SUMMARY

Editor’s Note: This week, we look back on broad themes that took shape during an unpredictable and unforgettable year.

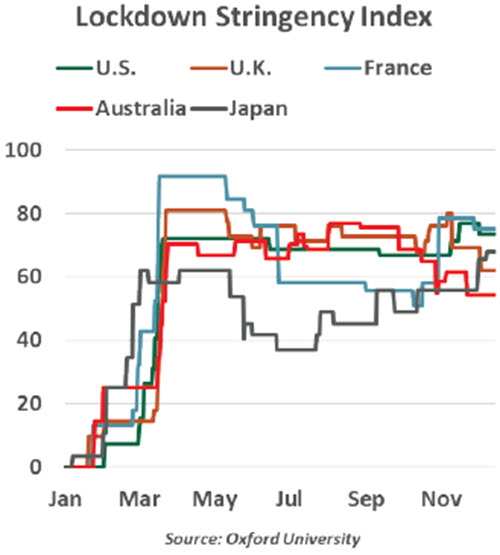

The Limits of Lockdowns

In the early days of COVID-19, only a few facts were known about the virus: It is potentially lethal, often asymptomatic, and spreads through airborne transmission. Absent a medical remedy, policymakers looked for solutions to keep people separated. Thus, lockdowns were born.

The effectiveness of lockdown policies will be a point of debate for a long time to come. On the one hand, they did help to reduce the spread of COVID-19: Countries and regions with strict lockdown policies during the spring all saw lower numbers of cases in the summer. But lockdowns were no cure. Most regions that tamed COVID-19 initially have entered a renewed wave. The lockdowns bought some time and preserved health care capacity, but they were not a durable solution.

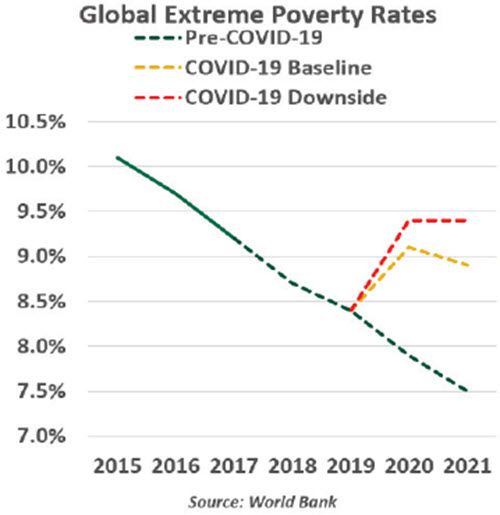

Lockdowns carry substantial economic costs. The World Bank estimates an overall loss of 5.2% of worldwide gross domestic product in 2020, triple the severity of the global financial crisis in 2009. While 2021 is shaping up to be a year of recovery, total global output will remain below 2019 levels. An assessment of the full cost of COVID-19 requires valuing intangibles like physical and mental health; we will consider it sufficient to say that everyone has felt some cost of the pandemic.

We cope by seeking normalcy, and some populations bristled at the restrictions placed on their lives. Indeed, as the initial round of lockdowns met its goal, many people concluded that the crisis had passed: as cases fell, people felt more confident leaving the home, and were not always careful in doing so. This return to activity drove record-setting economic growth in the third quarter but also fed the renewed wave of COVID-19 cases.

Protests against pandemic-related restrictions have grown worldwide. Some business owners and their customers have openly defied local shutdown ordinances. Educators are working hard to open schools as broadly and safely as possible, for the benefit of students and parents alike. The challenge is to balance the need to limit transmission and safeguard hospital capacity with the desire to limit economic and social damage.

Just this week, London and Germany started fresh cycles of stay-at-home orders; these won’t be the last. Avoiding contact is still an effective remedy, but it is bitter medicine we will be eager to stop taking in the year ahead.

Ks Everywhere

Since the onset of the pandemic, economists and observers have searched for an alphabetic shape to describe the potential courses of economic recovery: V, U, Z, W, and L have all been used. While the poor generally suffer more than the wealthy during crises, few analysts had foreseen the extreme K-shape of the current recovery, in which some do well, and others do not. This disparity has taken many forms.

In a sector sense, the upper arm of the letter ‘K’ symbolizes industries that have benefited from the pandemic: technology, online entertainment, pharmaceuticals and online retailers. The lower arm includes restaurants, bars, hotels, airlines and in-person retail, which witnessed a significant and sustained drop in demand.

“To this point, the global recovery has been very uneven.”

Large corporations have managed to sail through this crisis with modest damage or even growth, but thousands of small businesses around the world have incurred heavy losses or had to close.

Highly skilled workers are generally doing better than low-skilled and younger workers. The lowest-paying industries (like leisure and hospitality) have seen the biggest job cuts during the pandemic. Demands on families grew as schools switched to remote learning in spring and have not universally reopened. Women have borne a greater burden of job losses.

In higher income countries like the U.S., equity markets scaled new highs, a boon to shareholders; by contrast, lengthy lines at food banks have become a common sight. Over 20 million Americans are receiving jobless benefits, and 14 million of these are at risk of losing those benefits after Christmas. More than 50 million are at risk of experiencing food insecurity.

The pandemic has widened the inequality between richer nations and poorer ones. Many emerging markets simply lack the capacity to offer much support.

Income inequality has been a defining narrative of the 21st century, one driver of a global shift towards populism. COVID-19 is only going to widen the chasm. If populations were unhappy about the uneven recovery in the aftermath of the 2008 financial crisis, they are certainly not going to like this one either.

Government: Acting, Fast and Slow

Daniel Kahneman’s Thinking, Fast and Slow describes two modes of thought: Survival-oriented “System 1” is fast and instinctive, while “System 2” is slower and contemplative. Depending on the challenge at hand, each system serves a vital purpose. These two approaches to thinking were also apparent in legislative responses to COVID-19.

Policy actions at the outset of the pandemic were fast, effective and innovative. The U.S. Congress overcame acute partisan divisions to pass three bills in the month of March alone, culminating in the massive CARES Act. CARES was comprehensive, offering support for laid-off workers, consumer loan borrowers, small businesses, large industries and local governments. Fast action was not solely an American phenomenon, as legislatures around the world stepped up to support their economies and institutions. A crisis was upon us, and the fight-or-flight approach in System 1 thinking spurred our leaders to rapid action.

“Legislative responses to COVID were first purposeful, then political.”

But stimulus measures of this first vintage all shared a flaw: expiration dates. Early pandemic episodes, like those in China and Italy, suggested the virus would follow a severe but brief trajectory. Legislation assumed a temporary economic disruption, then a return to normalcy. The risks of lingering shocks and renewed outbreaks were left for another day.

Subsequent stimulus efforts have stumbled. As key provisions of the CARES Act expired over the summer, Congress could not agree to extend them; the impasse has continued through this week. Negotiations over job support in the U.K. were prolonged. Meanwhile, member states of the European Union needed months to agree on a joint €750 billion response, which has yet to take effect. The ability to ponder, deliberate and refine complex decisions with System 2 is part of humans’ evolutionary advantage – but the deliberations in this matter have gone on too long.

Behavioral researchers like Kahneman often point out how our thought processes can lead to irrational or sub-optimal decisions. Swift actions taken in the face of COVID-19 should be celebrated; the recent stasis should not.

Owe No? Owe Yes!

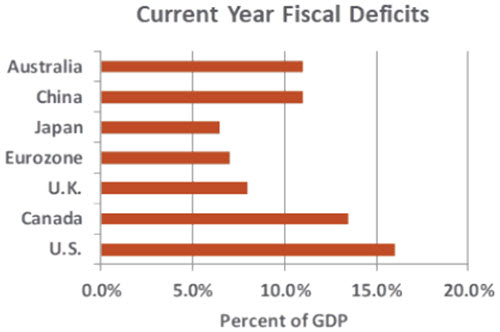

Hands were wringing at the start of 2020 over the enormity of debt around the world. The 2008 financial crisis had illustrated the risk of over-leveraging, and had produced a painful reckoning for consumers, firms and financial institutions. Governments took on additional borrowing to facilitate recovery, but were encouraged to embrace austerity as the expansion proceeded so that debt could be brought back under control. Academics were doing serious work on whether the level of global debt was sustainable, and warned of a potential future reckoning.

With the year drawing to a close, however, debt around the world has skyrocketed—and few seem overly concerned. Immense amounts of leverage have been taken on to deal with the economic consequences of COVID-19. Governments are the primary borrowers, but corporations also issued a record volume of bonds in 2020 (see chart). Investors have eagerly absorbed the new supply; central banks have added to the demand, expanding their purchases of both sovereign and corporate debt.

A strong, sustained national fiscal response was essential to offsetting the economic damage done by public health restrictions. Aid to those displaced from work, small businesses, and critical industries provided a bridge of support between the old normal and the new normal in many countries. Failing to provide would have been disastrous, and would have left countries with far worse budget challenges than they face today.

Firms were applauded for raising cash through bond issuances to shore up their balance sheets and prepare them for the challenges presented by the pandemic. The recent rally in both equity and corporate bond prices certainly suggests that investors are sanguine about default risk.

“Is the world getting too comfortable with debt?”

But will portfolio managers and the public continue to absorb additional borrowing without objection? Will they continue to accept low, or even negative, interest rates for doing so? Will central banks one day decide that their work is done, and begin reducing their balance sheets? Those questions may not become pressing next year, but they could one day. And that will be a difficult day for the bond markets.

Chain Reaction

International exchanges of goods and services account for about 60% of the world’s gross domestic product (GDP). Global companies have invested many years and considerable resources in optimizing their operations and finding the ideal places to source materials and conduct production. Once output is complete, intricate distribution networks whisk products away to their intended destinations quickly and efficiently.

These systems run on tight, just-in-time tolerances. Contingency plans exist, but are not designed to sustain processes in the event of widespread interruptions. The pandemic illustrated just how fragile global supply chains can become once links start breaking.

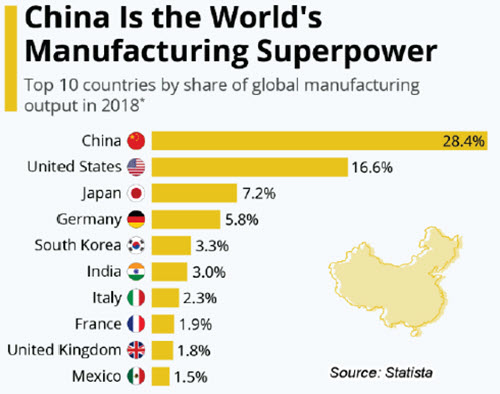

From a production perspective, the pandemic could not have started in a worse spot. China generally, and Wuhan specifically, play a central role in worldwide manufacturing. Even though shutdowns in China were brief relative to those that unfolded in other countries, the interruption triggered a chain of problems upstream and downstream. Raw materials and parts had trouble getting in; work in process and finished goods had trouble getting out. That impaired China’s vendors and its clients, and the bottlenecks radiated out from there.

And as we discussed last week, sophisticated logistics networks were disrupted by a scarcity of containers, constrictive public health measures taken at ports, the idling of commercial aircraft, and attrition among the ranks of truck drivers. It may be well into next year before everything is running smoothly again.

There are some who would prefer not to go back to the old system. The pandemic illustrated that there is too much reliance on individual companies and countries for certain products; personal protective equipment is a case in point. Some diversification could enhance resilience and reduce bilateral trade frictions. (The U.S. and China are the main event, but there are many others on the undercard.)

But reorienting global supply chains would be costly and time consuming, and the new networks would still be vulnerable to shocks. There will certainly be a lot of talk about changing chains, but making change is another thing entirely.

WHO Rose to the Occasion?

While COVID-19 has been a significant test of public health and public finances within countries, it has also put multilateral institutions like the World Bank, the International Monetary Fund (IMF) and the World Health Organization (WHO) under increased scrutiny. These global associations have endured contempt from some corners, but they remain central to recovering from the pandemic.

The WHO, which faced criticism initially for its slow response to the pandemic, has continued to play a vital role. The body has assisted over 120 nations, particularly those with poor health and disease control infrastructure, by providing timely information about the virus, building COVID response teams and equipping hospitals with supplies.

“A crisis without borders warrants a response without boundaries.”

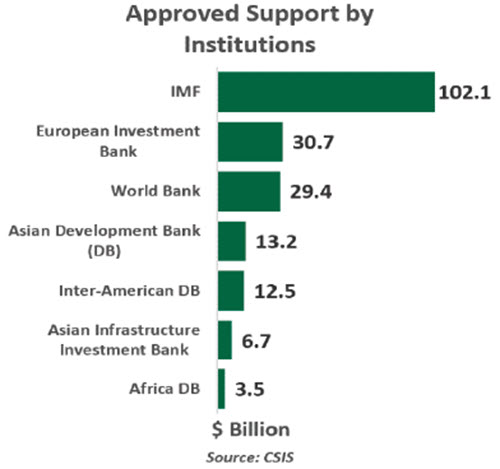

Other multinational institutions have also risen to the occasion. Between January and September 2020, international financial institutions and consortia approved over $180 billion in financial support to developing countries.

The World Bank has mobilized billions in financing tailored to the health, economic and social needs of nations dealing with the crisis. The IMF responded with unprecedented swiftness and scale, offering financial aid to more than 100 countries. The Fund temporary doubled access to its emergency facilities like the Rapid Credit Facility and Rapid Financing Instrument, extended debt service relief and established short-term liquidity lines.

While many are pinning their hopes on a vaccine, the virus will likely live on until vaccines are made available and affordable to every corner of the world. Emerging markets may be the last in line, and may therefore be most vulnerable to long-term damage. Global cooperation to ensure adequate health supplies and to avoid further ruptures in the global trading system will help to limit that damage.

John F. Kennedy once said, "when written in Chinese, the word crisis is composed of two characters. One represents danger, and the other represents opportunity." We hope politicians see support for multilateral institutions as an opportunity to strengthen global cooperation and collaboration.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2020 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit our terms and conditions page.

© Northern Trust

Read more commentaries by Northern Trust