Global Economic Outlook: Elusive Immunity

A dichotomy is appearing among advanced economies: Where inoculation programs are gaining momentum, economies are developing viral immunity and experiencing falling infections, lower mortality and improving economic activity. A strong economic rebound is anticipated during the summer in economies like the U.S. and the U.K., whose vaccination programs have progressed quickly. Consumers in these countries can sate their pent-up demand with substantial pent-up saving.

Bond markets in many countries have sold off in the past month amid growing concerns that extensive fiscal support and the release of pent-up demand may cause inflation to surge. We do not foresee rising yields as a major threat to economic recovery, as they are returning to the levels seen before the pandemic hit the world. We expect some transitory factors to generate higher inflation temporarily during the middle of the year, but lingering labor market slack will keep a lid on price pressure in the longer term.

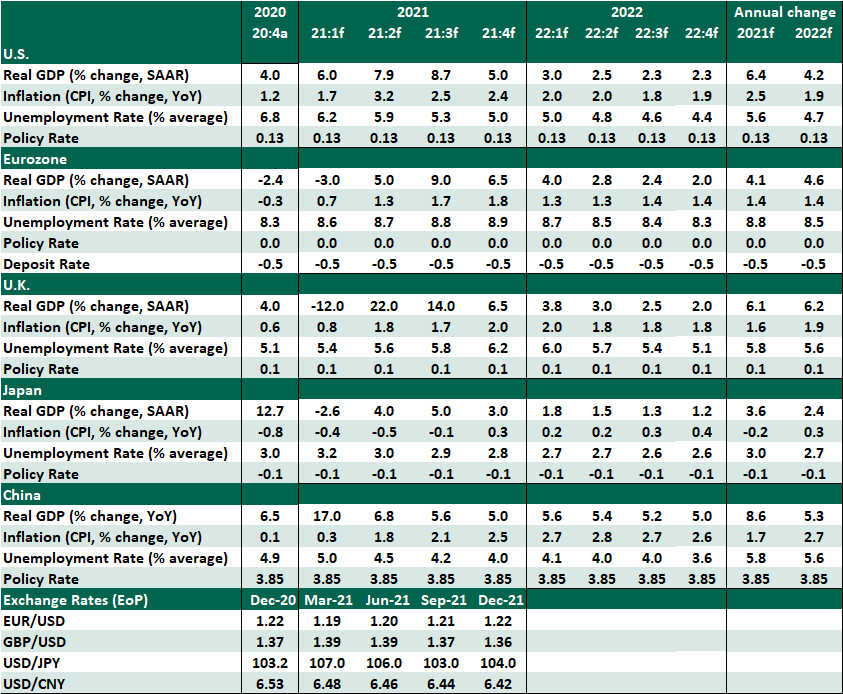

This month’s edition offers a deep dive into the eurozone economy, which is struggling to contain the coronavirus. We’ve also included quarterly detail in our forecast table.

Eurozone

- Vaccine rollouts continue to disappoint in many European countries, owing to manufacturing delays, sluggish delivery and concerns over potential side effects of a major vaccine. Although the health situation has generally improved since the start of the year, a recent increase in the number of infections has led to an extension of restrictions in some member states. As a result, there is a good chance that a widespread substantial reopening of economy will be delayed.

- The current set of restrictions on activity will cause a double-dip recession in the common currency region, but the extent of the damage will be far milder than that from the unprecedented shocks witnessed in 2020. We expect the vaccination drive will pick up pace in April as supplies increase and additional vaccines are approved.

- The improved rate of immunization will then contribute to a broad-based reopening of sectors and economies, triggering a strong consumer-led rebound into the middle of the year. But gross domestic product (GDP) will not recover to its pre-COVID level until early next year.

- Over the longer term, the eurozone recovery will largely be shaped by any lasting damage done to the labor market. Although most member states have automatic stabilizers or short-term work schemes in place to provide cushion, we expect the unemployment rate to remain elevated after these support measures are withdrawn.

- Inflation is set to rebound from the lows of 2020. Higher energy prices are pushing up headline measures, and year-over-year measures will be distorted by comparing current activity against an interval of lockdowns. These factors will send the headline inflation to closer to 2% at the end of the year, but only temporarily, as witnessed during early 2017. Core inflation will recover more gradually. Next year, the headline and core inflation are likely to converge and hover below 1.5% year-over-year.

- The better-targeted set of restrictions has allowed larger parts of the economy to function, though below normal levels. The construction and industrial sectors largely remain unaffected by restrictions and have continued to grow, while the consumer and service sectors continue to struggle with lockdown measures.

- Those counting on a “roaring twenties” summer holiday season this year will likely be left disappointed. In absence of a major boost to immunization programs, quarantine rules and travel restrictions could lead to another gloomy summer for the tourism industry. Tourism is an important sector of the eurozone economy, providing jobs to millions and accounting for an average of 11% of GDP in southern Europe and France. Countries like Greece, Spain and Italy won’t be able to fully recover without a widespread reopening of the tourism sector, potentially leaving them on the downside of a K-shaped recovery among nations.

- Against this relatively soft economic backdrop and downside risks to recovery, eurozone finance ministers have pledged to extend fiscal support through 2022 while brushing aside concerns about rising debt. Along with disbursements from the recovery fund approved last year, this will set the stage for a strong economic rebound in the second half of 2021, assuming the virus is tamed.

- While some central banks have been sanguine about the bond market sell-off and its implications for the economy, the European Central Bank (ECB) has taken a stronger tone. Realizing the fragile state of the eurozone economy and the damage that tighter financial conditions could cause, the ECB intends to ramp up its monthly asset purchases under the Pandemic Emergency Purchase Program. The central bank’s commitment to step up purchases will likely support bond prices and keep borrowing costs lower to support economic recovery.

- Brexit is done, but the new arrangement is causing trade disruption and tension between the U.K. and the EU. Britain unilaterally postponed the implementation of new trade arrangements between Great Britain and Northern Ireland, a move that will likely provoke retaliation from the EU. This move portrays the U.K. as a less reliable partner and will hamper negotiations on services and foreign policy matters between the two sides.