How to Participate in the Coming Electric Vehicle (EV) Boom

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn 1905, the first gas pump appeared in St. Louis, Missouri, to meet the fueling demands of a rapidly growing number of motorists. Before this innovation, which resembled a handheld water pump, people topped off their cars with gasoline they purchased in cans at the pharmacy or hardware store.

It wouldn’t be until 1913 that the first purpose-built, drive-up gas stations began popping up in cities all over the U.S.

As of this year, the country has more than 121,000 convenience stores that sell motor fuels. That figure doesn’t include the tens of thousands of supermarkets, kiosk fueling sites and other locations that also sell fuel.

But internal combustion engine (ICE) vehicles aren’t the only ones on the road today. By one estimate, there are some 26,000 electric vehicle (EV) charging stations open to the public in the U.S. right now, and if President Joe Biden gets his way, we’re going to need a whole lot more.

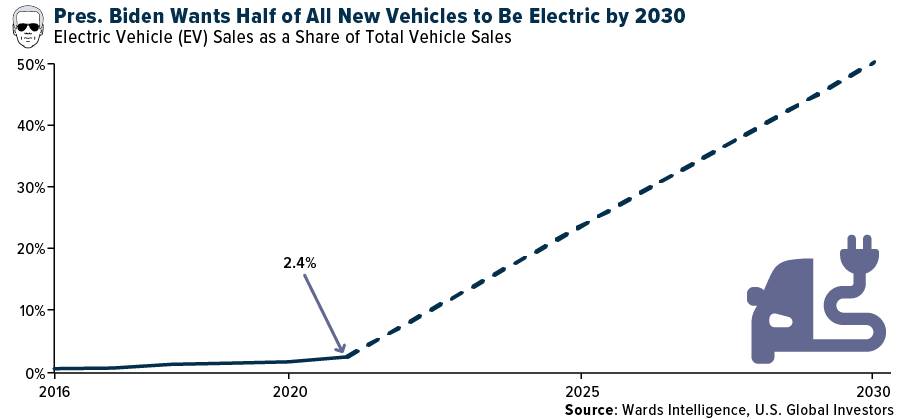

Half of All Vehicle Sales to Be Electric by 2030?

Five hundred thousand more, to be more precise. This week, Biden set a goal for 50% of all vehicles sold in the U.S. to be “battery electric, plug-in hybrid electric or fuel cell electric” by the end of the decade.

That’s a tall order. Today in the U.S., EV sales make up only 2.4% of all vehicle sales, according to Wards Intelligence. Billions of investment dollars have flowed into EV manufacturers—as much as $28 billion in 2020 alone—and many billions more will need to be invested to meet Biden’s goal.

It’s not impossible, though. In a joint statement following the president’s announcement, General Motors (GM) and Ford committed to achieving 40% to 50% of annual vehicle sales to be EV by the end of the decade. GM believes it can reach a “zero-emissions, all electric future” by 2035. Most carmakers, in fact, are making similar pledges.

A Boon to Metals and Mining

The question investors might have in light of this news is how to position their portfolios. Investing in select carmakers looks attractive—we invest in a few ourselves, including Tesla and Volkswagen—but my preferred way to get exposure is with the commodity producers supplying the metals and other materials that will be required to ramp up EV production.

The metal that most people think of when it comes to EVs is lithium or copper, the latter of which I’ve written about numerous times. But it’s important not to overlook other key metals. According to BloombergNEF, global nickel and aluminum demand could grow as much as 14 times between now and 2030, phosphorus and iron 13 times.

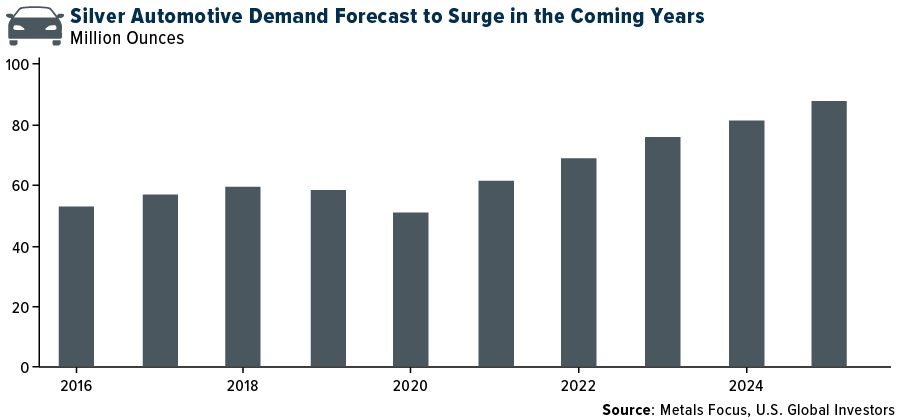

Silver demand should also benefit over the coming years. As the most conductive metal, silver will be increasingly used in nearly all components of next-generation vehicles, including switches, relays, breakers, fuses and more.

Selecting the right companies to invest in can be daunting. I’ve recommended several in the past year.

We like Nano One Materials, which develops high-performance cathode materials that are used in highly advanced lithium-ion batteries. Standard Lithium, which has projects in Arkansas and California, is up more than 550% over the past 12 months. For copper exposure, we continue to bet on Ivanhoe Mines, which reported this week that its Kamoa-Kakula concentrator plant in the Democratic Republic of Congo reached commercial production on July 1.

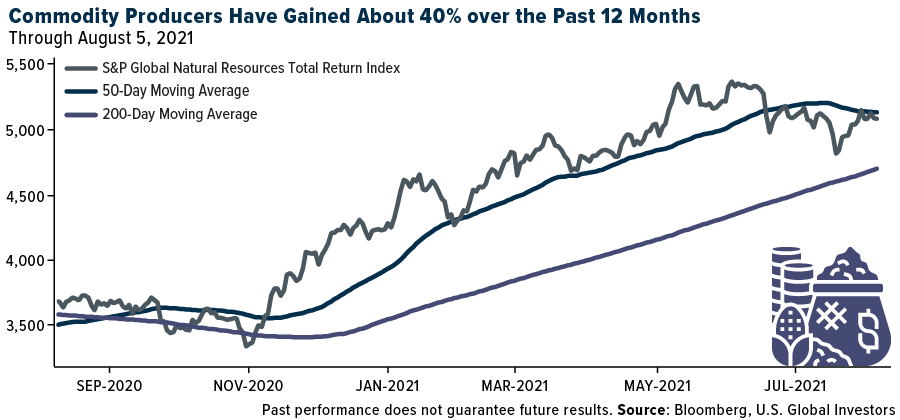

A possible solution may simply be to invest in an actively-managed natural resources fund that tracks a diversified group of companies involved in metals and mining. Take the S&P Global Natural Resources Index, which tracks 90 companies. It’s up nearly 40% over the past 12 months, and the 50-day moving average has remained above the 200-day since last September.

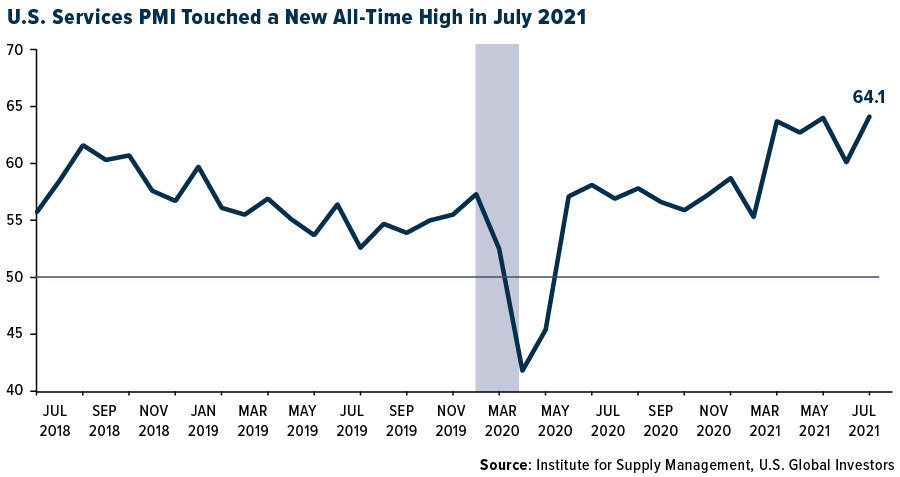

U.S. Manufacturing and Services PMIs at Record Levels

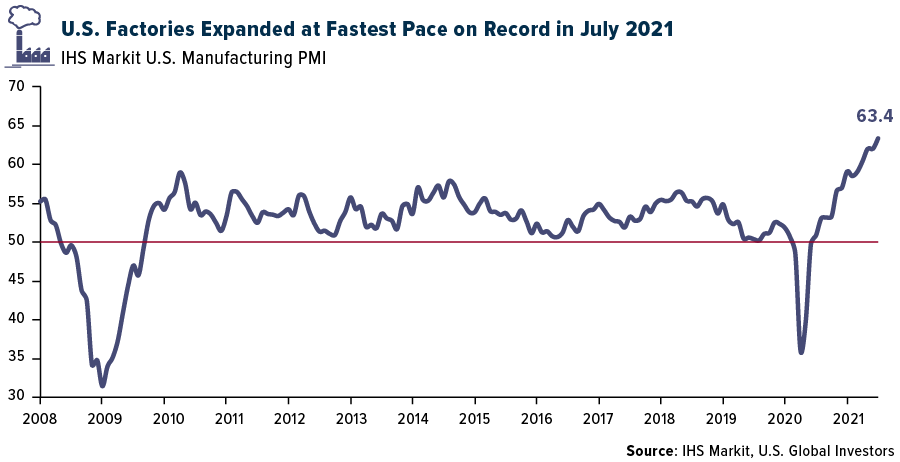

Contributing to my bullishness are the rate at which S&P 500 companies are beating earnings expectations and last month’s stunningly positive manufacturing and services PMI readings.

So far, 87% of companies in the S&P 500 have reported results for the second quarter, and of those, 87% have beaten Wall Street projections. If 87% were the final rate for the quarter, it would mark the highest such percentage since FactSet began tracking this data back in 2008.

July’s IHS Markit Manufacturing PMI came in at 63.4, the most significant improvement in U.S. factory operating conditions since records began in 2007. This is perhaps “the strongest sellers’ market that we’ve seen… with suppliers hiking prices for inputs into factories at the steepest rate yet recorded and manufacturers able to raise their selling prices to an unprecedented extent,” says IHS Markit’s Chris Williamson.

Service providers also had a blowout month. The Services PMI registered a 64.1, also an all-time high and the 14th straight month of expansion for the services sector.

It’s important to remember that the PMI, or purchasing manager’s index, is forward-looking. It measures factories and service providers’ expectations for growth in the next several months at least. When they’re more optimistic, as they are now, they’re more likely to increase orders for raw materials (in manufacturers’ case) and finished goods (in service providers’ case).

And with the U.S. economy having added close to 1 million jobs for two months straight, I expect demand to remain strong.

THERE’S STILL TIME!

On Wednesday, August 18, I’ll be participating in a webcast on gold and Bitcoin, and I will be joined by none other than Bitcoin evangelist Michael Saylor, founder and CEO of MicroStrategy. To get the link to book your spot for this exclusive conversation, email me at [email protected] with subject line “Michael Saylor webcast.” Demand has been higher than even I anticipated, so don’t hesitate to register!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.78%. The S&P 500 Stock Index rose 0.87%, while the Nasdaq Composite climbed 1.11%. The Russell 2000 small capitalization index gained 0.92% this week.

- The Hang Seng Composite gained 0.36% this week; while Taiwan was up 1.62% and the KOSPI rose 2.12%.

- The 10-year Treasury bond yield rose 7 basis points to 1.303%.

Airline Sector

Strengths

- The best performing airline stock for the week was Great Lakes Aviation, up 8.80%. American Airlines is seeing some positive developments. The company plans to reduce debt by $15 billion by 2025, above the $8-10 billion in scheduled debt payments. American noted that domestic corporate revenue was 45% recovered in June, which compares to Southwest Airlines’ 31%. Alaska Airlines, Delta Air Lines, and United Airlines all noted a 40% recovery in corporate demand.

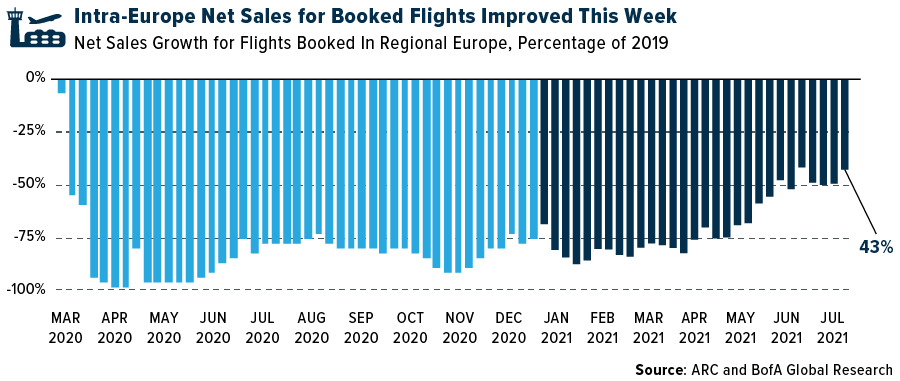

- The European airlines market continues to recover, according to research from Bank of America. As seen in the chart below, intra-Europe net sales for flights booked in regional Europe improved this week. Specifically, easyJet showed one of the biggest increases compared to 2019 levels, while all other airlines were up 1-2%, or only showed a marginal decline.

- The U.K. is reopening to fully vaccinated Americans and (most) European travelers, hoping for an influx of late-summer tourists. According to the Wall Street Journal and other news sources, England and Scotland announced they will allow vaccinated travelers from the U.S. and the European Union (excluding France), to enter the two countries without needing to quarantine.

Weaknesses

- The worst performing airline stock for the week was Controladora Vuelo, down 8.60%. After two particularly strong weeks of domestic booked traffic for September, the latest week stepped back, coming in at -1% versus +16% the week before, versus 2019 levels. International booked traffic for September also worsened to -58% in the latest week from -52%.

- In China, the TravelSky Weekly Volume Index fell 40% versus 2019 levels during the week, widening from -34% in the week prior (in particular, domestic volume was -13% versus 2019 levels, from -4% in the week before). The COVID-19 outbreak in multiple regions is adding to uncertainties regarding domestic air traffic.

- European airline bookings (as a percentage of 2019 levels) declined this week. Unfortunately, an increase in intra-Europe bookings was offset by a steep decline in international bookings. Intra-Europe net sales increased by 7 points to -43% of 2019 levels (versus -50% in the prior week). International net sales declined by 4 points to -76% (versus -72% in the prior week), and also fell week-over-week.

Opportunities

- Raymond James is bullish on Air Canada following the announcement of Canada allowing vaccinated travelers to and from the U.S. without quarantine restrictions, providing a much-needed glimmer of hope that the country will soon emerge from its prolonged "hibernation.” Canada announced it will allow fully vaccinated travelers to and from the U.S. as of August 9.

- Global capacity is indicated at -43% in July (no change), -39% in August (-2 points) and -31% in September, versus 2019. The delta variant continues to challenge the removal of international travel restrictions and appears to be driving more capacity reductions, globally.

