China's Crackdown on Bitcoin Mining Is Good News for North American Crypto Miners

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBitcoin erased its 2021 gains this week as China ramped up its crackdown on mining of the cryptocurrency, a move that’s expected to help shift the industry’s center of gravity from Asia to North America.

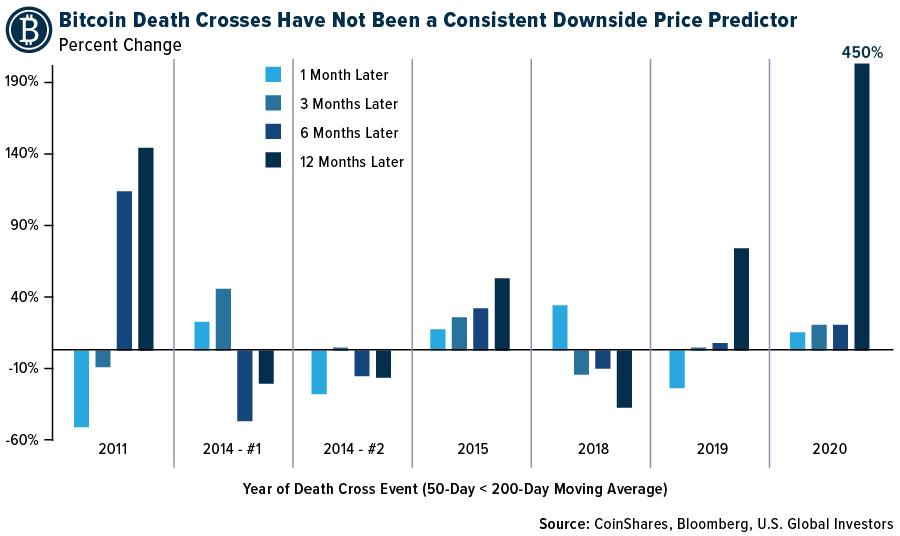

Meanwhile, the Bitcoin price formed a death cross on Monday, with the 50-day moving average trading below the 200-day moving average (MA). This technical pattern is often seen as a bearish sign of things to come, but that may not be the case with Bitcoin.

Bitcoin death crosses have not historically been consistent downside price predictors. Take a look at the chart below, shared in a Tuesday tweet by CoinShares. The digital asset investing firm analyzed Bitcoin’s price action one, three, six and 12 months following previous death crosses, and no pattern emerged suggesting that a sustained bear market was triggered when the 50-day MA dipped below the 200-day.

If anything, the chart shows that your chances of being rewarded improved the longer you held. A death cross occurred in March 2020, and had you held for a year, you could have seen returns as high as 450%, according to CoinShares.

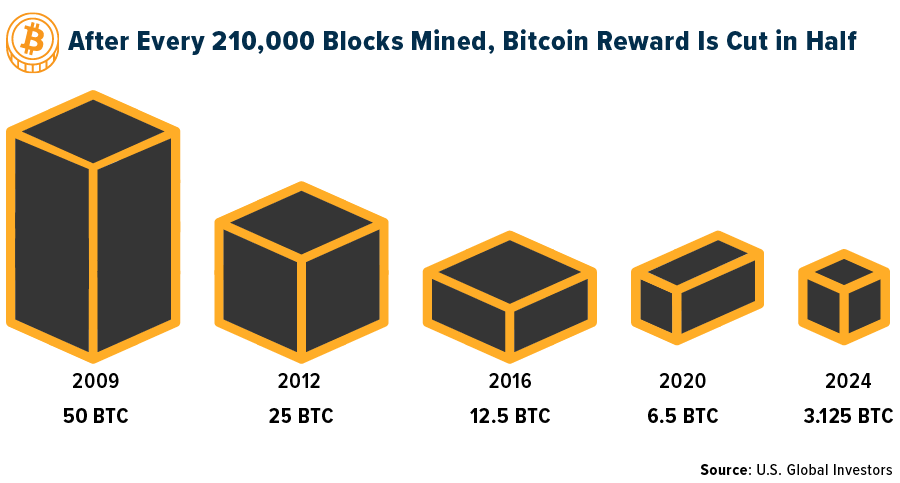

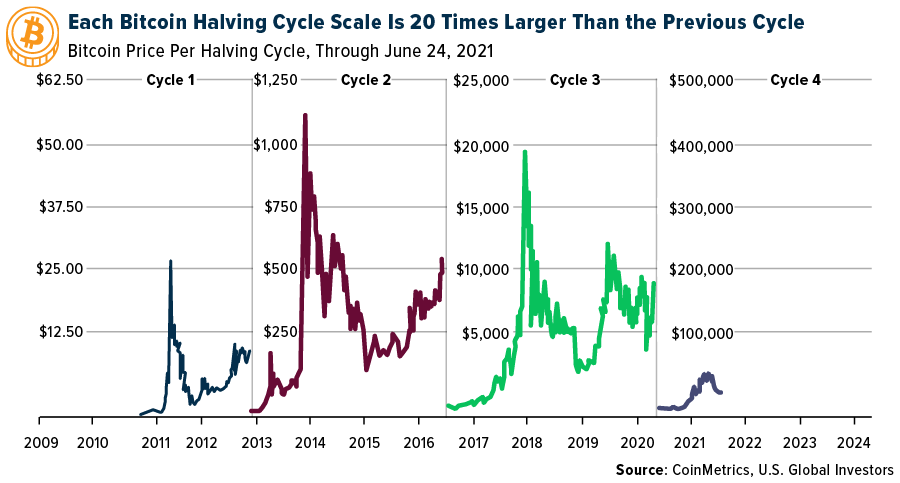

Bitcoin Price Range Has Expanded by a Factor of 20 with Each New Halving Cycle

I should also point out that Bitcoin’s price range appears to have expanded by a factor of 20 with each new halving cycle. As a reminder, halving events are built into the Bitcoin network and are designed to control the supply of the crypto. Whenever 210,000 blocks are mined, which happens roughly every four years, the reward Bitcoin miners receive is cut in half. Currently that reward is 6.25 BTC. It used to be 12.5 BTC, and before that, 25 BTC. When the next halving occurs, sometime in 2024, a block will contain only 3.125 BTC.

Acquiring a new Bitcoin, in other words, becomes increasingly more difficult—not unlike how gold mining has become more difficult over the years as large mineral deposits have become rarer and more expensive to develop.

In the first cycle, which ended with the halving in November 2012, Bitcoin reached a high of approximately $30; in the second, ended July 2016, it was $1,200; and in the third, ended May 2020, $20,000.

Here we are a little over one year into the fourth cycle (check out CoinMarketCap’s timer here), and so far Bitcoin’s price has topped $63,000. Could it hit $100,000, $200,000, $500,000? Obviously, past performance is no guarantee of future results, but the math suggests incredible upside potential, both in this cycle and the next (and the next, and so on).

Mining About to Get Easier for North American Crypto Miners, Thanks to China’s Crackdown

Having said that, mining is set to become a whole lot easier (and profitable) for North American crypto miners, thanks to the Chinese government’s aggressive crackdown on the industry. Until recently, China accounted for between 65% and 75% of all Bitcoin mining. Market dominance is expected to shift to North America, though, after an estimated 90% of China’s Bitcoin mining capacity has been ordered to shut down due to concerns over its environmental impact.

Blockchain.com data already shows that the global hashrate, a measure of the computational power used per second by the Bitcoin network, has fallen 50% from its peak in mid-April. It’s now at its lowest level since November 2020.

This could be highly favorable for U.S. and Canadian crypto miners, including HIVE Blockchain Technologies, who (for now) will no longer have to compete with China for precious blocks.

Big-Name Actors in Finance Bullish on Crypto

Some big-name actors in traditional finance are using this time as an opportunity to make their moves in the crypto ecosystem.

Bullish, a new crypto exchange that’s backed by a group of billionaires including PayPal co-founded Peter Thiel, is in talks to go public by merging with a special purpose acquisition company (SPAC). Launched in May, the exchange is an independent subsidiary of Block.one, the software company behind the open-source blockchain platform EOSIO. Bullish could be valued as high as $12 billion, according to Bloomberg.

And then there’s Andreessen Horowitz. Also known as a16z, the venture capital firm launched what’s believed to be the largest crypto fund to date, with more than $2.2 billion to invest. The mandate of the fund, named the Crypto Fund III, is to invest in a wide range of sub-industries within the ecosystem, including not just the digital currencies themselves but also decentralized finance (DeFi) companies, crypto trading and exchange firms, crypto brokerage firms, privacy and security firms and more.

“We are radically optimistic about crypto’s potential to restore trust and enable new kinds of governance where communities collectively make important decisions about how networks evolve, what behaviors are permitted and how economic benefits are distributed,” the Crypto Fund III team wrote.

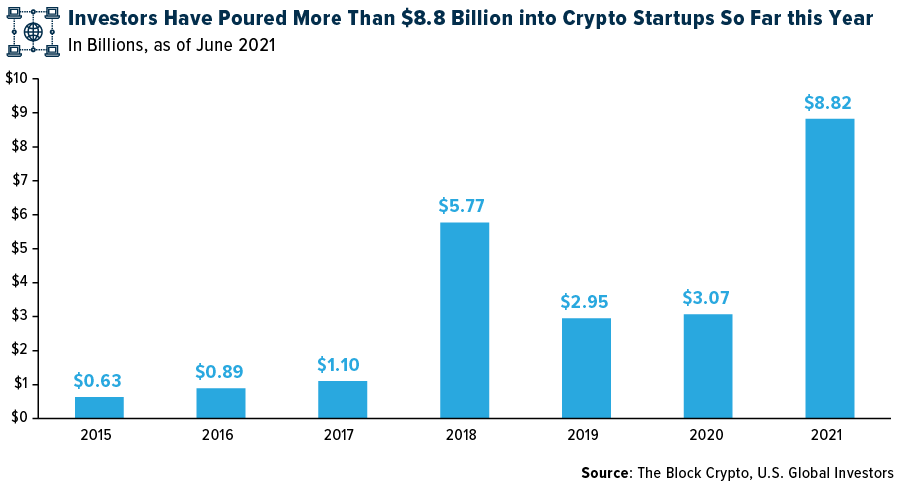

It’s not just a16z that’s radically optimistic. So far this year, investors have poured more than $8.8 billion into crypto startups and private equity, far outstripping the total amount seen in any other year.

It’s definitely an exciting time to be an investor in this nascent industry. Some people may worry it’s too late to start participating, but I believe we’re still in the bottom of the first inning. And with Bitcoin and ether well off their highs, now could be a very attractive entry point.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 3.44%. The S&P 500 Stock Index rose 2.74%, while the Nasdaq Composite climbed 2.35%. The Russell 2000 small capitalization index gained 4.32% this week.

- The Hang Seng Composite gained 1.69% this week; while Taiwan was up 1.57% and the KOSPI rose 1.07%.

- The 10-year Treasury bond yield rose 83 basis points to 1.53%.

