I started contemplating a vehicle purchase at the start of the year when my growing children began to have trouble fitting their legs into the back seat of our compact second car. Headlines of rising used car values caught my attention, so I shopped around for bids on my compact car. I was stunned to get a trade-in offer above what I had paid for the car three years ago. I took the occasion to upgrade to a new, larger vehicle—for which my options on dealer lots were limited, and I paid dearly.

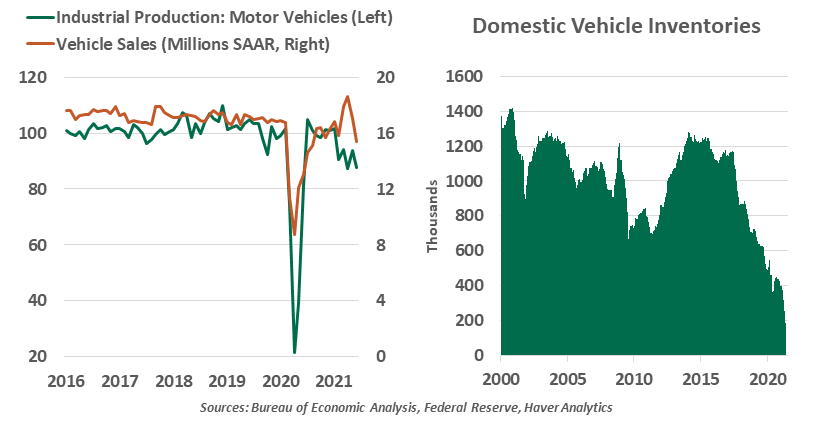

While some of the ups and downs of reopening after the pandemic were foreseeable, few predicted the disruption experienced by the automotive industry. As the economy shut down last year, auto sales plummeted, often for the simple reason that dealerships were closed. Drivers had fewer places to go for work or leisure; auto insurers gave rebates as accident rates fell in light of reduced driving. Rental car agencies culled their fleets as travel stopped, flooding the market with gently used cars. The outlook was grim for auto manufacturers, and they reduced their production accordingly.

But the recovery that began last spring was rapid and had unusual characteristics. Social distancing made driving more appealing than public transit, and families moving into single family homes to gain space for remote work had a greater need for cars than before the pandemic. Stimulus payments gave consumers money that could help with a major purchase like a car. Demand rebounded, draining inventories.

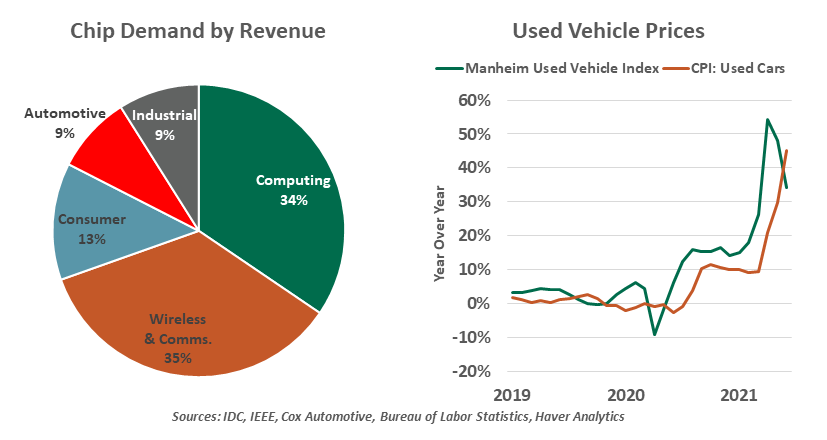

Automakers and their suppliers could not adjust their output quickly enough. When auto sales were soft, semiconductor makers diverted their shipments to other technology products that were in high demand, like consumer electronics. Chips may be small in size, but without them, vehicles cannot operate. From visible in-cabin comforts to hidden safety and engine control modules, even the most basic vehicle is a high-tech product. Hybrid drivetrains and electric vehicles require even more technology.

Throughout this year, chip shortages have caused manufacturers to idle plants, with some even going so far as to build partially-finished vehicles that are set aside, waiting for the necessary electronics to finish the product. Automakers’ industrial production remains well below potential.

|

Low inventories have not cooled demand for cars.

|

Vehicle electronic components use relatively simple, older chip designs. Processors do not need to be ultra-compact and power efficient, like those used in smartphones, nor as high-powered as those in desktop computers and servers. Attention in the semiconductor industry is rightly focused on expanding capacity, but new investment will likely be steered toward building newer types of chips. For automotive needs, existing chip fabricators are working at full capacity, with producers forecasting they will be caught up with automotive demands within a month.

While they wait, dealers have been left with less supply. A drive past a dealership will reveal cars parked less densely and back lots nowhere near full. But cars are still being sold. Demand is resilient, and with inventories lower, sellers have more pricing power. Some dealers are now questioning their old practice of carrying as much inventory as they could fit, which left dealers paying high financing costs for their unsold vehicles. Consumers now start (and some even complete) their shopping online and can see exactly which models a dealer has in stock; there may be less need for a dealer to have something for everyone who walks in the door.

Lower supply leads to higher prices, a story that is clearest in the used car market, where values have surged to new highs this year. It now appears that high prices are cooling activity, and measures of used vehicle values are beginning to decline.

Inflation remains a topic of concern, with the U.S. Consumer Price Index (CPI) growing at rates not seen since 2008. As we have discussed, for the past three months, the outlier surges in new and used car prices and car rental have driven a substantial portion of each month’s inflation. Movements in the Manheim Used Vehicle Value Index lead changes in the CPI measurement of used cars by a month or two; with Manheim having peaked in June, we expect a fall in used vehicle CPI to follow soon. Greater production of new vehicles will add supply and lower the prices of new cars and rentals.

|

This year’s auto market disruptions will fade, but more adaptation lies ahead.

|

We continue to believe the current dislocations in the automotive sector will fade. Chipmakers are catching up with shortfalls; new car inventories and rental fleets will be replenished; the used car market will cool down. In the longer run, however, the industry is in the midst of substantial changes. The current manufacturing disruption only magnified a fault line that emerged in events like the trade wars: supply chains are fragile and overextended, and manufacturers are reconsidering how best to produce their vehicles.

The vehicles themselves are changing as more electric vehicles (EVs) find mainstream adoption from both personal and fleet buyers. EVs have simpler drivetrains than can simplify manufacturing. However, they have a high reliance on batteries and semiconductors, heightening the risk of supply chain disruptions in these hot sectors. The latest bipartisan infrastructure proposal includes funding to build a nationwide network of EV charging stations, which will reduce a barrier to adoption—if manufacturers are ready to meet the demand.

In second quarter earnings calls, automakers warned of continued idling of plants and low inventories for the rest of the year. The disruption is lasting longer than we had hoped, but it will pass. Auto shoppers have always needed patience, and now is no exception. Anyone considering a purchase this year might do well to wait, as long as your family still fits in your current vehicle.

Don’t miss our latest insights:

The Fed Stays the Course

Britain Breaks Its Word

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.