- According to Bank of America, IAG's bookings have improved in recent months, with Spanish domestic flights over 100% of 2019 levels. Yet its focus on the U.K. and Ireland, which have stringent restrictions, means it has lagged the capacity recovery of its rivals. The U.K.'s decision to remove quarantine requirements for vaccinated EU and U.S. travelers should boost bookings, with Air France citing strong demand from U.S. citizens after EU restrictions eased.

Threats

- Analysts are estimating that Air France will need to raise 1.4 billion euros of additional equity capital to achieve its 2X leverage target by 2023, although 3.6 billion euros would be needed to resolve its negative equity. The company is still exploring further options to strengthen its balance sheet with equity or quasi-equity instruments, but the timing and size remain unclear.

- After a strong June, airline tickets booked through large and small corporate channels both failed to continue the pace in July. Domestic tickets sold through large corporate channels has flattened and remains down -52.9% this week. Smaller travel agency data remains down -25.2%. The delta variant is beginning to impact companies “return to office” plans.

- For the week ending July 25, system net sales took a step back to -47.4% versus 2019 (compared to last week's -45.7%) and is in line with the trailing eight-week average of -47%. Booking data has flattened out in the past two months. Domestic tickets sold were down -19.0% (versus -18.1% last week) which is in line with its trailing eight-week average. Domestic tickets sold through online channels has been bumpy in recent weeks but remains up +9.3% versus 2019. While the delta variant continues to remain a concern, the data may simply be normalizing as the industry moves past the peak summer travel season.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey gaining 3%. The best performing country in Asia this week was India, gaining 3.4%.

- The Hungarian forint was the best performing currency in emerging Europe this week, gaining 0.4%. The Taiwan dollar was the best performing currency in Asia this week, gaining 0.55%.

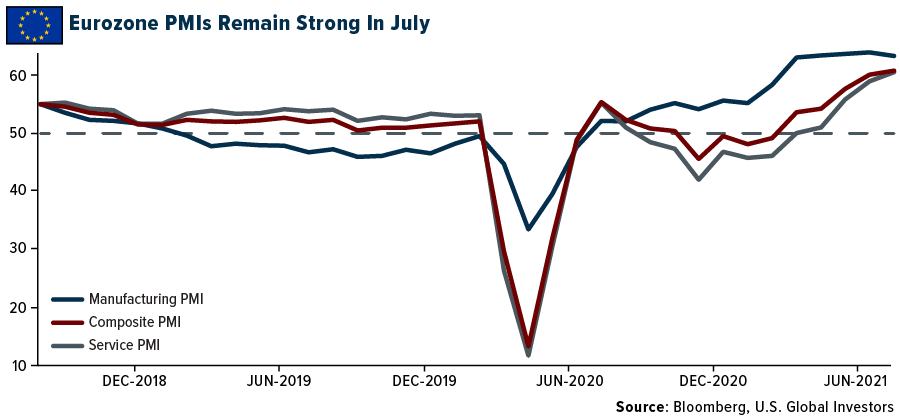

- Despite a downward revision, the final Eurozone Composite PMI showed its fastest rate of growth since June 2006 at 60.2, compared with flash reading of 60.6 and a prior showing of 59.5. Service PMI was also revised down to 59.8 versus the flash reading of 60.4. Manufacturing PMI was released at 62.8, below the prior reading of 63.4, but in-line with the expected 62.8.

Weaknesses

- The worst performing country in emerging Europe for the week was Romania, losing 0.2%. The worst performing country in Asia this week was Malaysia, losing 0.32%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 2%. The Thailand baht was the worst performing currency in Asia, losing 1.5%.

- Inflation in Turkey increased to 18.95% year-over-year compared to 17.75% the prior month. However, core inflation declined from 17.47% in July to 17.22% in June.

Opportunities

- European equites are moving higher. Reuters reports that stronger-than-expected quarterly results and a flurry of merger activity among European companies lifted sentiment this week in Europe despite growing concerns about slowing U.S. economic growth and soaring COVID cases, globally. From the two-thirds of STOXX 600 companies that have reported earnings so far, 67% have topped profit estimates, which is much better than the 51% beat-rate in the typical quarter.

- Turkish equites, especially banks, have outperformed recently. Brokers are noticing some foreign investors buying Turkish stocks again. We could see a rotation out of more expensive Chinese stocks as investors fear further market regulations. However, the Turkish lira weakened against the dollar this week as President Erdogan once again expressed his view that rates should be cut. The central bank decision will be announced next week. Most Bloomberg economists expect the main repo rate to remain unchanged at 19%.

- Eurozone investor confidence will likely remain at a high level when the data comes out next week. Easing restrictions and increased travel during the summer boosted investor confidence for an economic recovery.

Threats

- China has imposed national travel restrictions. Thirty-one provinces in the Asian nation told citizens not to travel to high-risk areas. Several airports have been temporarily closed while all flights in and out of Nanjing and Yangzhou have been suspended with train services curtailed. Beijing also imposed strict exit/entry restrictions. Asian countries outside of China are reporting an increased number of COVID cases as well.

- There is growing speculation that China may issue restrictions on gaming stocks after an editorial in the Economic Information Daily described online gaming as "spiritual opium" and that it is negatively impacting students' growth. The government may limit the time that minors spend on gaming to prevent internet “addiction.” Shares of Tencent declined on the news.

