Over the past month, the expectations of growth in the year ahead have surged, with fixed income markets repricing and investors shifting allocations in anticipation of growth. Though the movements can feel disconcerting, we see them as encouraging signals that the economy holds a great deal of promise for recovery.

The key risk to the outlook remains a COVID resurgence. The virus is mutating, but thus far, the new variants haven’t been overly threatening. Rapid vaccination is a driver of the currently well-controlled case rate and falling mortality, which we expect to continue. A full year into the COVID shock, we welcome reasons to be optimistic.

Influences on the Forecast

-

- The Biden administration has nearly passed its first significant policy, the $1.9 trillion American Rescue Plan. The package reflects the recent conventional wisdom that doing too much is preferable to a response that falls short, and modifications from the original proposal were minor. Negotiators deferred the $15 minimum wage proposal, pared back income eligibility for $1,400 economic impact payments, and lowered the federal unemployment insurance supplement to $300 from $400.

- With ratification this week, households have avoided a fiscal cliff of a loss of unemployment support. Small businesses and local government bodies will also gain from the package.

- The Department of the Treasury has proven capable of distributing funds quickly, which will lift income in March and consumption in the months ahead.

- The bill may prove to be too front-loaded. Most of the supports included in the legislation expire in September. If support is still needed later in the year, fiscal capacity and political will may be depleted.

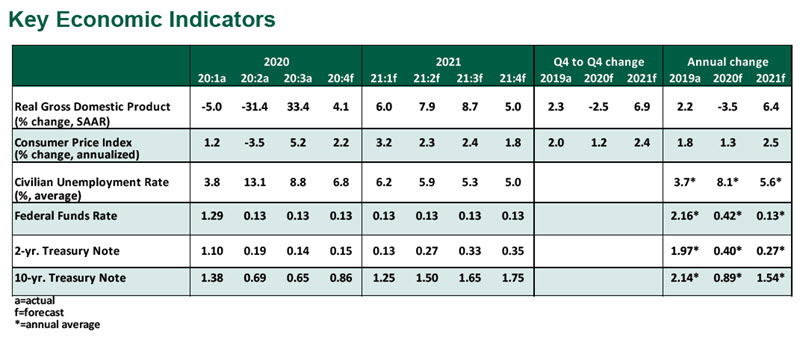

- On the basis of stimulus, vaccines, and pent-up demand, we have revised our growth forecast upward. Government spending may increase yet further if a sizeable infrastructure plan takes shape. Our forecast does not assume any further stimulus, but the potential exists for even stronger growth later in the year.

- The potential for growth has led to higher inflation expectations. Some transitory price shifts will be inevitable as consumers return en masse to deferred activities like restaurant dining and leisure travel. However, supply and demand will find equilibrium, and we do not expect sustained inflation that is too high for comfort. The rally in energy prices will raise headline inflation rates, but not core inflation readings that exclude food and energy. Year-over-year readings of inflation will also be elevated in the months ahead, as they will be comparisons against the deflation that occurred early in last year’s lockdown.

- Fixed income markets reacted to elevated growth and inflation prospects by selling off, leading to some worry about a challenge to the growth cycle. Higher yields increase the cost of corporate debt and raise mortgage rates, which may cool the housing sector. However, bond yields remain at historically low levels. The speed of the rise was more surprising than its direction. We do not expect substantial further increases in the near term, nor do we expect the Federal Reserve to alter its policies to address the long end of the yield curve.

- The employment report for February reflects a slow interval in the recovery. The unemployment rate improved only a tenth of a percentage point to 6.2%, and the labor force participation rate fell slightly. More than nine million workers remain displaced. The continued dislocation in labor markets is a frequently cited rationale for the Fed’s continued accommodative policies and the need for further fiscal support from Congress.

- High-frequency indicators are showing the beginnings of a recovery. Personal income in January increased by a rapid 10% month-over-month as $600 economic impact payments reached consumers. Personal spending rose by only 2.4%, lifting the personal saving rate once again above 20%. There are plenty of pent-up resources to sate pent-up demand.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust