Economic Commentary: Digital Currencies, Mortgage Forbearance, Pets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIN THIS ISSUE:

- Will Central Banks Take Currencies Digital?

- Mortgage Forbearance One Year Later

- Pets During the Pandemic

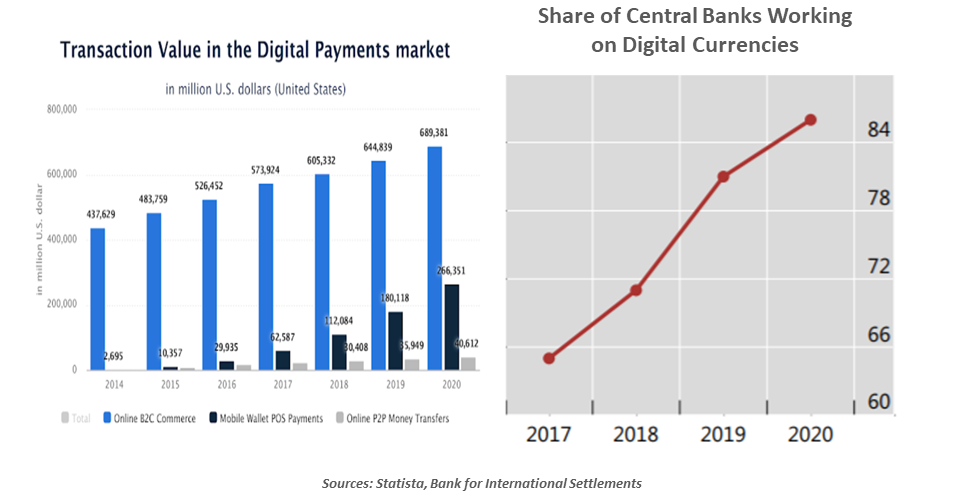

I have exactly eight dollars in my wallet at the moment. It’s the same eight dollars that were there fifteen months ago, long before the pandemic began. There just isn’t much need for currency anymore, with the expansion of cashless transacting, e-commerce and electronic wallets.

That’s one reason why I have been confused by the proliferation of cryptocurrencies. Digital transactions in traditional currencies have already taken over; why do we need new, volatile products to push us further in this direction? Many consider bitcoin more an object of speculation than an innovation in payments.

I have also been struggling to understand why the world’s central banks might want to bring forth their own digital currencies, which seem (at least on the surface) to be solutions to problems that don’t exist. But after digging a little more deeply into the topic, I found these efforts to have substantial merit and momentum.

The transformation of payments during recent decades has been remarkable. Cash and checks were once the dominant mediums of exchange, but credit and debit cards began taking over about 35 years ago. Initially only swiped at the point of sale, “cards” became more of a virtual concept with the advent of e-commerce. This facility has been taken to a new level by cashless payment platforms.

As sophisticated as the process appears on the surface, it remains hindered by a series of frictions. Payments must pass from one account to another, which are most often located at different institutions. Each side must confirm the amount and adjust balances accordingly. The banks and networks that facilitate the transaction add charges that can reach 4% of the tab. Transactions pass through a number of computer and payments systems during processing, all of which are vulnerable to service interruptions and cyberattacks.

A digital currency has the potential to overcome many of these frictions and frailties. Because it is based on a central electronic ledger that is shared by all institutions, payments could pass directly, quickly and cheaply from party to party, without intermediate steps. The role of clearing houses and processing companies would be deeply reduced, saving steps and costs. While no platform is impervious to cyberattacks, defensive efforts could be focused on protecting a single perimeter, instead of many.

Several technology companies have developed their own digital currencies. The most prominent example has been Facebook’s libra (now called Diem), whose value was going to be pegged to a basket of underlying currencies (making it a “stablecoin”). Facebook users would have digital “wallets” that could receive libra payments; the digital wallets would be linked to an account at a bank.

|

Digital currencies promise to make transacting faster and cheaper. |

But if a private company were to fail, the digital wallets it houses could become difficult to access and owners could be exposed to a loss of value. And there is no rule or mechanism that governs the supply of private digital currencies, which could leave them vulnerable to a loss of value if the currency became oversupplied.

