Economic Commentary: Biden Goes Big, U.S. Debt Ceiling, Scotland Elections

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIN THIS ISSUE:

- Will “Build Back Better” Bust the Budget?

- The U.S. Debt Ceiling Is Back in Play

- Scotland: Another Post-Brexit Headache

“Make no little plans. They have no magic to stir men’s blood.”

Residents of and visitors to Chicago likely know the work of the architect Daniel Burnham, even if they never learned his name. Aside from designing several landmark buildings, one of Burnham’s last works was the 1909 Plan of Chicago, his overarching view of how best to organize the fast-growing city. From individual structures to large-scale zoning, the 150-page illustrated volume lays out a well-considered vision. Following his own advice, he left behind no little plans.

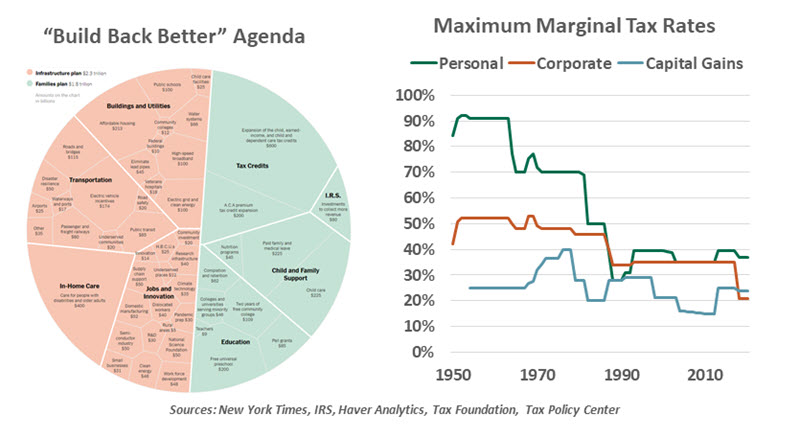

Members of the Biden administration appear to have taken Burnham’s guidance to heart. In two increments, they have laid out sprawling plans that could leave a lasting imprint on the scope of federal programs and the national economy.

We have previously discussed the $2.7 trillion American Jobs Plan (AJP), which proposes funding for conventional infrastructure, schools, hospitals and elder care. The administration has since debuted the American Families Plan (AFP), which calls for more spending on early childhood and community college education, paid sick and family medical leave, and making temporary child tax credits permanent, estimated to cost another $1.8 trillion. The AJP would be paid with corporate tax increases and reforms, while the AFP includes income tax hikes on higher earners.

Many of these ideas are worthy of discussion. For example, starting education earlier in life has benefits to children, who gain a stronger foundation for learning, and their families, who are relieved of some of the burden of child care. The effort could be justified on that general basis. But the White House included some optimistic economics, claiming every dollar invested in early childhood education returns more than $7 in greater productivity, better health and lower crime. Even if true, those intangible future gains do not help with the high up-front costs borne by taxpayers, including larger schools and more teachers.

Estimating the total costs and benefits of these proposals requires myriad assumptions about the long-term effects of investment. Moody’s is bullish, forecasting the Biden agenda would lead to a 3.5% improvement in real gross domestic product (GDP) and 4.4 million additional jobs by 2030, with a slight long-run reduction in the budget deficit. The Penn Wharton Budget Model is much less supportive, finding the AFP would cost $700 billion more than the White House estimates. Penn Wharton’s forecast includes second-order effects like higher government debt crowding out private investment and more generous social policies reducing hours worked, leading to a loss of 0.4% of GDP and a 4.6% increase to government debt by 2050, relative to the baseline outlook.

“The long-term budget impact of the Biden platform is the subject of intense debate.”

Senate reconciliation is likely to set the clearest boundary of what is achievable. This procedure allows the Senate to pass a bill with limited debate and approval by a simple majority. Reconciliation bills must be related to taxation and mandatory spending. The revenue and spending provisions in the latest Biden proposals do bring these provisions into scope for a reconciliation bill, but they must be carefully constructed to stay within the procedural boundaries of the process. The disqualification of a proposed minimum wage hike from the American Rescue Plan earlier this year will give legislators pause about making the bills too ambitious in scope.

An attempt at bipartisan compromise is underway. The conventional infrastructure projects in the American Jobs Plan could find some Republican support. Some initial talks have begun between the two parties, but we do not hold out hope for a compromise. From the opposition party’s perspective, there is little to be gained from agreeing to one smaller bill, only for the Families Plan they dislike to be passed with reconciliation.

