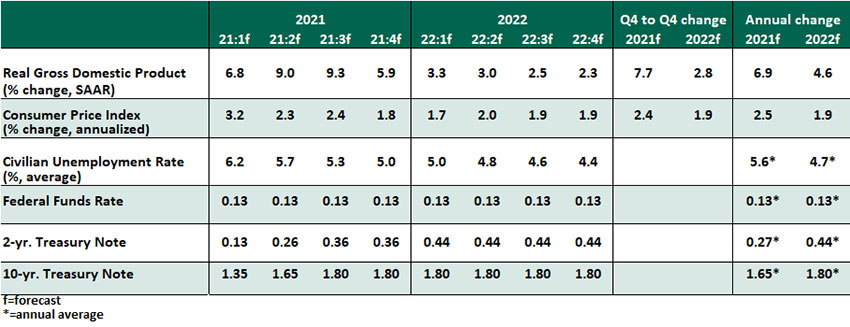

A year ago, the U.S. registered its deepest economic contraction since the Second World War. One year later, the economy is poised to post its strongest year of growth in almost four decades.

Economic activity is gaining traction, thanks to expanding vaccine distribution, lowered public health restrictions and substantial fiscal support. For the first time since the outbreak, the economic risks for the U.S. are tilted to the upside. Inflation will return, but won’t run out of control for reasons highlighted here.

The outlook is generally brightening, but uncertainty around the efficacy of current vaccines against mutated versions of the virus, which would cause a return of lockdowns, remains a key risk.

Influences on the Forecast

- The pace of COVID-19 vaccine administration in the U.S. continues to improve. The country is now among the world’s COVID-19 vaccine leaders as nearly one-third of Americans have received at least one dose. At the current pace of about three million shots per day, the U.S. can continue its broad-based reopening, but business and leisure travel will take longer to recover amid lingering virus concerns.

- The labor market has renewed its recovery, as reflected in the strong March employment report. Hiring increased to 916,000 jobs last month, the most since August. The unemployment rate declined by two-tenths to 6.0%. However, the recovery is far from complete, with total employment still 8.4 million below the pre-COVID level. We expect the hiring surge to continue for the next several months.

- Households are the key driver of recovery. The recently passed American Rescue Plan (ARP) will add to already-elevated excess savings, which should fuel consumption during the balance of the year. The ARP will not only provide support to households through checks, unemployment insurance and new tax benefits, but will also deliver assistance to businesses and state and local governments.

- Even before the potential impact of the ARP could be fully digested, President Biden’s focus shifted to the “Build Back Better” package. The plan is split into two separate proposals: the “American Jobs Plan” seeks to spend over $2.3 trillion on infrastructure, to be financed by higher corporate taxes. A second proposal, still forthcoming, will focus on child and healthcare spending. Though we expect another $1.5 trillion in infrastructure spending when enacted, it won’t materially alter our outlook. Unlike the ARP, spending under these proposals will likely be spread over several years, leading to gradual and lagged spillover benefits, potentially offset by tax increases.

- Base effects, fiscally stimulated growth and supply chain disruptions could pressure the price level in the coming months, but won’t be persistent. Inflation is set to exceed the central bank target range this summer before cooling off.

- The housing sector gained during the pandemic, and its momentum continues. Strong home sales coupled with tighter inventories pushed annual house price growth to multi-year highs. However, the sector is facing some uncertainty as Treasury rates have been on the rise, driving an increase in mortgage rates. In our view, rising rates are not a threat to the housing market yet, as yields have only climbed back to their pre-pandemic levels.

- The Federal Open Market Committee reaffirmed its dovish stance, despite higher projections for economic growth. The Fed also ruled out the need to contain long-term rates, noting very easy financial conditions overall. Tapering of asset purchases and interest rate increases are a long way off.