Major central banks would not face either of these risks. Their solvency is not in question, and they calibrate the supply of money to economic needs. In this regard, they have tremendous natural advantages over private digital currencies and cryptocurrencies. A central bank digital currency (CBDC) would be exchangeable for physical currency one-for-one, eliminating uncertainty about its role as a store of value.

Source: Bloomberg

Sponsoring a digital currency would also provide central banks with an immense amount of data that could provide real-time insights into economic and financial trends. Fraudulent or criminal activity would be easier to detect. And in some cases, a CBDC could allow central banks and governments to collaborate towards more efficient collection of taxes and reduce the fraction of the economy that works “off the books.”

There are other motivations for developing a CBDC. China is getting closer to introducing a digital RMB, which would facilitate transactions on a digital ledger controlled by Beijing. This could encourage more global transacting in the RMB, raising its status. And it could potentially be an avenue through which Chinese individuals and entities could work around international sanctions that restrict access to traditional global payments systems.

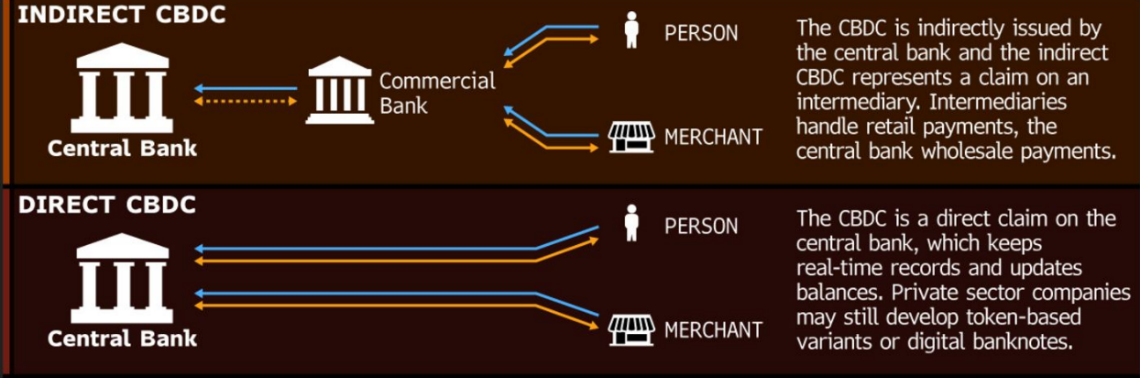

In a recent survey, the Bank for International Settlements reported that central banks around the world are doing research into both “direct” systems that allow individuals to have their own digital currency accounts, and “indirect” systems that only give access to more traditional intermediaries. The former has the potential advantage of improving the availability of banking services and speeding the distribution of stimulus funds, but it would place the central bank in direct competition with private banks for deposits. And absent strong protections on the use of CBDC data by governments, privacy could become a concern.

|

Central banks have immense natural advantages in offering a digital currency. |

Whichever path they choose, central banks will have to secure the legal authority to initiate a digital currency. Fewer than one-fifth of central banks currently have this ability, and the debate over granting additional license will certainly be an active one. (A proposal to allow the U.S. Federal Reserve to introduce a digital dollar was recently introduced in the U.S. Congress.) Banking interests will almost certainly push back against the direct model, and there will be other constituencies that object to either form on privacy grounds.

But if central banks don’t get into the game, the rise of private providers could create a risk to financial stability. And those private providers could harvest and utilize data in ways that make many people uncomfortable.

My research has led me to the conclusion that central bank digital currencies are coming. Now, if I could just find something that costs less than eight dollars, I’ll take my wallet down to zero.

