TINA Is Stupid

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGetting Lucky

Artificial Reality

Locked In

Washington DC, Maine, and Colorado

In the 1980s, British Prime Minister Margaret Thatcher liked to say, “There is no alternative” to her market-driven economic reform ideas. She said it so much people began abbreviating it as “TINA.”

Whatever you think of Lady Thatcher’s policies, the slogan was certainly effective politics. If victory is inevitable, you can either cooperate or be left behind. But her phrase actually goes back further to an 1851 book by Herbert Spencer, who also famously coined “survival of the fittest.”

More recently, TINA has been applied to investing. You must buy stocks because TINA. You can’t make money any other way. Just close your eyes, buy and hold forever. Or at least through a full market cycle.

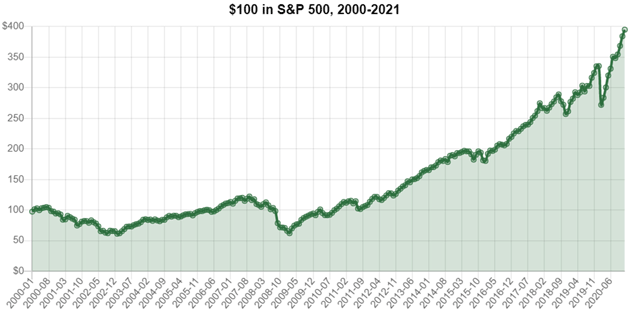

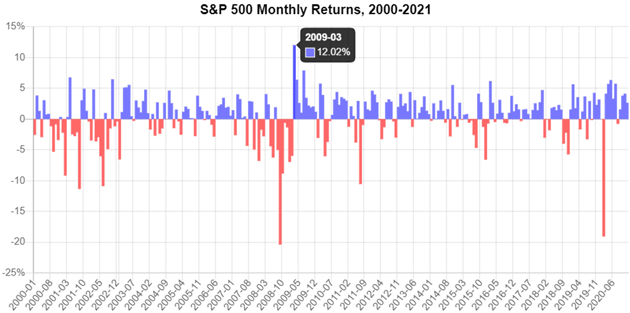

Frankly, I think that’s stupid. It isn’t true. First of all, buying and holding stocks isn’t guaranteed to work no matter how long you give it. There have been periods where stock market returns were less than zero for 20 years. Starting in 1966, it took 16 years for the market to recover back to its original level and in inflation-adjusted terms it was 26 years. The first decade of this century was essentially flat (see chart below).

However, there is nothing like a roaring bull market to make everybody forget the past. We all know it’s different this time (note sarcasm). I mean, the Fed has the wind at our back, and all we have to do is to unfurl the sails and move ever forward. Thus TINA.

It helps if you somehow had the wisdom to avoid the 2000s up until the magic point of March 2009 and then jump in. But what happened if you weren’t quite so prescient and invested at the beginning of 2000?

If you invested $100 in the S&P 500 at the beginning of 2000, you would have about $394.90 at the beginning of 2021, assuming you reinvested all dividends (in 2013 dollars to average the currency fluctuation). This is a return on investment of 294.9%, about 7% yearly. This investment result beat inflation for a 152.6% cumulative real return, roughly 4.5% per year.

By the way, those returns assume you had no taxes, investment management fees, platform fees, ETF and mutual fund fees, etc.

The chart below shows what’s happening for the last 21 years, and the sheer awesome power of a roaring bull market for the last 12 years. Even with the “Greenspan put,” the first 10 years of the 2000s ended essentially flat. And then the financial crisis, QEs 1, 2, and 3, with Jerome Powell adding another still-continuing QE after the COVID meltdown. Please note: I’m not saying the returns are artificial or are not real because quantitative easing was involved. They absolutely are.

Source: in2013dollars.com

Source: in2013dollars.com

You need to be incredibly lucky to only invest in bull markets. The odds still aren’t great unless you a) have a longer time horizon than most people do and 2) don’t get scared out by the inevitable downturns.

But more important, and the point to this week’s letter, is that there are alternatives to the kind of stock investing Wall Street usually peddles. And some of them are, in my opinion, far more likely to help investors achieve their goals.

