K2 Advisors Second Quarter Hedge-Fund Strategy Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWith a broad-based economic reopening coming closer into focus, investors are planning for the next stage in the cycle. Our K2 Advisors team believes geographical, asset class and sector rotations will be key to driving returns over the next 12 months. Brooks Ritchey and Robert Christian provide the team’s second quarter hedge-fund strategy outlook.

We expect hedge-fund managers who shift to securities that have lagged in recent years while hedging out broader market risks or shorting overvalued names will be more likely to generate high-quality returns.

Strategy Highlights

Long/Short Equity

While rising interest rates have triggered a rotation from growth into value, we expect our managers to capitalize on the increased dispersion. Rising inflation expectations should also favor long/short equity investors relative to other longer-duration assets.

Relative Value

Overweight outlook for volatility arbitrage and convertible arbitrage strategies driven by inefficiencies in pricing among various asset classes. Underweight outlook for fixed income arbitrage based on depressed volatility due to excess central bank liquidity.

Event Driven

Spreads have slightly widened but remain tight relative to historical averages. Increases in hostile activity and CEO confidence should be beneficial for the strategy. We believe n attractive opportunity set remains in the more complex merger situations as well as special situations equity, credit, and special-purpose acquisition companies (SPACs).

Credit

Long/short credit managers are increasingly focused on event-driven situations given low yields and tight spreads. Uncertainty in structured credit may lead to high levels of dispersion at the instrument, market, and manager level.

Global Macro

Managers remain focused on the macro trends accelerated by last year’s events and resulting accommodative policy mix that has continued into this year. Differences in economic recoveries between regions may provide opportunities for macro strategies.

Commodities

Inflation concerns, a weaker US dollar, tighter fundamentals, and positive roll yields are shining a brighter light on commodities. Winners and losers will likely emerge, increasing dispersion and favoring relative value strategies. We are overweight agricultural commodities on seasonal factors.

Insurance-Linked Securities

January 1 renewal rates were positive but not as strong as expected given capital flows into the space. We see a strong pipeline for cat bond issuance and likely positive pricing for June 1 reinsurance renewals following the large first-quarter US winter storm event.

Macro Themes We Are Discussing

Going into the second quarter of 2021 there are additional indications that the worst of the global COVID-19 health crisis is behind us. Multiple vaccines are available and being administered across the globe, hospitalization rates are plateauing or declining, and businesses are slowly reopening. Now what?

Where does a hedge fund or long-only fund manager allocate assets to both avoid areas of risk and capture returns in a post-pandemic world? We discuss these and other questions below.

Are equity and corporate debt valuations getting stretched?

The short answer is “it depends.” Certain sectors in the equity and investment-grade debt markets are priced for a strong recovery. This is evident in the above-average sector-level forward price/earnings and price/sales ratios, tight credit spreads in corporate bonds, and other valuation indicators. Other sectors have not participated in recent market gains but seem to offer better forward-looking value opportunities. Additionally, some sectors have historically benefited from an uptick in inflation while others have underperformed in inflationary environments. In this type of market environment, one typically sees substantial sector and asset class rotations as investors shift allocation tilts.

Active managers nimble enough to adapt to this new regime should be able to generate responsible returns. Hedge fund managers able to shift to the cheaper, cyclically focused, inflation-friendly companies while hedging out market risks using short positions in over-owned and overvalued securities should benefit, in our view.

Are bond yields too low given the prospects for strong gross domestic product (GDP) growth, potential shifts in monetary policy, or a possible overshoot of inflation targets?

Consensus among strategists, economists, and fund managers seems to be building around the idea that real and nominal yields have seen their cyclical lows. The thinking is that the economic slowdown caused by the pandemic was efficiently priced into lower global sovereign bond yields during 2020 but that governmental stimulus programs will lead to a robust economic recovery and higher real yields. If real yields move higher at the same time as inflation normalizes, this would suggest nominal yields are still too low (and yield curves too flat). Some macro hedge fund managers expect this to play out and have benefited from the recent decline in government bond prices. Furthermore, some long/short credit managers are seeing a relative value opportunity that should persist as rates move higher. Those corporate credits with a strong balance sheet should prosper while those with less than stellar credit fundamentals may lag in the recovery or decline in value.

Which equity and corporate fixed income sectors would benefit most from a global economic reopening? Which areas might lag?

If the market is in a “rotation cycle,” long positions that may offer return potential include stocks or bonds in the materials, industrials, financials, and energy sectors. While individual corporate fundamentals must be analyzed within these broader groups, many fund managers and analysts find the landscape ripe for ideas. On the flipside, individual equity or debt investments in the technology, health care, and consumer staples sectors could be fairly valued given the recent popularity of the work from-home theme.

