The Metaverse: What Every Early-Stage Investor Needs to Know

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsYou may not be familiar with the term metaverse, but if you’ve been a consumer of popular books, movies and video games over the past 30 years or so, you probably are aware of the concept.

Consider films like The Matrix or Ready Player One, set in vast virtual realities in which people live, work and play. In Neal Stephenson’s 1992 science fiction novel Snow Crash, believed to be the first work to contain the word metaverse, online inhabitants make transactions using digital currencies, as hyperinflation has all but destroyed fiat currency. No, really, Stephenson wrote this in 1992.

The reason I’m bringing this up now is because, like a lot of the best ideas from sci-fi, the metaverse could soon make the leap from page to reality.

If you listened to Facebook’s earnings call this week, you know what I’m talking about. CEO Mark Zuckerberg must have mentioned the word at least 20 times in his effort to describe the social media company’s plans to begin developing an immersive 3D internet-like experience.

Facebook, which reported record quarterly revenue of $29 billion, is in a very good position to bring such a high-tech, high-concept experience to consumers. Besides having a staggering 2.9 billion active monthly users, the company already sells the Oculus virtual reality (VR) headset and Portal smart display screen. It also will be releasing smart glasses in partnership with Ray-Ban.

“This is going to be the successor to the mobile internet,” Zuckerberg told shareholders on Thursday.

“You’re going to be able to access the metaverse from all different devices and different levels of fidelity from apps on phones and PCs to immersive virtual and augmented reality devices.”

If Web 1.0 describes the earliest days of the internet with static, one-way sites; and if Web 2.0 describes the period of the internet that emphasizes interactivity and user-generated content; then what Zuckerberg and others envision can only be called Web 3.0.

Investing Early in Web 3.0

A true metaverse, as seen in Ready Player One or Tron, may still be a few years away. In the meantime, Facebook and other pioneers are busy laying the groundwork for a future that permits families, friends, coworkers and more to meet and interact in shared digital spaces that look and feel authentic.

I’m not just talking about VR headsets and video conferencing. Even in cyberspace, people will need real-world services, from entertainment to finance. In the coming years, I imagine companies as various as Amazon, Netflix, DoorDash and Robinhood all rolling out their own contributions to a shared metaverse. Digital currencies will also be essential, which should benefit crypto miners and brokers.

With that in mind, I urge investors to keep an eye on this space.

Granted, that’s often hard to do, especially since everyday investors generally don’t have access to private, early-stage equity.

Snoop Dogg was among the earliest Robinhood investors Photo by: TechCrunch | Attribution 2.0 Generic (CC BY 2.0) |

Take Robinhood, for instance. Shares of the commission-free trading app favored by millennials began trading on Nasdaq this week after years of speculation. Before that, participation was restricted to angel investors, venture capitalists and other accredited investors who must meet certain capital requirements.

That includes rappers Snoop Dogg and Nas, both of whom invested in Robinhood seven years ago, according to BNN Bloomberg’s Jon Erlichman. At the time, the company was worth $62 million. Today, it’s valued at $32 billion, an incredible 516-fold increase.

Think about it: Only in America can a twentysomething Bulgarian immigrant (Robinhood founder Vlad Tenev) launch an app that disrupts the global brokerage industry. Only in America can two men whose childhoods were spent on the streets, with numerous run-ins with the law, become fabulously successful and wealthy through not only their musical talents but investment decisions.

2021 on Track to Be a Record Year for IPOs

This brings me to a topic I’ve written about before: the dearth of new public listings.

The sad truth is that, instead of having to deal with the (growing) mountain of rules and regulations that publicly traded firms must comply with, many companies have just chosen to stay private for longer. And once companies finally get around to tapping public markets, they may have already gone through their strongest period of growth. Robinhood was about eight years old at the time of its initial public offering (IPO), which is slightly less than the median 12 years old that most venture-backed tech companies were when they listed.

This hurts retail investors and families more than anyone else. Returns on private equity can often be very high, but again, everyday Americans generally don’t have access.

Fortunately, this trend appears to be reversing. As of July 29, there were 261 new listings so far in 2021, which is the most of any full year going back to 2014, according to Renaissance Capital. Meanwhile, companies have raised a record $94.2 billion, an increase of more than 20% from 2020.

The reason? In my opinion, Jay Clayton deserves a lot of the credit.

Clayton was one of former President Donald Trump’s best picks to head a federal agency. The Securities and Exchange Commission (SEC) chairman, who resigned in December 2020, made it his mission to encourage more companies to list on public exchanges earlier in their lifecycles.

He must have done something right.

“That bothers me,” Clayton said in 2018, referring to the lack of market availability. “If that trend continues, a much more select group is participating in the growth of the economy.”

It’s Not too Late to Be Early

I believe one of the most attractive early-stage investments remains cryptos, particularly Bitcoin and Ether, both of which are still in their infancy with incredible upside potential.

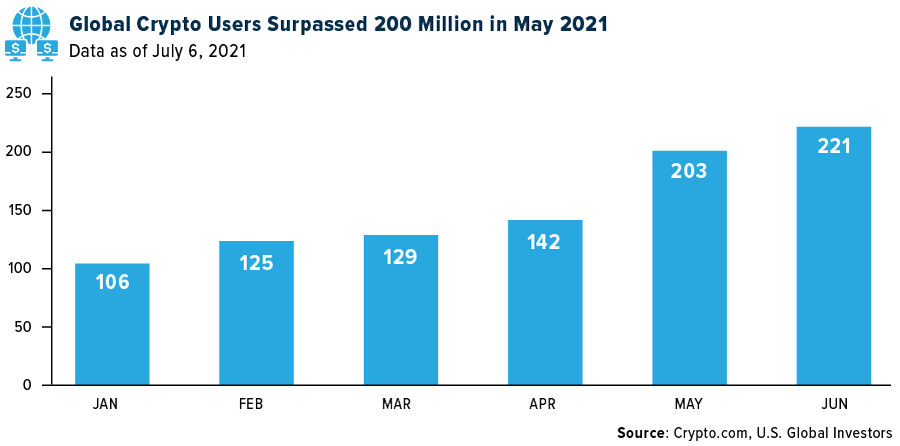

Others have the same idea, apparently. The number of people who use cryptocurrencies shot past 220 million for the first time, according to research by Crypto.com. As of the end of June, as many as 221 million people around the world were participating in the crypto ecosystem, including trading, investing and making transactions in Bitcoin, Ether and other digital coins.

What’s more, the pace of adoption appears to be quickening. Crypto.com observes it took only four months for the number of crypto users to double from 100 million to 200 million. To compare, it took nine months for use to jump from 65 million people to 100 million people.

And it’s not just individual investors who are driving adoption. Many companies have reported holding Bitcoin on their balance sheets, among the largest being Michael Saylor’s MicroStrategy (holding more than 105,000 BTC at a dollar value of $4.1 billion), Tesla (43,200 BTC/$1.5 billion) and Square (8,027 BTC/$220 million).

Speaking of Michael Saylor…

I’m pleased to share with you that the MicroStrategy founder and CEO will join me in my next webcast on gold and Bitcoin. Many slots have already been taken! To get the link to book your spot for this exclusive conversation, email me at [email protected] with subject line “Michael Saylor webcast.” Demand has been higher than even I anticipated, so don’t hesitate to register!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.36%. The S&P 500 Stock Index fell 0.37%, while the Nasdaq Composite fell 1.11%. The Russell 2000 small capitalization index gained 0.75% this week.

- The Hang Seng Composite lost 4.98% this week; while Taiwan was down 1.85% and the KOSPI fell 1.60%.

- The 10-year Treasury bond yield fell 5 basis points to 1.224%.

Airline Sector

Strengths

- The best performing airline stock for the week was Wizz Air, up 8.8% According to Morgan Stanley, most airlines have already seen a notable pickup in corporate travel from -80% versus 2019 in April to -60% in May and -40% to 45% projected for September. Furthermore, airlines expect the momentum to continue picking up as the year progresses as internal surveys show that permanent substitution of corporate travel will be as little as 5%.

- Airline earnings continue to come in ahead of expectations. Alaska Air reported second quarter earnings per share (EPS) of ($0.30), which is above consensus of ($0.44). Revenues were $1,527 billion, above consensus of $1,516 billion. Sun Country reported second quarter EPS of $0.07, above consensus of $(0.14). Allegiant reported second quarter EPS of $3.46, above consensus of $2.88. Spirit Airlines reported second quarter EPS of $(0.34), above consensus of $(0.79). These earnings surprises can be contributed to strong leisure travel demand.

- JetBlue Airways announced a multi-year extension of its co-branded credit card agreements with both Barclays and Mastercard, a partnership that is expected to expand the airline’s consumer and small business credit card portfolios. In the U.S., Barclays has been the exclusive issuer and Mastercard has been the exclusive network of the airline’s co-branded credit card program since 2016. Analysts believe this is a meaningful development as the airline is renewing the deal with much better economics.

Weaknesses

- The worst performing airline stock for the week was Hainan Air, down 11.7%. Global capacity is indicated to be down 43% in July, 37% in August and 30% in September versus 2019 levels. These values were 1% lower than the previous week. The delta variant continues to threaten the removal of international travel restrictions and the demand for travel to more affected regions.