Typically, potential investors are shown stock market returns over 60 to 80 years, which includes three or four full cycles, and then take those returns projected into the future. Save your money you are told, accumulate $1 million, and then you can take 5% a year for a 30-year retirement. Just keep your money invested and it will grow faster than your withdrawal rate, because the average return is over 7%.

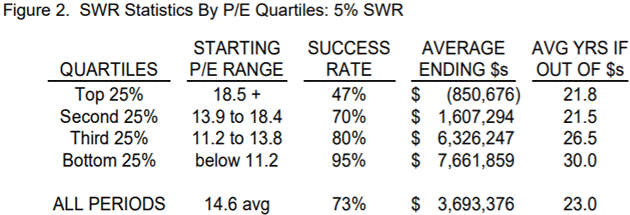

Well, not so fast. My friend Ed Easterling at Crestmont Research says it makes a great deal of difference when you start your retirement. If you start at a time of high valuations (like now) the chance your money will run out before 30 years is also quite high. In fact, in the chart below, if you start at the top 25% of valuation quartiles you would run out of money in an average of 21.8 years. Your money only lasts 30 years 47% of the time. Not exactly good odds. Starting at low valuations? Well, the force is with you.

Source: Crestmont Research

But taking these risks is precisely what TINA advocates suggest you do. For something as serious as retirement, I think that’s insane. There is no reason to take such risks. You have alternatives.

Today we’ll think about this “TINA” nonsense and look at some of the alternatives TINA advocates claim, or at least pretend, don’t even exist. They do exist and you deserve to know about them.

Getting Lucky

Financial planning is really a giant math problem. You can know some of the variables: your current age, how much money you have right now, how much you can add to savings each year, when you want to retire (or buy that house, etc.). Others you can only guess: your lifespan, the inflation rate, market returns and volatility, future tax policies, and so on.

Nevertheless, a good planner can crunch all those numbers and inform you what level of return you need. Then, you can look for investments that give you the best shot at reaching it. Many investors go wrong by overreaching. If all you need is 5% annual gains and you’re plunging most of your money into, say, tech stocks or Bitcoin, you may get lucky and earn a lot more than 5%. But you may also experience losses that prevent you from achieving an otherwise reasonable goal.

The other and perhaps more common problem is excessive goals that raise your return target, thereby forcing you to take more risk. If you are age 60 with no savings, and you want to stop working in 5 years, you will have an uphill climb. Those high tech-stock returns you hear about will seem pretty attractive. But in reaching for the stars, you run a high risk of falling back to earth. (The answer there is to dial back your expectations, but that’s not fun so few people do it.)

All this is much harder than it used to be because interest rates are so low. Not so long ago, those with modest goals could almost guarantee success with a portfolio of long-term bonds or CDs. Treasury bonds, blue-chip corporate bonds, even some tax-exempt muni bonds had decent returns and low-risk profiles. It was possible to invest a lump sum and be pretty certain of the outcome. You can still do that, but the outcome won’t help you nearly as much.

TINA advocates say none of this matters. Just buy stocks because nothing else is better. At least, that’s been the case for the last 12 years.

Let me state this clearly because it’s important. TINA advocates know stocks go down sometimes. They just don’t care. They’ve convinced themselves any losses are temporary. That may be true, especially for the last 12 years, but also irrelevant if the losses occur right when you need the money.

Artificial Reality

The non-TINA reality is both simpler and more complex. Stocks are a tool, but different jobs require different tools. If stocks are what you need, you still have to use them in a way that matches your goals and risk tolerance. (Note: I am not against holding stocks. I personally own a handful of stocks that are long-term investments for me. But that’s another story.)

Now, there are people who can buy a concentrated stock portfolio, ignore the ups and downs and hold on for years while they climb to a sustainably high level. It happens. But I can tell you, after decades in the business and thousands of client meetings, such people are rare. Having an advisor to encourage you through hard times helps, but then all too often they stop believing the advisor.

What most people really need is consistent growth. If your bogey is 7% annual returns, you’re better off getting as close as you can to 7% every year even if it means missing some upside in strong years. You’ll make it up by missing downside in other years. In other words, you want the predictability of bonds combined with the upside of stocks.

The statistical reality: You can end up in the top 10% of investors over 10 years if you simply are in the top 50% every year for 10 straight years. You don’t have to knock out the lights to win. Just avoid losing.

There was a survey done in 2000. The average investor expected to make 15% per year for the next 10 years. Oops. They got zero, especially after inflation. I daresay that if that survey was done today, it would have a similar higher expectation than a full market cycle average. Certainly nothing like 7%.

Portfolio strategists have long tried to deliver on that dream with ideas like the “60/40” stock/bond allocation. In theory, the bond part will gain value when the stocks are weak, thereby smoothing the overall return and reducing total portfolio volatility. A nice idea, and one that used to work fairly well. It hasn’t done so recently because yields are so low and the Fed’s QE has distorted bond prices beyond economic fundamentals. We can’t be confident they will zig or zag at the right times.

This new (and artificial) reality is becoming more obvious, and it’s a big problem. Trillions of dollars are invested in variations of the 60/40 idea. Almost every large pension plan and endowment keeps its money in some combination of stocks and bonds, but the bond part no longer behaves like it’s supposed to. Bond portfolios average 3% if you’re lucky. It’s probably more like 2% and in a rising interest rate market could be a lot less. It’s become dead weight, contributing little or nothing to overall returns and maybe even adding a new kind of risk.

Suppose, just for example, the Fed decides the economy is doing well enough to aggressively “taper” its various support programs. This could easily make stock prices fall (because liquidity will shrink) while long-term interest rates rise (because the economy is growing). That’s the worst of both worlds for a stock/bond strategy.

I’m not predicting that scenario, to be clear, though I think it’s possible. I mention it to illustrate how this new upside-down world may not work the way we expect.

Locked In

So what can you do? What’s the alternative to stocks?

One answer is stocks, but not all the time. “Market timing” is anathema to many financial advisors, and they’re not entirely wrong. Done badly (and most people do it badly) and with the wrong expectations, it will be worse than buy-and-hold. The key is to realize what timing can and can’t do. I don’t know anyone who captures all the upside and misses all the downside, but you don’t need to. Simply avoiding the worst part of major downturns helps. It helps even if it causes you to miss some gains when the cycle turns. Similarly, “rotation” strategies that stay fully invested but actively shift between market segments to follow momentum can have good results, too.

Part of my personal strategy is using diversified trading strategies, not necessarily diversified stock portfolios. You used to be able to get diversification in various sectors of the market (small-cap versus large-cap, international versus emerging markets versus US, etc.). Now all stock market sectors seemed to move together in a bear market. I have personally identified a handful of ETF trading strategies and managers that I feel comfortable with.

Other alternatives exist, too. Sadly, some of the best hedge funds and private investments aren’t publicly available. Our government has decided they are too dangerous for small investors but “accredited investors” who meet certain income and net worth requirements can jump right in. Like TINA, that is also stupid. Wealth doesn’t prove intelligence, nor does lack of it mean one needs protection. Nevertheless, it is the law for now, so we have to follow it.

If you qualify, I have personally had pleasant results in “private credit” funds. These are non-bank, non-traded lending programs. Investors can get high single-digit returns (or more with increased risk). I don’t like to use the term fixed income to describe them, thinking of them as more cash flow investments. Typically, investors receive higher returns because they give up liquidity. Investing in these is a multi-year commitment. You can’t get your money back until the defined period ends. It’s not like a bond fund you can redeem, or an ETF you can sell on an exchange. You are locked in.

But it turns out that sacrificing liquidity, if you can do it, is an excellent way to boost your returns. The investment itself earns more but, maybe more important, it removes the temptation to bail out at the wrong time. Investors in a three- or five-year private credit fund actually stick around for the full period.

The same is true for many “alternative” private investments. The variety is endless. Name an asset class, and several hedge funds probably trade it. They may not trade it successfully, but if you can get those who do to take your money, you may have found a good opportunity.

In the last few years, new platforms have expanded access to hedge funds for smaller accredited investors. Let’s say a hedge fund has a $10 million minimum investment. A platform would create a feeder fund into it, taking investments as small as $100,000 and aggregating them for a fee. They offer access to funds with very long-term track records, some of the most famous managers in the world and potentially better returns.

I have had a portfolio like that for some time now. We change funds over time, but not very often. “Switching” is a months-long process. Some years the diversified portfolio doesn’t look very smart with low returns. Then again, last year everybody seemed to hit a homerun, at least in my portfolio. At least for one year, my portfolio looked brilliant. But over time it smooths out the returns and helps me achieve my goals.

There are literally scores of different alternative investment strategies. Besides private credit hedge funds, there are closed-end funds which offer decent returns (along with volatility), various funds utilizing a particular manager’s edge, and focused dividend yield strategies.

Many dividend-oriented ETF’s and mutual funds have scores if not hundreds of underlying investments which drag down the average return. There are very good dividend strategy managers who build concentrated portfolios of what they feel are the best dividend-paying companies (with US or international companies or both) and are worth the fees they charge. Over a full cycle, the better managers can outperform the market with about half the volatility. Pair them up with some of the private credit strategies I mentioned above? You have a real chance of getting that 7%.

Without being (too) promotional, at Team Mauldin we like to break our strategies down into two components: Core and Explore. In a presentation we might say that 80% of your assets should be in Core and 20% in Explore. You want 80% in low-volatility, steady-eddy investments that will get you back to your 100% in 4–5 years. Then you get more aggressive with your Explore bucket, diversifying into investments which have much higher return potential, where you are looking for multiples and not 7%.

That 80/20 is just an example. The older you are the less risk you should take. How much risk you should be taking when you’re young depends on what your income levels are. Are you going to inherit wealth? A hundred questions have to be asked to determine the right portfolio design for you. There is no one-size-fits-all which is why I never try to put something like that in a letter. Creating an “Explore” portion of your portfolio is complex, takes time, and a lot depends on your personality.

But in general, you need a plan. My companies offer some of these products and I have compliance restrictions which keep me from getting too specific. The broader point, whatever your net worth, is to not accept this TINA fantasy. You have lots of alternatives to simply holding stocks. You may need professional help finding and accessing them, but they’re out there.

In fairness, there are hundreds of good advisors who generally do the same thing we do, just with their own flavor. Do your own search, but I would suggest avoiding advisors whose idea of portfolio construction is to buy and hold traditional stocks and/or ETFs in a TINA-like fashion.

I mentioned Ed Easterling above. If you are a serious investor and thinking about retiring, or simply want to understand the markets, you should read everything at Ed’s Crestmont Research site, plus his books, especially Unexpected Returns. Then, and only then, talk to your financial advisor. I’m really quite serious about that. Most advisors rely on some form of TINA. It’s hard to predict anything in this zero-rate, rising inflation world. But you still have some good choices.

Washington DC, Maine, and Colorado

My schedule is firming up somewhat. I plan to go to Washington DC for a few days before heading out to Bangor, Maine and then Grand Lake Stream for Camp Kotok, the annual fishing and economic fest. This year my youngest son Trey (who is now 26) will once again accompany me, which he has done for most years since he was 12. Then I will go to Steamboat, Colorado for a speaking engagement before heading back to Puerto Rico.

Trey will be coming to Puerto Rico in late July along with a friend he feels should “meet the parents.” Tiffani and my granddaughter Lively will show up a few days later. Shane and I are really looking forward to that. Her son Dakota has been with us for the last week or so.

I get asked all the time about what it’s like to live in Puerto Rico. I have to say that it is far better than I ever imagined it would be. The weather is typically fabulous, although it will get hot in August, but ironically nowhere near as hot as it does in Texas. I have met so many new friends. Shane is at the beach nearly every day snorkeling and getting her exercise. I have a great gym and I even get in a little golf. I am looking forward to traveling some again, but it is nice to come home to paradise.

And with that, let me hit the send button and wish you a great week. Take some time to meet with friends and avoid fewer people.

Your happy masks are no longer mandated here analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All