- Political tensions are running high in Belarus this week. Belarusian Olympic sprinter Krystsina Tsimanouskaya arrived in Vienna on Wednesday on her way to seek asylum in Poland after refusing to return to her homeland from the Tokyo Games for fear of persecution by the regime of President Alexander Lukashenko. The head of a group helping people who have fled Belarus, Vitaly Shishov, has been found dead near his home, reports the BBC.

Energy and Natural Resources Market

Strengths

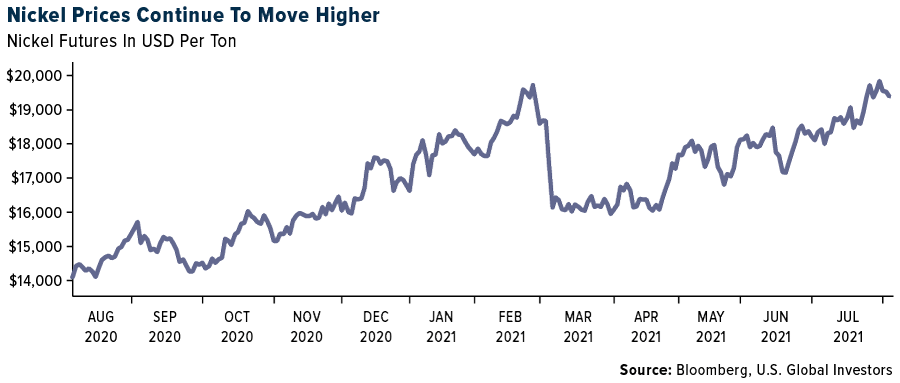

- The best performing commodity for the week was natural gas, up 5.34% which tipped over $4.00/mmbtu on the smallest gain in stockpile injections in 26 years amid record summer heat. Nickel prices are up 21% since bottoming out in early March as increased demand from stainless steel production is driving strength in the commodity. Over that same period, stainless steel prices are up 36% (44% year-to-date). Stainless steel accounts for 70% of global nickel consumption. According to Reuters, production of 300-series stainless steel, which contains 8-9% nickel, increased by 36% in the first half of 2021 versus the first half of 2020.

- A tightening global copper market is facing the real possibility of simultaneous strike disruptions at three mines in Chile, the top producer, writes Bloomberg. By far the most serious threat to global supply comes from Escondido, the biggest copper mine in the world, where workers rejected owner BHP Group’s final wage offer in voting last week. Unless the two sides can reach a deal in government-mediated talks this week, the article continues, the market may be left without production from a project that last year churned out 1.2 million metric tons. Two other smaller mines -- Codelco’s Andina and JX Nippon Mining & Metals’ Caserones -- are in the same situation as a country that accounts for more than a quarter of global copper, navigates a slew of collective bargaining at a particularly sensitive time in the metals cycle and in Chilean politics. The threat from the strikes appears to be keeping a floor on the copper price, which is likely to climb should there be any labor disruptions.

- CME Group's AUP Midwest aluminum premium futures forward curve continues to rally to record highs on August 2, following spot prices. Fresh buying, meanwhile, has come into the August and September contracts, with backwardations tightening further down the curve on ongoing supply concerns and the Unifor Union strike at Rio Tinto's BC Works smelter in British Columbia. Rio Tinto announced on July 26 that it would cut production at the smelter by around 35%.

Weaknesses

- U.S. lumber futures were the worst performing commodity, falling 12.75%, with market tightness easing. According to Random Lengths, the Framing Lumber Composite fell by $6 week-over-week to $479, marking the smallest weekly drop since mid-May. In the strand board market, the Composite fell $305 week-over-week to $723, with weakness most apparent again in Western Canadian markets as prices dropped $500/MSF (-50% week-over-week).

- Steel futures were under pressure on the Shanghai Futures Exchange, extending a slump of more than 5%. Beijing’s top leadership last week urged some easing of aggressive measures to cut carbon emissions, while pledging to ensure stability of supply and prices. The most-traded iron ore futures contract on the DCE for January 2022 delivery plunged to a four-month low on Thursday as market worries about shrinking iron ore demand turned market sentiment bearish.

- U.S. spot ethylene traded 2.25cpp lower, a 4% decrease week-over-week. Per IHSM, the U.S. ethylene spot market was active last week with 131 million total trades completed.

Opportunities

- HollyFrontier Corp. and an affiliate have agreed to buy Sinclair Oil Corp. for about $2.5 billion, a move that will expand its oil refining business and add a gas station chain, reports Bloomberg. The Dallas-based fuel producer will gain closely held Sinclair’s refineries, a renewable-diesel facility, and a network of over 300 distributors and 1,500 DINO-branded stations across 30 states. The all-stock transaction is worth about $1.8 billion, the company said in a statement. Holly Energy Partners LP, the company’s midstream business, will acquire Sinclair’s integrated crude and refined products pipelines and terminal assets for $758 million in stock and cash.

- As reported by Bloomberg, Australia’s second- and third-biggest oil and gas companies are set to merge to become one of the largest in the region and in the top 20 globally. Oil Search Ltd. on Monday said it agreed to an improved all-share offer from Santos Ltd. that would give its equity holders 0.6275 new Santos shares for each one held, giving them about 38.5% of the merged group. The combined entity would have a market capitalization of about $16 billion.

