Key Points:

Powerful restart

We stick to our pro-risk stance and tweak our tactical views as the U.S. leads a powerful global economic restart and our new nominal theme plays out.

Market backdrop

Stocks were little changed on the week as markets digested strong first quarter earnings reports and bond yields eased.

Policy focus

The Federal Reserve policy meeting will be in focus as markets look ahead to a potential tapering of its bond purchases to be signaled as early as June.

A powerful economic restart is underway in the U.S. – with Europe and emerging markets (EMs) set to follow. At the same time our new nominal theme has been playing out, with a hefty jump in inflation expectations but a more muted rise in nominal yields. Against this backdrop, we reiterate our pro-risk stance and refine our tactical views in response to adjustments in market pricing and valuations.

Chart of the week

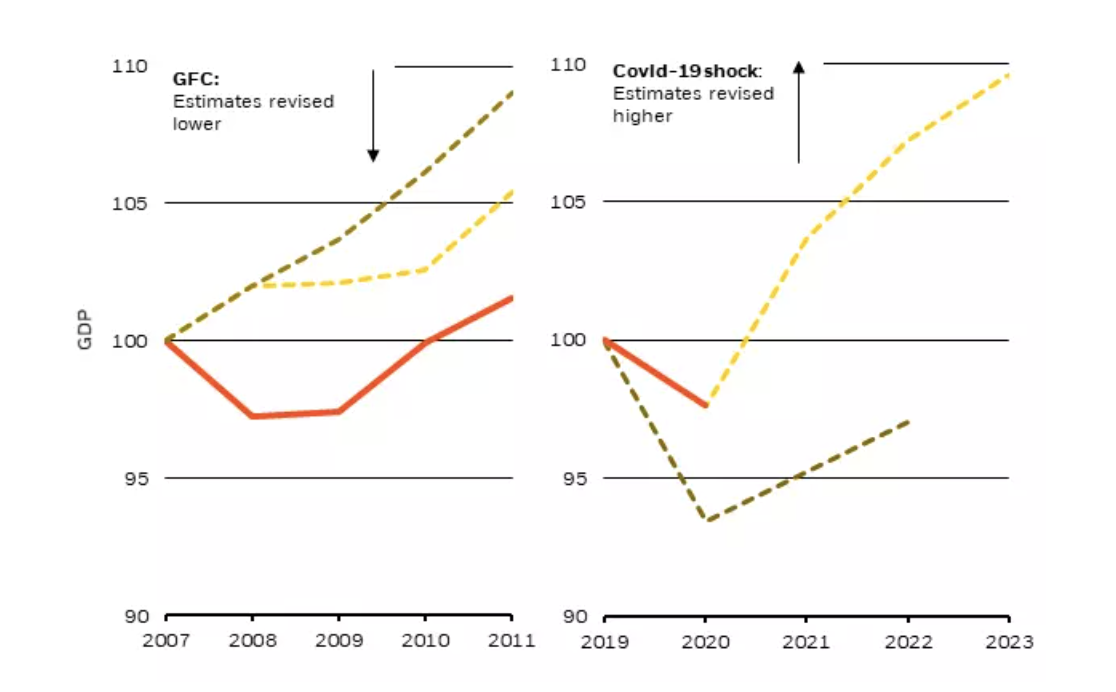

U.S. GDP estimates, global financial crisis and Covid-19 shock

We are at an uncertain juncture in markets. Investors are grappling with how to interpret unusual growth dynamics and new central bank frameworks. On the first, U.S. activity looks set to restart strongly this year, powered by pent-up demand across income cohorts and sky-high excess savings. Growth forecasts have been catching up, as the chart above shows, but the magnitude of the restart may still be underappreciated. This is in stark contrast to the repeat growth disappointments seen after the global financial crisis – and reflects the different nature of this shock. We see it as more akin to a natural disaster followed by a rapid “restart” – rather than a traditional business cycle recession followed by a “recovery.” This is why a year ago we warned against extrapolating too much from the steep decline in activity. Now the same is true – but in reverse. U.S. growth will likely peak over the summer but the eye-popping data will be transient: the more activity is restarted now, the less there will be to restart later. We see the rest of the world following the U.S. and reopening as vaccine rollouts pick up pace.