Airline Sector

Strengths

- The best performing airline stock for the week was Great Lakes Aviation, up 60.0%.Bookings continue to improve, according to Bank of America. Leisure travel tickets sold are up 16% this week versus 2019 levels, while only up 5% last week. International tickets are down 40% versus 2019 levels but were down 44% last week – so an improvement is seen. The U.S. was added to the European Union’s safe travel list, along with seven other countries last week, excluding the U.K. This is likely to lead to the removal of quarantine requirements for tested and vaccinated U.S. travelers.

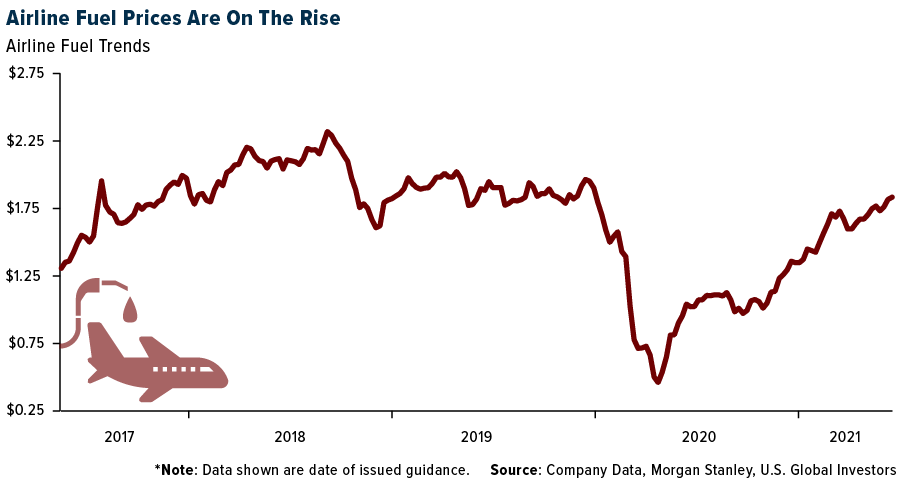

- Alaska Air released guidance for higher-than-expected operating cash flow despite higher fuel prices. This is due to better-than-expected demand in the second and third quarters and SG&A (selling, general and administrative expense) savings. The airline’s load factor guidance was increased to the high end of the 70-75% range.

- Qantas Airways is emerging from the pandemic in a better position than when it started. Almost all of its competitors have encountered significant financial stress, which resulted in the company’s market share increasing from 61% to 74%. Currently, it is one of the most financially secure airlines and is profitable this month. Tourism has been strong within Australia during the pandemic.

Weaknesses

- The worst performing airline stock for the week was Air Berlin, down 7.8%. American Airlines announced it will trim its schedule by 1% through mid-July to ease some of the summer travel disruptions. American canceled hundreds of flights over the weekend due to staffing shortages, maintenance, and other issues as travel demand surges towards pre-pandemic levels.

- UBS analyzed 247 countries and regions (60,000 travel routes) discovering there continues to be high levels of travel restrictions. Global travel restrictions remain heightened but slightly lower at 84% of global routes versus 85% of total routes two weeks earlier. Travel restrictions for G20 routes remained at previous levels but intra-EU travel restrictions remain close to 100% of routes.

- According to Goldman, net debt represents a higher proportion of enterprise value than before the pandemic. Goldman believes that airlines will be very leveraged for several years, even under a maximum debt paydown scenario.

Opportunities

- Southwest Airlines’ 50% off fall travel sale sparked strong web traffic this week. U.S. airlines website visits are up 52% versus 2019 levels, versus down 3% last week. Daily website visits for EU airlines increased to -32% of 2019 levels versus -36% in the prior week.

- Capacity is continuing to ramp up by U.S. airlines. Schedules for June, July and August are showing capacity at 88%, 92% and 93% of 2019 levels, respectively. Schedules for June, July and August are showing global capacity is expected to be at -49%, -28% and -31% of 2019 levels, respectively.

- The European Union recommended lifting travel restrictions on non-essential travel from 14 countries, including the United States. China is included on the list, but not the U.K. This is a major step in improving international arrivals, which fell 70% during the COVID-19 pandemic.

Threats

- Singapore Air’s mandatory convertible bonds were undersubscribed, with only 61% of supply being bought by investors. Controlling shareholder Temasek will absorb the unsold supply.

- Higher oil prices present a threat to airlines as fuel is generally 20-30% of the cost structure for most. While many of the U.S. airlines no longer hedge fuel, Southwest and Alaska are 69% and 52% hedged, respectively, for the remainder of 2021. Among Asian airlines, only Singapore Air and the Japanese airlines are fully hedged. Historically, higher oil prices have been passed to customers with a three-to-six-month time lag about 70% of the time.

- Lufthansa plans to launch an equity issue to reduce leverage, which may be of investor concern. This may prove challenging to raise sufficient new equity. Lufthansa’s revenue is 70% long haul revenue, and earnings recovery is likely to be delayed due to slow reopening of borders.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Poland, gaining 2.9%. The best performing country in Asia this week was China, gaining 2.4%.

- The Hungarian forint was the best performing currency in emerging Europe this week, gaining 2.0%. South Korean won was the best performing currency in Asia this week, gaining 0.71%.

- Preliminary June purchasing managers’ index numbers (PMIs) were released and came in stronger in the Eurozone. Manufacturing PMI stayed at 63.1, above expected 62.3. Service PMI spiked to 58 in June from 55.2 in May. Composite PMI increased to 59.2 from 57.1. Germany is driving the strength in manufacturing activities, as well as in the service segment.

Weaknesses

- The worst performing country in emerging Europe for the week was Czech Republic, losing 0.7%. The worst performing country in Asia this week was Thailand, losing 2.0%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 0.13%. The Thailand baht was the worst performing currency in Asia, losing 0.90%.

