Investors frequently ask us for opinions on specific countries within emerging markets. Depending on what’s in the headlines, the country might be China, India, Thailand or Mexico. Conversations that start top-down and focus on country allocation include many natural questions for those considering emerging markets. However, country should not be the first question, in our view. We believe companies should come first in the security selection process.

For the Matthews Emerging Markets Equity Fund, security selection is guided by three basic questions:

1. Do we want to own this business

2. Is management working for us as shareholders, or some other party—themselves, a controlling shareholder, a family, the government—that doesn’t include us?

3. Are we getting something great for the price we’re paying?

Once we’ve answered these questions, we begin to look at country considerations. Understanding how a manager approaches the intersection between country and company, in our view, is a large part of evaluating an Emerging Markets strategy. We believe the best chances of capturing durable growth come from strategies that prioritize company selection over country allocation. A generation ago, beer, banks and cement tended to be produced and consumed locally. Today, even these highly localized businesses have elements of global competition. Global trends and local tastes are perhaps balanced in something like cosmetics whereas in semiconductors it’s really one global market.

South Korea is an interesting example of the “continuum of competition” within emerging markets. Encompassing the full spectrum, South Korea is home to companies whose competition is primarily local, as well as those whose competition is primarily global. There’s also a large category of businesses that are in-between, where competition may be a blend of local and global. Consider a local coffee shop. The coziness, banter of the barista, corner location and Wi-Fi are local elements of completion. But sourcing beans, online payment and brand recognition is often global.

South Korea’s Cultural Resonance and Global Links

South Korea is enjoying an amazing moment of global cultural resonance, from the Oscar-winning film Parasite to the phenomenon of K-Pop and Korean BBQ. In this K-culture wave, we can spot the elements of local and global competition, too. South Korean band BTS has built a massive global fan base, with songs written, produced and performed mostly in Korean, directly competing with Justin Bieber for Billboard Music Awards.

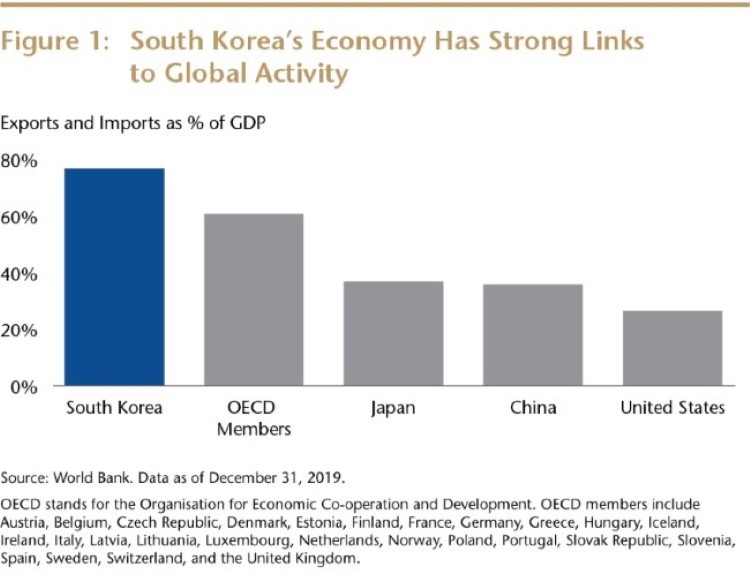

South Korea offers both opportunities and pitfalls for investors. Top down, the Korean economy is highly dependent on global activity. One quantitative measure of this dependence is the ratio of total exports plus imports to GDP. These linkages mean that Korea in aggregate can be more susceptible to global sentiment. This narrative, however, reflects very differently when considering individual company.

Is a Company’s Competition Local or Global?

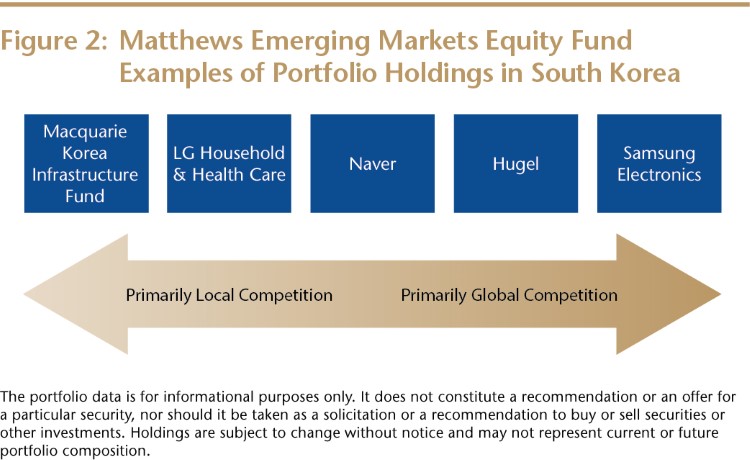

The Matthews Emerging Markets Equity Fund holds five South Korean companies that in our opinion almost perfectly illustrate the “continuum of competition.” Macquarie Korea Infrastructure Fund mainly operates toll roads, and, effectively, cannot do anything outside Korea. 100% of its revenues are generated domestically. Samsung Electronics is a well-known producer of phones and electronics that compete against other global brands, but more than half of its profits in 2019 came from its semiconductor division—a business unit that competes globally and operates according to global sales cycles. About 87% of Samsung’s sales occur outside Korea. (Source: Samsung Electronics.)