Help for Homeowners

March 2020 was a month like no other. As one-year retrospectives reflected on the public health and financial challenges faced back then, one other historic event happened last March: The passage of the CARES Act. The package was noteworthy for its size and the speed at which it moved. However, it assumed only a brief disruption, with most supports expiring in summer 2020.

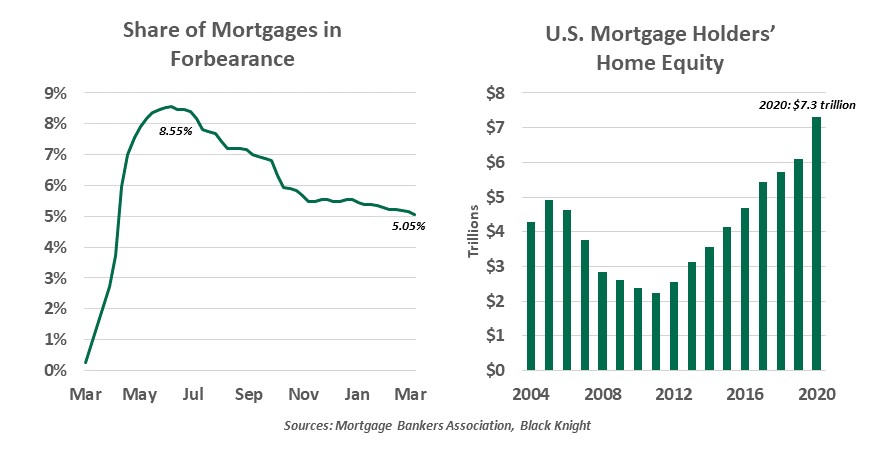

One CARES Act provision stood out for its length: A 12-month moratorium on mortgage foreclosures for loans insured by government-sponsored entities (GSEs), which represent the majority of the market. A year later, this program has broadly been a success.

Under the Act, mortgage borrowers could request forbearance without questions or conditions. At the program’s peak in June 2020, 8.6% of mortgages were in forbearance, a share that could have gone much higher. Many consumers prefer to stay on top of their payments, even when given an option to not make them.

As the program progressed, some other surprises emerged. The Mortgage Bankers Association found that 27% of borrowers who requested forbearance never actually stopped making payments. Another 15% repaid their missed payments in full immediately upon resuming monthly payments. These outcomes show a large number of borrowers who used this program did not need forbearance, but took advantage of it to protect their liquidity during an uncertain interval.

The CARES Act was not prescriptive about how to bring consumers out of forbearance, leaving lenders to sort out that important detail. Most servicers (who collect the payments from borrowers and pay the mortgage bondholders) have accrued missed payments into a new second loan, charging no interest, that will come due at the end of the mortgage term. The debt is still owed, but it is not an immediate obligation. Lenders can also renegotiate with borrowers to place them into a new loan with an extended term, but this more complicated than simply adding a second loan to an existing relationship.

Low rates led to a boom in refinancing last year, and that may have helped consumers decide to stay current on their loans. Borrowers need to be in good standing to refinance at the best rates, serving as a reward for avoiding forbearance.

|

The foreclosure crisis will not be repeated. |

As forbearance was taking off, mortgage servicers looked to be in a precarious position. Their income from borrowers could be stalled, but they were still expected to forward payments to bondholders. However, the GSEs agreed to step into their role as insurers after the fourth missed payment and took responsibility for subsequent payments to investors.

Despite the encouraging news, there remain over two million mortgages still in forbearance. The foreclosure moratorium has been continued through June and payment forbearance as far as September 2021. At that time, servicers may require borrowers to resume payments, sell their homes, or face foreclosure. Given the smooth transitions of borrowers thus far, it is likely that most can return to good standing if their missed payments are deferred to the end of the loan.