- China is planning to keep its pandemic border restrictions for another year. However, it is possible that China may ease restrictions between the mainland, Hong Kong, and Macau.

Opportunities

- As the chart below illustrates, U.S. financial conditions are tightly correlated with demand for risky assets, including emerging market stocks and currencies. The Federal Reserve is unlikely to hike in 2021 and 2022. “Monetary conditions should remain easy for some time,” said Didier Lambert, JPMorgan Asset Management’s lead portfolio manager for Emerging Markets (EM) fixed income. In addition, some central emerging markets started to hike rates. This week Hungary increased rates by 30 basis points and Czech Republic increased rates by 25 basis points. Russia hiked its repo rate already a few times this year. Currencies of these countries may see greater demand.

- The United States and China may renew discussions again. President Biden is set to push for a series of high-level meetings between Washington and Beijing officials. These meetings could take place as early as next week on the sidelines of the G20 summit. The White House is working on a direct call between President Biden and President Xi. It is possible that President Biden completed his trip to Europe having improved overall U.S./EU relations and is now turning to improve the U.S.’s relationship with China.

- RenCap Securities reported that Russia has done a huge shift away from oil dependency - with oil at 11% of GDP and 50% of revenue in 2006 to 5% of GDP and 28% of revenue in 2020. The shift has been negative for growth, as taxes have been raised in other areas. However, the bulk of the transition is over, so growth should start to accelerate.

Threats

- Hong Kong’s sole remaining pro-democracy newspaper published its last edition this week. It was forced to shut down after five editors and executives were arrested and millions of dollars in its assets were frozen as China continues to bring Hong Kong back to the mainland. Apple Daily was founded by Jimmy Lai in 1995 – just two years before Britain handed Hong Kong back to China.

- Russia re-opened flights to Turkey at the time when Moscow sees a new wave of COVID cases. 10,000 to 15,000 Russian tourists are expected to travel to Turkey daily, but if the COVID situation does not improve quickly in Russia, border closures may be soon reinstated. Turkey needs vacationers as tourism is essential to its economic growth.

- The Delta Plus Variant of COVID, first located in India, is spreading quickly in Europe. The hyper-transmissible strain of the novel coronavirus ‘the Delta Variant’ is expected to account for nearly 90% of the COVID cases in the EU, the European Centre for Disease Prevention and Control (ECDC) has warned.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was natural gas, up 8.77%. Natural gas stockpiles across the globe are decreasing as energy demand picks up.

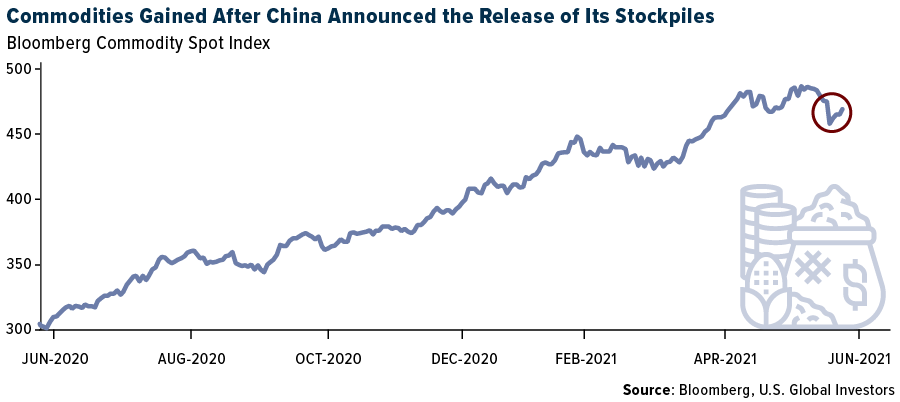

- President Joe Biden and a group of bipartisan senators agreed on a $579 billion U.S. infrastructure deal. The news was headwind for the commodities market as copper resumed its gains and nickel headed for the biggest weekly increase since 2019 amid supply concerns. Copper has been rebounding from a two-month low after China announced lower-than-expected state reserve sales of commodities. Meanwhile, cash nickel contracts on the London Metal Exchange (LME) traded at a steepening premium compared to the three-month futures, suggesting that spot demand is running ahead of supply. The chart below shows that the commodities market has sustained Chinese efforts to cool the rally.

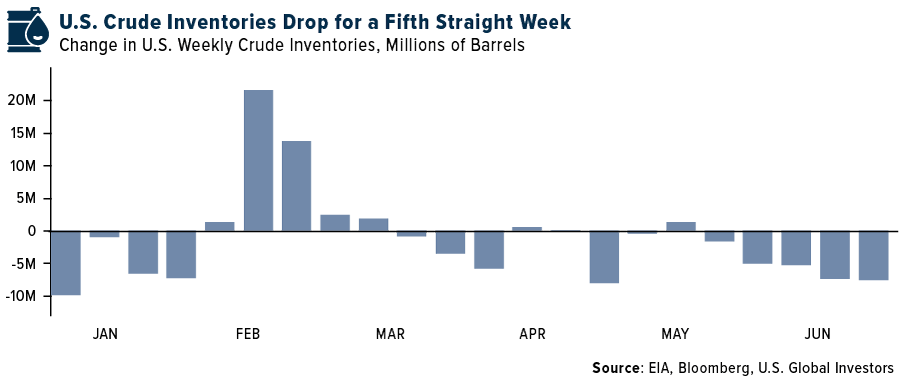

- Oil is headed for the longest winning streak since December on the back of improving demand and tightening supply. West Texas Intermediate (WTI) crude futures are on track to increase more than 3.5% this week, marking its fifth straight weekly advance, while Brent crude oil is trading at the highest level since October 2018. With demand continuing to rebound, the market expects OPEC+ to hike production by modest levels. Stockpiles in the U.S. and Europe continue to decline, with U.S. reporting a fifth week of declines in stockpiles. The chart below shows change in U.S. weekly crude inventories.