Hedge fund managers able to go long and short equities or corporate debt feel the gap in sector relative values has begun to close. Being long the securities that have lagged broader markets over the past few years while hedging out market risks using securities that are relatively overvalued should be a source of low-volatility returns.

The answers to these and other questions will be crucial for investors and fund managers looking to maintain recent performance gains and capture responsible returns going forward. From our vantage point, we sense the equity, bond, currency, and commodity markets began a regime shift during the fourth quarter of 2020. Many of the geographical, asset class, and sector rotations associated with this regime shift can be beneficial to actively managed portfolios.

Second-Quarter 2021 Outlook: Strategy Highlights

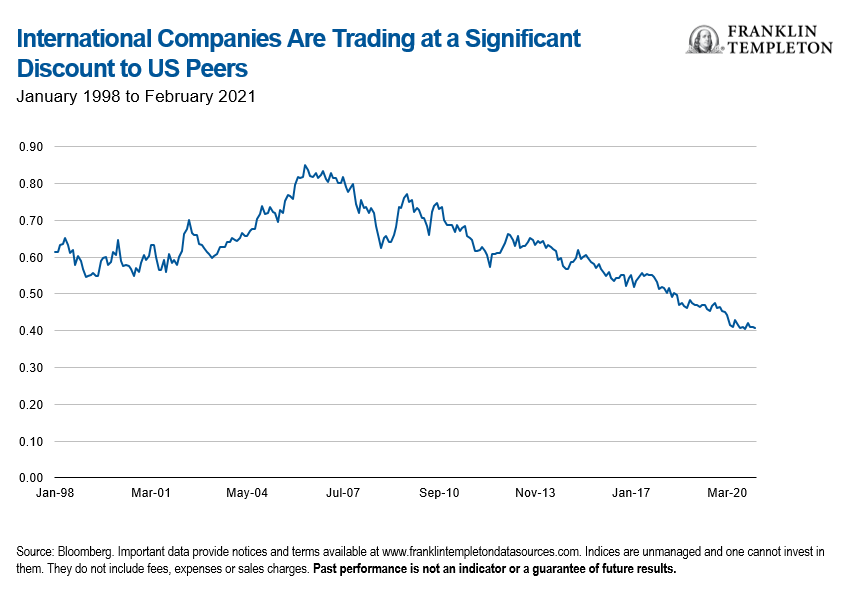

Long/Short Equity—International

As the end of the COVID-19 pandemic appears to be in sight, investors have been bullish on the reopening of global economies. We believe that international equity markets (MSCI EAFE Index) will benefit more than the US market (MSCI US Index) due to their larger exposure to overlooked cyclical companies. International cyclical equities are poised to benefit from secular trends in addition to recently rising US interest rates (which have hurt technology and other high-growth sectors that have outperformed over the last several years) along with the possibility of higher US corporate taxes. Even a potential third-wave lockdown and bumpy vaccine rollouts, as demonstrated by various countries’ responses to AstraZeneca’s vaccine, can lead to asymmetric responses to the reopening trade, enabling dispersion and alpha generation across the different geographies and sectors.

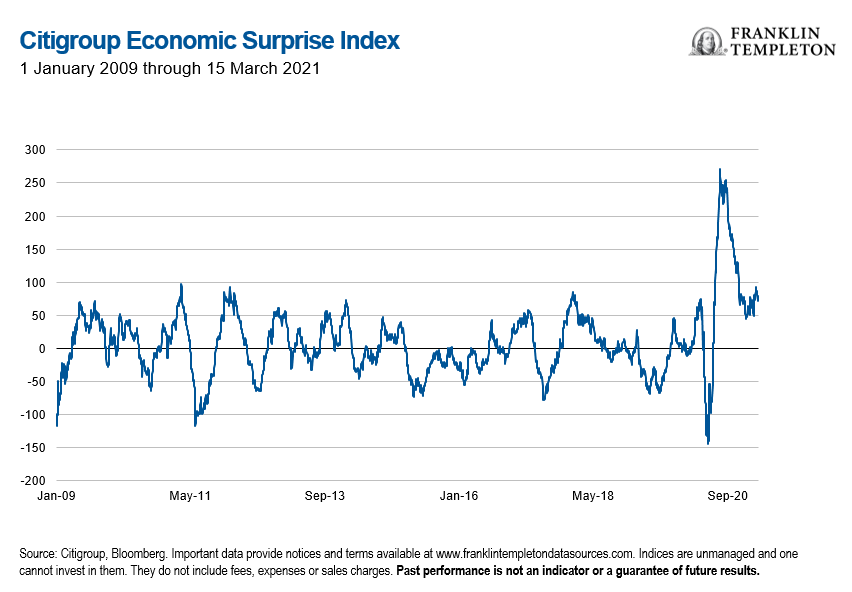

Global Macro

As the economic recovery from last year’s doldrums has continued, macro trends have started to take hold. The Citigroup Economic Surprise Index, which tracks economic data relative to forecasts, has recently indicated strong macro outperformance compared to the expectations of many economists. An environment in which such trends persist may support managers and strategies that are principally focused on such factors.

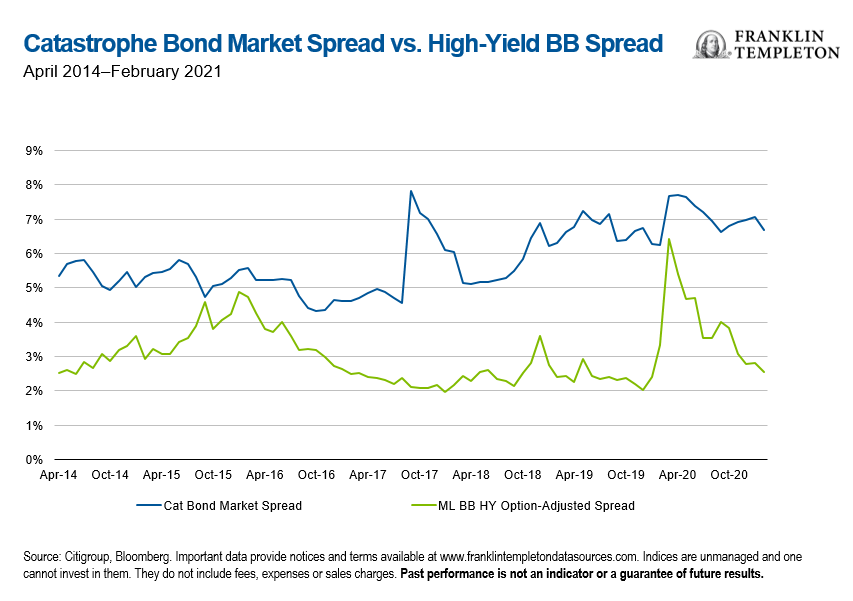

Insurance-Linked Securities

Although cat bond spreads have slightly tightened in the first quarter following inflows, they remain attractively priced versus corporate high yield (HY). The large US winter storm that primarily impacted Texas is likely to be a record event for the industry. This may support higher June 1 reinsurance pricing following higher January 1 pricing. In addition, a healthy spring cat bond pipeline is expected to provide additional trading opportunities in the second quarter.

What Are the Risks?

All investments involve risks, including possible loss or principal. Investments in alternative investment strategies and hedge funds (collectively, “alternative investments”) are complex and speculative investments, entail significant risk and should not be considered a complete investment program. Financial derivative instruments are often used in alternative investment strategies and involve costs and can create economic leverage in the fund’s portfolio which may result in significant volatility and cause the fund to participate in losses (as well as gains) in an amount that significantly exceeds the fund’s initial investment. Depending on the product invested in, an investment in alternative investments may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. There can be no assurance that the investment strategies employed by K2 or the managers of the investment entities selected by K2 will be successful.

The identification of attractive investment opportunities is difficult and involves a significant degree of uncertainty. Returns generated from alternative investments may not adequately compensate investors for the business and financial risks assumed. An investment in alternative investments is subject to those market risks common to entities investing in all types of securities, including market volatility.

Also, certain trading techniques employed by alternative investments, such as leverage and hedging, may increase the adverse impact to which an investment portfolio may be subject.

Depending on the structure of the product invested, alternative investments may not be required to provide investors with periodic pricing or valuation and there may be a lack of transparency as to the underlying assets. Investing in alternative investments may also involve tax consequences and a prospective investor should consult with a tax advisor before investing. In addition to direct asset-based fees and expenses, certain alternative investments such as funds of hedge funds incur additional indirect fees, expenses and asset-based compensation of investment funds in which these alternative investments invest.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of the date of publication and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

The information in this document is provided by K2 Advisors. K2 Advisors is a wholly owned subsidiary of K2 Advisors Holdings, LLC, which is a majority-owned subsidiary of Franklin Templeton Institutional, LLC, which, in turn, is a wholly owned subsidiary of Franklin Resources, Inc. (NYSE: BEN). K2 operates as an investment group of Franklin Templeton Alternative Strategies, a division of Franklin Resources, Inc., a global investment management organization operating as Franklin Templeton.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All