Key Takeaways „

- CLOs offer portfolios of floating-rate bank loans securitized across the rating spectrum. The availability of floating-rate bonds is limited in the U.S., and the choices for highquality floating-rate securities is even more limited, yet around 80% of CLOs carry a credit rating from A to AAA. „

- Relative to the investment-grade corporate credit market, CLOs have offered a consistent yield premium across the rating spectrum, in some cases as much as two times the yield offered over U.S. Treasuries. „

- In an environment where interest rates are low and the risk of higher Treasury yields has risen, allocations to AAA rated CLOs may help investors diversify a traditional fixed income portfolio, offering lower volatility, higher credit-quality and less sensitivity to any rise in interest rates.

CLOs are not a new asset class, but their availability to a wider range of fixed income investors is. CLOs have been a part of the vast securitized products market, which includes mortgage-backed securities (MBS) – the second-largest bond market in the world – for about 30 years. Like all securitized products, a CLO manager pools together different loans to create a portfolio in an attempt to produce a more diverse and more secure offering. MBS does this for home mortgages; CLOs do this for commercial bank loans.

A CLO is a portfolio of bank loans securitized into different instruments offering varying credit risk and thus varying credit ratings, although around 80% of CLOs carry a credit rating from A to AAA1.

Bank loans are issued to smaller companies that cannot typically access the bond markets. They carry credit ratings below investment grade, and are often used to refinance existing debt, finance acquisitions, or recapitalize the company. With over 70% of companies in America below investment grade, the market is large at over $1 trillion and includes many household names such as Chrysler, Dell and Avis2. In the last five years, the loan market has doubled, nearing the size of the U.S. high-yield bond market, which, at about $1.5 trillion in total assets, is considered one of the major fixed income asset classes3.

Until recently, investors that wanted to access the bank loan market had to individually analyze each loan, assess its risk and make an investment decision. The ability to buy a securitized portfolio of those loans was largely limited to institutional investors, such as banks, insurance companies and large asset management companies. But as the market has grown and new investment structures have come to market, CLOs are increasingly becoming the linkage between the needs of smaller companies seeking financing and investors seeking yield.

The U.S. Agencies, including Fannie Mae and Freddie Mac, use securitization when they issue mortgages to homeowners, create pools of the loans, add guarantees to improve the credit risk, and sell them on to investors in the form of mortgage-backed securities. Thanks to securitization, the U.S. mortgage market has grown to be an integral part of the U.S. economy.

CLOs offer AAA Ratings

Highly rated bonds are scarce in the U.S. fixed income market. Roughly 30 years ago, when the CLO market started, there were over 50 U.S. corporate bond issuers that were rated AAA. Today, there are two: Johnson & Johnson and Microsoft. Even the U.S. government lost its AAA rating, in 2011, when Standard & Poor's downgraded it to AA+. But AAA rated securities are the highest credit quality instruments that investors can buy, and for companies and governments the rating comes with some prestige and an aura of stability. Like the U.S. government (despite losing its AAA rating), AAA rated CLOs have never defaulted – not even in the Global Financial Crisis (GFC).4

CLOs offer Floating Interest Rates

Floating-rate securities have a variable coupon, paying a yield that rises and falls with a benchmark interest rate, such as LIBOR (the London Interbank Offer Rate). Because the coupon “floats” over the prevailing interest rate, the prices of floating-rate bonds are less sensitive to changes in the prevailing interest rate.

With the U.S. Federal Reserve’s (Fed) policy rate at zero – and not expected to rise anytime soon – Treasury yields are near historic lows. Assuming the Fed will remain reluctant to let government bond yields go negative, the price appreciation available from falling Treasury yields is limited. And yet the risk of higher yields remains as prevalent as it has over the last few decades. The economy, and the Fed, ultimately determine the path of interest rates, but in today’s environment the risks look more asymmetric than they have in a long time. An advantage of floating-rate securities is that they offer some neutrality on these risks. For investors concerned about the potential for interest rates to rise, allocating more exposure to floating-rate bonds could be an attractive solution.

Additionally, many bonds that pay a yield over U.S. Treasuries, such as investment-grade corporate bonds, have seen their risk increase as their debt has gotten longer. The average maturity of the Bloomberg Barclays U.S. Corporate Bond Index has been growing steadily, with the current duration (a measure of interestrate sensitivity) now above 8.5 years5, which means that a 1% rise in Treasury rates would result in near an -8.5% loss.

The availability of floating-rate bonds is limited in the U.S. market, and the choices for high-quality (rated A or above) securities is even more limited. Investors seeking floating-rate exposure have traditionally favored the bank loan market and thus had to accept a reduction in credit quality in their portfolios. With CLOs, investors can get floating-rate exposure from AAA assets.

