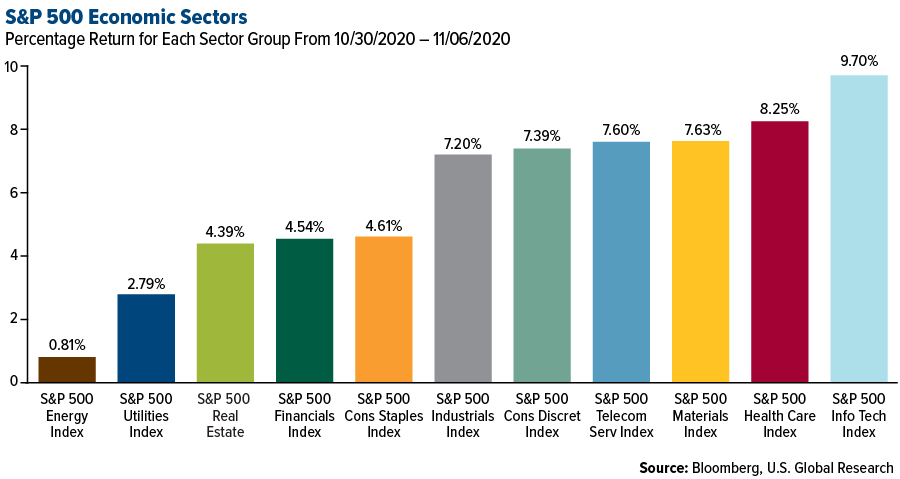

Businesses love Congressional gridlock for this very reason. Tech stocks had been trending down for days before the election as they faced antitrust scrutiny, but now that it appears certain Congress will remain divided, they’ve recovered most of their losses. The tech-heavy Nasdaq 100 jumped close to 10% for the week.

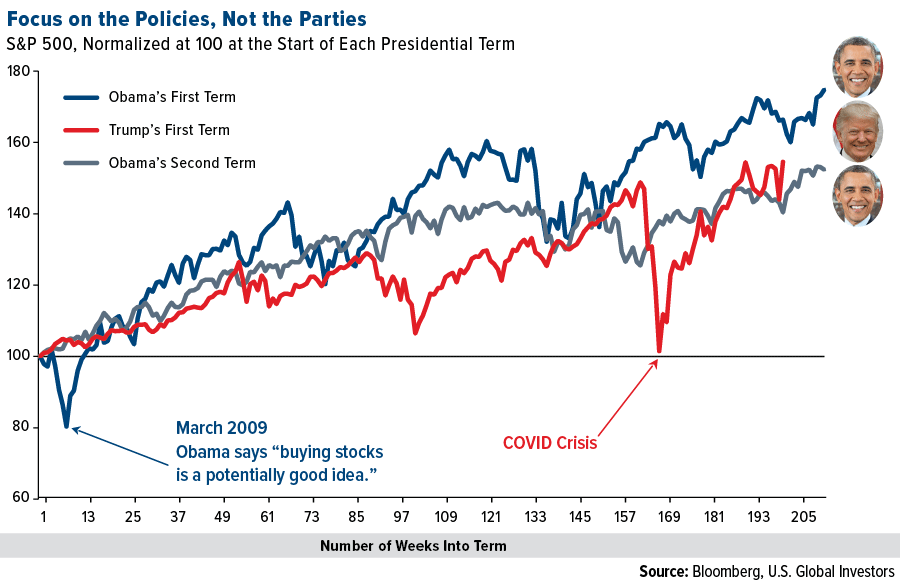

Focus on the Policies, Not Necessarily the Parties

Below is a chart I shared with you two years ago, after the 2018 midterm elections. Looking all the way back to 1928, average annual stock returns were highest (16%) when there was a Democratic president and split Congress, according to Bank of America (BofA). One caveat: This particular setup has a very small sample size, seen only in the last four years of President Barack Obama’s eight-year administration.

The largest sample size is when there was a Democratic president and Democratic Congress, seen in 34 out of 89 years. During those years, average returns were a still attractive 14%.

The reason I point that last part out is because you may be wondering about the ramifications should Democrats take full control of Congress in 2022. By my count, 22 Republican senators will face reelection that year, giving Democrats an opportunity to flip the upper chamber.

As I frequently say, it’s not the party that matters, but the policies. We believe government policy is a precursor to change, and that money can be made in America no matter who’s in charge. Case in point: Stocks recovered nicely in Obama’s first term following the housing market crash, despite there being a legislature controlled by Democrats. Health care stocks, in particular, were big winners between January 2009 and January 2013, rallying more than 80%.

Time to Hedge for Hyperinflation? Gold Above $1,950, Bitcoin at $16,000

At the same time, I don’t want to minimize the inflation risk if Biden is able to get more extreme left-wing legislation passed. Modern monetary theory (MMT) is a real threat I’ve written about before, most recently last week, when it was reported that Massachusetts senator Elizabeth Warren may be interested in a Cabinet position as Treasury secretary. Vermont senator Bernie Sanders, a self-proclaimed “Democratic Socialist,” may also end up with a role in Biden’s Cabinet, as Labor secretary.