Weaknesses

- The worst performing commodity for the week was corn, down 8.39%. Corn futures slumped as ample rain is forecasted to hit the U.S. farm belt.

- Iron ore prices in China slid for a second consecutive week as traders expect a seasonal lull in domestic steel consumption, reducing profitability of mills producing the metal. Construction and manufacturing activity in China slows down during the summer, and more mills have stepped up maintenance work as margins declined after domestic steel prices fell amid efforts to cool the commodities rally.

- Soybean-oil and ethanol-credit prices plummeted after the U.S. Supreme Court ruled in favor of oil refineries in a case on national biofuel policy. The court ruled that the Environmental Protection Agency has wide latitude to exempt refiners from requirements that they mix renewable fuels into gasoline and diesel. Soy oil fell almost 6% following the news, while corn, which is used to make ethanol, dropped as much as 3%. Ethanol-credits that track compliance with the blending law, known as Renewable Identification Numbers (RINs), fell as much as 27%. Both soybeans and corn are on track for a second straight month of declines, the longest losing streaks in more than a year.

Opportunities

- Trafigura Group forecasts that oil could top $100 per barrel in the next 12 to 18 months as the recovery from the pandemic drives a rebound in demand. Brent crude surged above $75 per barrel for the first time in two years as economies start lifting restrictions, leading to an increase in demand for gasoline, diesel, and jet fuel. The trading group’s global chief economist noted that the pick-up in consumption, which is currently driven by the U.S. and Europe, and structural underinvestment in new production will drive prices higher. Trafigura Group joins Bank of America Corp. and Goldman Sachs Group Inc. in forecasting that oil could breach the $100 per barrel mark.

- Horizons ETFs Management Canada launched two exchange-traded funds that provide investors exposure to lithium and hydrogen. The Horizons Global Lithium Producers Index ETF (HLIT) offers exposure to companies focused on mining or production of the metal, as well as lithium compounds and lithium-related components. The Horizons Global Hydrogen Index ETF (HYDR) offers exposure to companies that produce hydrogen fuel cells and hydrogen, as well as companies involved with equipment, storage, and transport.

- Mukesh Ambani, Chairman of Reliance Industries Ltd., unveiled an ambitious push into clean energy with $10.1 billion of investment over the next three years. The company, which gets 60% of its revenue from oil refining and petrochemicals, plans to spend $8.1 billion on four giga factories to make solar modules, hydrogen, fuel cells, and to build a battery grid to store electricity.

Threats

- Natural gas markets around the globe are rallying as a long and frigid winter drained gas stockpiles, with utility providers struggling to build them back up. Gas prices hit a 13-year high in Europe this week. European utilities will resort to burning more coal if a gas deficit does develop in the coming months. The gas sector has transformed from segmented between geographical regions to a global market, attributed to the ramp-up in new supply of liquefied natural gas (LNG) and growing liquidity in spot trading. This now means that Europe and North Asia compete for a finite supply of LNG, resulting in bidding wars that catapult spot rates.

- In a bid to help cool domestic inflation after commodities’ prices surged, Russia is planning temporary taxes on steel, nickel, aluminum, and copper exports. Economy Minister Maxim Reshetnikov said that the government is proposing that a duty of at least 15% will be effective from August 1, 2021, through year-end, with each metal also having a specific duty. These taxes could have far-reaching implications for global metals markets that are facing tight supply, like aluminum. United Co. Rusal International PJSC controls 10% of the global aluminum sector, MMC Norilsk Nickel PJSC produces 20% of the world’s nickel, while Russia is the third-biggest steel exporter.

- China Iron & Steel Association proposed that the government must strengthen its supervision of foreign iron ore traders in the country which, it alleges, conspired with miners to inflate prices. Additionally, profits of Chinese steelmaking mills are sinking rapidly as input costs have remained high and easing demand. Mills are being forced to scale back operations after output hit record-highs in the last two months.

Domestic Economy and Equities

Strengths

- Weekly initial jobless claims fell modestly to 411,000 in the week ending June 19 versus 418,000 the week prior. Continuing claims for the week ending 12-Jun fell to a new post-Covid low 3,390,000 vs prior 3,534,000.

- The manufacturing purchasing managers’ index (PMI) rose 0.5 points month-over-month to 62.6 (61.5 expected), a new record level, with confidence also higher due to loosening COVID restrictions. Services PMI declined 5.6 points to 64.8 (69.8 expected) although remained at the second highest level on record with new business gained.

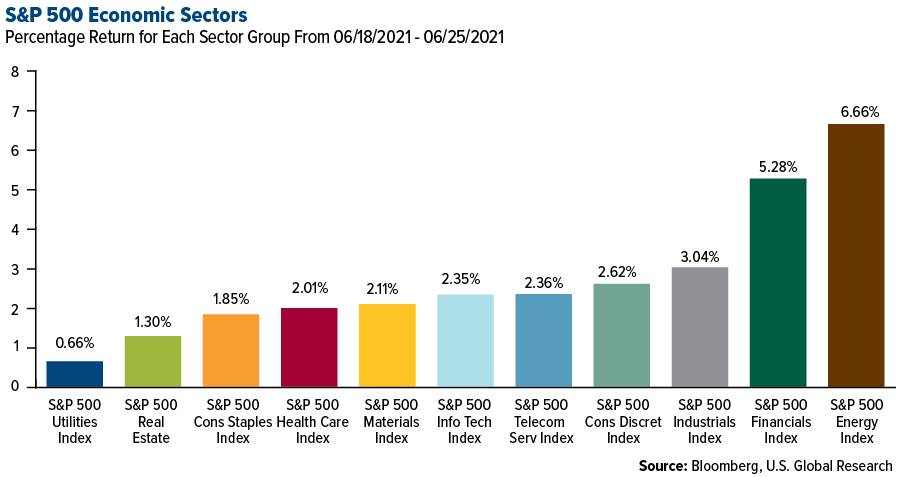

- Nike Inc. was the best performing S&P 500 stock for the week, increasing 19%. Shares gained after the company reported better-than-expected fourth-quarter results and forecasted annual revenue to surpass $50 billion for the first time. Several analysts increased their price targets on the stock.

