Vaccine Nationalism, Minimum Wage, Rising Energy Prices

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWeighing the costs of global vaccine access, minimum wage and the energy rally.

In this Issue:

- Variation In Vaccination

- More On The Minimum Wage

- Mixed Messages For Oil Producers

Nationalism is an ideology that promotes the interests of a nation, often to the exclusion or detriment of other countries. Rising nationalism across several countries in recent years has been at the root of geopolitical tensions and trade disruptions around the world. Now that school of thought threatens public and economic health.

Vaccine nationalism, where nations prioritize their own access to vaccines, is on the rise amid the ongoing global pandemic. A similar pattern was seen during other health crises, including the 2009 H1N1 influenza pandemic and the outbreaks of HIV/AIDS, smallpox and polio. In all of those instances, vaccines became available to poor nations only after the high-income group had secured adequate supplies.

The ideology isn’t new, but the stakes are higher this time. COVID-19 has taken an enormous toll: about two-and-a-half million lives have been lost and hundreds of millions of people have lost income (from employment loss or business closures). Even $12 trillion worth of fiscal support and trillions in newly printed money from central banks have thus far failed to cement a full recovery.

A year of intense research into more than 230 vaccine candidates has led to seven vaccines showing promising results, giving hope that the worst humanitarian and economic costs are behind us. However, the world is facing a reality check. The economy is facing a tougher start to 2021 than expected as infections surge and vaccine rollouts face hurdles.

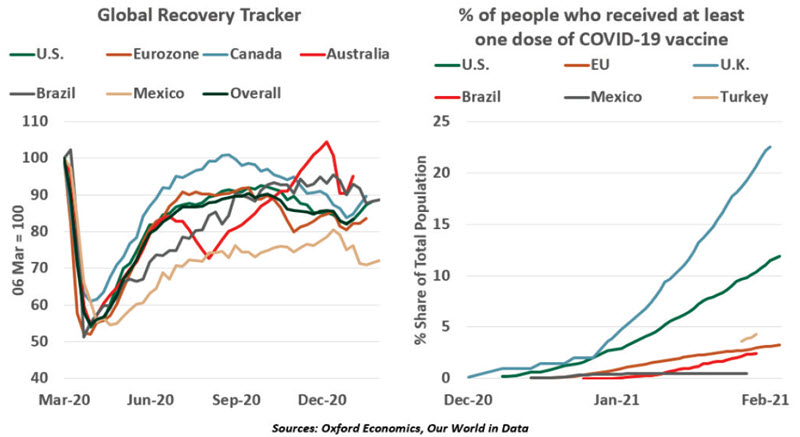

Finding the right vaccine hasn’t been enough to conquer the pandemic. Boosting production and making logistical arrangements to run mass immunization campaigns are proving to be extremely challenging, even for advanced economies. Inoculation programs have gotten off to a slow start, with Europe the worst performer among developed areas. Only 0.4% of the world’s population has been fully vaccinated. The share of the population that has received a first shot stands at 22.9% in the U.K. and 11.9% in the U.S., compared to only 3.4% in Germany and France, 3.3% in Spain, and 3.0% in Italy.

The immunization rate is improving. In the U.S., a daily average of 1.7 million doses are being administered; in the U.K., 0.4 million. That said, achieving herd immunity won’t be easy, given widespread hesitation to vaccination and the potentially low efficacy of vaccines against new variants of the virus. At the current rate, it will take nearly five years to cover 75% of the world population with a two-dose vaccine. This presents a significant threat. The longer COVID-19 is at large, the higher the risk of more transmissible and pernicious variants and consequent recurring disruptions to mobility and activity.

“Vaccine nationalism is triumphing over vaccine multilateralism.”

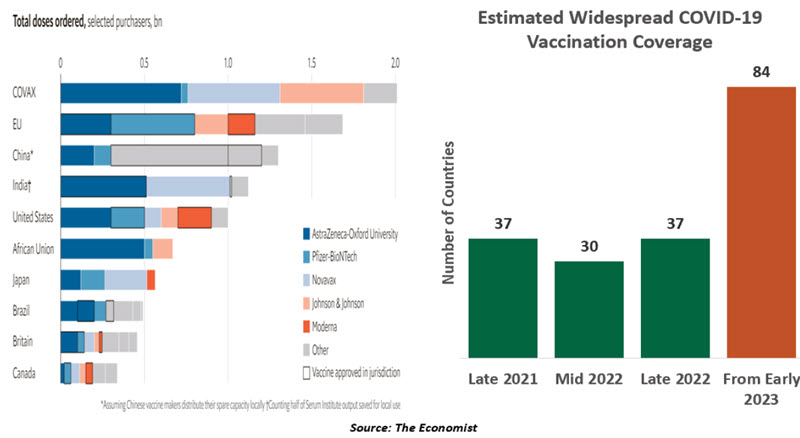

While advanced economies are administering vaccines, most low-income nations haven’t even started, which may leave some parts of the world achieving herd immunity faster than others. Many advanced countries have pre-ordered more doses than necessary to inoculate their populations. Of the 12.5 billion doses committed by major vaccine producers this year, 6.4 billion have already been ordered by rich countries. This has left poor nations to turn to the World Health Organization (WHO) or consider vaccine diplomacy, which may come with strings attached.