The second dynamic investors are grappling with is new central bank frameworks. Our new nominal theme helps us navigate this environment. The Federal Reserve is building credibility in its new framework and has set a high bar to change its easy policy stance, even in face of higher realized inflation. This has yet to be fully digested by markets, in our view. We see markets still underestimating the potential for the Fed to achieve above-target inflation in the medium term as it looks to make up for persistent undershoots in the past. This is why we think the direction of travel for yields is higher. But we believe the overall adjustment will be much more muted than one would have expected in the past based on growth dynamics – and much adjustment has already taken place.

General disclosure: This material is intended for information purposes only, and does not constitute investment advice, a recommendation or an offer or solicitation to purchase or sell any securities to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The opinions expressed are as of April 26, 2021, and are subject to change without notice. Reliance upon information in this material is at the sole discretion of the reader. Investing involves risks. Asset allocation and diversification does not guarantee investment returns and does not eliminate the risk of loss.

In the U.S. and Canada, this material is intended for public distribution. In EMEA Until 31 December 2020, issued by BlackRock Investment Management (UK) Limited, authorised and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL. Tel: + 44 (0)20 7743 3000. Registered in England and Wales No. 2020394, has issued this document for access by Professional Clients only and no other person should rely upon the information contained within it. For your protection telephone calls are usually recorded. Please refer to the Financial Conduct Authority website for a list of authorised activities conducted by BlackRock. From 31 December 2020, in the event the United Kingdom and the European Union do not enter into an arrangement which permits United Kingdom firms to offer and provide financial services into the European Union, the issuer of this material is:(i) BlackRock Investment Management (UK) Limited for all outside of the European Union; and(ii) BlackRock (Netherlands) B.V. for in the European Union, BlackRock (Netherlands) B.V. is authorised and regulated by the Netherlands Authority for the Financial Markets. Registered office Amstelplein 1, 1096 HA, Amsterdam, Tel: 020 – 549 5200, Tel: 31-20-549-5200. Trade Register No. 17068311 For your protection telephone calls are usually recorded. In Switzerland, this document is marketing material. This document shall be exclusively made available to, and directed at, qualified investors as defined in the Swiss Collective Investment Schemes Act of 23 June 2006, as amended. For investors in Israel: BlackRock Investment Management (UK) Limited is not licensed under Israel’s Regulation of Investment Advice, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”), nor does it carry insurance thereunder. In South Africa, please be advised that BlackRock Investment Management (UK) Limited is an authorized financial services provider with the South African Financial Services Board, FSP No. 43288. In the DIFC this material can be distributed in and from the Dubai International Financial Centre (DIFC) by BlackRock Advisors (UK) Limited — Dubai Branch which is regulated by the Dubai Financial Services Authority (DFSA). This material is only directed at 'Professional Clients’ and no other person should rely upon the information contained within it. In the Kingdom of Saudi Arabia this information is only directed to Exempt Persons, Authorized Persons or Investment Institutions, as defined in the relevant implementing regulations issued by the Capital Markets Authority (CMA). In the United Arab Emirates this material is only intended for -natural Qualified Investor as defined by the Securities and Commodities Authority (SCA) Chairman Decision No. 3/R.M. of 2017 concerning Promoting and Introducing Regulations. Neither the DFSA or any other authority or regulator located in the GCC or MENA region has approved this information. In the State of Kuwait, those who meet the description of a Professional Client as defined under the Kuwait Capital Markets Law and its Executive Bylaws. In the Sultanate of Oman, to sophisticated institutions who have experience in investing in local and international securities, are financially solvent and have knowledge of the risks associated with investing in securities. In Qatar, for distribution with pre-selected institutional investors or high net worth investors. In the Kingdom of Bahrain, to Central Bank of Bahrain (CBB) Category 1 or Category 2 licensed investment firms, CBB licensed banks or those who would meet the description of an Expert Investor or Accredited Investors as defined in the CBB Rulebook. The information contained in this document, does not constitute and should not be construed as an offer of, invitation, inducement or proposal to make an offer for, recommendation to apply for or an opinion or guidance on a financial product, service and/or strategy. In Singapore, this is issued by BlackRock (Singapore) Limited (Co. registration no. 200010143N). This advertisement or publication has not been reviewed by the Monetary Authority of Singapore. In Hong Kong, this material is issued by BlackRock Asset Management North Asia Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong. In South Korea, this material is for distribution to the Qualified Professional Investors (as defined in the Financial Investment Services and Capital Market Act and its sub-regulations). In Taiwan, independently operated by BlackRock Investment Management (Taiwan) Limited. Address: 28F., No. 100, Songren Rd., Xinyi Dist., Taipei City 110, Taiwan. Tel: (02)23261600. In Japan, this is issued by BlackRock Japan. Co., Ltd. (Financial Instruments Business Operator: The Kanto Regional Financial Bureau. License No375, Association Memberships: Japan Investment Advisers Association, the Investment Trusts Association, Japan, Japan Securities Dealers Association, Type II Financial Instruments Firms Association.) For Professional Investors only (Professional Investor is defined in Financial Instruments and Exchange Act). In Australia, issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975 AFSL 230 523 (BIMAL). The material provides general information only and does not take into account your individual objectives, financial situation, needs or circumstances. In China, this material may not be distributed to individuals resident in the People’s Republic of China (“PRC”, for such purposes, excluding Hong Kong, Macau and Taiwan) or entities registered in the PRC unless such parties have received all the required PRC government approvals to participate in any investment or receive any investment advisory or investment management services. For Other APAC Countries, this material is issued for Institutional Investors only (or professional/sophisticated /qualified investors, as such term may apply in local jurisdictions). In Latin America, for institutional investors and financial intermediaries only (not for public distribution). No securities regulator within Latin America has confirmed the accuracy of any information contained herein. The provision of investment management and investment advisory services is a regulated activity in Mexico thus is subject to strict rules. For more information on the Investment Advisory Services offered by BlackRock Mexico please refer to the Investment Services Guide available at www.blackrock.com/mx