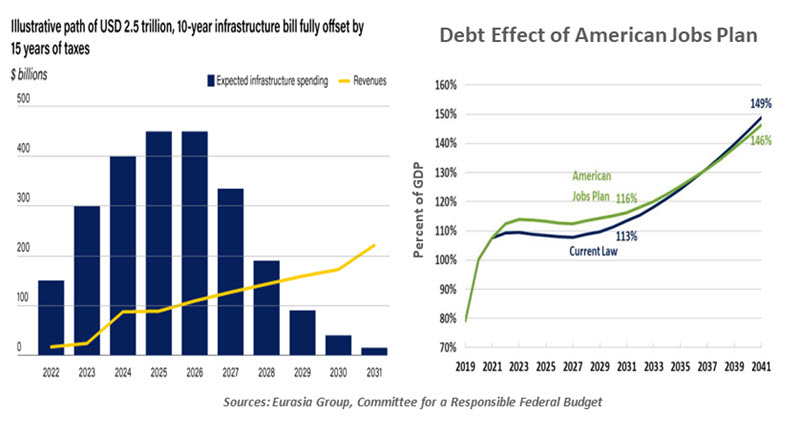

Though political and procedural challenges will arise, we do expect a slimmer set of policies will be ratified later this year. Some investment in conventional infrastructure is due. Gasoline shortages on the U.S. east coast and blackouts in Texas are just two recent examples of fragility. Investment in roads, bridges, electrical and broadband networks, vehicle electrification and other tangible infrastructure items are likely to be funded. We expect elements of both proposals will come together into one bill, along with the fiscal year 2022 budget and a debt ceiling increase in the fall.

These projects will lift the country’s rate of economic growth, but gradually. Large projects take years to plan and enact. In this important sense, the AJP and the AFP differ fundamentally from the pandemic relief programs.

President Biden insists the proposals will be paid for, and he has proposed tax increases to fund them. An increase to the corporate tax rate and the income taxes of the highest earners will be felt by the fewest voters. But with midterm elections next year and control of both houses of Congress in play, voting for a tax increase in the coming months might make campaigning more difficult.

“The Biden administration won’t get everything it is asking for, but parts of its proposals will pass.”

Many Plan of Chicago ideas never left the drawing board. Burnham proposed a grand civic center that is now the location of a highway interchange; many of the ring roads and tunnels in his maps were never seriously considered. However, the city benefitted from a vision that continues to guide its development more than 100 years later.

The Biden agenda will not be enacted in full, either. In the near term, it will bring about some needed infrastructure investment. In the long run, its vision for the economic future of the nation will certainly kindle active discussion. Whether the reader finds the ideas inspiring or wasteful, they have certainly stirred the blood.

Hitting the Ceiling

You might be forgiven for thinking that there are no bounds on the U.S. budget at the moment. Five pandemic relief bills with a combined price tag of almost $6 trillion have passed in the last 14 months. And as covered in this week’s lead article, another $4 trillion in long-term economic spending is being considered by the U.S. Congress.

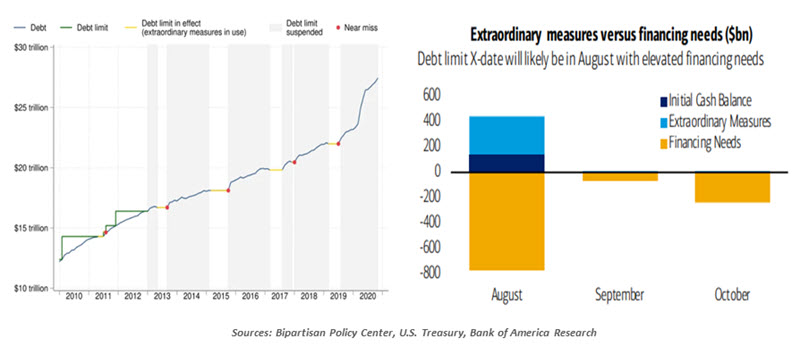

But, at least in theory, there is one barrier to the fiscal binge. The ceiling on Federal debt is scheduled to become binding again on July 31, ending a two-year suspension.

We’ve written about the debt ceiling many times. The United States is the only country which has this limitation; since the Congress weighs in directly on spending and taxation, the debt ceiling seems redundant and unnecessary. It has been the subject of unproductive political brinksmanship and the cause of government shutdowns (one of which prompted the rating agencies to downgrade Treasury debt). It hasn’t really been very binding; over its 104-year history, the ceiling has been extended almost 100 times, and it has been suspended six times in the last eight years.

But it does provide a platform for budget hawks to press their points. The desire to express objection is especially high this summer, as the most recent fiscal package passed on a party line vote. There is every chance the next round of government spending will also move without any support from across the aisle.

If the debt ceiling goes back into force this summer without modification, the government will be forced to use “extraordinary measures” to keep up operations. After those are exhausted (on the “X date”), the government will be living hand to mouth. The Treasury has been issuing extra debt at recent auctions to build up some reserves.

“The U.S. debt ceiling should be suspended... permanently.”

Under normal protocol, it would require 60 votes in the Senate to lift the debt ceiling. But both sides have used reconciliation procedures (which only require a simple majority) to their advantage during recent budget discussions; the 2017 tax cuts were passed in this manner. More than likely, leaders of the Senate will use reconciliation to prevent the debt ceiling from becoming a limitation to government operations.

The U.S. debt situation does require serious discussion. But the debt ceiling has not prompted that discussion in the past, and is unlikely to do so in the future. Best to take it out of the equation.

Separation Anxiety

There is a saying that goes: throwing yourself into the unknown opens doors to new opportunities. Perhaps this was the thought that motivated support for Brexit in 2016. Unfortunately, Brexit appears to have opened doors to more new challenges than new opportunities for the U.K.: Britain is facing trade frictions, uncertainty surrounding its financial sector, and the prospect of greatly reduced immigration. All will be costly to long-term economic output.

Uncertainty surrounding Scotland’s standing in the United Kingdom is a new but unsurprising addition to that list. The outcome of last week’s elections in Scotland has put the issue of an exit from the U.K. back on the political agenda. Though the market reaction to the election outcome has been muted, the stakes are high for both sides.

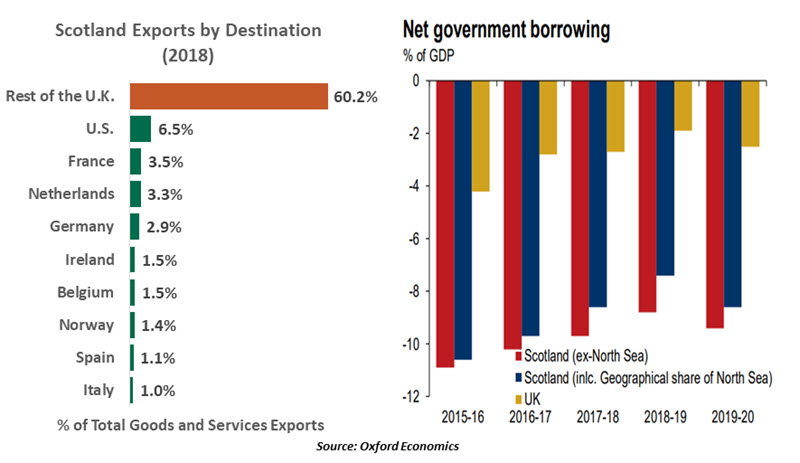

Scotland already enjoys a measure of self-rule. It has the power to formulate its own laws in several areas, including agriculture, education, health, housing, environment and justice. Scotland has a population of about 5.5 million, accounts for about 8% of the U.K.’s population, one-third of its land area and 7.5% of the British economy.

Despite this relatively modest economic footprint, Scotland’s departure would cause substantial disruption to commerce in Britain. Scotland is the third largest export market for the rest of the United Kingdom, after the European Union (EU) and the U.S. Brexit has already created complexities for businesses in the U.K., contributing to delays and damage to perishable items held at ports. These worries would increase significantly if Scotland became independent.

The Scots were not pleased with Brexit, and could seek to resume membership in the EU if they were on their own. Joining the EU might lower trade barriers with the Bloc, but will lead to more barriers with its largest trading partner. Almost two-thirds of Scotland’s total exports go to England, Wales and Northern Ireland.

According to the London School of Economics, Brexit already stands to reduce Scotland’s long-term income per capita by 2%. Trade barriers after exit from the United Kingdom would likely reduce income per capita by even more. Leaving the U.K. would be two to three times as damaging to Scotland’s economy than Brexit in the long run.

The extraction and distribution of oil and gas earnings from the North Sea will only complicate matters. According to research by the University of Aberdeen, Scottish waters contain 80% of North Sea output; London would certainly not allow Scotland to stake a full claim to the reserves and then export them south.

Scotland’s exit would add to the toll of Brexit in weakening Britain’s place in the world. While the U.K. now enjoys autonomy to enter into free trade agreements with other nations, a smaller U.K. will have less bargaining power in trade negotiations. Given the number of agreements that London has to strike in the post-Brexit world, it needs all the leverage that it can get.

Monetary and fiscal costs for an independent Scotland will be significant. While the position of the Scottish National Party is to retain the British Pound as a formal currency, the Scots would lose the backing of the Bank of England and will have to form a new central bank. To use the pound, Scotland would have to maintain large sterling reserves and would lack the ability to set an independent monetary policy.

“Economic costs will outweigh any benefits from Scottish independence.”

On the fiscal front, Scotland has been running high fiscal deficits, even before the pandemic. In 2019-20, it had a fiscal deficit 8.6% of gross domestic product (GDP) compared to Britain’s 2.6% of GDP. Scotland would have to take on a share of U.K. sovereign debt upon separation; if this were done on the basis of population, the Scottish government would be saddled with debt equal to about 115% of GDP.

Scottish independence isn’t a given yet, but the election outcome has pushed the likelihood of a second referendum higher. At the very least, the situation in the highlands will be a distraction for Westminster; at worst, an Act of Disunion could create serious economic upheaval.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All