Most low-income countries are pinning their hopes on COVID-19 Vaccines Global Access (COVAX), a WHO-led initiative aimed at global procurement of COVID-19 vaccines. But COVAX can’t meet all requirements for mass immunizations in low-income countries. The 1.3 billion doses secured under the scheme thus far will only be enough to immunize about 20% of each country’s population this year. Further delays are likely, considering some producers (like those in the EU) have been ordered to restrict exports of vaccines.

Funding is another problem for the multilateral initiative. COVAX is currently facing a funding gap of $4.3 billion to procure vaccines for the most needy countries. It is operating without participation from China and the U.S., though the Biden administration has indicated it intends to join.

Global herd immunity will be difficult to achieve at all. More than 80 poor nations will not have widespread access to coronavirus vaccines before 2023. For most middle-income countries, including China and India (with high vaccine production capacity), the vaccination timeline will stretch to late 2022. Even if low-income countries can secure adequate doses, the challenges to vaccination faced by economies with better health and financial infrastructures suggest those countries will struggle with cost and logistical issues (like a lack of cold storage facilities) in vaccinating their populations.

“Vaccines will be the best economic stimulus for cementing the global recovery.”

It is understandable that governments are under pressure to prioritize their own citizens. But the costs of delayed mass inoculation will be immense for all. Developing nations forced to default to long lockdowns will hamper trade and supply chains, dampening the economic recovery globally. Many are already at risk of debt distress and finding themselves on the downward leg of the K-shaped recovery. Unequal access to vaccines will reverse years of economic progress of developing nations and increase the risk of social unrest. According to the International Monetary Fund, countries with more frequent and severe epidemics experience greater unrest. The International Chamber of Commerce has estimated that the global economy stands to lose up to $9.2 trillion, a burden that will afflict both developing and advanced economies.

The failure of multilateral institutions to ensure adequate supply to poor economies will create a vacuum allowing countries like Russia and China to use vaccine diplomacy to further their interests. The motives behind China’s Belt and Road Initiative should serve as a caution.

Strong multilateral cooperation is required to bring the pandemic under control. Vaccine nationalism is a recipe for disaster. As WHO Director-General Tedros Adhanom Ghebreyesus recently warned, “these actions will only prolong the pandemic, the restrictions needed to contain it, and human and economic suffering.” So long as the pandemic threatens any part of the world, normalcy will not be restored anywhere.

Fight For $15

Ryan explores proposals to raise the minimum wage.

I still remember receiving my first paycheck. My initial day of employment at a retail garden center fell on the last day of a pay period. One day of work at the then-minimum wage of $5.15 came to net pay of about $35. Handing me a check, the store owner shrugged and said, “Sorry.”

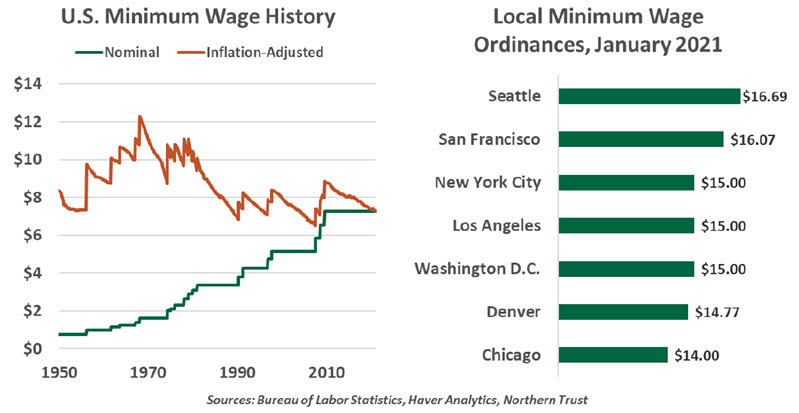

Minimum wages may be low, but they are an important safeguard. By setting a floor on the value of labor, these laws guard against worker exploitation. The U.S. passed its first minimum wage of $0.25 in 1938, after which it was raised incrementally to $7.25 in 2009, where it still sits today. Proposals to increase it have attracted renewed debate as to its appropriate level.

Critics of the Biden administration’s proposal tend to focus on the headline of a hike to a $15 minimum wage. However, it is important to note that $15 would not become the target wage until 2025. The wage would rise to $9.50 upon passage, then grow in annual increments to $15.

Going more than a decade without a raise may feel like a long stretch, but in practice, most low-wage workers have seen increases. Twenty-nine states have minimum wages greater than the federal level, and dozens of cities and counties have set even higher standards. While $15 sounds high to many observers, it has been the standard in a handful of cities for years. Several large employers have policies of paying well above the minimum. A federal minimum wage is a blunt tool for a nation as large and economically diverse as the United States; local policies have allowed areas with higher costs of living to tailor their policies as needed.

Local wage shifts have enabled expansive volumes of research, starting with a seminal study of the cross-border effects resulting when New Jersey set a higher minimum wage than neighboring Pennsylvania in 1992. Employment did not fall in New Jersey as much as economic theory would have predicted. Studies have come to disparate conclusions, and papers can be cited to support a variety of opinions. One theme has emerged from several studies: employers pass higher wage costs to consumers in the form of higher prices. This is not a bad outcome in areas with higher-income earners who can afford price increases. Raising the wage nationally, however, may lead consumers who cannot afford higher prices to change their purchasing behaviors.

The wide range of interpretations is evident in the Congressional Budget Office (CBO) evaluation of Biden’s wage proposal. The CBO foresees mixed results: Aggregate income to workers who stay employed would grow by $509 billion over ten years, but $175 billion of wages would be lost due to lower employment. The CBO estimates total payrolls would fall by 1.4 million workers, but the number of people in poverty would fall by 900,000. These results can provide fuel for any sort of motivated reasoning.

“$7.25 is low, but $15 is high in much of the nation.”

In practice, the downsides of minimum wage increases have rarely been as stark as economic theory predicts, and their ripple effects can be strong. While less than 1% of workers earn the federal minimum wage, an increase lifts up everyone earning a wage between the old and new minimums. Greater wages can reduce dependency on social safety nets and increase personal consumption, which flows through to tax revenues.

Biden’s plan includes a provision that is worthwhile regardless of the current wage level. After reaching its $15 target, the minimum wage would automatically adjust each year based on the growth in aggregate wages. This indexing would address the long intervals during which nominal wages lose their real value, and hopefully head off contentious debates in the future.

Local policies have been an incomplete stopgap, and voter enthusiasm for the $15 proposal shows the national rate has been neglected for too long. Millions of workers carry on at or near these pay rates. An increase is due, even if not all the way to $15. Indexing to inflation thereafter would allow us to put these unpleasant arguments behind us, making them as distant a memory as my “sorry” minimum wage paycheck.

Fueling Confusion

Increases of 50% in an individual stock price over a short span of time are not uncommon these days. After the recent mania over GameStop and Bitcoin, 50% seems pedestrian.

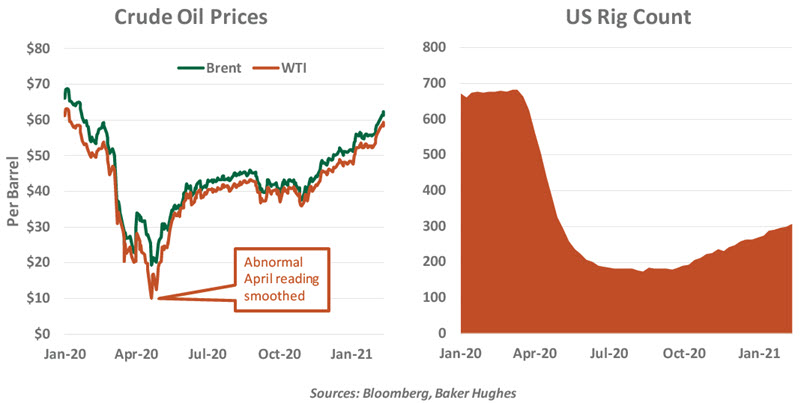

So the 50% increase in oil prices since last fall has not garnered the attention it might have normally. But it has had an important impact on markets: energy prices feed directly into inflation and inflation expectations. Higher costs for crude have been a subtle contributor to the reflation trade, which has driven long-term interest rates upward around the world.

The price of a barrel of oil decreased sharply during the initial phases of the pandemic, falling from about $60 to $20 during the first quarter of 2020. Petroleum is used primarily for transportation, and demand collapsed when households were locked down, shipping demand softened and airlines parked large portions of their fleets. Mobility is one of the new data series we have tracked during the pandemic, and it has remained depressed even as public health restrictions eased.

“We’ll still need a lot of petroleum on our way to a greener future.”

Oil markets began recovering last summer, as major producers agreed to restrict supply. But prices really began to accelerate when COVID-19 vaccines were perfected, bringing the promise of a full economic recovery and normal levels of mobility.

What has been surprising in the recent run-up is the tepid response from U.S. producers; the number of active wells remains down more than 50% from their peaks of a year ago. U.S. suppliers had taken on a substantial amount of debt to finance their operations, which became too much to bear when the pandemic hit. Having worked to get borrowing under control (in some cases, through bankruptcy), energy firms are loath to lose discipline. And the new U.S. administration’s plans to address climate change are giving these companies pause.

Many economies around the world are seeking to become carbon-neutral. But they will be dependent on fossil fuels, at least to some degree, for some time to come. Balancing the quest for a greener future with the desire for moderate energy costs in the present will be a real challenge.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All