Not FDIC Insured | May Lose Value | No Bank Guarantee

© 2021 BlackRock, Inc. All Rights Reserved. BLACKROCK, iSHARES and ALADDIN are trademarks of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.

BIIM0421U/M-1620917

As a result of these two key dynamics, we maintain our pro-risk tactical view. We remain overweight equities, neutral credit and underweight government bonds on a tactical basis. Yet we have tweaked some of our tactical views given significant moves in market pricing. For example, 10-year Treasury yields have more than tripled from last year’s lows around 0.5%. This leaves less room for further rises in yields on a tactical horizon, in our view. U.S. inflation expectations also have come a long way since we moved to an overweight in U.S. Treasury Protected Securities (TIPS) early last year. As a result, we are trimming our tactical underweight to U.S. Treasuries and closing our overweight in TIPS – even as we see room for yields to push higher and inflationary pressures to build further in the medium term. In a world starved for income, we have upgraded EM local currency debt on attractive valuations and the prospect of a stable dollar as the restart broadens, prefer high yield over investment grade credit and see opportunities in private markets. Within equities we express our pro-cyclical stance through overweights to EM and U.S. small caps as beneficiaries of the vaccine-led restart.

Bottom line: The broadening restart – coupled with our belief that this will not translate into significantly higher rates – underpins our pro-risk stance. Risks remain, however, on the tactical horizon. One is a market overreaction to exceptional growth data in the months ahead. We may see bouts of volatility as markets test the Fed’s resolve to stay “behind the curve” on inflation. Any temporary spikes in rates may challenge EM assets in particular, but we advocate staying invested and looking through any turbulence as our “new nominal” plays out. Want to know more? BII’s Global Outlook (GO) meeting on April 27 is a chance to hear from us directly and ask questions. Contact your BlackRock relationship manager for details.

Download the full commentary

Read our past weekly commentaries here.

© BlackRock

Read more commentaries by BlackRock