Even these rather clear endpoints of one Korean company generating all its revenue inside Korea and the other much more driven by global sales is complicated. For example, South Korea has recently seen an explosion in tourism. According to Bloomberg data, international arrivals were 8 million 10 years ago and 17.5 million in 2019, with much of this growth coming from neighboring countries like China. South Koreans have also caught the travel bug and outbound trips have similarly grown. The current pandemic means fewer tourist arrival and fewer outbound trips. Naturally, this means less traffic on the airport expressway. So, there are “global” influences on domestic revenues. Similarly, Samsung’s assets, governance structure, and R&D are much more locally based in Korea than its revenues are.

Contrasting Macquarie Korea Infrastructure Fund and Samsung Electronics does highlight how company fundamentals can differ substantially within a country. Our remaining holdings in South Korea generate 60-75% of their revenues in Korea. However, their prospects and multiples are much more influenced by what happens elsewhere. Two of them, Hugel and LG Household and Health Care, are in large part driven by what happens in China, while the third, Naver, is unique among Korean companies for its success in Japan. Hugel is a biotechnology company that in 2019 generated 60% of its sales from Korea. (Source: Hugel.) LG Household & Health Care is a consumer company that derived over 70% of its topline sales domestically (Source: LG Household & Health Care). Finally, Naver is the leading search engine in Korea where it has the dominant share over global competitors. Around two-thirds of Naver’s revenues are generated domestically. We’ll explore how the “continuum of competition” applies to Hugel, LG Household & Health Care and Naver and explain why their futures are really more driven by factors exogenous to country of domicile.

Hugel’s main product competes with Allergan’s Botox. Botox, a high spec botulism toxin that applied in specific doses and specific ways causes skin to firm up reducing the appearance of wrinkles, is a huge brand name and a lucrative business for Allergan. Hugel produces a similar product used primarily for cosmetic purposes. The product is currently approved in many markets including domestically in Korea and internationally in places like Taiwan. The big non-linear catalyst for the company is pending approval by China’s Food and Drug Administration for use in one of the world’s largest beauty markets. The company is also seeking regulatory approval in other markets, including the United States. Therefore, we believe Hugel’s prospects are far more international than its trailing sales would indicate at the moment, should Hugel continue to sell the same thing, but more broadly.

LG Household & Health Care is similarly heavily influenced by China. While 70% of its topline sales are from Korea, the narrative is more complicated both in terms of revenues and profitability. LG Household & Health Care has different segments. Its most profitable segment, cosmetics, drove 76% of profitability in 2019, despite making up 62% of its sales that year. The company’s cosmetics, particularly its luxury Whoo brand, are very popular with Chinese consumers. A meaningful portion of cosmetic sales are to Chinese consumers buying in Korea. These sales are both to Chinese nationals visiting Korea and daigou sales. Daigou sales are essentially bulk buying in Korea for cross-border export unofficially to China. As a company like LG Household & Health Care builds out its distribution in China, it’s quite likely that some of these cross-border sales will decline and be replaced by sales recorded as international. The end user hasn’t changed, but the sales breakdown may migrate.

Naver is a company that has re-invented itself several times and is perhaps best known as a local champion that, via better results, came to dominate internet search in the Korean language. Over the years it has succeeded in developing several IT platform services beyond search like cloud computing and payments, and Naver also owns content assets including a large anime platform, music conduit, and live streaming platform. One thing that makes the company unique is its success in Japan. Naver owns the majority of a company that is a dominant chat platform in Japan and Taiwan. Part of the value creation narrative for Naver is clarity around its assets and position in Japan.

All five of the South Korean holdings in the Matthews Emerging Markets Equity Fund are different in terms of who they compete against. One is entirely domestic and one is mostly global. The other three have pieces of their narrative that are both local and global. Biotech requires local approvals, but the science, safety and efficacy are pretty much global. Cosmetics is about brands. Chinese consumers can pick freely between domestic, Korean, French, American or Japanese tubes of lipstick. Search engines require adapting globally competitive technology to the needs of its domestic audiences. When we think about South Korea, we think about what drives our companies and then we think about the country. Certain companies are heavily influenced by the demographics, politics or macro trade winds of their country of domicile. Others are more subject to global trends in taste or technology. It’s not uncommon that the prospects of a company end up being more about somewhere other than where the company started out. We hope our dissection of our five South Korean holdings illustrates this to our investors and those who are considering the Matthews Emerging Markets Equity Fund as part of their portfolio.

John Paul Lech Portfolio Manager Matthews Asia

Investments involve risk. Past performance is no guarantee of future results. Investments in emerging and frontier securities may involve risks such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Additionally, investing in emerging and frontier markets countries are substantially smaller, less liquid and more volatile than securities markets in more developed markets

Important Information

Portfolio holdings for the Fund may vary from time to time from what is shown. The information is presented to solely illustrate Matthews Asia’s investment process. It should not be considered a recommendation of the securities discussed, nor are presentation as to whether the securities are currently held by the Fund. The results of any possible investment in the securities are not representative of the results of other investments by the Fund. Performance of the Fund and a list of current holdings are available at matthewsasia.com.

You should carefully consider the investment objectives, risks, charges and expenses of the Matthews Asia Funds before making an investment decision. A prospectus or summary prospectus with this and other information about the Funds may be obtained by visiting matthewsasia.com. Please read the prospectus carefully before investing as it explains the risks associated with investing in international and emerging markets.

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Investing in small- and mid-size companies is more risky and volatile than investing in large companies as they may be more volatile and less liquid than larger companies. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.