Covered call strategies can help investors manage short-term volatility and may provide better long-term outcomes while seeking to provide attractive monthly income to investors

Equity markets snapped back from the COVID-19 related sell-off in early 2020. In fact, the S&P 500 is up 63% since its low in March 20201, supported by accommodative monetary policy (low interest rates) and fiscal stimulus. This has left many investors asking questions – are stocks too high?... is market volatility here to stay?... how can I diversify my portfolio2 and help meet my income needs?

Regardless of your short-term view on the market, over the long term, covered call strategies may enhance risk-adjusted returns and provide favorable upside/downside capture ratios.

We believe investors seeking to manage their equity market risk should consider equity covered call closed-end fund (“CEF”) strategies as a way of seeking to minimize downside exposure while meeting their income needs.

Why use covered calls?

BlackRock believes that by using an equity covered call strategy, investors can reduce portfolio volatility by capturing option premiums, without having to sacrifice long-term performance. In a covered call strategy, investors sell call options against their equity holdings and receive an upfront “option premium” in exchange for forgoing potential capital appreciation if the underlying stock appreciates above the option strike price. These option premiums generate cash flow which help to mitigate some of the downside risk to owning the stock.

Adapting to market changes with active management

BlackRock equity CEFs employ a unique approach to covered call strategies by primarily writing single stock options versus index options. Each strategy is customized in terms of the amount of overwriting (selling) on the portfolio and the underlying stocks that are covered as well as diversifying both how far in or out of money the option is and the time to maturity of the options. This strategy is designed to maximize upside capture and option premiums while mitigating downside risk.

To illustrate how this works in practice, as the market sold off and volatility spiked in March 2020, BlackRock increased strike prices across its equity CEF lineup (i.e. wrote options further out-of-the-money) while generating similar option premiums due to the elevated level of volatility. As a result, the funds were in a position to capture more upside as the market bottomed on March 21st. Combining active security selection with an active covered call strategy may produce better outcomes for equity-income investors, specifically in the CEF structure3.

Why single stock options?

BlackRock uses single stock options rather than index options. There are many benefits to the single stock approach including:

Maximizes portfolio manager flexibility

Provides portfolio management with the tools they need to capture their view on individual stocks rather than the market as whole (index options).

Harnesses greater volatility to seek to maximize income

Single stock options may offer higher option premiums, which may allow the portfolio manager to minimize the portfolio overwrite percentage, allowing the potential for greater capital appreciation.

Customizable to potentially boost returns

Enables collaboration with portfolio management teams to optimize overwriting strategy on a stock by stock, product by product basis by customizing the portfolio overwrite percentage, strike prices and duration of options.

The drawback to using single stock options is that you may get the security “called away”, potentially capping upside in the security.

The results..