Weaknesses

- Employment grew at the slowest pace in three months while confidence moderated with companies noting higher shipping costs. Many companies throughout the U.S. are reporting labor shortages.

- U.S. home prices in May posted their biggest annual increase in more than two decades, as low borrowing rates fueled demand. The median existing-home sales price topped $350,000 for the first time, 24% higher than the prior year. Buyers are having trouble finding properties they can afford.

- Biogen Inc., a pharmaceutical company, was the worst performing S&P 500 stock for the week, losing 13.2%. Biogen’s rival, Eli Lilly is trying to get its Alzheimer’s treatment approved by the Food and Drug Administration (FDA). Biogen’s Alzheimer’s treatment was approved by the FDA just a few weeks ago.

Opportunities

- The U.S. consumer price index (CPI) rose 5% year-over-year in May, the highest level in 13 years, while core inflation was at 3.8%, the highest level in 30 years. Despite these numbers, Federal Reserve Chairman Jerome Powell believes that inflation impacts on the economy were largely transitory. Powell cited pandemic demand for airline tickets, for example, as many are getting vaccinated and deciding to travel at the same time. Rising prices in the U.S. have been driven not by a surplus of money above pre-pandemic levels, but in many cases by supplies of goods and services that are below pre-pandemic levels.

- Following a meeting with a bipartisan group of senators, President Biden on Thursday announced an infrastructure deal. As expected, the top line is $1.2 trillion over eight years with $579 billion in new spending. The White House outline shows $109 billion for roads and bridges, $66 billion for rail, $65 billion for broadband, $55 billion for water infrastructure, and $49 billion for public transit. The deal involves no new individual taxes or user fees.

- All 23 of the nation's biggest banks are healthy enough to withstand a sudden economic catastrophe, the Federal Reserve said Thursday as it released the results from its latest “stress tests," giving the banks the green light to resume paying out dividends to investors and buying back stock. The Fed also said it would remove all coronavirus pandemic restrictions it put on the banking industry last year, following the results of the tests.

Threats

- The Delta variant of the coronavirus is spreading rapidly throughout the U.S. The Delta strain, which first emerged in India in late 2020, will probably make up 50% of COVID-19 infections in the United States by early- to mid-July, said Willian Lee, Vice President of Science at population genomics company Helix, Wall Street Journal reported.

- Treasury Secretary Janet Yellen warned on Wednesday that the U.S. could face a serious risk of default as soon as August if Congress does not raise or suspend the debt limit. She stressed that to avoid uncertainty for financial markets, let alone the catastrophic economic consequences, Congress should pass new debt limit legislation before the latest suspension expires on July 31.

- U.S. 10-year yields increased and may continue to move higher after President Biden sealed a $579 billion infrastructure deal with legislators. Rising yields are negatively correlated with bond prices and equites.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Quant, rising 48.00%.

- New York Digital Investment Group (NYDIG) and Q2 Holdings announced their partnership to provide access to Bitcoin for bank account holders in the U.S. Q2, a firm that specializes in providing digital services to financial institutions, provides internet banking services to about 30% of the top 100 U.S. banks and serves over 10% of the country’s digital banking customers. This partnership, as per a press release, could potentially open Bitcoin buying, selling and custody channels to 18.3 million bank customers in the U.S. in a bid to provide easy access to Bitcoin for U.S. customers, NYDIG has already partnered with Financial Technology (fintech) firm Fidelity National Information Services, cloud-based digital banking service provider Alkami, and California-based First Foundation Bank.

- El Salvador’s President Nayib Bukele announced that the nation’s Bitcoin Law is set to come into effect on September 7, 2021, which will make the largest cryptocurrency a legal tender within the nation. The government will use the Chivo e-wallet, preloaded with $30 of Bitcoin for anyone who downloads it. The users will have to verify their identity via Chivo’s face recognition software before receiving the $30 in Bitcoin. The law was passed by El Salvador’s legislature on June 9, 2021, by a supermajority.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Kusama, down 42.87%.

- Founders of AfriCrypt, a South Africa-based crypto investment firm, have allegedly disappeared with approximately 69,000 Bitcoins, worth an estimated $2.3 billion. According to investors in AfriCrypt, they received an email claiming that the platform was ending operations and freezing all accounts after it fell victim to an alleged hack, adding that the investors should not report the hack to law enforcement, claiming that it would only slow down the recovery process. AfriCrypt’s founders – 20-year-old Ameer Cajee and 17-year-old Raees Cajee—reportedly transferred the pooled investor funds and fled to the U.K.

- The U.S. Securities and Exchange Commission (SEC) postponed its decision on whether to approve a Bitcoin exchange-traded fund (ETF) filed by Texas-based Valkyrie Digital Assets. After receiving comments on the proposed rule changes regarding the Valkyrie Bitcoin Fund, the SEC delayed its deadline for a decision by 45 days, and is designating August 10, 2021, as the revised date for its decision. This comes a week after the SEC delayed its decision on the VanEck Bitcoin Trust for the second time, citing that it would need more answers from interested parties on questions regarding the susceptibility of a Bitcoin ETF to market manipulation.

