Listen to the Global Economic Discussion

There is a sharp divergence in economic performance among nations at the moment. We are seeing a rebound in advanced economies and weakening activity in emerging markets, driven in both cases by the trajectory of COVID-19 infections.

Rising vaccinations, easing public health restrictions, pent-up demand and accumulated savings have set the stage for a strong second phase of recovery in advanced economies. The concern in these cases, especially in the U.S., is overheating and inflation. By contrast, elevated infections and renewed restrictions in major countries like India and Brazil show the pandemic is far from over.

The global recovery will not be complete without a sustained recovery in emerging markets, which contribute importantly to global demand and supply chains. New emerging COVID-19 variants remain a key risk for all nations.

Following is our outlook on how major economies are poised for this year of reopening.

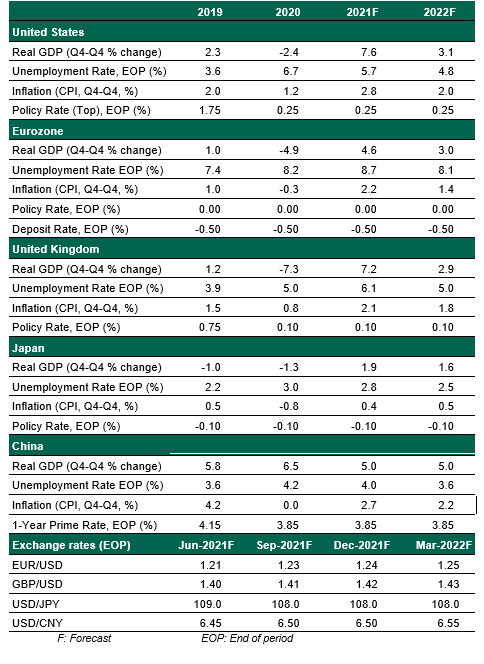

United States

- U.S. gross domestic product (GDP) grew at an annualized rate of 6.4% in the first quarter, held back only by slow exports and inventory depletion amid supply chain interruptions. Growth in the second quarter will be even stronger. Concerns are mounting about inflation in this context, especially after the consumer price index (CPI) grew by 4.2% year-over-year in April. We agree with the U.S. Federal Reserve that current inflationary forces will prove transient, as consumers return to former spending patterns and supply chain shortages are resolved.

- The rapid pace of reopening is leading to some surprises in economic data. Job creation in April was far below expectations, but falling unemployment claims and a high number of job openings suggest that is not the start of a trend. Retail sales growth was slow in April, but they increased from the record high level set in March. No decisions should be made on a single data print; economic momentum is still strongly supportive of growth.