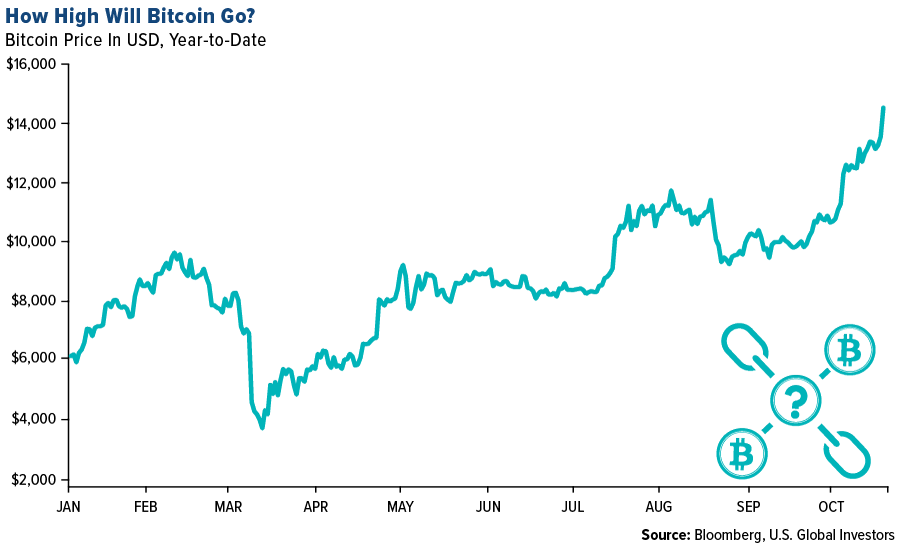

Among the inflation hedges CLSA analysts highlighted this week are gold and bitcoin. Indeed, this week has been highly constructive for both assets, with gold advancing nearly 4% to trade above $1,950 an ounce. Bitcoin was trading above $16,000 today for the first time since January 2018.

Holdings in gold-backed ETFs have had an incredible run this year as investors seek a safe haven. Such products saw their 11th straight month of positive inflows in October, bringing total global holdings to over 110.8 million ounces, according to Bloomberg data.

Thanks to higher metal prices and investor interest, gold mining equities have lately been cash flow machines. Gold royalty companies, including Franco-Nevada and Royal Gold, reported record revenues in the third quarter. Franco reported close to $280 million in revenues, up 43% quarter-over-quarter (qoq) and approximately 19% year-over-year (yoy). Royal Gold reported $147 million, up 22% qoq and 27% yoy.

I have high expectations for Wheaton Precious Metals, which is scheduled to report this Monday.

Buffett’s Midas Touch Is Back

Another company that had a blowout quarter was senior producer Barrick Gold. The company reported record free cash flow of more than $1.3 billion. On a per-share basis, free cash flow growth was up 155% from both the previous quarter and the same time last year. Shares of Barrick closed up nearly 7% yesterday on the news.

If you recall, Warren Buffett bought shares of Barrick in the second quarter, after he bashed gold for years because it doesn’t pay a dividend. (And yet neither does Berkshire Hathaway.) Perhaps Buffett’s Midas touch is back?

Kirkland Lake also released stellar financial data on higher gold prices. Free cash flow came in at 273%, with per-share growth up an incredible 200% yoy and 15% qoq.

321gold.com founder Bob Moriarty and I discussed both companies in greater detail during our webcast this week. In case you missed it, you can watch the replay by clicking here. I know you’ll love the slides!

