In this Issue:

- Student Debt: From Forbearance to Forgiveness

- Is The Biden Stimulus Plan Too Big?

- Australia-China Trade Tensions

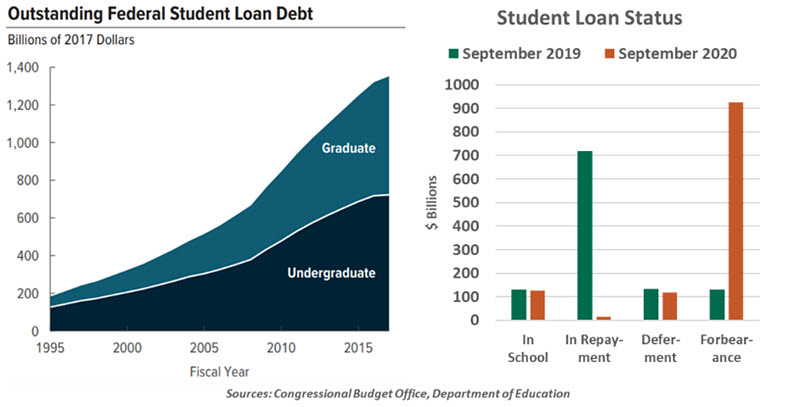

“When you find yourself in a hole, stop digging.” This time-tested maxim can work well for finding a path out of personal debt. Small behavioral changes can allow people to stop running up credit accounts and start paying them down. But when the “hole” represents $1.7 trillion in liabilities held by nearly 48 million people in the U.S., simple frugality will not be sufficient. Greater interventions may be needed.

Momentum is gathering around a debt forgiveness program for student loans. We agree the problem calls for policy responses, but we do not believe cancelling loans is the correct course. It is neither efficient nor equitable, and leaves root causes of the problem unaddressed.

The conditions we outlined in our last discussion of student debt have not changed; only the amounts of money and borrowers have continued to grow. The cost of college tuition has consistently outpaced broader measures of inflation, but the value of a degree remains high. College-educated workers earn higher wages and experience lower unemployment, so students continue to put themselves into debt to better their long-term fortunes. Some succeed, while others do not.

These conditions have led to a generation-defining burden of student debt, which carries costs beyond just financial obligations. Fiscally responsible young adults will focus their budgets on their student loans, but that can crowd out other important investments like retirement savings and homeownership. Couples may defer marriage and family formation until their finances are under control, weighing on the country’s already-slow birth rate. Meanwhile, those with the fortune of family support allowing a debt-free graduation will start their adult lives without the same financial burden, raising inequality.

Mild remedies are already available. Forbearance on federal student loans has always been an option during hardships like job loss. The CARES Act granted all federal borrowers a temporary forbearance, now extended through September 2021. Income-based repayment (IBR) plans for federal loans are available, which allow borrowers with low or moderate incomes to cap their student loan payments at 10% of their disposable income; any unpaid balance is forgiven typically after 20 years. While these programs can help to balance household budgets for a time, the loans remain prominent in borrowers’ lives.

“Student debt forgiveness is not a progressive policy”

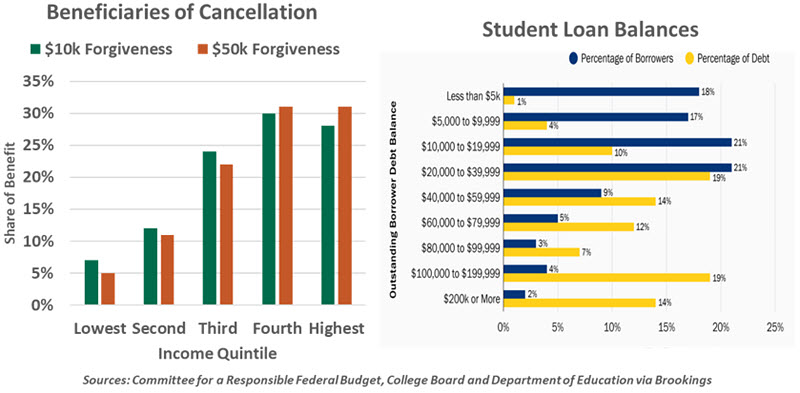

A challenge facing 48 million voters is not one that politicians can ignore for long. In the 2020 party primary, Democratic presidential contenders floated various reform ideas. At present, there are dueling proposals to write off $10,000 or $50,000 of all borrowers’ balances, which could be the subject of an executive order from the president. Even the smaller proposal would be a boon, with 38% of borrowers seeing their balance go to zero.

As the Biden administration moves on from the acute demands of COVID-19 relief, action on student loans will be a gauge of how progressive his priorities are. But from an economic standpoint, writing off student debt is not progressive at all. The data show the benefits would accrue largely to high earners.