For a borrower in forbearance who suffered a permanent income impairment, a forced sale may not be the worst outcome. House prices appreciated in 2020, and higher mortgage lending standards have improved the quality of loans on the books today. This will not be a repeat of the foreclosure crisis: Only 1.5% of mortgagees are estimated to be underwater today, compared to a third or more in the aftermath of the financial crisis. Foreclosure is a slow, expensive process for lenders and a traumatic life event for homeowners; avoiding it is best for all involved.

Measures like the CARES Act helped prevent a public health crisis from spiraling into a complete economic meltdown. Its call for mortgage forbearance kept short-term problems with financial health from spiraling into a systemic housing crisis. Some of the painful lessons learned in 2008 have proved very helpful this time around.

Reigning Cats and Dogs

Apart from our keenness in economics, members of our economic team now have one more thing in common. All three of our families adopted dogs in 2020. We’re not the only ones: the last year has seen a staggering rise in pet ownership in many parts of the world. Roughly 3.2 million British and 11.4 million American households have acquired pets since the onset of the pandemic.

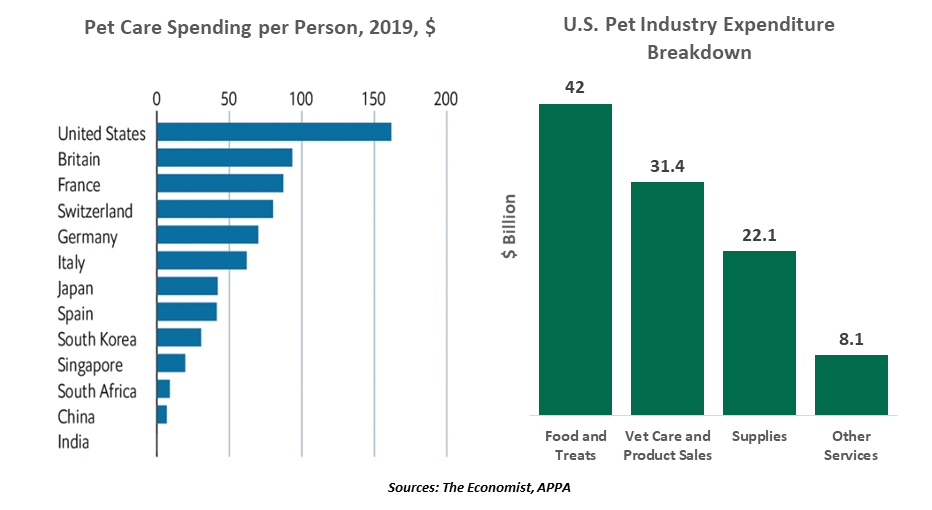

Pets are thought of as family, and caring for their needs has become a priority. As a result, pet care has been a thriving business. Even before the pandemic, spending on our animals had been growing at a dramatic rate, with a number of countries witnessing higher-than-ever pet ownership. According to a 2019 Euromonitor International report, the pet care market grew by over 66% in the last decade, compared to a 43% expansion of the global economy. On a per-person basis, Americans, followed by the British, splurge the most on their pets, averaging more than $150 and $90 per person in 2019 respectively. (Costs can vary by type and size of the pet.) India’s estimated $430 million pet care market is one of the fastest growing in the world.

|

The pet industry is thriving during the pandemic. |

The pandemic has provided further impetus to the industry amid rising ownership and willingness to splurge on care products and services. Brexit and the boost to the pet population are causing a national shortage of pet food in the U.K. The pet care and pet food sectors are attracting interest from investors. The price of the ProShares Pet Care ETF has almost doubled in the past year. The global pet care industry is expected to grow at a 6.1% average annual rate from 2021 to 2027.

I don’t need to rely on statistics to see how pet ownership and the pet industry are booming. During my dog’s daily walks and occasional grooming sessions at the local puppy salon, we frequently find old friends with new pets. Having a pet has been a great diversion during the pandemic—and, as the three of us can attest, the money we spend on caring for them has added momentum to the economic recovery.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All