For the past several decades, investors have generally been playing limbo with inflation. No matter how much they lowered their expectations, somehow inflation seemed to squeeze under the bar. The limbo dance could be over. Investors should now realize inflation expectations are set very low and inflation seems increasingly likely to hurdle that very low bar.

Whenever one hints at an increase in inflation, one is immediately asked how high inflation might go. However, that’s the wrong question.

Investors should ask “what’s the probability inflation could be higher than expected?”

Consensus inflation expectations are roughly 2% (based on TIPS break even rates), so the pertinent question is what is the likelihood that inflation will be higher than roughly 2%. We think jumping that hurdle is currently much easier than investors believe.

The game has shifted from limbo to hurdles.

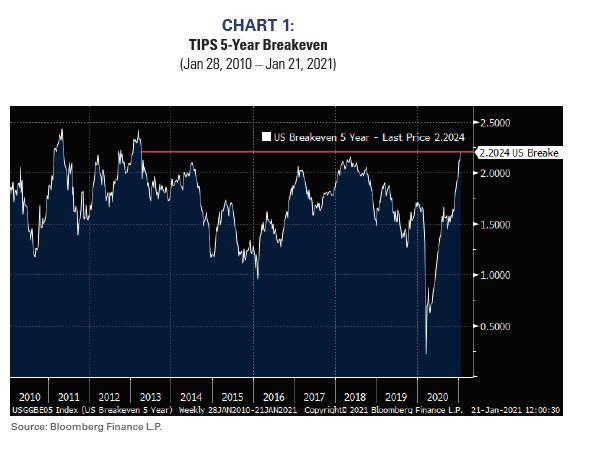

Breakevens on the rise

TIPS breakevens, or the implied inflation rate that equates TIPS1 to nominal Treasuries, has been rapidly rising of late. Of course, some of the increase is simply attributable to the increase in economic activity subsequent to the pandemic shutdown, but it is likely attributable to other factors as well.

Production bottlenecks have appeared in the global economy, US wages are rising at a fast pace, unionization may be increasing, import prices are no longer fostering deflation, and record US money growth seem to suggest the upward trend in breakevens might not be quite as temporary as some believe.

Five-year breakevens have rebounded sharply and are now the highest in eight years.

CHART 1:

TIPS 5-Year Breakeven

(Jan 28, 2010 – Jan 21, 2021)

In 1981, Reagan disbanded PATCO. Today, Google unionizes.

August 5, 1981 was a seminal date in the fight against inflation. On that day, President Reagan disbanded the Professional Air Traffic Controllers Organization (PATCO), and union power began a multi-decade ebbing.

The link between union membership and wages has been a hot political issue ever since, but it is relatively clear the decline in US union membership has been a major disinflationary force.

Recently, there was an event that seems equally as important, but in the opposite direction. Few observers have commented on the inflation implication of the recent unionization of Google. It will be interesting to see if the declining trend in union membership that began in 1981 starts to reverse, labor costs increase, and 2% inflation becomes more easily achievable.

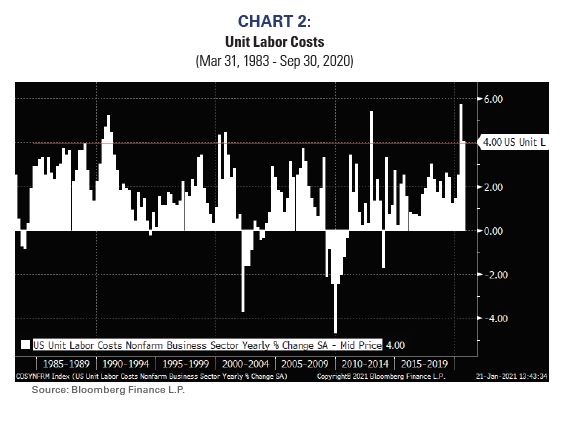

Unit Labor Costs rising at an unusual rate

Unit Labor Costs (ULCs), which measure the cost of labor per unit produced, are one of the basic building blocks of inflation. Higher ULCs imply lower productivity and lower profit margins, and companies have historically often reacted to margin pressure by attempting to increase prices.

From 1983-2019 there were only 7 quarters during which ULCs rose 4% or more and only 1 quarter since 2000. However, ULCs during the past two quarters have risen faster than 4%. There have not been two consecutive quarters during which ULCs rose more than 4% since the early 1990s. Yet, forecasters remain sanguine about inflation despite that the past two quarters’ increase in ULCs is so rare.

CHART 2:

Unit Labor Costs

(Mar 31, 1983 - Sep 30, 2020)

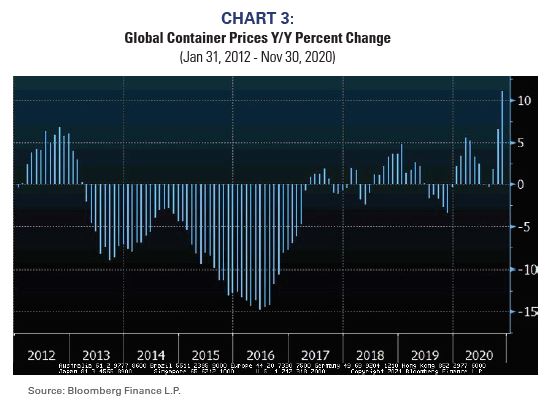

Trade costs rising

Despite political rhetoric, the US trade deficit has again ballooned, and is back to the worst levels of 2008/9. A trade deficit is not necessarily bad if the dollar is strong and the US imports deflation.

However, as many a developing world economist can attest, a trade deficit’s negatives can be compounded by a weak currency and importing inflation.

While one has to be careful making hyperbolic comparisons of the US economy to developing world economies, the combination of ballooning trade deficit and global trade bottlenecks suggest the consensus forecast of 2% inflation could be too low. For example, global container prices are now rising more than 10% and anecdotal evidence shows shipping bottlenecks appear to be increasing both in number and magnitude.

CHART 3:

Global Container Prices Y/Y Percent Change

(Jan 31, 2012 - Nov 30, 2020)

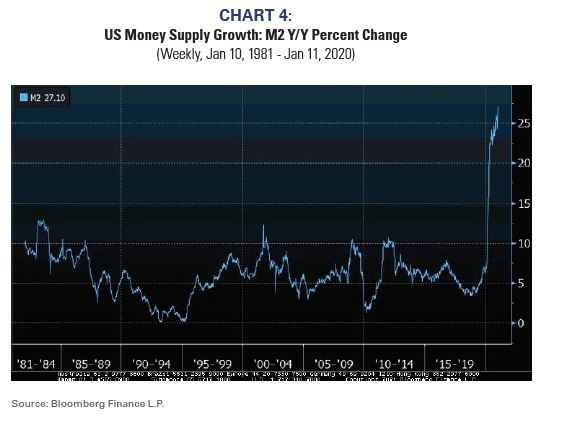

Money growth off the charts

US money growth is literally off the charts. M22 growth is now 27%, by far the fastest growth in the nearly 40 years of data. To further put this in perspective, this is the first time US money growth is faster than China’s money growth. It won’t take much for 27% money growth to translate to an inflation rate greater than 2%.

Some have said very low velocity of money3 prevents inflation from occurring. The velocity of money has indeed been decreasing, but “prevents” may be too optimistic when money growth is so strong. The current velocity of money is about 1.1. Using 25% M2 growth and current money supply and nominal GDP, nominal GDP would still grow more than 6% even if the economy could not absorb the extra money and velocity plunged to 0.95.

CHART 4:

US Money Supply Growth: M2 Y/Y Percent Change

(Weekly, Jan 10, 1981 - Jan 11, 2020)

Take the “over”

For many years, investors repeatedly won by taking the “under” on inflation regardless of how low inflation expectations were. However, the global and US economies may be changing in such a way it might prove beneficial to start taking the “over” on inflation. Such a shift would drive a wholesale reshuffling of leadership as investors reposition within markets. Long-duration growth tech stocks would not look as attractive in a period of sustained higher inflation. Cyclical companies levered to nominal growth may come back in vogue. The long duration bet within fixed income that worked so well for the last several decades may be jettisoned in favor of shorter duration bonds. Indeed, inflation seems to hold the key to a sea change in nearly every asset class.

Get ready for inflation to shift from limbo to hurdles.

1 TIPS: For descriptors, see “Index Descriptions” at end of document.

2 M2: For descriptors, see “Index Descriptions” at end of document.

3 Velocity of Money: For descriptors, see “Index Descriptions” at end of document.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

TIPS: US Treasury Inflation-Protected Securities, or TIPS, provide protection against inflation. The principal of a TIPS increases with inflation and decreases with deflation, as measured by the Consumer Price Index. When a TIPS matures, it pays out the adjusted principal or original principal, whichever is greater. TIPS pay interest twice a year, at a fixed rate. The rate is applied to the adjusted principal; so, like the principal, interest payments rise with inflation and fall with deflation.

M2: M2 Money Supply consists of M1 plus (1) savings deposits (including money market deposit accounts); (2) small-denomination time deposits (time deposits in amounts of less than $100,000) less individual retirement account (IRA) and Keogh balances at depository institutions; and (3) balances in retail money market mutual funds less IRA and Keogh balances at money market mutual funds. Seasonally adjusted M2 is constructed by summing savings deposits, small-denomination time deposits, and retail money funds, each seasonally adjusted separately, and adding this result to seasonally adjusted M1. M1 consists of (1) currency outside the

U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) demand deposits at commercial banks (excluding those amounts held by depository institutions, the U.S. government, and foreign banks and official institutions) less cash items in the process of collection and Federal Reserve float; and (3) other checkable deposits (OCDs), consisting of negotiable order of withdrawal, or NOW, and automatic transfer service, or ATS, accounts at depository institutions, credit union share draft accounts, and demand deposits at thrift institutions. Seasonally adjusted M1 is constructed by summing currency, demand deposits, and OCDs, each seasonally adjusted separately.

Velocity of Money: Velocity of money is the average number of times a unit of money (as measured, for instance, by a monetary aggregate, in this case M2) turns over during a specified period of time.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be inappropriate for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided “as is” without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

© Copyright 2021 Richard Bernstein Advisors LLC. All rights reserved. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

© Richard Bernstein Advisors

More Asian/European Markets Topics >