Economic Commentary: China's Recovery, U.S. Trade Deficit, Household Well-Being

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIN THIS ISSUE:

- Is China’s Recovery Losing Steam?

- Record U.S. Trade Deficit

- Many U.S. Households Are Not At All Well

FIFO ─ first in, first out ─ is a term used in accounting for inventories. But it can also be used to describe China’s experience with COVID-19. China was “first in” to contagion and mass shutdowns, and was the “first out,” recovering from pandemic-induced disruptions to economic activity. As other countries struggled to contain the virus, China was the only major economy to have expanded in 2020.

China is now also the first major economy to unwind its pandemic-related stimulus measures, and headline figures show the power of its progress. China’s real gross domestic product (GDP) grew at a staggering year-over-year rate of 18.3% in the first quarter, its biggest increase since reporting began in 1992. That said, it is unlikely that China’s economy can keep up such lofty momentum.

China’s economic rebound has been aided by debt-fueled state investments in industries, along with a surge in exports. As COVID-19 led to plant closures in several parts of the world, Beijing’s factories saw a higher volume of overseas orders for goods ranging from protective kits to electronics for working from home.

As manufacturing in the rest of the world comes back online, China’s export growth will lose some steam. Chinese manufacturing activity is already taking a modest hit due to disruptions in supply chains, reflected in the softer Purchasing Managers’ Index for April. Semiconductor shortages, along with rising input costs, are weighing on China’s electronics and auto industries.

Momentum in the Chinese service sector is softening, indicating domestic demand remains a weak link in this recovery. Household spending in China has constantly fallen short of expectations and has lagged the overall recovery from the pandemic. Lingering concerns around public health and the health of the economy have kept Chinese consumers conservative, resulting in an increase in household savings. Retail sales growth in China decelerated notably in April, even after adjusting for the “base effects” that have made trend analysis so difficult during this pandemic interval.

This presents a challenge for Chinese policymakers, as relying on pro-growth industrial policies will delay the shift towards the consumption- and services-driven economy that Beijing has been seeking for some time. Turning away from reforms and returning to large-scale stimulus will likely reduce the risk of credit defaults, but will amplify long-term structural problems in the economy.

Letting the economy function without financial “steroids” will come with own set of challenges. Reduced policy support will weigh on infrastructure and the overheated property market, both key drivers of recovery. Bond defaults by Chinese corporations rose to a record $15.1 billion in the first quarter, with real estate developers alone accounting for over a quarter of that amount. If policy continues to tighten, that number is only going to rise.

Soft domestic demand and surging defaults will complicate Chinese policymaking.

Global investors are already concerned about the slow pace of debt restructuring, as only about one-fifth of Chinese corporations that defaulted on their U.S. dollar bonds since 2018 have completed the resolution process.

The Chinese labor market has been improving, with the headline unemployment rate dropping to 5.1% in April, its lowest level in a year. Unfortunately, this is not considered to be a precise indicator. The actual unemployment rate could well be higher than the official measure, which has been unusually steady for the past two decades. No other country has seen this kind of stability in its reported employment outcomes.

Demographics will also challenge China’s drive to transition from an investment-driven to a consumption-based economy. Not only is China’s population growth slowing, but it is also aging. The number of Chinese over the age of 65 years is expected to double from 200 million to 400 million by 2049. As a result, China’s labor force and the contribution of consumption to economic growth will shrink over time.

Trade frictions with major trading partners, particularly the U.S., are another pain point for Chinese policymakers. Beijing is seeking to reduce dependence on foreign technology amid tensions with the U.S., which will require substantial financial resources. China is committing to boost research and development spending by 7% annually to bring total spending to $580 billion by 2025. Chinese tech firms listed on the U.S. exchanges are facing regulatory threats.

|

The Chinese economy faces multiple challenges: some are immediate, others are longer-term. |

China is a significant source of global carbon emissions, so its plan to become carbon neutral by 2060 is a welcome announcement. But the country has yet to unveil its plan to meet its commitment to the Paris climate accord. Considering the economy’s dependence on coal and other energy intensive industries, transitioning to a new low-carbon model will be a daunting task for the government.

China might be winning the war against the pandemic, but it is fighting several domestic and international economic battles. The most important one among those is containing financial risks and leverage. Trade difficulties with a series of other nations (not just the U.S.) present external risks. Managing these delicate situations will be difficult.

Being the “first out” of the pandemic gives China valuable time to foster domestic reforms and address its internal imbalances. These efforts will be critical to China’s ambition to be first among the world’s economies.

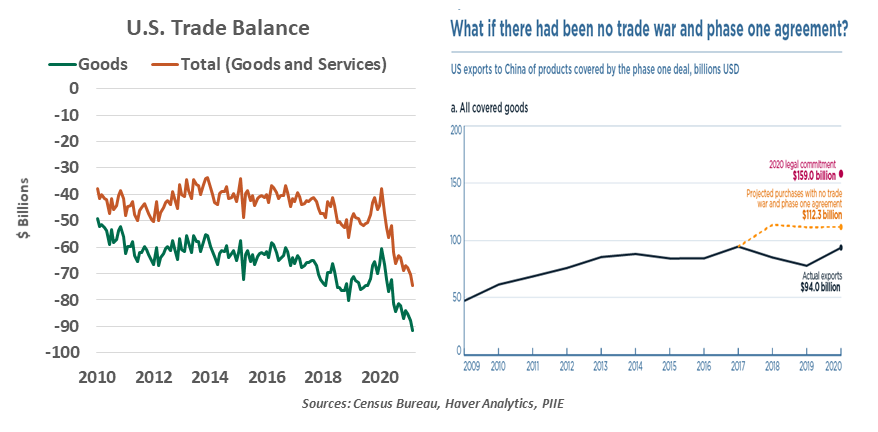

Hitting A New Low

Before the pandemic, the U.S. trade imbalance was a topic of considerable discussion. Many cited it as evidence that unfair global trading practices had caused the nation to lose productive capacity. Strong policies, including a series of new tariffs, were implemented in an effort to change course.

Today, the U.S. trade imbalance has soared to new records. This isn’t necessarily evidence of policy failure; as it has in other economic arenas, the pandemic has created transitory impacts that have pushed the deficit higher. But the fundamental issues underlying international imbalances remain unaddressed.

On the demand side of the deficit, the relative strength of U.S. consumers has been at play. Though the pandemic caused a rapid rise in unemployment, most U.S. consumers stayed employed over the course of the recession; those out of work have received a steady stream of benefits. Restrictions in the service sector led to more consumption of goods, which has drawn in more overseas products.

Rising oil prices are also contributing to the trade imbalance. As more people move about more often, they are using more oil for transportation. And because domestic oil production has not responded robustly to higher prices, more of this oil is imported. Many U.S. producers were stretched financially and did not survive the low oil prices of last year; with movement toward greener ways of doing things, the sector remains diminished from its pre-pandemic position.

On the supply side, the pandemic idled or slowed facilities in some parts of the U.S., increasing reliance on imported substitutes. Further, many markets for American exports endured deep recessions that curtailed orders for U.S. output.

As we have discussed, the cost of transporting imports is rising: cargo vessels are at capacity, containers are in short supply and ports are backed up. Last year, some merchants tried to avoid the rising costs of shipping by deferring orders and running down their inventories. That turned out to be a costly miscalculation: as inventories were depleted, restocking orders pushed up imports, and shipping prices are now even higher.

|

U.S. consumer spending has helped the world to recover, but has also led to record trade deficits. |

These dynamics were defining features of first-quarter U.S. gross domestic product (GDP) growth. The annualized growth rate of 6.4% was good, but its composition was uneven. Consumption grew by over 10%, but imports grew faster than exports, creating a drag on GDP. Though overall exports grew by an annualized 18.4%, imports grew at an even faster clip of 19.7%. And a substantial draw-down of inventories also weighed on growth. We believe the quest to rebuild inventories and get exporters back online will lead to high upcoming GDP prints, though imported inventories will keep the trade balance wide.

We expect the trade position to eventually moderate. U.S. consumers are expected to continue their binge for two or three more quarters, but their energy will eventually be eclipsed by consumers in countries in earlier stages of their reopening. U.S. manufacturers are operating at a high level, and poised to regain market share.

Over the longer term, improvement in the trade deficit will depend, in part, on negotiations with China. We are now in the second year of the two-year “Phase One” trade deal signed in 2020; China hasn’t come close to meeting the targets that were set out. The pandemic played a role, but wasn’t the only factor in the underage.

The U.S.’ structural trade deficit is unlikely to change, but the forces pushing it to new records are likely to subside. Returning to the old normal, however, is probably not enough.

Ailing

The Federal Reserve released an updated report on the economic well-being of U.S. households this week. The conclusion: many Americans are still under the weather.

The pandemic has created a dramatic divergence of fortunes. Those with college degrees and jobs that can be done remotely have gained, while workers with more modest levels of education and those from minority communities have had a much more difficult time. The opposing trajectories have led journalists to dub this a “K-shaped” recovery.

The Fed report provides stark evidence of the growing divide, and reminds us of just how many people are suffering from economic insecurity. Among the findings:

- Nearly a quarter of respondents were worse off financially than they were a year ago.

- More than one-fourth of adults were either unable to pay their monthly bills or were one $400 financial setback away from being unable to pay them in full.

|

Some families handled the pandemic well; others were manhandled by it. |

- Fourteen percent of adults reported being laid off in 2020. Fewer than one-quarter of them had been called back to their old jobs by the end of the year.

- Highly educated workers were much more successful at transitioning to work from home. Only 35% of college graduates reported doing no work from home, as opposed to 82% among those with a high school education or less.

- In another sign of the “she-cession,” 14% of women reported they were not working because of child care obligations, as opposed to only 5% of men.

- Seven percent of Americans changed who they lived with because of COVID-19, most often moving in with parents or grown children. These transitions were most likely born of economic necessity.

- Twelve percent of Americans under the age of 40 who had intended on enrolling in college cancelled those plans because of the pandemic. Overall, college enrollment dropped by 25%.

- More than 40% of Americans deferred medical treatment last year, due to some combination of COVID concerns and an inability to pay.

The Fed’s report card provides a stark illustration of the economic consequences of COVID-19. Conditions are improving, but many families have a long way to go before they can restore their well-being.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All