CLOs offer Attractive Yields

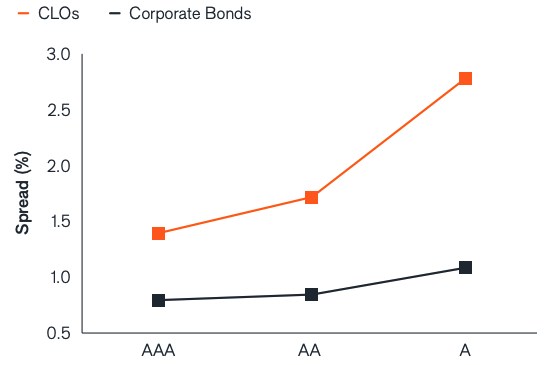

Relative to the investment-grade corporate credit market, CLOs have offered a consistent yield premium across the rating spectrum, in some cases as much as two times the yield offered over U.S. Treasury bonds.

CLO and Corporate Credit Spreads by Rating

Source: Bloomberg Barclays rating-category subindices for corporate bonds, JPMorgan discount margin indices for CLOs. Bloomberg, as of 30 September 2020.

Note: Spread is the additional yield provided over comparable U.S. Treasuries

One common explanation for the higher yields is the relative newness of the market, including many investors’ lack of familiarity with it. But the growth of the CLO market has been accompanied by increased trading volumes and improving liquidity. In March 2020, when bond market volatility was peaking and volumes in many fixed income markets fell precipitously, trading volume in CLOs surged, setting a new monthly record for the asset class.6 Meanwhile, the number of CLO managers has grown steadily, more than tripling over the last decade7, increasing both liquidity in the secondary market and more willingness on the part of broker-dealers to transact and hold the products. Indeed, through the COVID-19 crisis to date, CLO structures generally operated as expected, and in many cases better than the market expected.

It is also possible that CLOs have paid comparatively higher yields precisely because they are floating. As floating-rate securities offer less capital appreciation potential in a falling-rate environment, it would have been rational for investors to favor fixed-rate securities, like U.S. Treasuries and most corporate bonds and securitized products, as interest rates trended lower. However, now that the Fed’s policy rate is zero and Treasuries out to the 10-year note pay less than 1%8, floating-rate exposure may be seen as more of an asset than a liability, and investor demand will drive yields lower.

Nevertheless, a lack of familiarity with CLOs is likely a reason for yields to have been relatively high historically, and a reason they may stay high. Professional management of CLOs does require expertise as the asset class has intricate nuances. Extensive due diligence and strong quantitative analysis is required to properly assess the opportunities. Despite how fast the CLO market is growing, there are a limited number of managers with the experience, resources and technical skills required. The market is still not, in our view, “efficient,” nor is it likely to become so anytime soon. In the meantime, the diversity of loans and CLO managers available provide a wide opportunity set for active, and experienced, investors seeking to build diverse exposure in the CLO market.

Advantages of CLOs’ Unique Structure

Like many securitized products, CLOs can provide investment-grade ratings due to the inherent diversity gained from holding a portfolio of different loans with different characteristics. But CLOs also have additional credit enhancement as a result of their unique structure. The manager of a CLO is required to periodically ensure that there is more than enough collateral in the underlying loans to support the interest and principal for each tranche (or rating tier) of the CLO, starting with the AAA tranche and working down the rating tiers. If, at any point, there is insufficient collateral, the cash flows originally intended for the lower-rated tranches are diverted to the highest-rated tranches. As such, in a time of stress, the AAA tranches could be repaid sooner than expected, as opposed to later or less. Put differently, in times of market stress, the credit-quality of the higher-rated tranches generally improves rather than deteriorates.

CLO Credit Protections have Improved since the GFC

CLOS, as portfolios, are more diverse than a sample of the underlying bank loans. They are also actively managed. As a result, CLOs have had lower default rates than the broader loan market, and this has improved with expanded credit protections added since the GFC. The peak in loan defaults was in 2014, at over 4.5%, and have been in the 1% to 2% range since 2015. CLO defaults, in contrast, peaked in 2002 at near 0.4% and have been either zero or negligible ever since9. According to Moody’s, of the more than 5,000 CLO tranches outstanding in the nearly 20 years surrounding the GFC, only 1.1% were “impaired” in some way. And, no senior tranches – those rated Aa or Aaa – suffered any losses. Simply put, neither the loan default rate nor the loan loss rate – even in the GFC – have come close to the levels required to impair investment-grade CLOs10.

While no security is without some risk of loss, the amount of protection provided to the highest-rated tranches of a typical CLO has increased dramatically since the GFC, and today the protections are as stringent as any part of the securitized market. These additional protections provided to the highest-rated tranches of a typical CLO have been a significant factor in helping the market grow and expand its investor base.

Role of CLOs in a Fixed Income Portfolio

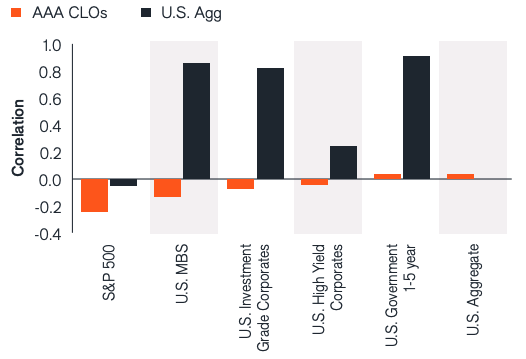

The correlation between the returns of CLOs and the returns of major equity and fixed income asset classes is low to negative, primarily due to the securities’ high credit rating and floating-rate yields. To see how striking these minimal (and sometimes negative) correlations are, consider the correlations of the benchmark Bloomberg Barclays U.S. Aggregate Bond Index, as shown in the chart below. CLOs’ correlations to everything from the S&P 500 to the U.S. Treasury market have been lower across the board.

Correlations of AAA CLOs and the U.S. Aggregate Benchmark

Source: Bloomberg, as of 30 September 2020.

Notes: Correlation of monthly returns March 2012 to September 2020. Indices or securities used to represent asset classes; US High Yield (iBoxx $ Liquid High Yield Index), US Investment Grade (iBoxx $ Investment Grade Corporate Bond Index), US Government 1-5 Year (Bloomberg Barclays US Gov/Credit Float Adjusted 1-5 YR Index), US Aggregate Bond (Bloomberg Barclays US Aggregate Bond Index).

In an environment where interest rates are low, real yields (the yield paid after taking into account expected inflation) are negative, and the risk of higher Treasury yields has risen (while corporate bond durations have risen), we encourage investors to consider their portfolio construction carefully. Allocations to AAA rated CLOs may help investors diversify a traditional fixed income portfolio, offering lower volatility, higher credit-quality and less sensitivity to any rise in interest rates.

But sector selection is only part of the process. Ultimately, we believe the value in active bond asset management comes from security selection within sectors like CLOs that are identified as offering attractive risk/reward across a variety of asset allocation strategies. Characteristics of individual securities and CLO managers can vary widely, and it is the role of the manager – ideally armed with decades of experience – to pick securities that offer better risk/reward and combine them into a portfolio with the yield and risk targets that investors seek.

John Kerschner, CFA

Head of U.S. Securitized Products

John Kerschner is Head of U.S. Securitized Products at Janus Henderson Investors and a Portfolio Manager of the Multi-Sector Credit strategy and Mortgage-Backed Securities ETF. He also has co-managed the fixed income portion of the Perkins Value Plus Income strategy since 2018. In his role as Head of U.S. Securitized Products, Mr. Kerschner primarily focuses on mortgagebacked securities and other structured products. Prior to joining Janus in 2010, Mr. Kerschner was director of portfolio management at BBW Capital Advisors. Before that, he worked for Woodbourne Investment Management, where he was global head of credit investing. Mr. Kerschner began his career at Smith Breeden Associates as an assistant portfolio manager and was promoted several times over 12 years, becoming a principal, senior portfolio manager and director of the ABS-CDO group.

Mr. Kerschner received his bachelor of arts degree in biology from Yale University, graduating cum laude. He earned his MBA from Duke University, Fuqua School of Business, where he was designated a Fuqua Scholar. Mr. Kerschner holds the Chartered Financial Analyst designation and has 30 years of financial industry experience.

Nick Childs, CFA

Portfolio Manager

Nick Childs is a Portfolio Manager at Janus Henderson Investors, a position he has held since 2018. He is responsible for managing the Mortgage-Backed Securities ETF, with a primary focus on valuing opportunities and managing exposure of mortgage-backed securities (MBS). Additionally, he is a Securitized Products Analyst. Prior to joining Janus in 2017 as a securitized products analyst, he was a portfolio manager from 2012 to 2016 at Proprietary Capital, LLC, where he managed alternative fixed income strategies specializing in MBS, absolute return investing. His work with Proprietary Capital included managing all major U.S. interest rate and MBS risks, modeling borrower behavior and MBS deal structure, and advancing market-neutral hedging strategies. Before that, he was vice president at Barclays Capital in their capital markets division, where he focused on securitized products from 2007 until 2012. Prior to joining Barclays, he was vice president at Lehman Brothers. He began his career at State Street Global Advisors in 2003.

Mr. Childs received his bachelor of science degree in finance with a minor in economics from the University of Denver. He holds the Chartered Financial Analyst designation and has 17 years of financial industry experience.

Jessica Shill

Assistant Portfolio Manager

Jessica Shill is a Securitized Products Analyst and Assistant Portfolio Manager at Janus Henderson Investors. Ms. Shill became assistant portfolio manager in 2020 and has held the analyst position since joining the firm in 2019. Prior to this, she was an intern and an analyst for the Wells Fargo Investment Portfolio.

Ms. Shill received her bachelor of arts degree in economics from Bryn Mawr College, where she graduated cum laude. She has 3 years of financial industry experience.