In this Issue:

- Senate Outcomes and the Economic Agenda

- The Case for Additional Stimulus

- Brexit Is Done, but Not Dusted

This week’s scene in the U.S. Capitol is one none of us will soon forget. Divisions within the U.S. populace run deep. We hold out hope they can be bridged through more productive means than Wednesday’s revolt. The incoming Senate has an opportunity to take the lead in restoring a shared national purpose…and in reinforcing the U.S. economy.

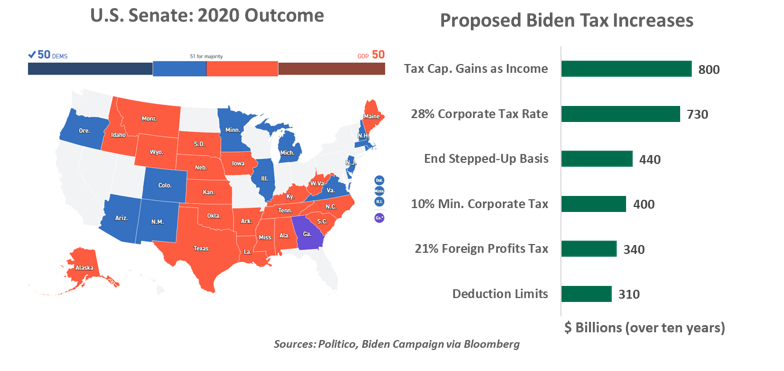

Prior to this week’s run-off elections, our legislative outlook called for continued gridlock. But Georgia voters sent two more Democrats to the Senate, meaning the chamber will have 50 representatives from each party. Any tie votes will be broken by the Democratic vice president-elect, opening the way to a more active legislative agenda. Yet while the scope for new actions has widened, it is not unlimited.

In the near term, the prospects for further COVID-related fiscal support have improved. The latter half of 2020 revealed a bipartisan willingness to pass some form of stimulus, but compromise was persistently out of reach among the House, Senate, and White House. With those components now aligned (albeit narrowly) under one party, progress should become easier to achieve.

As discussed in the following article, the package ratified at the end of the year kept its cost in check with smaller payments and shorter timespans for support. It will prove insufficient to tide the economy over to the first half of 2021. The new Congress will likely make supplemental economic impact payments ($1,400 per person has been proposed) an early order of business. Other relief is likely to accompany this measure.

Tax increases, which had appeared to be off the table, may be employed to help pay for the budget expansion. Though fiscally defensible, this would be difficult to prioritize. Tax hikes are unpopular under any conditions, and increasing the tax burden at the outset of a growth cycle would be especially poor timing. Tax code changes, if any, are likely to be marginal, such as small increases to income tax rates for the highest earners or a repeal of the step-up in basis for inherited capital gains.

It is important to note that while some fiscal measures can be passed with a simple majority, others require a larger plurality. The budget reconciliation process allows entitlement spending and revenue provisions to be passed with 51 votes. Beyond that exception, bills must be approved by 60 senators to end a filibuster, allowing a minority of senators to stop legislation.

Confirmation of cabinet and judicial appointees require the approval of a simple majority of the Senate, a bar that is now easier for the incoming administration to clear. President-elect Biden’s nominations have generally been pragmatic ones, but the possibility of additional industry regulation has increased. The U.S. Department of Justice is expected to take a more aggressive tack with technology companies.

Health care was a high priority for candidate Biden, who hopes to build upon the Affordable Care Act with a public insurance option. The structure of the U.S. healthcare system is

|

Democrats’ legislative prospects improved, but this was not a blue wave.

|

costly and inefficient, and proposals for reform are plentiful. But tackling the problem proved to be a tremendous use of political capital for Barack Obama, and the party may deem other initiatives to be more urgent and less fractious. The U.S. courts may also present a roadblock to progress.

Infrastructure has long appeared to be a topic of bipartisan support, but concrete bills have been elusive. Democrats may seek to steer infrastructure investments to support their ambitious green agenda, but some in Congress will be wary of the resulting impact on heavy industries.

Biden may also emphasize investment in education, which can take many forms. After Biden’s election, early speculation surrounded student loan debt forgiveness, a policy that can lift up burdened consumers but will be difficult to structure fairly. Many Democratic primary candidates supported some variant of free college, which may take the shape of free community college courses or subsidies for retraining.

In all matters, the delicate balance of power will restrain the most ambitious proposals that Democrats floated in their 2020 campaigns. Opinions vary within the Democratic party, and Biden is a centrist who holds out hope for bipartisanship. Rubber-stamp support for all proposals from all 50 senators is unlikely, and Democrats’ margin in the House is narrowed. Because leadership cannot afford to lose votes, each member will have some capacity to steer the agenda.

The even split in the Senate was unexpected, but it may not be unwelcome. The 50-50 outcome should not only pave the way for policies that support sustainable growth, but might jump-start a new cycle of cooperation that would prove a potent antidote to this week’s chaos.

When Too Much Is Not Enough

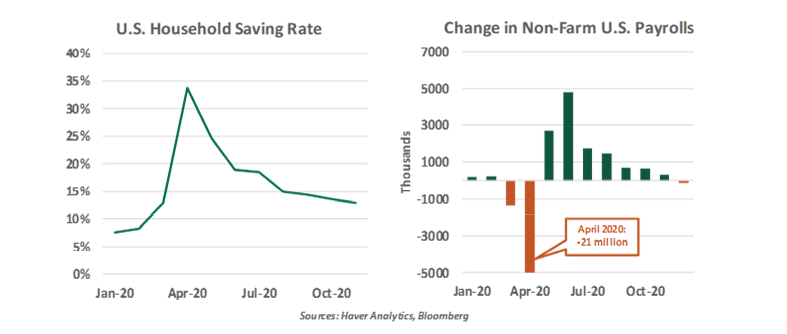

The pandemic forced many families to downsize gatherings during the recently concluded holidays. Many seasonal bakers, however, didn’t get the memo. Production of cookies and other sweet treats seemed to be undiminished, requiring household members to boost their consumption. The resulting sugar rush is unlikely to be sustained long into the new year.

Members of the U.S. Congress delivered an energy boost to the American economy just prior to the holiday recess. The package of unemployment benefits, aid to small businesses, and direct payments to households will boost consumption. But the resulting economic rush may not last long enough into the new year.

The initial rounds of pandemic stimulus, passed last spring, were unprecedented in their size and scale. But they were constructed under the assumption that the challenge presented by COVID-19 would pass by summer’s end. As support programs for the unemployed and small businesses expired, the stress placed on individuals and the economy as a whole increased. This reduced economic momentum in the final months of 2020.

Congress began consideration of an extension to various support programs last August, but there was considerable resistance. Some worried that workers were declining opportunities to return to their posts because their benefit payments exceeded their salaries. Others were hesitant to provide salvation to firms and governments that had not managed well. As vaccines were approved for use, promising an end point for the pandemic, hope arose that households and enterprises could soon fend for themselves. These factors prolonged negotiations and made it difficult to reach consensus.

|

The December stimulus bill is better than nothing, but it’s not enough.

|

The latest wave of COVID-19 infections, which has reached a dangerous new peak, began to break down objections. In early December, a bipartisan group of lawmakers worked to craft the $900 billion package that was ratified just before year end. It is better than nothing, but probably not enough. Some key features:

- Another round of direct payments to households is on its way: $600 for individuals ($1200 for married couples) and another $600 for children (up to two), phased out above certain income levels. Consumers will spend a good bit of this money, but using last spring’s payments as a guide, a lot of it will be saved. This could mute the beneficial impact on consumption.

- Unemployment benefits were extended, but at reduced levels and for a short period of time. Federal supplements to beneficiaries will continue at $300, half the former rate. Recipients of special Pandemic Unemployment Assistance (primarily for the self-employed) will see their support sustained. Both of these facilities are set to expire in mid-March. The U.S. job market went back into contraction in December, and may struggle to generate new positions with COVID-19 caseloads at such high levels.

- Another $285 billion will be allocated to the Paycheck Protection Program (PPP), under which small businesses can take out forgivable loans if they maintain their payrolls. The latest round will be focused on small, private firms with fewer than 300 employees whose revenue has dropped by 25% or more.

The additional measures will help, but much more will be needed. COVID-19 contagion is proceeding rapidly and vaccination is proceeding slowly. It seems highly unlikely that the U.S. economy will be fully and durably reopened by the beginning of spring, when features of the act are due to expire. The bill gives rental tenants only a one month reprieve from evictions, leaving millions at risk. The December measure also did not include additional aid to state and local governments, whose budget challenges are causing contractions in payrolls and public services.

As discussed earlier, the outcome of the Georgia runoff elections has certainly changed the political calculus surrounding economic stimulus. While securing passage of any legislation will be challenging given the divisions between and within parties, the probability of another economic support effort from Congress has certainly risen in the past few days. It’s a bit early to speculate over the size and composition of a package, but it’s likely we’ll have cause to upgrade our forecasts for growth in the coming weeks.

There are certainly good questions about whether we can afford all of this. The fiscal diet that might one day be needed to regain financial fitness could be a strict one. But sweetening the outlook at this point is important if we hope to head off a bitter future.

New Year’s Resolution

The year 2020 was full of major, world-shifting events. Along with the pandemic and the drama surrounding the U.S. presidential election, the resolution of Brexit was also historic. After more than four decades of membership in the European Union (EU), four years of negotiations, two general elections and three prime ministers, the U.K. finally completed its divorce from the EU days before the December 31 deadline.

Both sides, particularly the U.K., made concessions during the course of final negotiations. Issues surrounding the Irish border, fishing, the level playing field of trade and the divorce bill all proved difficult to resolve. As part of the agreement, labeled as “Canada plus plus” by British Prime Minister Boris Johnson, the U.K. has attained tariff- and quota-free goods trade with the EU and ended the role of the European Court of Justice in settling trade disputes.

The EU has avoided a hard border on the island of Ireland and preserved the “four freedoms” of its single market (free movement of goods, services, people and capital). The 1,200-page accord covers a broad range of other areas including investment, competition, state aid, tax transparency, air and road transport, energy and sustainability, fisheries, data protection, and security coordination. The deal curtails the free movement of people between the U.K. and the EU, and reintroduces temporary visas for vocational purposes.

The thorniest issue of the “level playing field” was resolved by the principle of “managed divergence,” with both sides reserving the right to retaliate to ensure one side doesn’t gain an unfair competitive advantage. On fisheries, the EU agreed to give up 25% of its existing quotas in British waters over a transition period of five-and-a-half years, followed by annual negotiations.

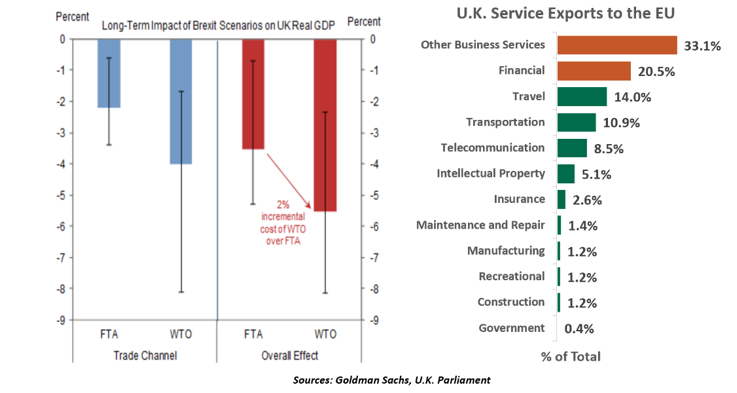

The deal has spared the U.K. economy some of the most dire costs from a cliff-edge Brexit, but will still cause a sizeable loss of output in the long run compared to remaining in the bloc. Moreover, the new arrangement is creating non-tariff barriers to trade and cross-border mobility, which didn’t exist until last year, for both sides. Goods will now be subject to new customs, paperwork and regulatory checks, including rules of origin and stringent local content requirements. These new rules are resulting in delays at the border and disturbed supply chains.

The disruption is already visible as some European online retailers are no longer delivering goods to the U.K., citing tax changes, bureaucracy and cost concerns. International shipping firms have

|

The Brexit agreement is done, but the door to potential future strains is still open.

|

started levying additional charges on cross-border shipments. According to Britain’s revenue authority, new import and export declarations alone will cost U.K. companies £7.5 billion ($10.3 billion) yearly.

The accord respects the major red lines of both parties but has left the door open to future flashpoints. Services, which account for 80% of the U.K. economy and are notably reliant on exports to the EU, were largely left out of the deal, with no mutual automatic recognition of professional qualifications and licenses. U.K. financial firms have lost blanket access to the bloc and have only been granted temporary regulatory equivalence for derivatives clearing and settling Irish securities. Hoping to maintain London as a global financial hub, the British government has allowed EU firms to stay for up to three years, in the hope they will apply for permanent authorization.

The U.K. now enjoys the ability to strike new trade deals and diverge from European regulatory standards, but in doing so the nation could face tariffs on exports into its biggest market. The U.K. will have to tread carefully while charting its new journey. This year, all eyes will be on whether the remaining issues can be ironed out and what risks and unintended consequences may arise. This is not the end of a story for the U.K.; it is the beginning of a new chapter.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

More Innovative ETFs Topics >