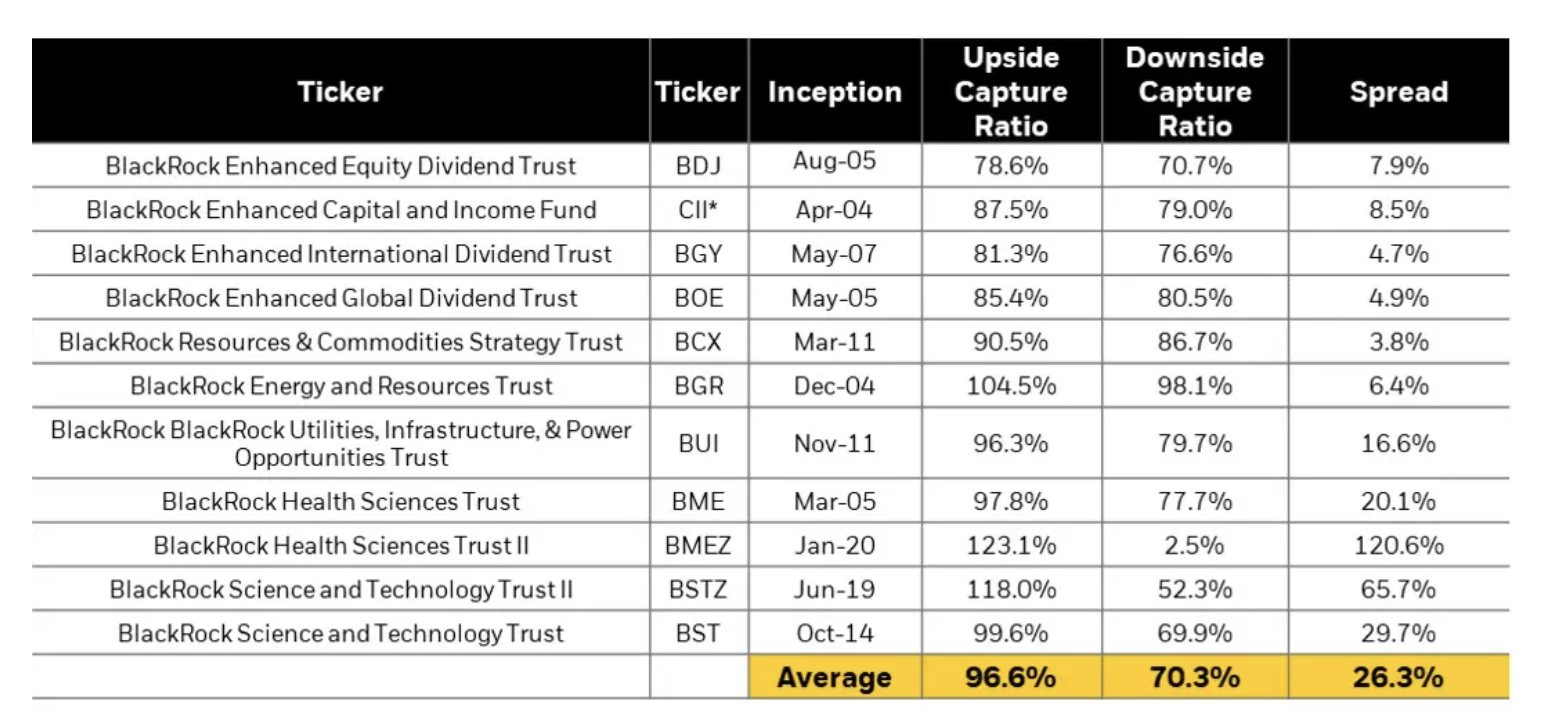

As indicated in Exhibit 1, this approach has produced asymmetric capture ratios, which means that, on average, the funds have achieved greater participation in rising markets with comparably lower participation in declining markets. The average upside capture ratio for BlackRock equity covered call CEFs is 96.6% and the average downside capture ratio is 70.3%.

Exhibit 1: Upside/Downside Capture Ratio

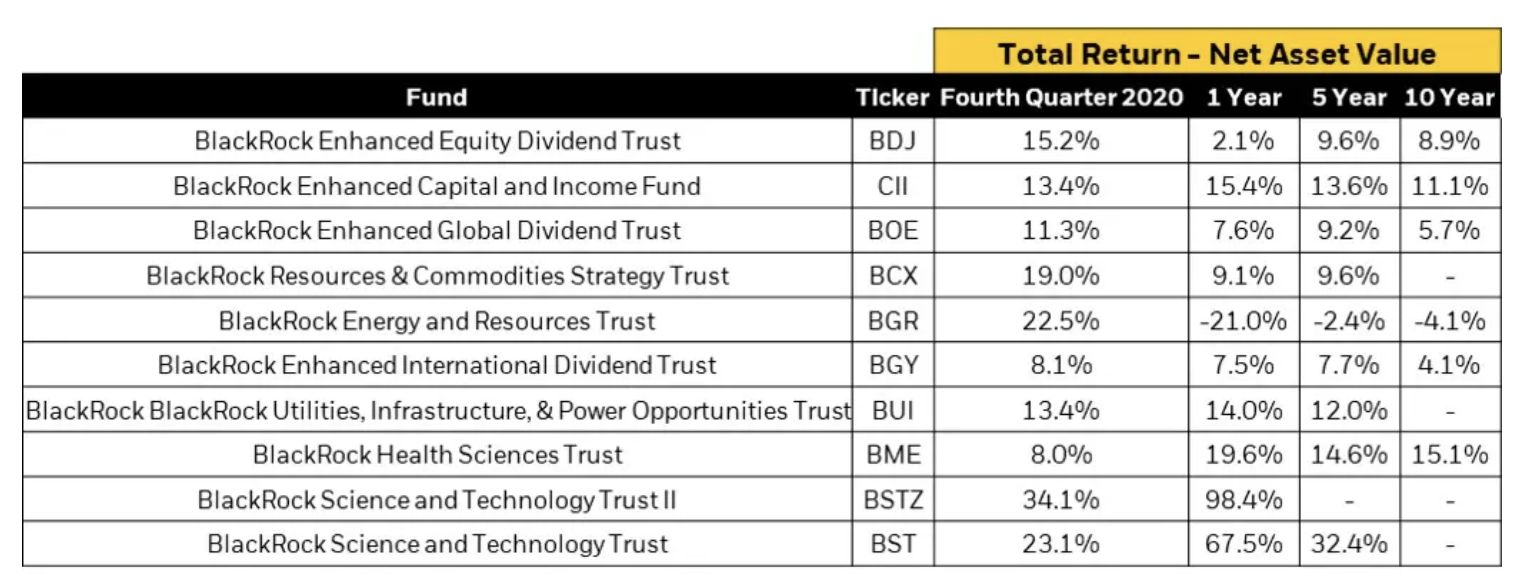

Exhibit 2: BlackRock Equity CEF NAV Returns

How can you potentially benefit from the closed-end fund structure?

• Potential for higher distribution rates relative to a long-only equity portfolio. Many equity CEFs, including all of BlackRock’s CEF equity products, use a managed distribution plan, in which the fund sponsor aligns the fund’s distribution rate with the long-term expected total return of the portfolio. A large portion of the distribution will be funded through capital appreciation (realized or unrealized capital gains from the portfolio and covered call strategy), essentially “monetizing” total return in the form of a monthly distribution to investors4. This allows equity CEFs to potentially pay out more than their mutual fund counterparts. The average annual distribution rate for equity covered call CEFs is 7.7%, compared to 2.4% for equity income mutual funds, according to Lipper5.

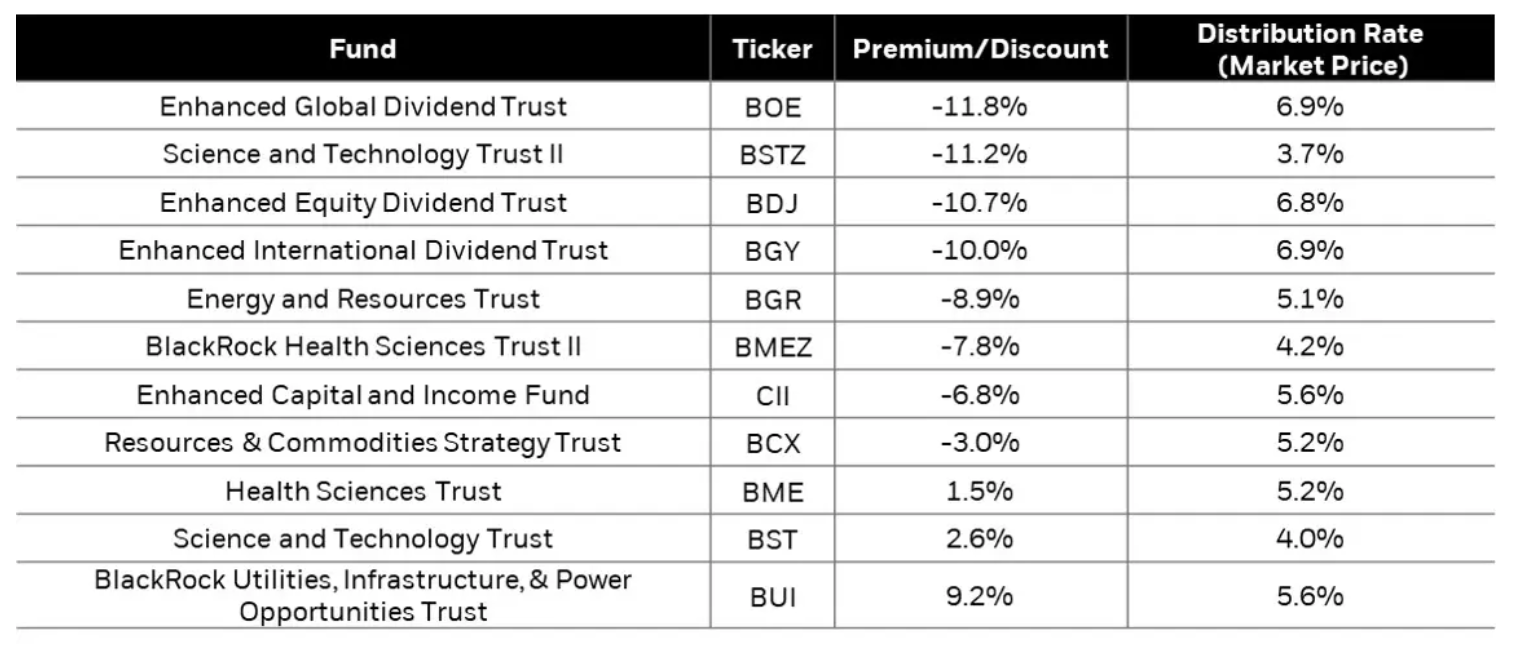

• Potential to buy funds at a discount CEFs effectively have two values for investors to evaluate. One is fund’s net asset value (“NAV”), or the aggregated value of its underlying holdings. The other is the market price of the CEF itself as it’s traded on the exchange. In many cases, equity CEFs are currently trading at a discount to their NAV. The average equity covered call CEF currently trades at a discount of -5.3%6. We believe this could present an entry point for long-term investors to buy equity securities at a “discount” to their current market value.

Exhibit 3: BlackRock Equity Covered Call CEFs

© BlackRock

Read more commentaries by BlackRock