- Investors poured more money than ever into renewable energy in the first half of the year, but the pace is far from enough to sufficiently curb increasing carbon emissions. As much as $174 billion was spent on solar, offshore wind and other green technologies and companies in the period, according to data from Bloomberg.

Threats

- The world’s biggest steel industry is preparing for more cuts to production as China pushes forward with its plan to reduce emissions from heavily polluting sectors, clouding the outlook for iron ore demand. There will be more notable reductions in crude steel output along with government-led environmental checks, the China Iron & Steel Association said on its WeChat channel on Sunday. Daily production at major mills fell 5.6% in the first 10 days of July from June.

- BHP Group will this week enter government-mediated talks with workers at Escondido, the world’s largest copper mine, in a last-ditch effort to avert a strike, reports Reuters. Two other smaller mines -- Codelco’s Andina and JX Nippon Mining & Metals’ Caserones – are in a similar situation, as workers vie for a greater share of the riches following copper’s ascent to record highs above $10,000 in May.

- Oil declined for a third day as the coronavirus spread in Asia, particularly China, continuing to threaten demand. West Texas Intermediate futures slumped 1.9%, after retreating 4.6% in the previous two sessions. The delta strain of COVID-19 has been detected in almost half of China’s 32 provinces in just two weeks, and at least 46 cities have advised residents not to travel unless strictly necessary.

Domestic Economy and Equities

Strengths

- Purchasing managers’ index (PMI) data remains strong in the United States. The final July Manufacturing PMI came in at 63.4 versus 63.1 in June, the Service PMI came in at 59.9 versus the prior reading of 59.8. Composite PMI increased to 59.9 from 59.7, pointing to a strong market recovery.

- The number of Americans filing for first-time unemployment benefits fell this week, a sign that the U.S. job market continues to heal. First-time jobless claims dropped to 385,000 during the week ended July 31, matching estimates for 385,000 and down from a revised 399,999 the previous week.

- Under Armor was the best performing S&P 500 stock for the week, increasing 22.25%. Shares appreciated after the company reported strong second quarter results.

Weaknesses

- Private payroll firm ADP reported on Wednesday that employers added a disappointing 330,000 jobs in July, way below expectations, suggesting the labor market has stalled amid the surge in coronavirus cases.

- Mortgage applications fell 1.7% from a week earlier, according to data from the Mortgage Bankers Association's (MBA) Weekly Mortgage Applications Survey for the week ending July 30, 2021.

- IPG Photonics Corporation, a semiconductor devices maker, was the worst performing S&P 500 stock for the week, losing 16.84%. Shares declined after the company reported disappointing results.

Opportunities

- Inflation will come out next week and Bloomberg’s economists predict July inflation to drop to 0.6% from 0.9% in June. Year-over-year inflation may decline to 5.3% in July from 5.4%. It is a small move, but in the right direction.

- Reports suggest Senate leadership is getting ready to wrap up ongoing debates about amendments to the bipartisan infrastructure bill. Majority leader Schumer filed a cloture motion on Friday with the vote likely to take place on Saturday (and with final passage perhaps on Monday or Tuesday). This is a $1 trillion infrastructure plan that includes $550 billion in new spending on transportation, broadband and utility systems.

- Mortgage buyer Freddie Mac reported Thursday that 30-year mortgage rates fell below 3%. The average for a 30-year mortgage fell to 2.77% from 2.80% last week. This rate dip presents an opportunity for refinancing.

Threats

- Citi's Global Strategy team downgraded Unites States equities to neutral from overweight on Wednesday. The broker flagged expectations for 10-year Treasury yields to rise toward 2.0% into 2022 from the current 1.2% level, with real yields forecast to rise 70 basis points.

- The United States hit a six-month high for new COVID cases with over 100,000 infections reported on Wednesday, according to a Reuters tally, as the delta variant ravages areas where people did not get vaccinated. The delta variant, first detected in India, accounts for 83% of all new cases reported in the United States, according to the Centers for Disease Control and Prevention.

- Although the labor market is improving, it is still in a deep hole with 7-9 million people unemployed. Federal Reserve Bank of Minneapolis President Neel Kashaki is optimistic that we should have a strong labor market in the fall, but “it is so frustrating now for all of us that the delta variant is surging the way that it is,” he said.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Zugacoin, rising 245,000%.

- Despite dimming odds that U.S. regulators will approve a structure for a cryptocurrency ETF, Grayscale Investments continues to build out its ETF team. According to Bloomberg, the company behind the largest cryptocurrency fund has tapped David LaValle, former CEO of index provider Alerian, as its global head of ETFs.

- Canadian precious-metals retailer Kitco is getting into the stablecoin game, writes CoinDesk. According to a press release on Wednesday, Kitco Gold (KGLD) will be fully backed by physical gold held in Kitco’s Direct Reserve vaults, the article explains, and will track the real-time market value of the yellow metal.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Plethori, down 79.22%.

- Politicians and regulators have a flawed understanding of the cryptocurrency market and its technological underpinnings, according to billionaire crypto proponent Mike Novogratz. Amid the chorus of stringent crypto regulations among several U.S. leaders, Novogratz is looking to counter anti-cryptocurrency sentiments circulating in Washington, writes CoinTelegraph. On Tuesday, he tweeted that politicians and regulators must to do their homework before devising policies to regulate the industry.

- Two leading Republican senators are at odd on how-to step-up tax reporting requirements for companies that serve the crypto community. Because they are looking for revenue to offset the infrastructure bill costs so it could be less than optimal in in rule implementation.

Opportunities

- The U.S. SEC needs clear authority over platforms that trade or lend cryptocurrencies, according to Chairman Gary Gensler in an interview with CNBC this week. As reported by CoinDesk, Gensler spoke of the agency’s desire to “stitch together” consumer protection on platforms that offer lending or trading of both tokens sold as securities and tokens sold as commodities.

- On Tuesday, Binance – the world’s largest cryptocurrency exchange by trading volumes – announced a partnership with crypto-fiat hybrid payment platform Alchemy Pay, writes CoinTelegraph. Binance Pay users will now be able to pay across merchants of Alchemy Pay’s partners, including Shopify and software technology firm Arcadier.

- Nasdaq-listed Victory Capital has applied to the U.S. SEC to list an ETF tracking the Nasdaq Crypto Index, reports Yahoo! Finance. The company revealed its plan to enter the crypto market in June through a private fund tracking the NCI aimed at accredited investors, the article continues. It also announced intentions to launch private funds that mirrored equivalent Nasdaq indexes tracking the performance of Bitcoin and Ether.

Threats

- The SEC is considering whether to require Bitcoin mining to report their climate impact. Greenhouse gas emissions from cryptocurrency mining form an interesting intersection as it consumes a significant amount of electricity. SkyBridge Capital recently bought carbon offsets to green their Bitcoin holding, so the industry is already starting to consider these risks.

- Cryptocurrency Bitcoin SV is under a blockchain attack that appears to have inflicted at least some damage to the network, writes Bloomberg, according to a firm that analyzes system data. The 51% attack, as it is labeled, could enable the intruders to prevent new transactions from gaining confirmations, the article explains, thus giving them the power to stop payments between some or all users, or double-spend coins.

- Evidently, furniture maker Ethan Allen Interiors does not want to be associated with the crypto crowd. To make this perfectly clear, they announced on Thursday that they were changing their ticker symbol on the New York Stock Exchange from “ETH” to “ETD” to avoid confusion with cryptocurrency. The company specified that their brand is to evoke “classic, country, coastal and modern.” Ethan Allen Interiors does not do crypto.

Gold Market

This week spot gold closed the week at $1,763.03, down $51.16 per ounce, or 2.82%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 4.53%. The S&P/TSX Venture Index came in essentially unchanged for the week. The U.S. Trade-Weighted Dollar rose 0.66%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-1 | Caixin China PMI Mfg | 51.0 | 50.3 | 51.3 |

| Aug-2 | ISM Manufacturing | 61.0 | 59.5 | 60.6 |

| Aug-3 | Durable Goods Orders | 0.8% | 0.9% | 0.8% |

| Aug-4 | ADP Employment Change | 690k | 330k | 680k |

| Aug-5 | Initial Jobless Claims | 383k | 358k | 399k |

| Aug-6 | Change in Nonfarm Payrolls | 870k | 643k | 938k |

| Aug-10 | Germany ZEW Survey Expectations | 55.0 | -- | 63.3 |

| Aug-10 | Germany ZEW Survey Current Situation | 30.0 | -- | 21.9 |

| Aug-11 | Germany CPI YoY | 3.8% | -- | 3.8% |

| Aug-11 | CPI YoY | 5.3% | -- | 5.4% |

| Aug-12 | Initial Jobless Claims | 375k | -- | 385k |

| Aug-12 | PPI Final Demand YoY | 7.1% | -- | 7.3% |

Strengths

- The best performing precious metal for the week was palladium, but still off 1.28%, as precious metals took a hit across the board. Sudan’s official gold output nearly doubled in the first half of 2021 as authorities reined in smuggling, a Sudanese Mineral Resources Co. representative said, marking a partial success in efforts to salvage the economy. The North African nation recorded production of 30.3 tons between January and the end of June, compared to 15.6 tons in the same period the year before.

- Gold imports by India jumped to the highest in three months in July as economic activity picked up after a deadly coronavirus wave subsided, and prices in the second-biggest consumer softened. Inbound shipments surged 71% from a year earlier to 43.6 tons last month.

- SSR Mining said it returned to a second-quarter profit on higher gold production from its four mines. The company said it earned $51.6 million, or $0.25 per share, in the period, compared to a loss of $6.28 million, or $0.05, in the second quarter of 2020.

Weaknesses

- The worst performing precious metal for the week was platinum, down 6.46%, on news citing weaker industrial demand due to the new delta variant of the coronavirus. Platinum has already been in a weak trend with its price falling each of the past three months. AngloGold’s first half production was 1,200,000 ounces of gold, 7% behind consensus of 1,285,000 ounces. Cash costs were $1,003 per ounce, 8% ahead of consensus of $930 per ounce. Earnings per share (EPS) came in at 86 cents and was a 13% miss to consensus.

- Perth Mint says gold coin and minted bar sales totaled 70,658 ounces last month, according to figures on its website. Sales compare with 72,910 ounces in June, according to previously released data. Silver sales were at 1.3 million ounces in July versus 1.82 million ounces in June.

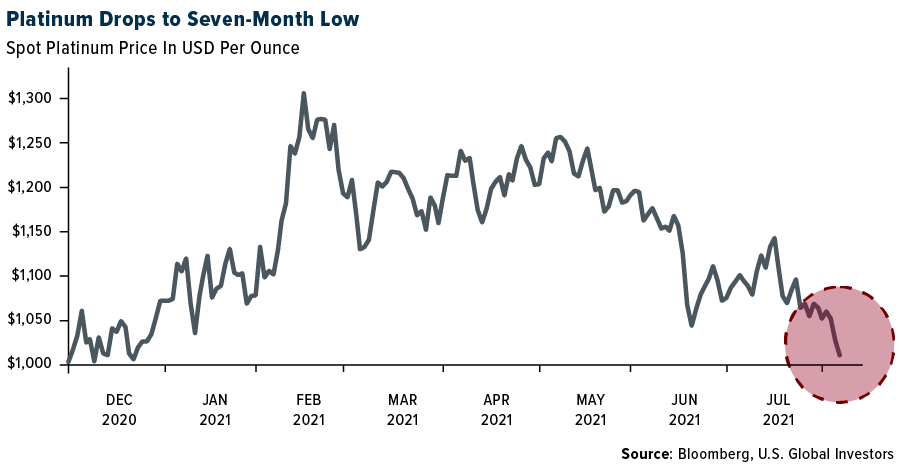

- Platinum dropped to a seven-month low as the spread of the coronavirus dents the outlook for industrial commodities, while a Federal Reserve official indicated the central bank is on course to taper stimulus. The metal used in catalytic converters fell for a third day as the spread of the delta strain punctures the narrative of a rapid global recovery. Platinum has tumbled 19% from this year’s peak in February as a computer-chip shortage curbed auto production.

Opportunities

- Gold is primed to surge to fresh highs as the risks around central banks unwinding massive stimulus are under-appreciated by investors, said Diego Parrilla, who manages the $250 million Quadriga Igneo fund and forecast the metal’s rise to a record last year.

- Auteco Minerals reported drilling results outside of its currently defined resources. The company reported an intercept of 9.8 meters at 3.1 grams per tonne grade of gold. Auteco’s Pickel Crow gold project currently has 1.7 million ounces of defined gold and with its current 50,000 meter drilling program it expects the resource to grow larger. In June the company released a resource which grew the previous estimate by 71%. Its Inferred Resource comprises a high-grade component of 1,470,000 ounces at 10.1 gram per tonne gold.

- Sibanye Stillwater entered into an agreement to buy Eramet’s Sandouville nickel hydrometallurgical processing plant, as it advances its plans to build a presence in the battery-metals sector. Neil Froneman, CEO of Sibanye Stillwater has communicated in the past that the company has considered an acquisition in the gold mining space. The nickel production line follows on the heels of a Sibanye investment into a Finnish-based lithium company.

Threats

- Most analysts expect gold to gradually decline over the next few years. The post-pandemic recovery, Federal Reserve tapering, and a stronger dollar will all weigh on the metal, which could fall to $1,700 an ounce by year-end and then decline further in 2022, UBS Group AG strategists, including Wayne Gordon and Giovanni Staunovo, said in a note.

- The Nigeria Extractive Industries Transparency Initiative (NEITI) has said that the 1% contribution of the mining sector to Nigeria's GDP was unacceptable. The agency described the activities of illegal minerals buying centers across the country as major revenue leakages to government, saying that it has become worrisome to the organization. In the past year, Thor Exploration has started its legal gold mining operations in Nigeria and recently poured its first gold doré bars.

- Gold trimmed gains after a report showed robust expansion in U.S. service industries last month, reducing demand for the metal as a haven and fueling concerns that Federal Reserve policymakers could soon scale back support for the economy. Friday’s price drop was the most in seven weeks and seems overdone compared to the backdrop on the “traditional” infrastructure spending bill and the $3.5 trillion economic package to follow.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2021):

American Airlines

Alaska Air Group

Delta Air Lines

United Airlines

easyJet PLC

Air Canada

BHP Group

Tesla Inc.

Volkswagen AG

Nano One Metals Corp.

Standard Lithium Ltd.

Ivanhoe Mines Ltd.

SSR Mining

Auteco Minerals

Sibanye Stillwater

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country's borders in a specific period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The TravelSky Weekly Volume Index measures air traffic volume specific to the Chinese air market.

The index includes 90 of the largest publicly-traded companies in natural resources and commodities businesses that meet specific investability requirements, offering investors diversified and investable equity exposure across 3 primary commodity-related sectors: agribusiness, energy, and metals & mining. The index includes 90 of the largest publicly-traded companies in natural resources and commodities businesses that meet specific investability requirements, offering investors diversified and investable equity exposure across 3 primary commodity-related sectors: agribusiness, energy, and metals & mining. The S&P Global Natural Resources Index includes 90 of the largest publicly traded companies in natural resources and commodities businesses that meet specific inevitability requirements, offering investors diversified and investable equity exposure across 3 primary commodity-related sectors: agribusiness, energy and metals & mining.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All