Biden’s $400 Billion Manufacturing Plan

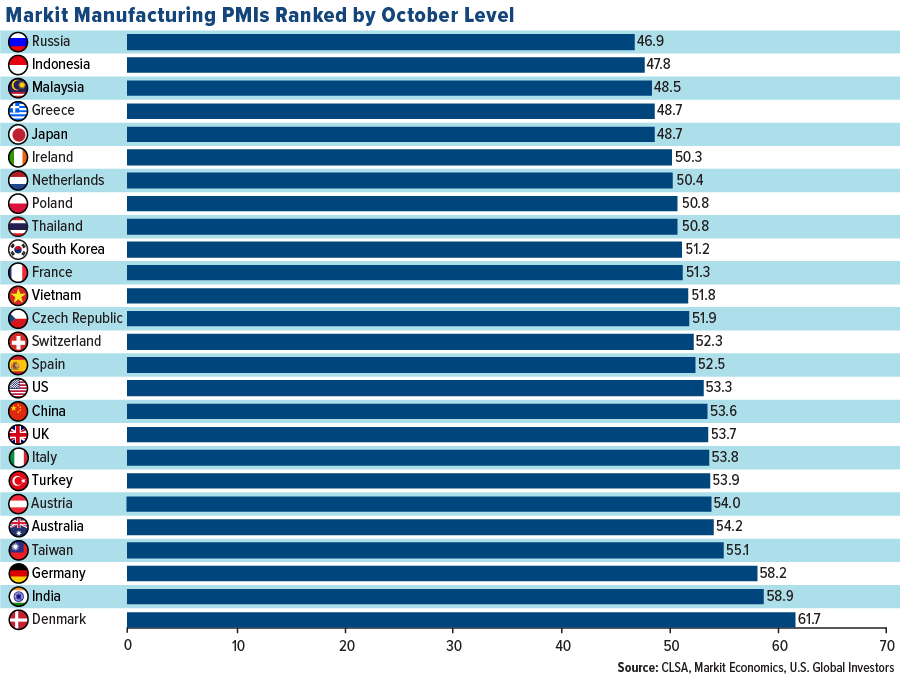

Under President Trump, the manufacturing sector has been very strong, even post-COVID. Last month, the U.S. purchasing manager’s index (PMI) came in at 53.3, which is on the higher end of countries ranked by PMI.

I don’t anticipate this changing or weakening under a President Biden. In July, the former vice president unveiled a four-year, $400 billion package to spur manufacturing and $300 billion for research and development. The goal is that the plan would create as many as 5 million jobs, many of them to replace those lost due to the pandemic.

Passing such a package may be difficult with Republicans in charge of the Senate, but should it become law, I expect demand for commodities and raw materials to benefit.

Gold Market

This week spot gold closed at $1,951.35, up $72.54 per ounce, or 3.86%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 10.62 percent. The S&P/TSX Venture Index came in up 8.56 percent. The U.S. Trade-Weighted Dollar fell 1.84%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-1 | Caixin China PMI Mfg | 52.8 | 53.6 | 53.0 |

| Nov-2 | ISM Manufacturing | 56.0 | 59.3 | 55.4 |

| Nov-3 | Durable Goods Orders | 1.9% | 1.9% | 1.9% |

| Nov-4 | ADP Employment Change | 643k | 365k | 753k |

| Nov-5 | Initial Jobless Claims | 735k | 751k | 758k |

| Nov-5 | FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Nov-6 | Change in Nonfarm Payrolls | 580k | 638k | 672k |

| Nov-10 | Germany ZEW Survey Expectations | 41.9 | -- | 56.1 |

| Nov-10 | Germany ZEW Survey Current Situation | -65.0 | -- | -59.5 |

| Nov-12 | Germany CPI YoY | -0.2% | -- | -0.2% |

| Nov-12 | Initial Jobless Claims | 725k | -- | 751k |

| Nov-12 | CPI YoY | 1.3% | -- | 1.4% |

| Nov-13 | PPI Final Demand YoY | 0.4% | -- | 0.4% |

Strengths

- The best performing precious metal for the week was palladium, up 12.64%, despite hedge funds cutting their positioning to a 10-week low. Gold had its best weekly gain since July as Joe Biden moves closer to winning the presidential election and on prospects for further Federal Reserve stimulus. The yellow metal hit a six-week high, also boosted by the declining U.S. dollar. Velocity Trade Capital analyst Michael Siperco wrote this week that the election outcome won’t change gold’s bullish trend as the longer-term macro outlook is already well established to support the metal.

- Barrick Gold reported its highest quarterly revenue since its 2019 merger with Randgold on stronger bullion prices. The second-largest gold producer announced $3.54 billion in revenue for the quarter ended September 30. Barrick raised its dividend by 12.5% to 9 cents a share.

- AngloGold Ashanti also doubled its dividend payout ratio due to surging gold prices. Bloomberg notes the world’s third-largest gold producer will now return 20% of free cash flow before growth capital to shareholders. In the September quarter, AngloGold’s free cash flow rose nearly fourfold to $339 million.

Weaknesses

- The worst performing precious metal for the week was gold, but still up 3.86%. Anglo American Platinum lowered its refined output and sales guidance after shutting its second smelting plan due to water leaks, reports Bloomberg. The company said the shutdown will cut earnings before interest, taxes, depreciation, and amortization by $380 million.

- Kinross Gold reported revenue for the third quarter of $1.13 billion, below the average estimate of $1.17 billion. Revenue was still up 29% year-over-year. Gold production was down slightly year-over-year to 603,312 ounces.

- The President of Ghana is asking for a second parliamentary review of the country’s proposed gold royalty fund after an initial probe raised concerns, reports Bloomberg. The $500 million IPO was suspended last month after calls by opposition groups who criticized the lack of transparency in the fund.

Opportunities

- VTB Bank PJSC, Russia’s second-biggest lender and top gold buyer, is betting on precious metals to boost profits. The bank is prioritizing physical gold trading and lending to mining companies as they are one of the few sectors to benefit from the pandemic, said First Deputy Chairman Yuri Soloview in an interview. Bloomberg reports that the bank said it plans to start the first Russian ETF backed by bullion.