To start with, about a third of Americans do not attend college (and consequently have lower earnings), and would not benefit at all from relief. From there, higher student loan balances are typically a sign of more education and are often held by workers with advanced degrees; almost half of student debt outstanding was taken on for graduate education. These are the borrowers most likely to be able to repay their loans without any need for social support.

Student loan forgiveness would come at a substantial cost. Since the government holds most student debt, the cost would be added to the annual deficit. A $10,000 write-off for borrowers would weigh in at $377 billion, and increasing it to $50,000 would raise the price tag to about $650 billion. By contrast, the CARES Act’s unemployment supports cost about $442 billion, which provided well-targeted aid to a subset of the population that most needed it.

There are other objections. Debt forgiveness can be viewed as rewarding reckless credit decisions; borrowers who made sacrifices to avoid indebtedness or studiously pay down their loans may feel foolish for their responsible choices. Under current law, the write-down would be treated as taxable income, creating an immediate liability for borrowers. And forgiveness by executive order could face legal challenges as an overreach of presidential authority.

There are better ways to tackle the problem. Rather than a one-time cancellation of principal, Congress could build upon the existing IBR structure. Enrollment in IBR could be automated and simplified. IBR can be improved for borrowers by requiring a lower share of income to be directed to payments or by phasing out balances after a shorter interval of repayment. These changes could not, however, be made through an executive order from the president; Congress would need to pass legislation to change this program.

“Writing off debt without reforming the system risks a recurrence.”

Conventional consumer credit underwriting does not apply to student loans: funds are available to make education possible for all students. That bridge to upward mobility should be preserved. However, the government should apply more stringency to educational institutions. Colleges or degree programs with high drop-out rates and whose graduates show no income gains should face scrutiny and potentially lose their access to federal loan programs.

2005 legislation made it effectively impossible to discharge student debt in bankruptcy. Congress may change that law at its discretion. While bankruptcy should always be a tool of last resort, it should also be a viable way to climb out of debt.

The hole created by student debt is too large to ignore, but simply filling it in would be too narrow of a treatment. Real reform of the program and the educational system it supports will be needed to prevent students from digging themselves, and the nation, deeper into debt.

Fuzzy Math

Debate over the American Rescue Plan (ARP), the Biden administration’s $1.9 trillion fiscal stimulus proposal, reached a crescendo this week. Supporters of the ARP defend its size by noting that doing something too small will leave the American economy vulnerable to a slow recovery and lasting damage. Detractors counter by saying that something more modest will be plenty, and doing too much risks overheating the expansion.

Economic models are used to determine which group is correct. The calculations involved are complex, and a number of tenuous assumptions are required to complete them. The field excites only the most hard-core of policy analysts, but the numbers that emerge affect us all.

The cost of the proposed legislation is clear. What is not clear is how much economic activity each component will generate. For example, direct payments to households will prompt increases in spending; this, in turn, will generate revenue and profits for businesses, who may need to re-order and hire to keep pace. But exactly how much of these knock-on effects will result from the measure is a difficult question.

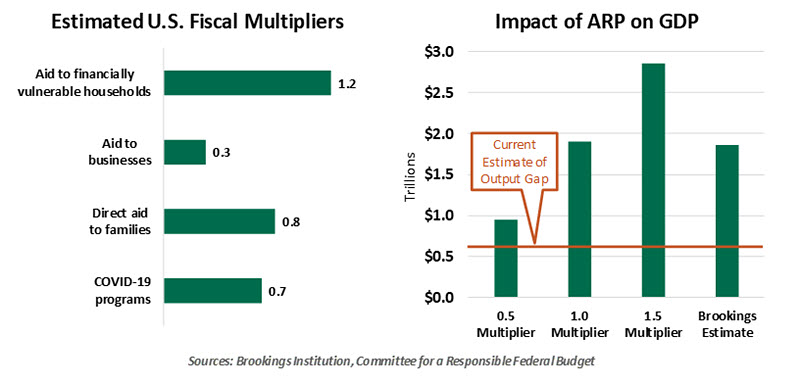

“Fiscal multipliers,” which express the amount of incremental gross domestic product (GDP) produced by a given policy option, attempt to provide answers. From a purely economic perspective, efforts with high multipliers are preferred; they generate more activity, and are therefore more likely to pay for themselves with incremental tax receipts.

Estimating fiscal multipliers is not an easy calculation. Studies are not done in a laboratory setting, where trials can isolate the influences of different agents. For example, if both monetary and fiscal policies are easing, it is difficult to pinpoint the impact of one versus the other. The potency of policy varies over time, and calculations may reflect the leanings of the economist performing them.

With those caveats, the elements of the Biden package have a range of estimated multipliers. As shown in the chart below, aid to financially vulnerable households, which includes supplemental unemployment benefits, has the biggest impact. Direct aid to families, which includes stimulus checks, is somewhat less impactful. For this reason, and reasons of equity, the design of the stimulus check program has come under criticism from both sides of the aisle.

The size of the Biden program has also attracted criticism from a range of observers. With vaccination gaining steam (an effort that will be accelerated by funding from the Biden plan), the promise of a durable reopening at midyear is rising. From there, the economy should recover without as much policy support. To some, including former Treasury Secretary Lawrence Summers, the ARP goes well beyond what is needed, and might risk overheating the economy.

Summers and others base their reasoning on what is called the output gap, which is simply the difference between actual and potential economic growth. During recessions, output gaps grow, and are reflected in idled workers and facilities. Expansions eventually re-employ these resources. If the economy grows faster than its long-run potential for too long, these resources could get strained, creating a context for higher inflation.

Simulations performed by a number of sources suggest the ARP will more than close the current output gap. But the projections are highly imprecise. Models that estimate fiscal multipliers have a large margin of error: the Congressional Budget Office, which does very good work in this area, offers a range of 0.5 to 2.5 for multipliers on federal spending. That is big enough to drive a truck through.

“Estimating the impact of fiscal policy on economic performance is a highly imprecise exercise.”

Estimates of potential growth, which determine the size of the output gap, rely on long-term projections of productivity growth, which many think are understated. Even a modest upward revision to this assumption changes the calculus substantially. To reinforce this contention, actual growth exceeded potential growth prior to the pandemic, but reflation did not result.

The efforts to look at policy alternatives rigorously has a lot of merit. Unfortunately, the effort often clouds more than it clarifies.

Down Under

The U.S. and China have been embroiled in a trade war since 2018, but America isn’t the only nation whose relations with Beijing have soured. India finds itself in a border dispute with China, Canada has sparred with China over human rights, and the U.K. has objected to China’s handling of Hong Kong. Most recently, China’s trade relations with Australia have been unraveling.

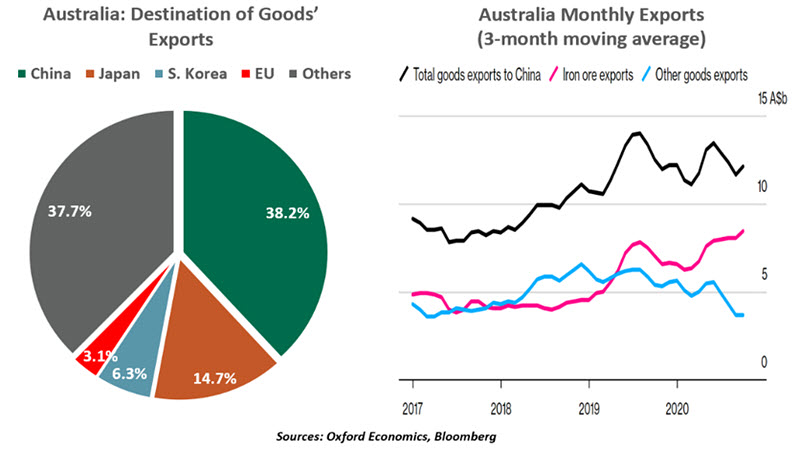

Australia’s moves to ban Chinese technology companies from its 5G network and to call for an inquiry into the origins of COVID-19 have triggered a series of sharp responses from Beijing. Australian wine and barley are now subject to heavy tariffs (212% and 80% respectively), and Chinese importers were asked to stop buying Australian cotton, lobsters and coal (stranding 6.4 million tons of coal in the waters outside China’s ports). Tariffs have forced Australian exporters to explore other markets, but the direct cost to the economy and trade has been nominal (about $3 billion in lost exports last year out of $100 billion plus in annual exports to China).

A lasting severance of trade ties with China will inflict visible damage on Australia’s economy. Australian exports to China have risen every year since 2016, following the China-Australia Free Trade Agreement (ChAFTA) in 2015. In fact, Australia is more dependent on China than on any other advanced economy in the world, with China accounting for nearly 40% of Australian goods exports.

Australia is the world’s largest producer of iron ore, the raw material for making steel. China spared this commodity from tariffs, to prevent damage to its own economy. Over half the iron ore consumed in China is imported from Australia: restrictions on those imports would disrupt China’s steel industry and in turn its infrastructure growth ─ a key contributor to the economy. So Canberra holds some of the cards in the trade dispute.

“Australia’s exports depend on China, and China’s production depends on Australia.”

Just as the U.S.-China trade war has left both nations worse off, this one too bodes poorly for both parties. But at some point, Beijing will have to re-think how many trade battles it can afford without causing harm to its economy. Punishing partners may lead them to look for better relationships elsewhere.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

More 529/College Planning Topics >