Europe is in the spotlight this month, with a key European Central Bank (ECB) meeting and a pivotal German election that could have significant medium-term implications for the fiscal stance of Europe’s largest economy. We see the ECB’s forecast revisions reaffirming inflation will likely stay below target in the medium term, requiring further policy support. Coupled with a broadening economic restart, this supports our tactical overweight stance on European equities.

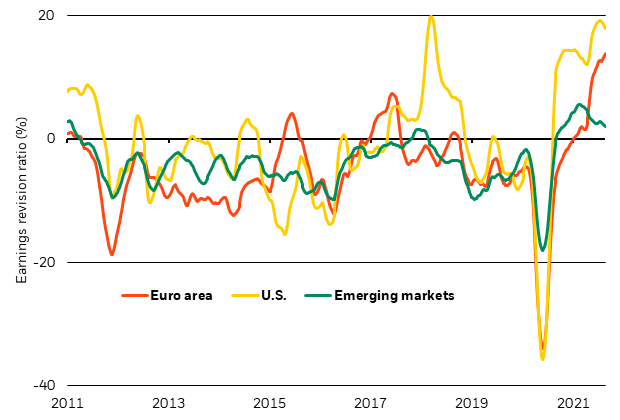

Euro area earnings momentum

Earnings revision ratios: Euro area vs. U.S. and EM, 2011-2021

Sources: BlackRock Investment Institute, with data from Refinitiv Datastream and Bloomberg, August 2021. Notes: The chart shows a three-month moving average of earnings revisions ratios – or the ratio of corporate earnings upgrades to downgrades for each region shown. The three markets are represented by the MSCI EMU Index, MSCI USA Index and MSCI Emerging Markets Index.

The economic restart has been broadening beyond the U.S. – aided by an acceleration in vaccine rollouts, particularly in Europe and the rest of the developed world. This has supported a sharp rise in European corporate earnings revisions from last year’s trough. Earnings revision ratios – the ratio of the number of stocks with corporate earnings upgrades to those with downgrades – are still on the rise in Europe, just as the ratio looks to be stalling in the U.S. (from high levels) and has already been trending lower in emerging markets. See the chart above. This shift in momentum lies behind our recent tactical upgrade in European equities to overweight, and our neutral stance on U.S. equities. Against this backdrop, the ECB meets this month in its second policy meeting since the central bank adopted a new policy framework. We expect the central bank to reinforce a low-inflation outlook for the medium term, paving the way for additional easing in 2022 and further supporting our tactical preference for euro area equities.

The ECB may choose at its September meeting to reduce the pace of asset purchases under its pandemic emergency purchase program (PEPP). The backdrop: easier financing conditions, especially with lower bond yields. Yet concerns that global financial conditions may tighten later this year around the likely start of the Fed’s taper of its asset purchases might persuade the ECB to leave the pace unchanged. In any case, we see this as an operational decision – and not one sending a signal about future policy. The central bank may lift its near-term growth and inflation forecasts, but we expect its outlook to show inflation remaining far below the ECB’s target over the medium term. Unlike the Fed, the ECB has not switched to target average inflation. This means any near-term overshoot of its inflation target – such as the recent upside surprise in the flash August print for euro area inflation – should not affect future policy decisions: The central bank will let inflation bygones be bygones. The weak medium-term inflation outlook implies that the ECB will need to step up its asset purchase program after the pandemic-era PEPP – which will run at least until March 2022 – expires.

The German election later in the month will be the first in a series of key elections in Europe that may be decisive in shaping the future of the region. It could have important medium-term implications for the country’s fiscal stance, business environment and plans to deal with climate change. The election looks to be wide open, with the Social Democratic Party (SPD) recently overtaking Angela Merkel’s conservative Christian democratic alliance (CDU/CSU) in a major poll for the first time in 15 years; and the process of forming a governing coalition could be drawn out. We do not see a repeat of euro crisis-style austerity as likely, not least because the Stability and Growth Pact (SGP) is suspended until 2023. Yet Germany’s fiscal stance could become more restrictive if a center-right coalition were to prevail. A more conservative fiscal stance in Germany could complicate matters for Europe if monetary policy alone is not enough to bring low inflation back up to target.

Bottom line: We see the ECB meeting this week paving the way for additional easing measures after the end of its PEPP. We also believe investors should be on the lookout for the longer-term policy implications of a new governing coalition in Germany, particularly on fiscal policy. We recently upgraded European equities to overweight on the back of the broadening restart helped by accelerating vaccinations. Valuations remain attractive relative to history and look even more attractive than at the start of the year thanks to strong earnings; investor inflows into the region are only just starting to pick up. We are neutral on German bunds and peripherals.