- The Reserve Bank of India said in a report that it is considering diversifying the pool of assets it invests its foreign reserves in, and may increase purchases of gold and dollars, according to Reuters. The report also noted that the bank has already gradually increased gold investments.

- Rich Ross, CMT of Evercore ISI, noted that “We are living in a material world without inflation, which is genius!” Buy compelling breakouts in gold and silver fueled be the weaker dollar and the inevitability of more stimulus.

Threats

- The Veladero gold operation in Argentina is selling only enough bullion to keep the mine running due to currency restrictions, said Barrick Gold CEO Mark Bristow on the third-quarter conference call. “Due to the ongoing financial crisis in Argentina, the government has maintained currency restrictions and the forced repatriation of export sales into pesos.” Veladero has had a difficult time due to the nationwide quarantine and winter weather has delayed two projects.

- Dan Barclay, head of Bank of Montreal capital-markets division, which is the mining industry’s top dealmaker, said that few deals will get done without greater clarity on the economy and pandemic. “There’s lots of conversations going on, lots of people exploring new ways to think and new ways to operate. The probability of a lot of action is going to be conditional on that economic recovery.” According to Bloomberg data, mining companies have been involved in $52 billion worth of acquisitions in 2020, which is less than half the value of deals seen during industry consolidation in the mid-2000s.

- Southwest Airlines warns workers of first layoffs in company history as just a slice of the estimated 174 million jobs that are expected to be lost by the World Travel & Tourism Council this year due to COVID-19 travel restrictions. With new virus cases exceeding 100,000 per day now in the U.S. it will become increasingly difficult to navigate a clear path to recovery.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 6.87 percent. The S&P 500 Stock Index rose 7.42 percent, while the Nasdaq Composite climbed 9.01 percent. The Russell 2000 small capitalization index gained 6.94 percent this week.

- The Hang Seng Composite gained 6.96 percent this week; while Taiwan was up 3.40 percent and the KOSPI rose 6.59 percent.

- The 10-year Treasury bond yield fell 5 basis points to 0.823 percent.

Domestic Economy and Equities

Strengths

- Employment growth was better than expected in October and the unemployment rate fell sharply even as the U.S. faces the challenge of surging coronavirus cases. The Labor Department reported Friday that nonfarm payrolls increased by 638,000 and the unemployment rate was at 6.9%.

- The Institute for Supply Management (ISM) said on Monday its index of national factory activity increased to a reading of 59.3 last month, writes CNBC. That was the highest since November 2018 and followed a reading of 55.4 in September.

- Arista Networks was the best performing S&P 500 stock for the week, increasing 25.90 percent. The company reported results for the third quarter of 2020 that beat expectations on both the top and bottom lines. Further, management guided for strong revenue growth in the upcoming fourth quarter.

Weaknesses

- National nonresidential construction spending fell 1.6% in September, according to an Associated Builders and Contractors analysis of data published today by the U.S. Census Bureau. On a seasonally adjusted annualized basis, monthly spending totaled $794.3 billion. Among the sixteen nonresidential subcategories, thirteen were down on a monthly basis.

- U.S. productivity gains cooled in the third quarter, writes Bloomberg, despite the record pace of economic growth, as a surge in output was accompanied by a huge increase in hours worked. Nonfarm business employee output per hour increased at a 4.9% annualized rate from July through September, according to Labor Department data released Thursday.

- Hanesbrands was the worst performing S&P 500 stock for the week, falling 20.04%. Shares plunged as the company reported a review of its busines and a slump in sales at a time when everyone’s wearing leisure clothing.

Opportunities

- A report published by Citigroup Inc. strategists notes they expect all post-election scenarios to be bullish for municipal, both tax-exempts and taxables. Their reasoning boils down to three key considerations: It follows that a Democratic sweep is the best-case scenario, as it would pave the way for a larger fiscal-aid package, higher taxes and more infrastructure spending. The “least bullish” would be Joe Biden winning the presidency while Republicans hold the Senate, with a status quo election falling somewhere in the middle. The muni-Treasury ratio, which is how investors typically measure relative value between municipals and treasuries, is currently around 107% for the 10-year ratio. That’s higher than any point from late 2016 through February.

- Legal marijuana is becoming the American norm, writes Bloomberg, as ballot measures passed in Arizona, Mississippi, Montana, New Jersey, and South Dakota, adding to the 33 states that already allow it for medical or recreational purposes. Adult-use pot will be legal in 15 of those states.

- Uber and Lyft shares jumped over 15% after California voters approved a proposition to continue classifying their drivers as independent contractors instead of employees.

Threats

- Many governments are setting tighter restrictions as COVID-19 infections spike. Europe has been battered by the resurgent virus, with many countries choosing some form of lockdown to halt the spread. Cases are also surging in the U.S., especially in the Southwest and Midwest.

- We know more about the DOJ trying to halt the Visa-Plaid merger. The Department of Justice is alleging Visa's motivation for acquiring the fintech stems from a desire to limit the startup's competitive threat to its $4 billion debit business.

- JPMorgan Chase & Co. is getting bearish on Manhattan apartments, according to Bloomberg. The lender will tighten the terms of mortgages it finances for most co-operatives and condominiums in the borough, according to a Nov. 4 notice sent to loan professionals. Chase will limit jumbo loans to 70% of the sale price starting next week, down from 80%. Slackening buyer demand has sent Manhattan sales plummeting during the Covid-19 pandemic.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was lumber, up 6.38%, with no letup in housing demand. Copper, along with gold, had its best weekly gain since June as Joe Biden inches closer to winning the drawn-out U.S. presidential election as the dollar falls. Clean energy investors saw a boost from the potential Biden victory. The S&P Global Clean Energy Index hit a record on Thursday, as Biden appears closer to the presidency and has a $2 trillion clean energy plan.

- Higher gold prices are pushing the world’s top miners to increase dividends for shareholders. Barrick, the second-largest gold producer, announced $3.54 billion in revenue for the quarter ended September 30 and raised its dividend by 12.5% to 9 cents a share. AngloGold Ashanti also doubled its dividend payout ratio. Bloomberg notes the world’s third-largest gold producer will now return 20% of free cash flow before growth capital to shareholders. In the September quarter, AngloGold’s free cash flow rose nearly fourfold to $339 million.

- Several metals rose on Tuesday after Chinese President Xi Jinping said the economy can double in size by 2035. China is pushing for electric cars to be 20% of new car sales by 2025, which is a big boost for the metals used to produce them. Copper rose 1.3% and nickel was up 1.7% on the news. In landmark rule move Colorado’s Oil and Gas Conservation Commission voted 5-0 to ban routine flaring and venting at oil and gas well sites to mitigate climate change.

Weaknesses

- The worst performing commodity for the week was natural gas, down 13.77% on unseasonably mild temperatures as we enter November. Crude oil fell below $38 a barrel on Thursday as investors weigh news that the U.S. became the first country to hit over 100,000 new COVID cases in a single day. The demand outlook continues to worsen, and the glut of oil grows. Royal Vopak NV, the world’s largest independent oil storage producer, said it has no open space at its key locations in the Netherlands, UAE and Singapore, reports Bloomberg.

- According to Chile’s National Mining Society, Chile will see investment in copper mining lag for at least two years as the country rewrites a constitution that underpinned nearly 30 years of mining growth, reports Reuters. Large new projects are unlikely until there is clarity around the new constitution and what it might include. Several issues are being discussed that could impact mining such as indigenous rights, environmental protections and worker benefits.

- Iron ore had its third weekly loss in the past four as port stockpiles in China hit 130.8 tons, the most since February. Traders remain uncertain about the short-term outlook as demand weakens and exports increase from top producers Brazil and Australia.

Opportunities

- Tanzania is in the final stage of approving a permit for the country’s first rare earths mine to Australia’s Peak Resources Ltd., reports Bloomberg. The East African nation is seeking a bigger share of revenue from natural resources and is also approving a gold mining license for OreCorp Ltd. Tanzania is the continent’s fourth biggest gold producer and hopes to increase mineral earnings by a third in the next three years.

- Top lithium producer Albermarle Corp says the metal would benefit from a Joe Biden victory. CEO Kent Masters said in a phone interview with Bloomberg that “the market side of it would be more favorable with Biden” since there are incentives for electrification and electric vehicles. Another benefit of a Biden presidency could be less friction around trade and a less antagonistic approach with China, could help the lithium-ion battery supply chain.