- SkyWest’s stock is down 25% and is among the worst performers despite lower earnings leverage to fuel/fare volatility. Concerns around United Airline’s plan to reduce its single-class/50-seat RJs and potential for medium/longer-term pilot supply issues are key reasons for the selloff.

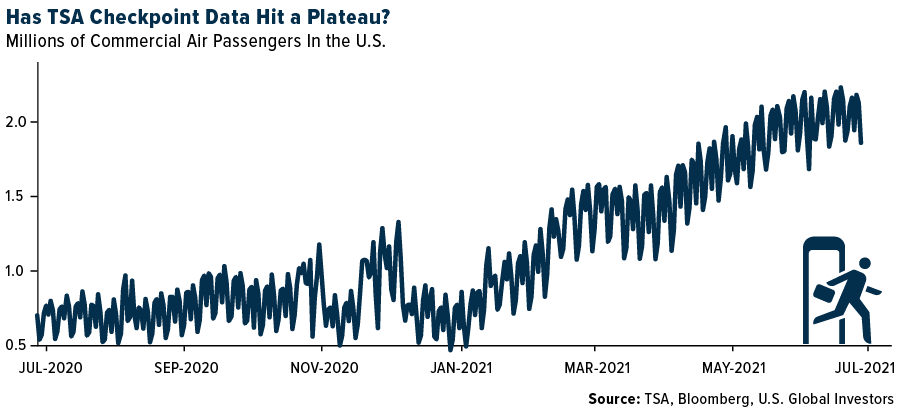

- Last week, system net sales fell 46% versus 2019, which was better than last week's down 50%, but slightly below the prior trend of down 42%. Similarly, domestic tickets sold grew by 12%, also better than up 8% last week, but below the growth of 16% the prior four weeks. TSA checkpoint data is showing a plateau, as seen in the chart below, although room for continued growth still exists as we move into the holiday travel season later this year.

Opportunities

- According to Morgan Stanley, travel budget recovery has slowed down, but the U.S. should be leading the way in 2022. Travel budgets are expected to be down an average of 39% versus 2019 in the second half compared to the 57% drop seen in the first half of the year. The pace of recovery will increase in 2022 with budgets expected to be down only 17% on average. In addition, while 62% of European respondents expect cuts of greater than 50%, only 45% of U.S. counterparts expect the same.

- According to Morgan Stanley, passenger volumes continue to deteriorate as well, though expectations are for higher passenger volumes, with the U.S. leading the way in 2022. In addition to travel budgets, the group’s latest data suggests 2022 volumes versus 2019 volumes will be down 21%, a 3% decrease versus March. Europe is the laggard with 57% expecting a decline of 30-50% compared to just 25% of U.S. respondents anticipating the same.

- Ryanair presented a bullish message about growth opportunities in Europe this week, as other carriers retrench. The company announced 10 new bases across the Baltics, Scandinavia, Croatia, Italy, France, Greece, and Morocco. It also signed extensions of long-term deals at some of its existing large bases. Ryanair aims to increase its capacity at primary airports from 70% of departures to 80%.

Threats

- In Europe, according to Morgan Stanley, there is no anticipated recovery in corporate air travel in Europe prior to 2023/2024, and higher environmental concerns on travel support this thesis. All in all, weaker demand and a 27% shift of travel into virtual events could negatively impact legacy carriers.

- JetBlue’s newly introduced near-term, and 2022 cost outlook are looking worse than expected. While headwinds are tied to inflationary pressures for labor, and airport costs are consistent with commentary from the rest of the industry, these have the potential to abate over the medium-term.

- The U.S. will not lift international travel restrictions at this time due to the COVID-19 Delta variant and the rising number of U.S. coronavirus cases.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 3.1%. The best relative performing country in Asia this week was Indonesia, losing 0.40%.

- The Turkish lira was the best performing currency in emerging Europe this week, gaining 1.6%. The Philippine peso was the best performing currency in Asia this week, gaining 0.56%.

- Economic growth in the Eurozone came in better-than-expected. GDP expanded by 2% in the second quarter after contracting 0.30% in the first quarter, ending a double-dip recession. The second-quarter growth figure was stronger than the 1.5% foreseen by market analysts.

Weaknesses

- The worst performing country in emerging Europe for the week was Romania, losing 0.50%. The worst performing country in Asia this week was Hong Kong, losing 5.3%.

- The Romanian leu was the worst relative performing currency in emerging Europe this week, up slightly by 0.90%. The Pakistani rupee was the worst performing currency in Asia this week, losing 0.11%.

- China’s recent regulatory crackdowns on a range of local private companies have triggered a heavy sell-off in top Chinese technology stocks. The repercussions have also started seeping into the Asian nation’s currency and debt markets.

Opportunities

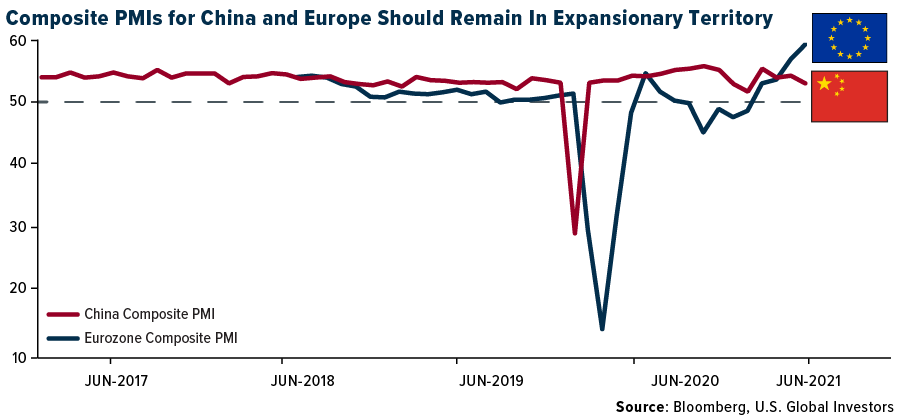

- July purchasing managers’ index (PMI) data will come out next week. Recently, China’s Service and Manufacturing PMIs weakened moderately but these numbers should remain in expansionary territory, pointing to a continued market recovery. In Europe, PMIs recently strengthened as well, and likely won’t move by much. Summer travel trends supported the Service PMI in Europe as many European countries allowed passengers with the vaccine to travel freely between the member states.

- Singapore plans to relax more coronavirus curbs, including starting to allow quarantine-free travel in September. This will mark the first time the country sets a timeline to reopen borders that have been mostly shut for more than a year. The Southeast Asian city-state expects 80% of its population to be fully vaccinated by then.

- China is expected to release strong exports next week with trade balance increasing to a surplus of 52 billion in July from 51.53 billion in June. Easing global lockdowns have helped spur demand for Chinese goods.

Threats

- The International Monetary Fund (IMF) on Tuesday maintained its 6% global growth forecast for 2021, upgrading its outlook for the United States and other wealthy economies but cutting estimates for developing countries struggling with surging COVID-19 infections. Developed markets have better access to vaccines and continued fiscal support, while emerging markets face difficulties on both fronts, the IMF said in an update to its World Economic Outlook.

- China’s regulatory crackdown on the technology sector continues. Beijing imposed a ban on education companies from making profits or going public. Separately, China's market regulator announced a ban on Tencent from engaging in exclusive music copyright agreements and fined the company for anti-market practices. Recently, China weighed heavy penalties on Didi over its U.S. listing. This crackdown has contributed to significant underperformance of the Hang Seng Tech Index since February.

- Asia’s coronavirus situation continues to worsen. South Korea announced it will raise social distancing alerts to the second-highest level across most of the country this week. Sydney's lockdowns are set to be extended in some areas beyond Friday. Singapore continues to battle separate clusters after tightening restrictions last week. In Indonesia, however, the government has eased some restrictions.

Energy and Natural Resources Market

Strengths

- Aluminum was the best performing commodity this week, gaining 4.69%. Aluminum supplies from China are being reduced by electricity rationing and in Canada due to labor strikes. Retail fuel margins are increasing. U.S. fuel margins are at 26.6 cents per gallon, up from 24.7cents per gallon last quarter. This is positive for companies that have a large downstream presence such as Exxon and Chevron.

- According to the World Steel Association, global crude steel production rose 12.3% to 167.9 million tons in June. China produced 55.9% of global crude steel last month, with its output climbing 2.5% to 93.9 million tons. Higher steel production was also driven by increases in Spain (up 56.6%), France (up 54.8%), Japan (up 44.3%) and Canada (up 43.0%).

- Western Pacific lumber pricing saw its first increase since May as escalating wildfires, coupled with Canfor's production curtailment, boosted market sentiment. Lumber ended the week up 1% at $490, down 55% relative to the second quarter, and down 16% year-over-year. However, lumber is up 95% so far this year.

Weaknesses

- Iron ore futures were the worst performing commodity for the week, down 5.64%. China is pushing to curtail steel production, one of its dirtiest polluting industries, to meet emissions goals. Russian steel companies recently had a 15% export duty imposed on them by the government. The export duty is a temporary measure running from August 1 until December 31. The Russian government is considering additional taxation on the sector and is currently discussing the matter with these companies.

- Global benchmark phosphate prices were down slightly this week as the market is in a seasonally slower period for demand. Urea prices have also softened across major regions.

- Analyst checks with distributors suggest that the U.S. residential solar industry has started to face labor shortages in July, which could potentially impact project economics or leave some demand on the table in 2021. Demand is still healthy, up over 25% year-to-year in 2021, despite labor and component shortages.

