This July, we find ourselves looking back on a half a year of upside surprises. As the year started, we expected a better run than we had in 2020, which was a low standard to surpass. Rapid progress distributing vaccines followed, which has allowed for a potent and prolonged boost to economic activity.

The strength of demand has certainly caught the supply side of the economy off guard. Supply chain stress is elevated, as are inflation readings; we expect both to recede in the months ahead. The labor market recovery has not yet been as rapid as we had hoped, but each month, more people are going back to work.

The current combination of loosened restrictions, returning to work, and catching up on vacations and social gatherings during the peak season of summer likely mean we are at the apex of economic activity for the year. In the second half of the year, supply will catch up with demand, hiring will carry on, and the economy will continue its return to normalcy.

Influences on the Forecast

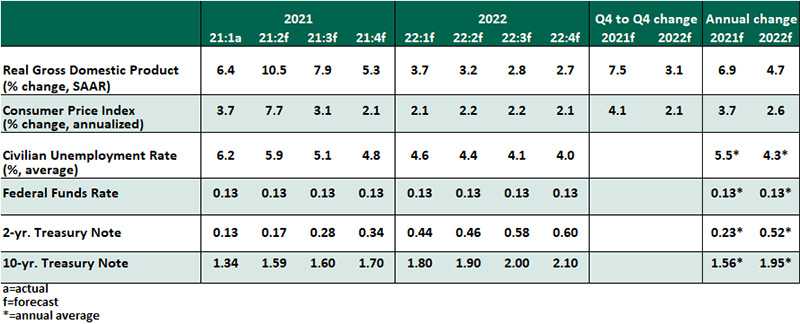

- The June Employment Situation Summary showed a gain of 850,000 jobs, an encouraging reading after lackluster job creation in April (269,000) and May (583,000). The unemployment rate rose slightly to 5.9%, and the labor force participation rate remained unchanged, reflecting ongoing labor supply constraints.

- Job and wage gains were strongest in the hard-hit leisure and hospitality sector as businesses respond to consumers’ higher demand for services.

- Expanded unemployment insurance has been blamed by some for the slow return to work, and 25 states have curtailed benefits. Initial evidence from those states is inconclusive and would not have appeared in the June employment report.

Benefits will expire nationwide in the first week of September, just as schools reopen.

- Inflation remains a topic of concern. The personal consumption expenditures price index grew 3.9% year-over-year in May, its highest rate since 2008. Excluding food and energy, prices rose by 3.4%. Upcoming readings of inflation should be lower as base effects of measurement during spring 2020 lockdowns fall out of the calculation. Consumers may experience higher prices in specific categories like travel and used car purchases, but not in ways we expect to be broad-based or sustained. Businesses are facing persistently elevated costs of labor and materials, which increase the upside risk to final prices.

- At the June meeting of the Federal Open Market Committee, the "dot plot" in the quarterly Summary of Economic Projections showed most committee members expect at least one Federal Funds Rate increase by the end of 2023. While not a binding commitment, the dot plot suggests Fed governors are becoming more confident in their expectations of continued employment gains and moderate inflation in the years ahead.

- Fear of repeating the 2013 “Taper Tantrum” is making the Fed cautious about a hurried announcement of reducing its asset purchase program. However, each month of job gains and elevated inflation will make it harder for the Fed to put off a change to its crisis-era levels of accommodation. We expect a plan to be announced in the months ahead, with tapering to begin in early 2022 and conclude by the end of next year.

- House prices continued their rapid appreciation, with the Federal Housing Finance Agency price index gaining over 15% year-over-year in April. However, monthly readings of purchase activity show the market is slowing: elevated prices are keeping shoppers away, while supply chain disruptions are slowing home builders’ delivery of finished homes.

- COVID-19 remains a concern, especially as the Delta variant of the virus spreads. Experiences in Israel and the U.K. suggest that vaccines are still effective against severe infections from this highly-contagious mutation. Efforts to continue inoculating as many people as possible remain necessary.

- Lingering uncertainty is evident in movements in the yield on 10-year U.S. Treasury bonds, which have recently fallen by 30 basis points. Some investors may be moving away from risk assets as the fastest interval of the recovery passes its peak, but slower growth is still growth. Renewed spread of COVID-19 is weighing on sentiment. Fixed income markets are also still digesting the shift in the Fed’s rate outlook.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.