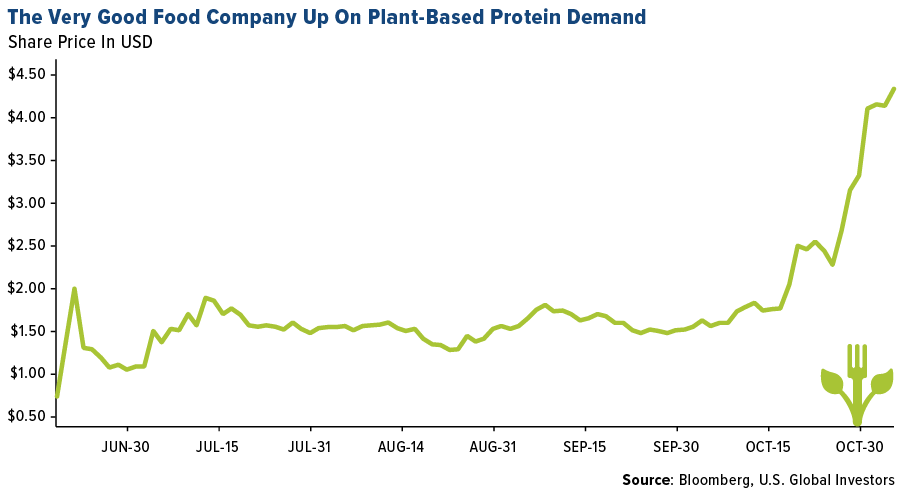

- The market for plant-based protein alternatives is surging at a frantic pace, which is positive for companies such as Beyond Meat, Else Nutrition Holdings and The Very Good Food Company. The latter of those three companies went public in June and has since seen its shares surge in Canada. The Very Good Food Company partnered with Pamela Anderson to bring awareness to meat alternatives and signed a wholesale distribution partnership with UNFI Canada.

Threats

- The world’s biggest solar power company, China’s Longi Green Energy Technology Co., said a shortage of glass is raising costs and delaying production of new panels. Bloomberg notes that prices for glass covering photovoltaic panels have risen 71% since July, as manufacturers struggle to keep up with soaring demand. This could slow down the transition to green energy and adoption of solar technology if prices continue to rise.

- Trade tensions between China and Australia, two top commodity producers, heated up this week after China ordered traders to stop purchasing at least seven categories of Australian commodities. “China seems determined to punish Australia and make it an example to other countries,” said Richard McGregor, a senior fellow at Sydney-based think tank the Lowy Institute. “They want to show there’s a cost for political disagreements.” Australia has called for an independent probe into the origins of the coronavirus, ramping up tensions that were already high after blocking Huawei in 2018.

- The EU is mulling “green certificates” for liquefied natural gas (LNG) imports as a way to put pressure on global exporters of LNG, as part of the continent’s efforts to slash fossil fuel pollution across the entire production chain. Last month Engie SA shelved plans to buy LNG exporter NextDecade after environmental groups lobbied the French utility to drop the deal on pollution concerns.

Airline Sector

Strengths

- The best performing airline for the week was Azul SA-ADR, up 21.35%

- IndiGo, India’s largest airline, is in talks for its next batch of jet engine orders, according to people familiar with the matter. This is a rare deal in the airline sector that has been paralyzed by decimated travel. IndiGo is in talks with Pratt & Whitney and CFM International about engines to power 150 new Airbus A320neo jets.

- Major airlines are ramping up efforts to attract travelers, with some offering 2-for-1 deals and other big promotions. AirAsia, Malaysia’s largest airline, is offering unlimited flights within the country at a fixed price to help stimulate domestic tourism. Ryanair is giving customers a buy one, get one free ticket on flights across the United Kingdom, reports CBS News.

Weaknesses

- The worst performing airline for the week was Hawaiian Holdings, completely flat at 0.00%.

- England banned overseas air travel until December 2 in a move to help curb its resurgence of coronavirus infections. Bloomberg reports that airlines had not been informed of the restrictions prior to Prime Minister Boris Johnson’s announcement on Saturday. Carriers were thrown into a fresh crisis to deal with the even further reduced travel demand.

- Lufthansa, Europe’s biggest airline, said in an earnings release that capacity development must increase from 25% of year-ago levels to about 50% in order to meet its goal of returning to positive operation cash flow in 2021, reports Bloomberg. Shares are down 51% so far in 2020. The carrier said some progress has been made to stop the bleeding cash, predicting that operating cash drain will be limited to $411 million a month this quarter.

Opportunities

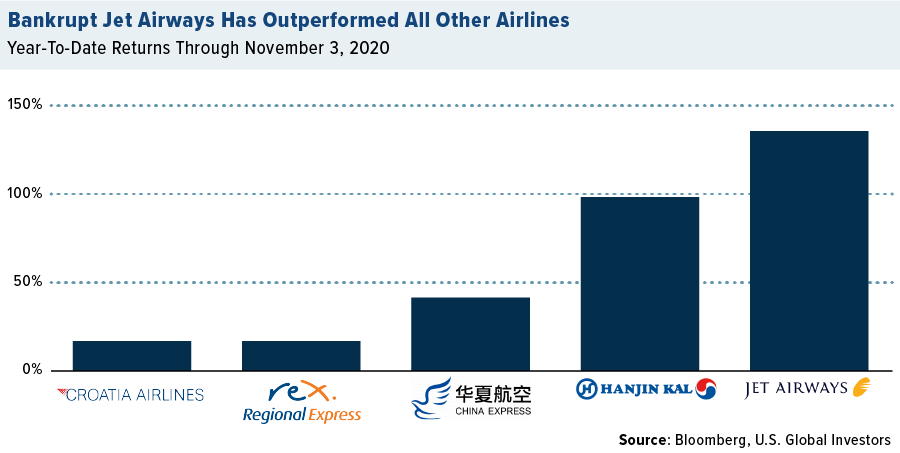

- The world’s best-performing airline stock so far in 2020 is bankrupt Indian carrier Jet Airways India Ltd. The stock has surged nearly 150% this year versus the 42% drop in the Bloomberg World Airlines Index, which tracks 27 of the world’s largest carriers. The carrier is up on investor hopes that it will successfully emerge from a restructuring. Bloomberg reports almost 17,000 creditors are seeking claims of around $3.4 billion, and it does not have any employees and hardly any landing slots.

- Air France-KLM shares rose on Thursday after the Netherlands gave approval to a $4 billion bailout after pilots agreed to wage caps that could last for five years. The bailout for the Dutch arm of the carrier is tied to a 15% cost reduction plan to boost profitability.

- Japan Airlines said it will raise as much as $1.6 billion via an overseas and domestic share sales and will use the proceeds to reduce debt and strengthen finances, reports Bloomberg. The shares will be offered at a 3% to 6% discount. The carrier hopes to weather the pandemic rut without any major job cuts.

Threats

- U.S. pilot unions say the Federal Aviation Administration (FAA) should improve its proposal for training pilots how to handle a nose-down pitch of the Boeing 737 Max, which has been grounded due to crashes related to that malfunction. AP reports the union representing Southwest pilots said the number of steps to remember and carry out in that type of emergency is too many and could increase error rates. The pilots also said in the simulator it was difficult to recall all the steps in order. This could further delay the return of 737 Max jets to the sky.

- A surge in coronavirus cases in England resulted in a new one-month travel ban. With cases growing all over Europe, lockdowns could continue and hurt air travel even further. Ryanair CEO Michael O’Leary said in a Bloomberg TV interview that there’s “risk to the downside” with new travel curbs.

- An entire Southwest Airlines flight from Nashville to Las Vegas was forced to deplane before takeoff on Tuesday after a passenger refused to wear a mask and would not leave the plane, reports Fox News. Mask policies continue to cause problems on flights and could deter travelers from flying – both those who won’t wear a mask and those worried that flights are not safe during the pandemic.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Poland, gaining 10.6 percent. The best performing country in Asia this week was South Korea, gaining 6.6 percent.

- The Czech koruna was the best performing currency in emerging Europe this week, gaining 4.5 percent. The Indonesian rupiah was the best performing currency in Asia this week, gaining 3.6 percent.

- Manufacturing in India climbed to the highest level in over a decade. The IHS Markit India manufacturing purchasing managers’ index (PMI) rose to 58.9 in October from 56.8 in September. China’s manufacturing PMI remined strong in October at 51.4 as well, although slightly weaker than the September reading of 51.5.

Weaknesses

- The worst relative performing country in emerging Europe for the week was Czech Republic, gaining 2.7 percent. The worst relative performing country in Asia this week was Vietnam, gaining 1.4 percent.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 2 percent. The Vietnamese dong was the worst relative performing currency in Asia this week, gaining 5 basis points.

- Europe continues to impose new restrictive measures to prevent the spread of the coronavirus. This week Poland, with a population of 38 million, reported 25,000 daily new infections, compared to the United States with 330 million people reporting more than 100,000 infections a day. Greece announced nation-wide lockdowns until the end of the month, and Poland is expected to announce more restrictions this weekend.

Opportunities

- The Communist Party of China released its five-year and long-term economic plan. GDP per capita should reach the middle level of advanced economies by 2035 with income per capita doubling. This implies an average GDP growth of 4.73 percent from 2021-2035. JPMorgan predicts 8.7 percent GDP growth in 2021, mainly due to a low base in 2020.

- China aims to achieve carbon neutrality in 2060, which will likely deepen its de-carbonization efforts. China hopes 20% of the country’s energy consumption to be renewable by 2025, five years earlier than its prior target. Renewable energy stocks look set for further upside.

- European Union negotiators reached a preliminary deal on a mechanism linking the recovery fund to the adherence of democratic standards. The eurozone will start distributing the much-needed recovery fund of 750 billion euros in January 2021. In Western Europe, Italy and Spain will be the biggest beneficiaries and in central emerging Europe, Poland is set to get the largest amount. .

Threats

- Although U.S. presidential voting is behind us, the political uncertainty remains as it may take days if not weeks for the world to know the outcome of the November 3rd election. For now, global emerging equites have recorded gains and currencies appreciated sharply against the dollar. However, uncertainty usually leads to more volatility and sharp price reversals.

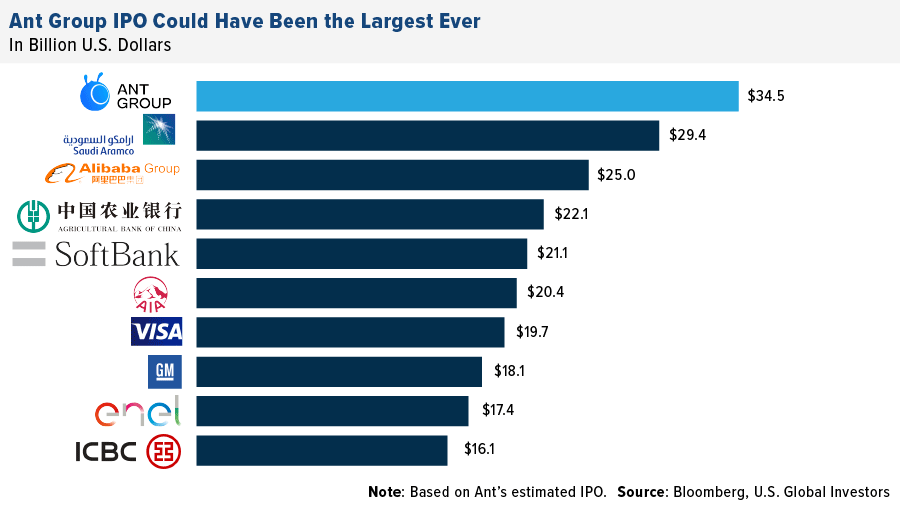

- Last week Ant Group IPO raised $34.5 billion, but this week, just days before its debut, China announced that shares will not be listed on the Hong Kong or the Shanghai Stock Exchange as previously planned due to regulatory changes. The IPO is expected to be delayed by about six months, and funds will be returned to investors in the meantime, according to news portal QQ.com.

- Eurozone manufacturing PMI was reported at 54.8 in October, up from 54.4 in September. However, the index may shrink in coming weeks due to the nationwide lockdowns that eurozone members started to implement recently. Due to the second wave of the virus in Europe and the new lockdown, GDP may contract in the fourth quarter and next year’s recovery may be much weaker than previously announced.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended November 6 was Chainpay, up over 9,000%.

- The U.S. presidential election winner is still undecided, and bitcoin is experiencing a major rally, reports CoinTelegraph. Today the popular digital currency nearly reached $16,000, which is the highest level it has seen since January.

- According to Tether’s official transparency data, the USDT market cap crossed a $17 billion mark for the first time, writes CoinTelegraph, hitting over $17 billion in total assets. In fact, as of mid-September, Tether’s market cap had seen nearly a four-fold increase since the beginning of the year.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended November 6 was Crypto Price Index, down 98%.

- The bullish momentum enjoyed by the security token market in the first three quarters of the year has subsided, writes CoinTelegraph, with monthly volume crashing by more than 40 percent for the second time in a row. The monthly security token trade was at $22 million in August, slumped to $9.15 million in September, and finally slid to $5.27 million in October.

- The U.S. is suing for the forfeiture of thousands of bitcoins totaling more than $1 billion (that it recently seized), the Department of Justice said on Thursday. As reported by CoinDesk, the seizure was tied to an early darknet market Silk Road and is the largest the U.S. has ever conducted. The seized funds include over 69,370 bitcoin and nearly equivalent amounts of forked cryptos bitcoin cash (BCH), bitcoin gold (BTG) and bitcoin satoshi vision (BSV).

Opportunities

- As reported by CoinTelegraph, AP News published U.S. presidential election results on the blockchain this week. Using blockchain-based technologies provided a secure and unhackable record of the state-by-state results as they came in, the article explains.

- Australian Senator Andrew Bragg believes that blockchain technology can solve a number of major regulatory issues in his home country, writes CoinTelegraph. Bragg specifies that the technology is a useful took in reducing complications associated with financial regulatory compliance and transparency, adding that it can also solve major problems associated with time zones.

- As the price of bitcoin rallies, some observers say the move is being driven higher by retail greed and the fear of missing out (FOMO). However, Google data suggests otherwise, writes CoinDesk. Google Trends is currently returning a value of 10 for the worldwide search query “bitcoin price,” which is significantly lower than the value of 93 observed in December 2017.

Threats

- In October, Binance was part of an exit scam that was executed by alleged automated market maker Wine Swap, who moved 19 different cryptocurrencies held in its address to a personal address. Luckily, in an announcement made Thursday, Binance said it has gained custody of an estimated 99.9% of the $345,000 worth of crypto that was stolen.

- Reversing a rally to $14,000 seen on Tuesday, bitcoin fell Wednesday by 3.3% alongside traditional markets after President Trump alleged “fraud” in the U.S. presidential election, writes CoinDesk, pledging to stop vote counting.

- Layer1 Technologies, a bitcoin miner, has been dragged into a lawsuit from a co-founder who claims he invested millions of dollars and was then forced out of the firm, writes CoinDesk. Plaintiff Jakov Dolic alleges that Layer1 CEO Alexander Leigl “falsely promised” that he would be able to raise $50 million from investors for a “large bitcoin mining operation.” However, the investments didn’t arrive, the article continues, so Dolic says he spent millions of his own funds to purchase a power substation (with the alleged understanding Leigl would refund him). Per the allegations, Dolic didn’t receive anything for his investment.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits