Evolving Risks, School Reopenings, Long-Term Rates

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn this Issue:

- New Risks: Normalizing the Abnormal

- Getting School Back in Session

- Long-Term Rates, Near-Term Concerns

The eager entrepreneur sits at the desk of a startup investor, seeking the seed funding that will allow her to open her dream restaurant. “Your pitch sounds great,” says the investor, “but I have one question: Could your business survive a year-long government shutdown mandate that prevents customers from dining on premises?”

Not long ago, that question would sound preposterous, perhaps paranoid. Today, it is legitimate.

Our concept of plausible risks has entirely changed. COVID-19 is top of mind, and not just because of business risks like those described above. The scope of health risks and necessary mitigations has widened; we newly question whether merely leaving the home is wise or necessary.

A variety of adverse events have occurred recently, as simmering risks boiled over. While climate change takes place over a long range of time, it can manifest suddenly. The recent cases of Texas freezing and California burning added to a rising frequency of severe natural disasters around the globe. These episodes are consequences of the long-running (and long-ignored) risks from pollution. Reports of high-profile cybersecurity incidents are on the rise, the result of the gradual increase in concentration among technology service providers and a steady accumulation of bad actors.

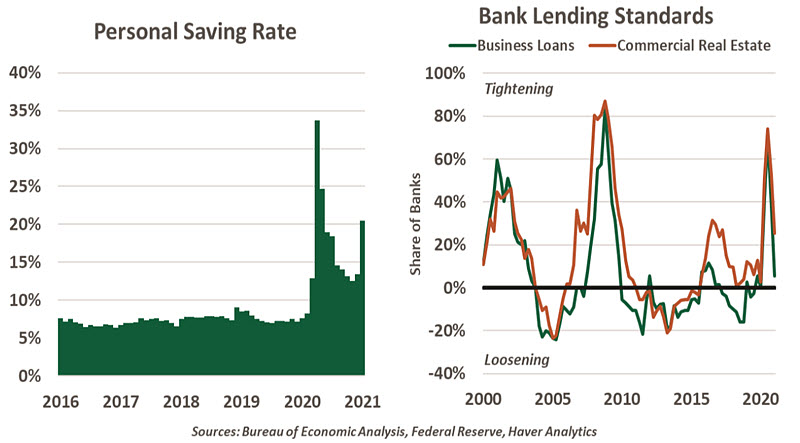

Unforeseen events quickly and palpably rattle markets. In 2008, equity markets sold off, the Cboe Volatility Index (VIX) reading set a new high, and bond yields plumbed new depths as the financial sector reckoned with an overproduction of mortgages. Though it felt like a once-in-a-lifetime interval of stress, just 12 years later, the pandemic brought about an even more severe downturn. Last March witnessed another record high in the VIX and a plunge to even lower depths in yields. And just as markets stabilized, the GameStop mania provided sudden evidence of the long-term rise of social media and the decades-long collapse in the cost of trading shares.

Taken together, abrupt shocks feel overwhelming, and their causes insurmountable. When uncertainty prevails, our instinct is to limit our exposure to risks. But the flight to safety can be an overreaction. Behavioral research has taught us about the recency bias, in which the experiences freshest in our minds feel most likely to recur. Unpleasant memories can suppress risk appetites: Investments slow and cash becomes more appealing. These were both drivers of the equity market sell-off in March 2020.

Normalizing the abnormal leads to broad and long-lasting risks to the full economy. Cognitively, a lack of certainty renders every decision harder to make, from social plans to business deals. Simple solutions gain appeal as our mindset shifts from growth to mere survival. At the height of a crisis, simple plans like universal lockdowns are effective. Confidently transitioning back into normal operations is difficult, as seen in the complex decisions to reopen schools, discussed below.

When stress arises, we expect our leaders to act, but their interventions can create moral hazard. In Texas, federal emergency support helped to prevent the worst outcomes, but was needed only because the state power system lacked resilience. The tendency of homeowners to rebuild on flood plains after their homes have been washed away is another example where better preparation would have avoided public costs. To avoid the worst case scenarios, economic actors must be incented to plan ahead; the courts and insurance carriers are carrying this message.

“Decision-making requires confidence in the future, which is in short supply.”

As tail risks become more frequent and their manifestations more severe, business continuity plans are growing in scope and importance. Employers must plan for staff shortages, supply chain disruptions and new ways of serving customers. Governments must plan for disruptions of all kinds and pursue policies that reduce their frequency and severity.

Elevated risk can alter the trajectory of growth in more permanent ways. Displaced workers do not recover lost wages; the decline in the U.S. labor force suggests many workers are waiting out the crisis on the sidelines, hoping for their jobs to return as demand recovers. Larger corporations gain an advantage, as they are more likely than their smaller competitors to have the resources to weather a storm, impairing the entrepreneurial lifecycle.

On the brighter side, volatility can present opportunity. For all our fears that firms and households will hold to a more conservative mantle, we see a glimmer of hope in the data. Contrary to past recessions, in 2020, the U.S. Census Bureau reported a sudden rise in new business applications. These appear to be primarily online businesses, often sole proprietorships. Online startups have never been easier to launch, and consumers have spotted opportunities to start small ventures. Sudden shocks can lead to rapid adaptation.

“Events can only be “unprecedented” once.”

Crises will pass, leaving behind war stories and lessons learned. Organizations need a robust risk management framework to identify, measure, mitigate and monitor risks. The inventories of risks may be growing, but they can still be managed. Some adaptations in the current crisis may bring about permanent changes, like more jobs being done entirely from home. Disasters, pandemics and other crises will happen again. Avoidance is not possible, but resilience is.

The aftermath of a crisis is also an opportune time to revisit public responses. Direct government intervention, whether by paying unemployment or sandbagging buildings on a flood plain, is costly and inefficient. Resources would be better directed at reducing the frequency and severity of crises than responding to them. Infrastructure investments can help reduce some climate risks, while prudent regulation can limit risky behaviors.

Smart planning can keep our imagined restauranteur from defeat. Many restaurants have demonstrated that they can scrape by with carryout orders, delivery and cook-at-home meal kits. These alternatives now belong in all business plans going forward. The unexpected can provide very useful food for thought.

Class Action

Ever since COVID-19 vaccines showed promise in the lab, strategies for implementing them have been the subject of active debate. Public health considerations are at the forefront as allocation decisions are being made, but economic considerations can’t be too far behind. The pandemic has been incredibly costly to many workers, firms, and communities; commerce cannot truly heal until life returns to a more normal cadence.

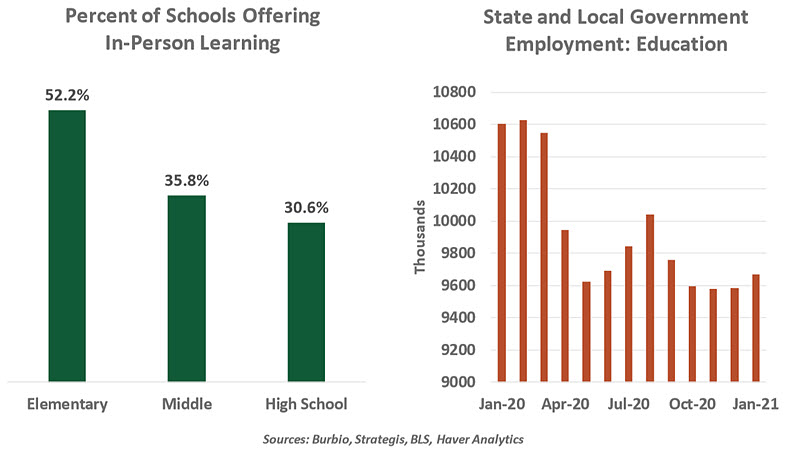

A central part of this effort is getting schools reopened. When students were sent home last spring, the ensuing ripple effect hindered the economy in the present, and will hinder it in the future. Parents were forced to become tutors, proctors, and hall monitors, which took time away from their jobs. Keeping up with both proved too much for thousands of workers, some of whom dropped from full time to part time or left the labor force to oversee their children. This burden has fallen disproportionately on women, for whom labor force participation has fallen sharply; some observers have termed this a “she-cession.”

Whenever anyone reduces their participation in the labor market, they often find it hard to re-enter. On-the-job learning stops, and networks atrophy. (Labor economists call this “scarring.”) Financially, savings are depleted and lifetime earnings prospects diminish.

As we discussed last week, students have typically had a substandard experience with distance learning. Many do not have the devices or internet access that “attendance” now requires; others don’t pay the same attention at home that they would in the classroom. Access to extra instruction is uneven. The loss of education time and quality during the pandemic will diminish innovation and productivity for many years to come.

Learning at home also deprives students of the social interactions that take place at school, which are an important part of their development. Sports and activities have been cancelled. And almost a million educational jobs have been lost at the state and local levels over the past year, as shuttered schools reduce their payrolls.

“Reopening schools is a critical step in the journey to a full economic recovery.”

Recognizing this, officials have been trying to find a formula for getting classrooms reopened just as soon as possible. Hybrid schedules and shifts have been attempted, but these systems call for students to be sent back home if a classmate tests positive. The on-again, off-again cycle makes it difficult for parents to commit to a work schedule.

According to research from the Centers for Disease Control, schoolchildren account for a very small percentage of COVID-19 cases, and “in-person learning in schools has not been associated with substantial community transmission.” Residual risk can be managed with masking and contact tracing. But debates over these measures at some school board meetings have been difficult, mirroring the broader dissonance surrounding pandemic management that has been on display for most of the past year.

Mistrust between faculty and administrators, especially within public education, has not helped. The two groups have found it difficult to agree on health protocols, with teachers defying back-to-work instructions until a high level of safety can be guaranteed. Each side has claimed that self-interest, and not students’ interest, is the opponents’ motivation.

Successive stimulus packages have allocated substantial amounts of money to help reopen schools. According to Strategas, an economic consulting firm, Congress has appropriated roughly $1,000 per student for this effort, with much of it unspent. Whatever administrative hurdles are preventing the disbursement of these funds should be cleared as soon as possible.

Health care workers have been deemed essential to battling COVID-19, and have been included in the first wave of inoculation. Thereafter, teachers should be given a place near the top of the list. Getting schools back into session will accelerate recovery from the recession.

Non-Taper Tantrums

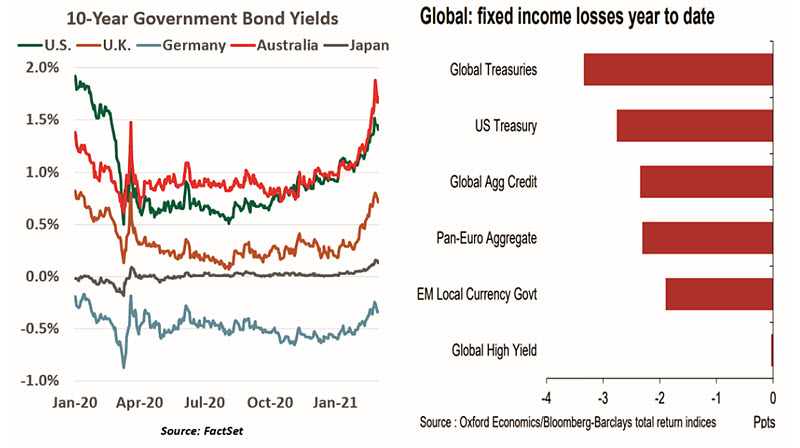

Since the turn of the year, vaccine progress, growth optimism and prospects of substantial fiscal stimulus have led to upward pressure on sovereign bond yields around the world. Last week, the 10-year U.S. Treasury yield reached its highest level in a year, with similar trends visible in other major markets.

“Long-term rates have risen, but not to alarming levels.”

Australian bonds were the worst hit, with the yield on the 10-year government bond almost doubling in just one month. The Reserve Bank of Australia (RBA) intervened by increasing its pace of bond purchases, leading to the sharpest rally in bond prices since the turbulence last March. High rates attract foreign investment and make the Australian dollar stronger, which hinders the country’s trade competitiveness. The RBA’s intervention was meant to blunt this development.

Other central banks have stayed on the sidelines, as they see interest rate increases as a healthy correction. Very low yields have been blamed for fueling increases in asset prices that may not be sustainable, and the reversion in rates may therefore curb the enthusiasm. And intervention might give markets a sense that the central bank has a yield ceiling in mind, which could promote unwanted outcomes in financial markets.

A continued sell-off, however, could force the hands of central bankers. In the U.S., tumbling bond prices are pushing mortgage interest rates upward, which could take some of steam out of the housing market. With the eurozone economy struggling, the European Central Bank may be forced to step up its Pandemic Emergency Purchase Program to prevent tightening of financial conditions.

And it should be noted that higher yields in developing countries can raise borrowing costs for emerging markets, which may not be in the best position to pay them. As we wrote recently, financial problems in the developing world could cause some measure of financial instability.

Yields have risen suddenly, but they are now approaching levels seen just before the pandemic hit the world. We do not foresee rising interest rates as a meaningful threat to building economic momentum.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All