Opportunities

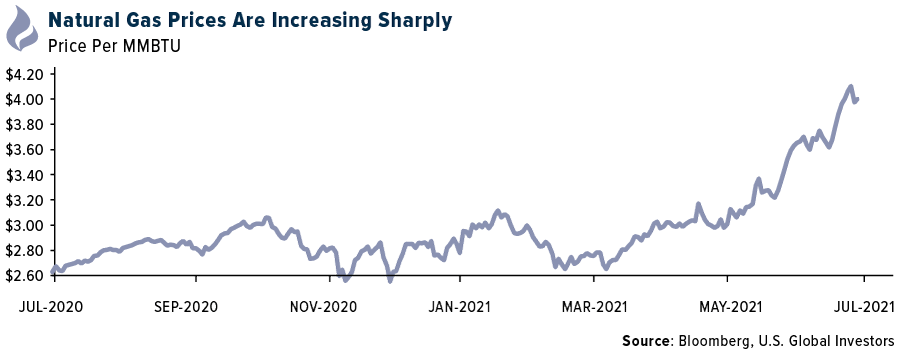

- Henry Hub natural gas spot prices have surged to $4 per million Btu in recent days on extremely bullish weather outlooks. Further price-induced demand headwinds are necessary to keep year-end U.S. natural gas inventories at normalized levels, both this year and next. Warm weather continues to drive natural gas prices higher. Demand has increased while the supply response remains subdued. Europe is also facing natural gas shortages with strong demand currently limiting what must be stored for the winter heating season. Cargos of LNG are hard to acquire as well.

- Aluminum is heading for a seismic shift as a long-running supply glut starts to fade, writes Bloomberg, setting the stage for shortages and a price rally that could run for years. Demand is set to surge on the back of climate-change investment, and mega-producer China -- which accounts for more than half of global output -- is cracking down on smelting to reduce pollution and meet green targets. Aluminum has already jumped 26% this year to about $2,500 a ton.

- The oil industry is looking to boost investor returns with increased dividends and some stock buy backs too. Royal Dutch Shell raised its dividend nearly 40% and will buy back $2 billion in shares. BP Plc and Equinor ASA have recently boosted dividends, too. Chevron has a relatively strong balance sheet and CEO Mike Wirth has expressed a willingness to begin buying shares at some point. However, he is also being cautious, insisting that any repurchase program must be sustainable through the ups and downs of the crude price cycle. Chevron’s tone seems to reflect that it sees an uncertain future regarding climate change legislation likely on the political agenda.

Threats

- The Canadian union Unifor said on Sunday that about 900 workers started a strike action at global miner Rio Tinto's operations in the western Canadian province of British Columbia. Unifor issued a 72-hour strike notice on Wednesday after nearly seven weeks of unproductive talks over proposed changes to workers' retirement benefits and unresolved grievances. The company said that required staff and employees are now taking on operational duties to ensure the smelter and powerhouse continue to function safely.

- The petroleum industry is still extremely important to our current and near future energy mix, but headlines saying that Rio Tinto wrote a $2.4 billion check for a new lithium mine to start construction next year in Serbia, has to give one some pause. This is a potential threat to current market-leading producers of lithium, such as Albemarle and SQM. However, all the new supply will likely be absorbed by electric vehicles as mother nature turns the heat up on the planet.

- Ethane, a key component in plastic production, is trading at a nearly two-and-a-half-year high in the U.S. The higher price of ethane also threatens to drive up plastics prices, adding to widespread concerns about inflation. Supply trends across the various grades of polyethylene have been relatively tight.

Domestic Economy and Equities

Strengths

- According to FactSet's latest Earnings Insights, the blended growth rate for second quarter S&P 500 earnings is 74.2%, up over 1% from the end of the last quarter. The report shows that 88% of companies have surpassed consensus earnings per share (EPS) expectations, ahead of the one- and five-year averages of 83% and 75%, respectively.

- July’s consumer confidence came in at 129.1 versus the consensus for 124.0, which is slightly above June's upwardly revised 128.9. This is the highest headline reading since January 2020.

- Advanced Micro Devices, a semi-conductor producer, was the best performing S&P 500 stock for the week, increasing 15.4%. Chip makers had a strong trading session on Thursday, as a global semiconductor shortage is allowing chip makers to essentially sell everything they can produce.

Weaknesses

- Amazon reported second quarter revenue that came in 2% below Wall Street estimates, while operating income missed by 1%. The company also guided for third quarter revenue and operating income well below consensus.

- June new home sales came in at a 676,000, down 6.6% from May's 724,000 pace and below consensus for 800,000. On a year-over-yar basis, new home sales are down 19.4%, the lowest monthly level since April 2020.

- Citrix System, a software company, was the worst performing S&P 500 stock for the week, losing 12.3%. Shares declined after the company released disappointing second quarter results.

Opportunities

- The International Monetary Fund (IMF) on Tuesday maintained its 6% global growth forecast for 2021, upgrading its outlook for the United States and other wealthy economies but cutting estimates for developing countries struggling with surging COVID-19 infections. "Close to 40 percent of the population in advanced economies has been fully vaccinated, compared with 11 percent in emerging market economies, and a tiny fraction in low-income developing countries," Gita Gopinath, the IMF's chief economist said.

- Final Markit U.S. Manufacturing PMI data will be released soon for July. The number will likely come in at 63.1, pointing to strong recovery in the U.S. supported by massive fiscal and monetary stimulus.

- The July unemployment rate will be released next week. Bloomberg economists predict unemployment to decrease to 5.7% in July from 5.9% in June. The rate will most likely continue to decline to pre-pandemic levels over the coming months.

Threats

- The Federal Reserve on Wednesday signaled that the countdown has begun on scaling back its massive support for the U.S. economy, while giving no clear hint about when the tapering might be announced. The Fed has been buying $120 billion a month in mortgages and Treasuries as part of a strategy to keep U.S. interest rates low. The central bank said last December it wouldn’t begin to wind down its massive bond-buying program until “substantial” progress had been made toward its goals of low unemployment and stable inflation.

- The United States is not yet ready to lift its international travel restrictions due to concerns over the contagious Delta variant, officials said Monday. The highly contagious Delta strain has spread across at least 100 countries of the world. It is now the dominant strain in the U.S., accounting for more than 80% of infections and a surge of deaths among people who had not yet received their vaccine.

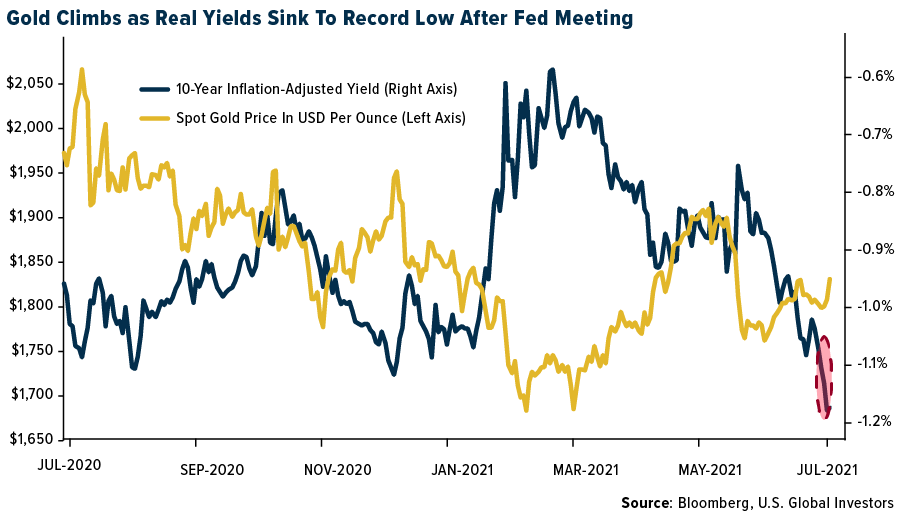

- U.S. real yields hit a record low on growth concerns. The Financial Times highlighted negative real yields in the major Western markets with the U.S. 10-year Treasury sinking to -1.127% on Monday, while the Eurozone 10-year real interest rate swap traded at a record low of -1.65%.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Shield Network, rising over 5,000%.

- The payments team at Amazon is exploring letting customers use cryptocurrencies to pay for their orders, writes Bloomberg, a development that’s roiling digital currency markets. Last week an Amazon job posting was published seeking a “Digital Currency and Blockchain Product Lead.”

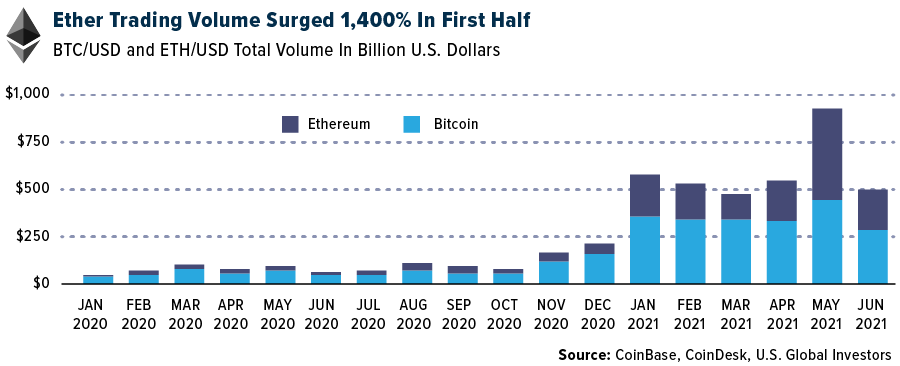

- In the first half of the year, Ether trading volume surged 1,400% as institutions took exposure, reports CoinDesk. In fact, the Ether market grew three times faster than Bitcoin in the first six months of the year. As seen in the chart below, Ether also outperformed Bitcoin in terms of volume growth and price performance, similarly outshining the S&P 500 and gold in price performance.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Capital X Cell, down 98.93%.

- According to a former Bitcoin ETF expectant, the United States SEC may not approve a Bitcoin exchange-traded fund until 2023, writes CoinTelegraph. Speaking to Business Insider, co-founder of investment firm Wilshire Phoenix, William Cai, remarked that 2022 and 2023 are the earliest possible times for the SEC to greenlight a BTC ETF. Several Bitcoin ETF hopefuls currently have filings with the SEC, including fund management outfit Global X, which submitted earlier in the month, the article continues.

- According to a Twitter post on Tuesday, a “significant” bug, with the potential to expose users’ true transactions, has been spotted in the privacy-centric cryptocurrency Monero (XMR), writes CoinDesk. Identified in Monero’s decoy selection algorithm, the bug occurs when a user spends their funds received in a transaction before roughly 20 minutes has passed. As the article goes on to explain, users may avoid the bug altogether by waiting one hour or more before spending their newly received Monero until a fix is implemented in a future wallet software update.

Opportunities

- As reported by CoinTelegraph, there has been installation of over 10,000 new crypto ATMs worldwide in 2021, a spike of 71.73%. The United States is leading this space, having installed nearly 48 ATMs per day.

- Bitcoin mining facilities are setting up shop in Texas, writes CoinTelegraph, and many are saying the Lone Star State could be the idea location. Texas’ deregulated power grid, increasing renewable energy and political leaders that are publicly pro-crypto have caused a number of mining companies to head to the second-largest state in the U.S.

- Goldman Sachs has filed an application with the U.S. SEC for an ETF that would offer exposure to public companies in decentralized finance (DeFi) and blockchain around the globe, reports CoinDesk. According to the filing, the fund would invest at least 80% of its assets into companies that advance blockchain technology and the digitization of finance.

Threats

- According to the Senate’s bipartisan infrastructure deal, stricter rules could be imposed on cryptocurrency investors to collect more taxes to fund a portion of the $550 billion investment into transportation and power systems, reports Bloomberg. A summary of the plan shows that the provisions would raise an additional $28 billion from cryptocurrency transactions.

- On Monday, Bloomberg reported that Tether is being investigated by the U.S. Department of Justice for possible offenses conducted years ago. The price of Bitcoin fell on the day in reaction to the news, to which a request for comment was not immediately returned by Tether. As CoinDesk reports, Tether (which administers USDT – the crypto market’s largest stablecoin), has long been dogged by accusations of murky banking relationships.

- Companies such as Tesla and MicroStrategy that have emerged as some of Bitcoin’s biggest backers will have to reckon with their digital holdings in earnings reports next week, writes Bloomberg, after the price of the token tumbled 41% in the second quarter. “There will be repercussions from the volatility of the price in the quarter,” said Jack Ciesielski with R.G. Associates.

Gold Market

This week spot gold closed the week at $1,814.19, up $12.04 per ounce, or 0.67%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.27%. The S&P/TSX Venture Index came in up 2.56%. The U.S. Trade-Weighted Dollar slid 0.93%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jul-26 | Hong Kong Exports YoY | 24.0% | 33.0% | 24.0% |

| Jul-26 | New Home Sales | 796k | 676k | 724k |

| Jul-27 | Durable Goods Orders | 2.2% | 0.8% | 3.2% |

| Jul-27 | Conf. Board Consumer Confidence | 123.9 | 129.1 | 128.9 |

| Jul-28 | FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Jul-29 | Germany CPI YoY | 3.2% | 3.8% | 2.3% |

| Jul-29 | Initial Jobless Claims | 385k | 400k | 424k |

| Jul-29 | GDP Annualized QoQ | 8.4% | 6.5% | 6.3% |

| Jul-30 | Eurozone CPI Core YoY | 0.7% | 0.7% | 0.9% |

| Aug-1 | Caixin China PMI Mfg | 51.0 | -- | 51.3 |

| Aug-2 | ISM Manufacturing | 60.8 | -- | 60.6 |

| Aug-3 | Durable Goods Orders | -- | -- | 0.8% |

| Aug-4 | ADP Employment Change | 650k | -- | 692k |

| Aug-5 | Initial Jobless Claims | 380k | -- | 400k |

| Aug-6 | Change in Nonfarm Payrolls | 888k | -- | 850k |

Strengths

- The best performing precious metal for the week was silver, up 1.25%. Silver led the precious metals rally this week following the Federal Reserve meeting. Gold also rose as real yields held near a record low and the U.S. dollar eased after the Fed said that while it’s moving closer to reducing stimulus, the U.S. central bank wants to see more progress toward its goals first. Chairman Jerome Powell commented that there is still some way to go to meet the conditions for tapering and that officials discussed how to scale back bond buying when the time came. Powell spoke after the Federal Open Market Committee (FOMC) held interest rates near zero and maintained asset purchases at $120 billion a month.

- Barrick Gold has been awarded four exploration licenses for 19 blocks following its participation in the International Bid-Round led by the Egyptian government for exploration of gold and associated minerals in the highly prospective Eastern Desert region of the country. The Eastern Desert is part of the Proterozoic Arabian Nubian Shield, which hosts the giant Sukari deposit and numerous other gold occurrences, but which has seen no recent systematic exploration. Barrick intends to work closely with the Egyptian Mineral Resource Authority and other participating exploration and mining companies, over the period of a year, to finalize the terms of Egypt’s exploitation license agreement which will apply to the industry.

- Agnico Eagle Mines reported earnings per share (EPS) of $0.69, ahead of consensus of $0.59. Production of 526,000 ounces was above consensus as well. Slightly better results were reported at the Meliadine mine (less maintenance interruption) and Pinos Altos (better plant performance and higher tons from the Sinter deposit).

Weaknesses

- The worst performing precious metal for the week was platinum, down 1.13%, with palladium also negative for the week. Exchange-traded funds (ETFs) cut their holdings recently, bringing this year's net sales to 6.93 million ounces, according to data compiled by Bloomberg. The sales were equivalent to $57.2 million. Total gold held by ETFs fell 6.5% this year to 100.1 million ounces, the lowest level since May 13. It’s notable that holdings in SPDR Gold Shares have ebbed to a two-month low, and the loss of a few more tonnes would drive it to the lowest level in well over a year.

- Kinross Gold posted lower production at higher costs than consensus in the second quarter leading to an earnings and cash flow miss. Production of 538,000 ounces was 5% lower than consensus while cash costs of $830 were 9% higher than consensus. EPS of $0.12 per share was slightly below consensus. The company increased cash cost by 5% due to the expected downtime at Tasiast in the second half along with inflationary pressures.

- IAMGOLD announced its second quarter 2021 production, a reduction to its 2021 guidance and a significant capex increase at the Côté gold project. Second quarter gold production came in at 139,000 ounces, below consensus of 157,000 ounces, and below first quarter production of 156,000 ounces. The miss was driven by lower-than-forecast production at Rosebel, which produced 25,000 ounces, and was slightly offset by production of 106,000 ounces at Essakane.

Opportunities

- Northern Star outlined a five-year plan to increase production by 25% to 2 million ounces per year by fiscal year 2026. The improved production outlook is largely driven by a flagged 45% production increase at Kalgoorlie Production Centre over the next five years. Growth capex was also provided for fiscal year 2023 (A$425m) and fiscal year 2024 (A$380m) which are higher than previous forecasts by 84% and 230%, respectively.

- Arizona Metals Corp. released another round of drilling from the silver/zinc zone at Kay. Four holes were released, including Hole 27. Hole 27 is outside the historic Exxon resource, the deepest hole drilled to date by the company, extending the silver zone depth by 20%. Also, the average drilled grade of the silver zone has increased by 9%, showing grades are improving with tighter spacing.

- Egyptian billionaire Naguib Sawiris has founded a $1.4 billion fund, La Mancha Fund, for his gold mining investments and new opportunities in the sector, the Financial Times reports, citing an interview with Sawiris. The fund will focus on gold mining and will invest in battery metals necessary for electric cars. The fund will be “deep value, long-only,” and open to new investors, Sawiris explains.

Threats

- First Quantum reported an EPS miss on taxes being higher than expected. The stock may be weak due to legal challenges in Panama. Cobre Panama pays a 2% royalty versus the current Panamanian Mining Code of 5% on base metals. Panama has set up a commission to negotiate the mine’s current fiscal regime.

- Golden Star cuts its yearly production forecast after announcing second quarter results. Gold production was cut from 165,000-175,000 ounces to 145,000-155,000 ounces in 2021.

- The recent rally in Bitcoin has presented a challenge to gold, as it is viewed as an alternative asset class. Bitcoin rallied around 20% over the past week as Amazon is looking into accepting payment from its customers in cryptocurrencies as well as hiring a crypto team.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All