Opportunities

- Digital Assets AG (DAAG), a Switzerland-based token issuer, announced the launch of its stock-tokenization infrastructure on the Solana blockchain. This will allow users of the FTX Cryptocurrency Derivatives Exchange trading platform a novel way to access traditional equity markets. DAAG reported that FTX customers, who have completed Know Your Customer (KYC) documentation, will have access to 55 free-floating stocks which can be traded even when the traditional exchanges are closed. Free-floating stocks are assets that have received regulatory approval for trading on a tokenized platform, and DAAG said that tokenized stock offerings are valid in the European Economic Area through a prospectus endorsed by Liechtenstein’s Financial Market Authority.

- Venture capital firm Andreessen Horowitz launched the biggest-ever crypto venture fund, Crypto Fund III, at $2.2 billion. The California-based company said that the fund will be used to finance cryptocurrency networks and teams that contribute to the new decentralized economy—investing in all stages, from early seed-stage projects to fully developed later-stage networks. Andreessen Horowitz is already a prolific investor in the blockchain industry with investments in the Solana blockchain, non-fungible token (NFT) marketplace OpenSea, Talos trading platform, Coinbase, and Facebook-backed Diem.

- Citigroup announced that its wealth management division has formed a Digital Assets Group, which will focus on all aspects of the fast-growing space of blockchain enabled finance. As part of Citi Global Wealth Investments (CGWI), Citi’s Digital Assets Group will service clients interested in the world of digital assets such as cryptocurrencies, NFTs, stablecoins, and central bank digital currencies (CBDC). This announcement marks the foray of another legacy bank into the digital asset space amidst increased interest from its clients.

Threats

- Earlier this week, Bitcoin’s hash rate dropped by 16.94% in less than 24 hours after authorities in China’s Sichuan province ordered 26 mining farms to close operations. This latest crackdown on cryptocurrency mining in China is being attributed as the reason for Bitcoin’s latest slump, as the largest cryptocurrency fell below $29,000 for the first time since January 2021. In April, Chinese authorities in Xinjiang region imposed a ban on cryptocurrency mining, cutting Bitcoin’s hash rate by 30% and contributed to a $10,000 decline in Bitcoin’s price. Chinese miners account for roughly 65% of the total computational power backing the Bitcoin blockchain, and a decline in total hash rate reduces the overall security of the network and increases the time spent on validating blocks and transactions, further reducing the profitability of miners. The following chart shows that Bitcoin dropped below $30,000 this week on the back of China’s crackdown.

- Japan’s Financial Services Agency (FSA) issued a warning to cryptocurrency exchange Binance, stating that the exchange is not registered to do business with residents of Japan. The FSA had issued a similar warning to Binance in March 2018, and to Bybit this year, as none of these exchanges are registered in the country.

- MicroStrategy Inc. is set to mark down the value of 13,005 Bitcoins it purchased this week after the price of the largest cryptocurrency plunged. The company had bought these Bitcoins at an average price of $37,617 per coin and accounting rules dictate that MicroStrategy must write down the value of its holdings once the market value dops below the price at which it had acquired the coins. The company is set to take a charge of $284.5 million in its next earnings report from previous write downs, and it will bring MicroStrategy’s total Bitcoin-related impairments to more than $500 million.

Gold Market

This week spot gold closed the week at $1,781.44, up $17.28 per ounce, or 0.98%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.35%. The S&P/TSX Venture Index came in up 0.18%. The U.S. Trade-Weighted Dollar fell 0.45%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-23 | New Home Sales | 865k | 769k | 817k |

| Jun-24 | Durable Goods Orders | 2.8% | 2.3% | -0.8% |

| Jun-24 | GDP Annualized QoQ | 6.4% | 6.4% | 6.4% |

| Jun-24 | Initial Jobless Claims | 380k | 411k | 418k |

| Jun-28 | Hong Kong Exports YoY | -- | -- | 24.4% |

| Jun-29 | Germany CPI YoY | 2.3% | -- | 2.5% |

| Jun-29 | Conf. Board Consumer Confidence | 119.0 | -- | 117.2 |

| Jun-30 | Eurozone CPI Core YoY | 0.9% | -- | 1.0% |

| Jun-30 | ADP Employment Change | 575k | -- | 978k |

| Jun-30 | Caixin China PMI Mfg | 51.9 | -- | 52.0 |

| Jul-1 | Initial Jobless Claims | 380k | -- | 411k |

| Jul-1 | ISM Manufacturing | 61.0 | -- | 61.2 |

| Jul-2 | Change in Nonfarm Payrolls | 700K | -- | 559k |

| Jul-2 | Durable Goods Orders | -- | -- | 2.3% |

Strengths

- The best performing precious metal for the week was palladium, up 6.67%, as platinum group metals bounced back strongly this week from the double-digit losses experienced last week. Gold continued to stabilize after comments from Fed Chairman Jerome Powell indicated that inflation should move back to the 2% target once supply imbalances are resolved. Toward the end of the week, gold edged lower as economic data indicated a recovery is underway.

- Silvercorp Metals reported assays from its 2021 exploration program at the LME mine at its Ying Mining District. The average of 60 infill and step out holes drilled on known veins averaged 448 grams per ton silver. This is higher than the current measure and indicated (M&I) grade of 301 grams per ton silver.

- Montage Gold Corp last night provided an update on developments at its Kon Gold Project, with a positive takeaway in our view of the rapid pace of development that the company continues to have. With seven drill rigs turning, this program is now 95% complete with a total of 49,694m drilled to date since commencement of the program in January 2021.

Weaknesses

- The worst performing precious metal for the week was gold, but still up 0.98%. Hochschild Mining reported that a bus operated by one of its contractors to transport employees between the Pallancata operation and the city of Arequipa in southern Peru was involved in a traffic accident resulting in 27 fatalities and 13 injuries. A total of 50 miners were in the bus when it flipped.

- Equinox Gold Corp. said Tuesday that a mine in the Mexican state of Guerrero has been blockaded by a group of unionized employees and members of the Xochipala community. The Canada-based mining company said it has suspended operations at its Los Filos mine, and said that it is working to find a long-term solution with the union and community members who are demanding higher payments than were contractually agreed upon.

- Kinross Gold provided an update on the Tasiast fire that occurred on June 15. The company has resumed mining activities (including stripping to access higher grade ore), while milling operations remain suspended. Kinross is building higher grade stockpiles for when the mill restarts – possibly by year-end. Preliminary estimates indicate a restart of the SAG mill by year-end at a cost of up to $50 million. Production estimates were reduced by 13% for 2021.

Opportunities

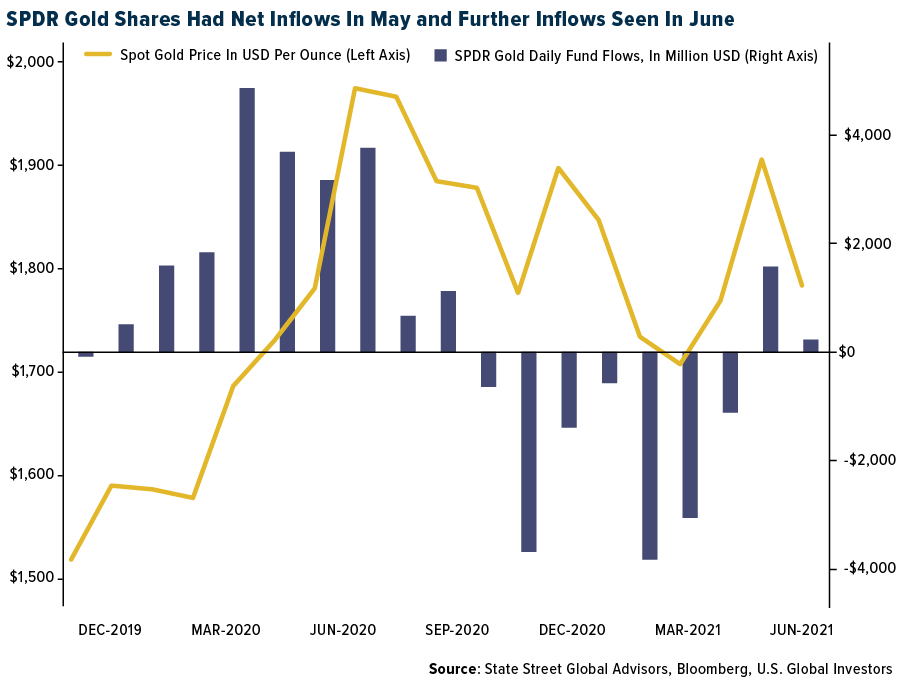

- Gold purchases by central banks and ETFs is continuing. Poland’s gold holdings increased 1% in May, to $7.4MM ounces. The May purchase was the first major purchase by the central bank since 2019. Thailand has boosted its gold reserves 60% in recent months. ETFs added 283,000 ounces of gold last week, which was the biggest increase since March 19. Gold has had seven straight weeks of inflows. Net inflows have been $390 million in the first three weeks of June.

- De Grey Mining released its maiden resource statement for its gold discovery at Hemi, declaring 6.8 million ounces at a finding cost of just A$8.50 per ounce, well below industry averages. This brings the gold inventory up to 9.0 million ounces for De Grey’s Mallina Gold Prospect. De Grey’s gold discovery is in the Pilbara region, not known for gold discoveries, but more the home to the iron ore mining districts. This still provides a costs advantage to De Grey as there is well developed infrastructure support in the region, which could lower capital costs.

- Indonesia, home to one of the world’s largest gold mines, plans to set up a bullion bank to spur trading of the precious metal domestically. The plan is to start this bank in 2024. Indonesia currently exports much of its gold to countries such as Singapore and Australia.

Threats

- Morgan Stanley forecasts that scaled back bond buying and higher interest rates are likely to be a drag on gold. Susan Bates, commodity strategist, wrote that higher inflation is likely to be transitory. Jewelry markets are expected to recover but total sales will likely end 2021 12% lower than the pre-pandemic year of 2019. Morgan Stanley left intact its $1,680 price target. A counter factor outside the Morgan Stanley report that investors will be watching for, that would overpower the transitory inflation argument, would be rising wages for labor.

- Bolivian lawmakers are debating a bill that would require all gold produced in the country to be offered to the central bank as the nation builds its reserves and cracks down on the illegal bullion trade. Local producers would need certification to sell abroad and would first be required to offer their gold to the central bank at international prices in return for tax breaks.

- According to RBC, new projects have faced upward pressure on capital costs due to ongoing cost inflation including steel (up 50% or more year-to-date) and labor. Since 2019, RBC estimates that project capital intensity has increased by 25%, with average cost to build a 100,000 ounce per year operation of $205 million. Operating costs are also under pressure. Diesel is one of the largest components of input costs, with higher prices to date (up 25%) placing upward pressure on operating costs. RBC estimates a $90 per ounce cost impact for open pits versus $28 per ounce for underground mines.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits