Economic Commentary: Demographics, Housing, Olympics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIN THIS ISSUE:

- The Pandemic Has Done Damage to Demographics

- U.S. Housing Boom

- Japan: Recovery and Olympics On The Line

A friend of mine was trying to find a silver lining amid the dark clouds that accumulated during the early days of the pandemic. Her son and his wife, both of whom had busy jobs, had been forced off the road and out of the office. The additional time together at home, she hoped, would result in a grandchild.

I was hoping she would be granted her wish, although for less sentimental reasons. Population growth in developed countries has slowed to a crawl over the past several years, and actually declined in China last year. A few more babies would help keep the labor force from shrinking in the decades ahead. But not even last year’s home confinement prompted more procreation.

Last year’s baby bust is just one aspect of the damage done to the world’s demographics during the last year. The pandemic has taken a significant toll on populations, costing lives and increasing disabilities. The scale and ability of the labor force are important foundations for long-term economic growth; both have been diminished by COVID-19. Once the current frenzy of economic reopening subsides, countries may face a more challenging long-term outlook.

Prior to the pandemic, we contended demographics were being overlooked as an economic issue. In our 2019 essay "Age Isn’t Just a Number," we highlighted the significant impact advancing seniority will have on growth, inflation and market performance. Fewer workers mean less output, more stress on retirement systems, and more risks to debt sustainability.

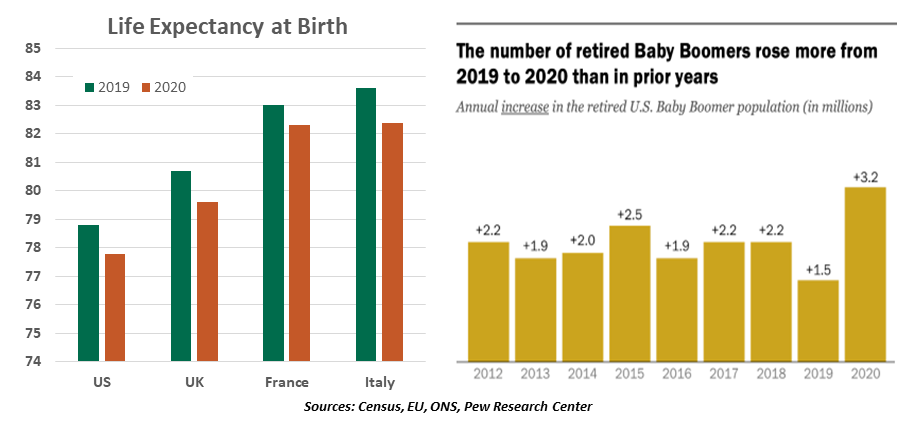

COVID-19 has made the situation much worse. To date, the disease has claimed 3.7 million lives around the world; as a result, life expectancy in Europe and the United States dropped by about a full year from 2019 to 2020. Studies have further shown that about 10% of COVID-19 survivors are dealing with long-term after-effects that can limit their ability to work.

Beyond these direct health consequences, the pandemic has had other deleterious impacts on the global labor force. We have seen a rise in early retirements; the Schwarz Center for Economic Policy Analysis estimates that 1.7 million Americans have chosen to end their careers before normal retirement age over the last 12 months. In the United Kingdom, Hargreaves Lansdown estimates that more than half of Britons who retired between March and September of 2020 did so because of the pandemic.

Some of these new retirees were undoubtedly motivated by the demonstration of life’s fragility, and wanted to enjoy the years ahead. Others anticipated an uphill climb to rejoin the labor market, and opted to take retirement benefits early when their unemployment insurance expired. Whatever the reason, early retirement curtails the economy’s access to hands and minds. As economic and public health conditions improve, some may get back to work, but others will not.

|

Demographics remains an economic topic that deserves more attention. |

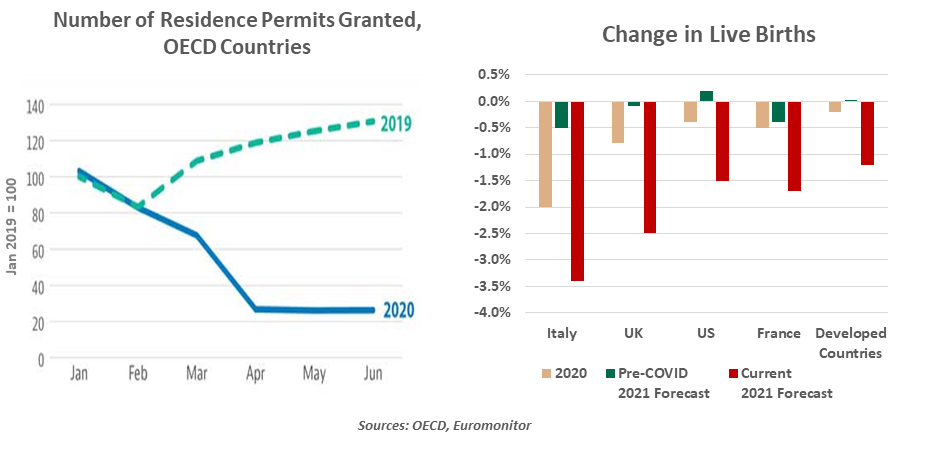

Border closings have been a common tactic to limit the importation of COVID-19, but they came with a cost. Immigration levels have plunged across the developed world, with immediate implications for seasonal hiring and educational institutions. Longer-term, the lull in new entrants will hinder labor force growth and innovation: immigrant communities are more likely to be granted patents and start new businesses, which contribute importantly to economic vitality.

While there has been some loosening of travel restrictions for tourists, allowances for new permanent residents remain limited. Global attitudes towards immigration had hardened in the decade after the global financial crisis, and policy makers may therefore take extra time in considering whether to re-open their doors to new permanent residents.

The anticipation of a baby boomlet as couples retreated to their homes made for a cute story, but it ran counter to the economic research into fertility. Firstly, the notion that events like blizzards and blackouts result in birth surges nine months later is not borne out by data. More importantly, recessions are bad for birth rates: when incomes diminish, parents can’t afford as many children.

Since the pandemic began, birth rates in France hit a 75-year low. Birth rates in Asia, already very low, fell even further. To arrest its own severe decline in fertility, China recently announced plans to allow couples to have a third child; but lingering economic uncertainty among the Chinese population may render the policy ineffective.

The rapid recovery from COVID-19 in many developed markets will, hopefully, limit long-term demographic costs. Health crises can suppress birth rates by diminishing the population of childbearing women and creating health-related uncertainty that causes potential parents to hesitate. While the loss of life over the last year has been tragic, it does not come close to the mortality seen during past global pandemics. And vaccination seems to have ameliorated contagion risks in many western countries.

|

Policies to sustain labor force growth will be essential in the years ahead. |

A strong economic recovery has the potential to restore incomes and wealth sooner than normal, which might also help reduce the disincentive to fertility. If demand continues to stress the capacity of the labor force, immigration may become more attractive to policy makers.

But even restoration of a pre-pandemic normal could leave many countries around the world with a long-term demographic deficit that will be difficult to close. Incentives for increasing family size are only a partial solution; child care programs have increased labor force participation in some countries, but you have to have children to make use of child care.

As of this writing, my friend is still hoping for news that a grandchild is on the way. Her son and his wife decided to adopt a pandemic puppy; my friend refers to it as her grand-dog-ter. But unless we can teach the canine to code, the addition to her family is not going to help the economy.

Roof Over Your Head

Buying a home is a major life milestone, and not a decision made lightly. Before considering a home purchase, the buyer must establish a steady source of income and accumulate savings. But even for those who have gotten their financial houses in order, high home prices in today’s market are proving to be a hindrance.

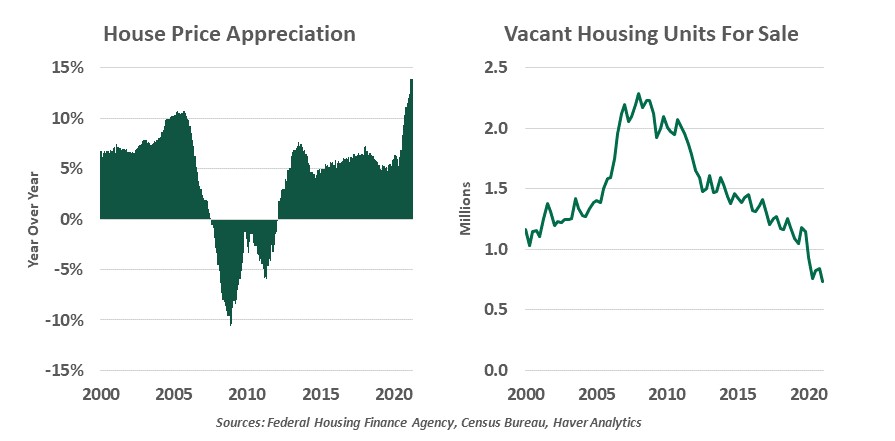

The most recent readings on house prices are eye-popping. Both the Federal Housing Finance Agency and S&P/Case-Shiller measures reflect gains of over 13% year-over-year in March. The National Association of Realtors (NAR) reported the rise of the median sales price of a single family home to $347,400 in April, more than 20% higher than last year. While home shoppers may find these conditions challenging, current homeowners are feeling wealthier, one of many drivers of buoyant spending this year.

Prices are rising in part because supply is scarce. The NAR estimates only 2-3 months of housing supply has been available throughout 2021, which is low by historical standards. Much of the depleted supply can be traced to substantial pull-forward of purchases caused by the pandemic. Working and schooling from home made many families desire more space, and homes were purchased in a hurry last year.

Unlike many consumer products, the supply of houses does not easily adjust to demand. New homes take months to build, and land in the most desirable areas is scarce. Supply chain challenges have reduced the availability of building materials and raised their prices. House shoppers are finding fewer choices, and listed properties are often gone in an instant; anecdotes of high bids made sight unseen are growing.

A hot interval for real estate does not mean the beginning of a new housing bubble. Mortgage underwriting standards have been stringent since the global financial crisis. Anyone who has purchased a home in the past decade has experienced the additional scrutiny of employment, financial records and property appraisals. Banks and mortgage agencies have not been reckless; for the most part, credit remains available only to well-qualified borrowers.

Higher prices are working to limit demand. Weekly reports of mortgage applications for purchases rose in 2020 but have been on a downward trend since the start of the year. As some buyers are priced out of the market, the purchase frenzy seen recently should ebb. This will also keep a floor under demand for rental housing.

Higher house prices have also made it easier for struggling borrowers to find an exit strategy from their mortgages. This is fortunate, as the foreclosure moratorium on agency loans is set to expire this month. Over two million borrowers remain in forbearance, down from a peak of 4.3 million in June 2020. Helping these borrowers return to repayment or move to an affordable home, rather than face foreclosure, will carry broad benefits.

|

Working from home has opened new geographic markets to home buyers. |

The real estate shopping dynamic has broadened, as well. As more jobs move to a fully remote arrangement, buyers may find they are no longer bound to live near their employers. Online portals allow buyers to browse nationwide. Residential construction advisory firm Zonda estimates that more than half of buyers in lower-cost markets are making long-distance relocations; these buyers would have represented less than 20% of activity in a typical year.

Trading out of a high-cost area leads to more than a lower mortgage payment: It can make the difference between a household needing two incomes or just one. While these transactions are pushing up prices in lower-cost regions, they may likewise temper gains in high-cost cities.

We view housing as one of many markets experiencing ripples from the pandemic that will linger for a year or more. High demand for housing is a favorable sign for the overall economy. Home buyers’ patience will be tested, but their perseverance will be rewarded.

Spoilsport

Some high-income countries, like Australia, were initially lauded for their efforts in containing the spread of COVID-19, but have more recently been the subject of some criticism. With vaccination, not quarantine, emerging as the most effective way of containing the pandemic, countries cannot afford to fall behind in inoculating their citizens. Unfortunately, Japan is far behind in the vaccination race, just as it is preparing to host some of the world’s biggest races.

Japan escaped the worst of the pandemic during its initial phase. The population was highly compliant with public health measures, and mask-wearing was already a common practice. Through the end of winter, the number of cases per capita in Japan was infinitesimal when compared to that of the U.S. and Europe.

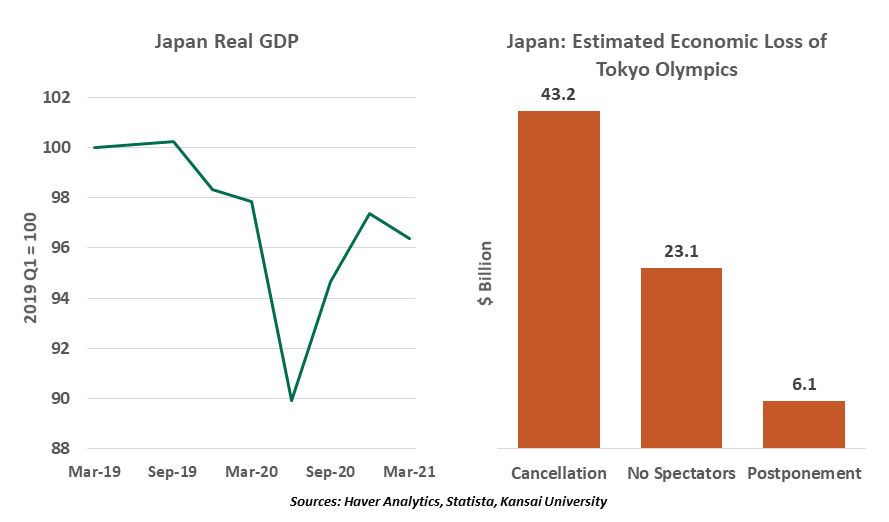

But since then, Japan has been dealing with an increase in infections. States of emergency for major Japanese cities are in place until at least June 20, just over a month before the opening ceremonies of the delayed summer Olympic games. That leaves little time for the economy to return to normalcy before the competition.

Though the event will be hosted without spectators from abroad, Japan is likely to see an arrival of 100,000 athletes, trainers, officials and reporters. While many athletes will be vaccinated before arrival, many will not. Japan has fully vaccinated only about 4% of its population, the lowest among wealthy nations; this leaves most of the Japanese public vulnerable to infection if COVID-19 arrives with one of the Olympic delegations.

Against this backdrop, clamor for postponing or cancelling the games is growing louder day-by-day. This would have an enormous economic cost; Japan will already be deprived of the spending that would have been done by the one million international spectators who will not be attending. The Tokyo games are the most heavily sponsored in history, and some sponsor revenue would have to be forfeited if the games do not go on. According to a study, cancellation would cost Japan $43 billion, while a televised-only event would translate to a $23 billion hit to the economy.

|

Postponing the Olympics again might be the best option, but stakeholders want the Games to go on. |

Postponing the Olympics would be the least economically damaging outcome. Unfortunately, it is not an option the stakeholders are considering. Putting on a successful Games will provide much-needed economic impetus to the Japanese economy. But the gathering could torch a costly wave of infections in Japan and abroad.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All