Gold. What’s wrong with it? From spiking inflation, falling real interest rates, and massive money printing, it seems logical that gold, a touted inflation hedge, should be rising. Yet, so far this year, gold has done little.

So, what’s wrong with this precious metal? Absolutely, nothing.

Is Gold Really An Inflation Hedge

One of the primary arguments for owning precious metals, particularly physical gold, is its effective hedge for inflation. However, is that still the case today?

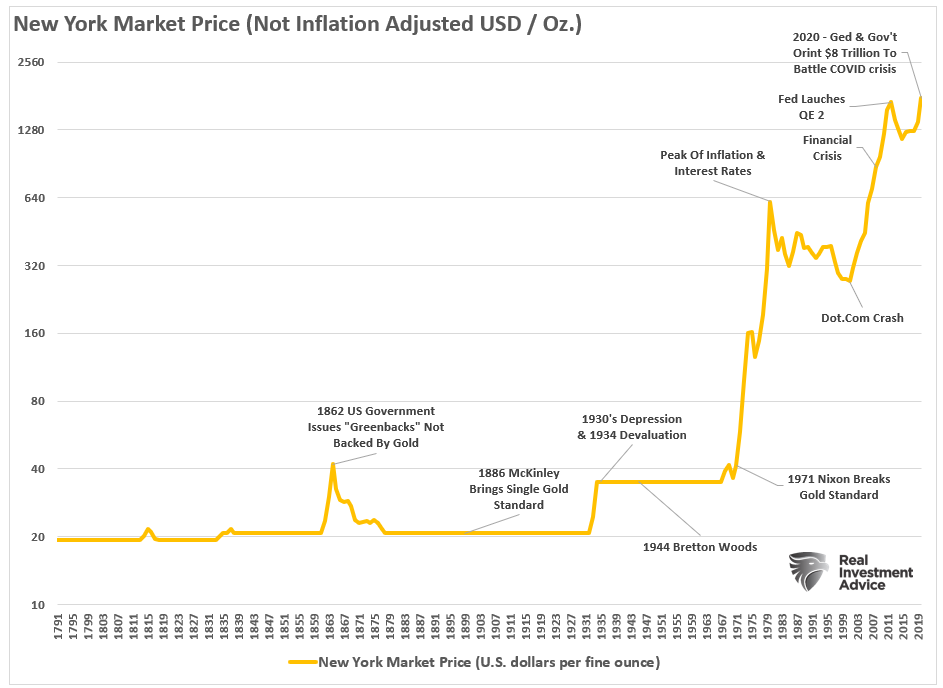

The chart below shows the non-inflation-adjusted price and key events throughout history.

The U.S. being on a “gold standard” is a crucial consideration of the argument of gold being an effective hedge against inflation.

“The gold standard is a monetary system where a country’s currency or paper money has a value directly linked to gold. With the gold standard, countries agreed to convert paper money into a fixed amount of gold. A country that uses the gold standard sets a fixed price for gold and buys and sells gold at that price. That fixed price is used to determine the value of the currency. For example, if the U.S. sets the price of gold at $500 an ounce, the value of the dollar would be 1/500th of an ounce of gold.” – Investopedia

As you can see in the chart above, prices remained stable until the point that President Nixon ended the gold standard in the U.S. However, for this analysis, the question is whether the golden metal is, or was, a good hedge against inflation?

Timing Is Everything

The answer is both “yes” and “no.”

As with all things investing-related, it is always a function of when you start. For investors in the stock market, those who started when valuations were in low double to single digits did much better than those with high valuations. (That is a lesson many of the Millennial and Gen Z investing group will come to learn.)

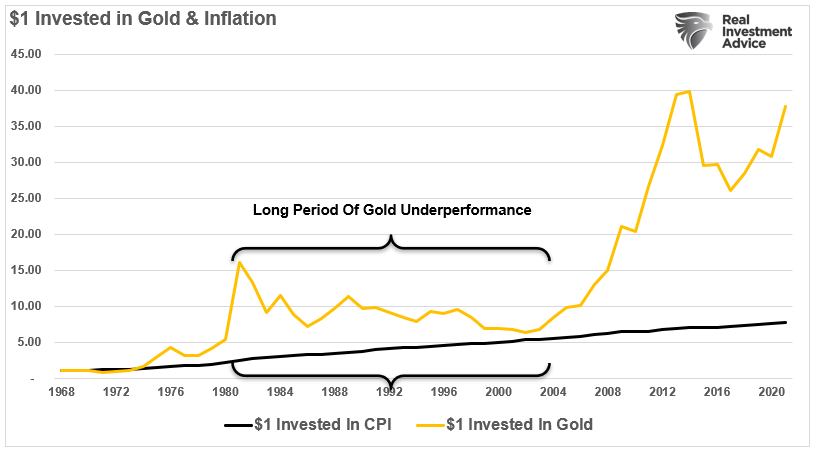

The chart below shows $1 invested in gold (non-inflation adjusted) and “inflation” as measured by the Consumer Price Index.

At first glance, like with the stock market, it is easy to see the precious metal outperformed inflation over time. However, that is only true if you bought gold before 1980, between 2002 and 2013, or in 2017. If you purchased gold outside those periods, you lost money relative to inflation.

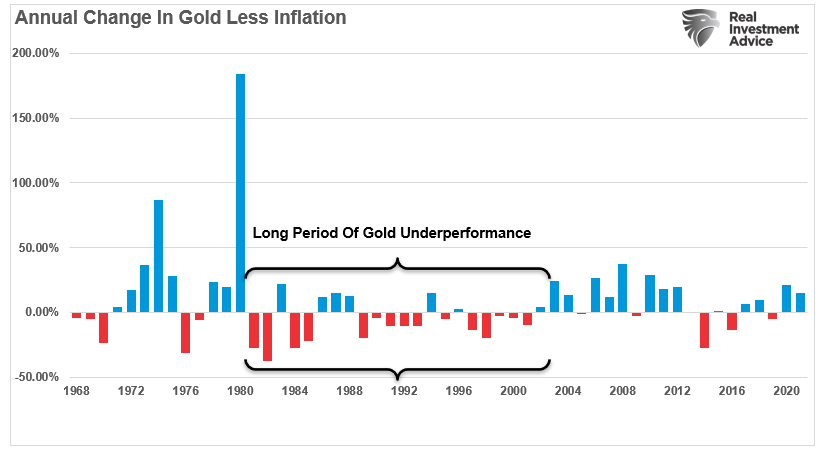

The following chart makes this concept easier to grasp by showing the difference in the annual rate of change and inflation.

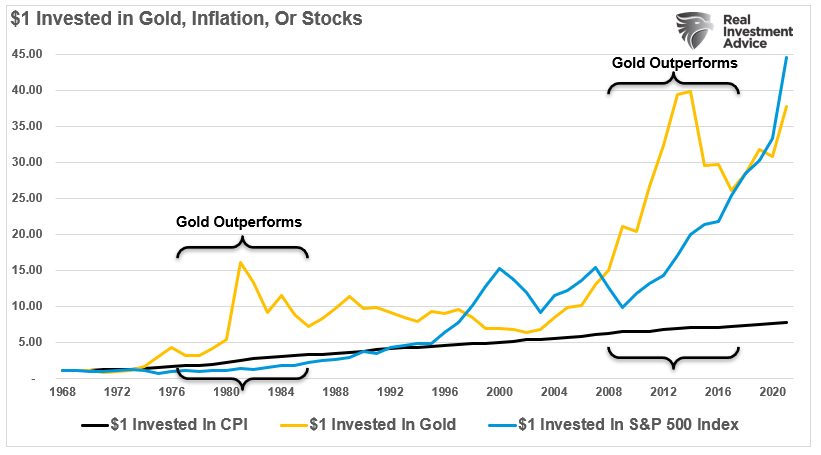

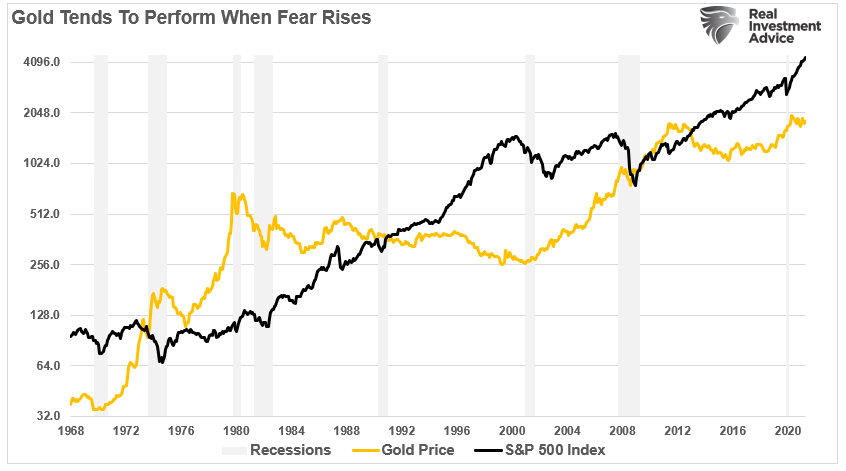

For every investment, there is always an “opportunity cost.” There is nothing wrong with owning gold in your portfolio, except when other assets, in this case, we will use the S&P 500 index, provides a higher rate of return.

Currently, given the influx of $120 billion a month from the Federal Reserve, the stock market provides a higher rate of return on investment than owning gold. Therefore, market participants choose to own ethereal assets due to the belief in “insurance against loss” rather than hard assets.

Will this “psychology” eventually change? Absolutely.

However, the question is, how much “lost opportunity” was there in the process? That is an evaluation that each investor will have to make for themselves to determine if such aligns with their investment goals and objectives.

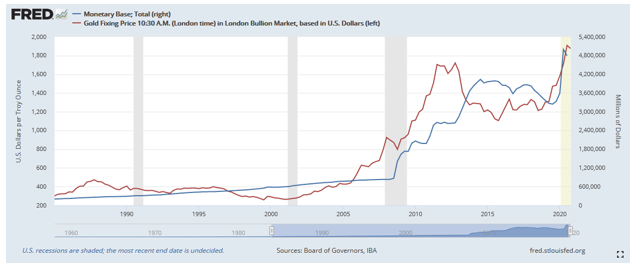

Gold’s Correlation to the Fed’s Footprint

As noted, there are certainly valid concerns of the Fed’s ongoing monetary interventions. As Michael Lebowitzpreviously reported:

“Linking real rates to the degree of central bank action form the basis on which we can look at the dollar’s value through the prism of gold. The first graph below shows gold has trended similarly to the monetary base.”

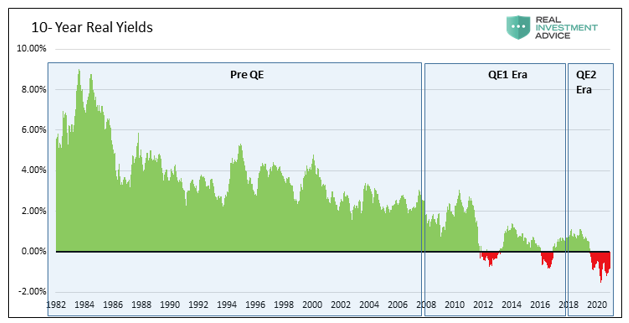

The next set of scatter plots are more compelling. They tell the story of how the price of the preciious metal became increasingly correlated to real yields as they decline. Said differently, gold is growing more positively correlated to the size of the Fed’s footprint.

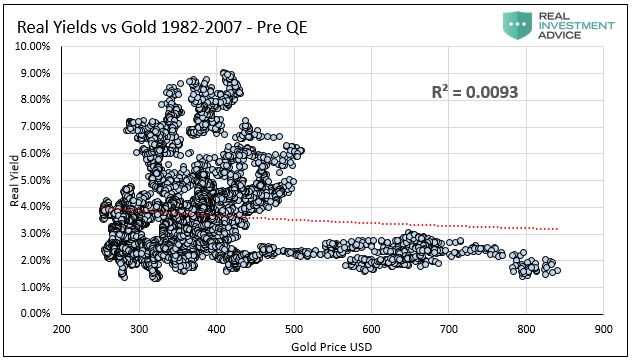

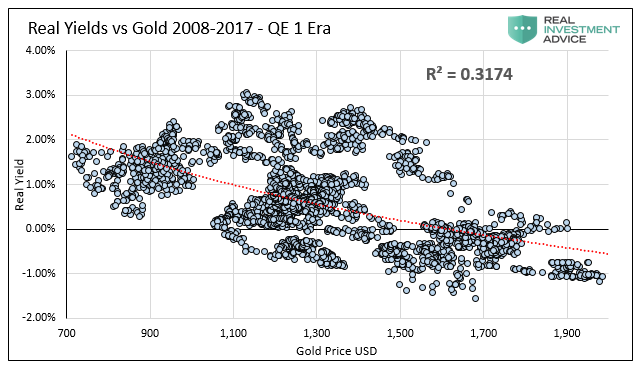

The three scatter plots break down the relationship into three-time horizons as shown below.

The Pre QE period, covers 1982-2007. During this period, real yields averaged +3.73%. The R-squared of .0093 shows no correlation.

The second graph covers Financial Crisis-related QE, 2008-2017. During this period, real yields averaged +0.77%. The R-squared of .3174 shows a moderate correlation.

The last graph, the QE2 Era, covers the period after the Fed started reducing their balance sheet and then sharply increasing it in late 2019. During this period, real yields averaged +0.00%, with plenty of instances of negative real yields. The R-squared of .7865 shows a significant correlation.

As he concludes:

“The message is not in the price of gold per se but its strong correlation to destructive fiscal and monetary policies.“

The Gold “Fear Trade”

There is one key “takeaway” from this article.

“Fear.”

Investors tend to buy “hard assets” when there is “fear” of increasing debt, inflation, a dollar decline, recession, a market crash.

So, let’s revisit the “original” question: “What is wrong with gold?”

Absolutely nothing. Except there is presently no “fear” present to drive investors into the psychological “safe haven” of gold. That lack of fear is evident in everything from:

Record issuance of money losing IPO’s.

Mass issuance of SPAC’s

Record margin debt levels.

Near record stock valuations.

Retail investors taking on personal debt to invest.

Bitcoin.

Belief by investors of the “Fed Put”

You get the idea.

Two Primary Problems

When it comes to investing, individuals need to determine “why” they own gold? Is it a short-term bet on prices rising or a “psychological” trade based on “fear” and “emotion?”

If it is the former, there is nothing wrong with owning gold. It is a commodity that will rise and fall in price. Given that gold has no fundamentals (earnings or dividends), the “price” of gold is all you need to know to trade the metal successfully.

The latter is more problematic. Given that gold is no longer exchangeable for currency, and vice versa, the broken link as an inflation hedge remains. In today’s “fiat” currency economy, the ability to use gold as a method for transactions on a global scale remains destroyed. Therefore, gold has become a “fear trade” over concerns of the dollar’s demise, inflation, and an economic reset.

While there are valid reasons to be concerned with such disastrous outcomes, those events can take decades to play out. For example, Japan is the poster child of a demographic timebomb combined with the world’s highest debt-to-GDP ratio. Such remains the case since the turn of the century, but the “bug has yet to hit the windshield.” Yes, it eventually will, but how much longer it will take is unknown.

Final “Precious” Thoughts

Therefore, from an investor’s standpoint, the question is not whether you should own gold, but “when?” Too much of your asset allocation in a “fear trade” when there is literally “no fear” in the financial markets could lead to a more significant loss of future purchasing power than inflation. In other words, “opportunity cost” can have as large an outcome on your financial future as inflation or the dollar’s demise.

As is always the case, timing is everything.

Is there anything wrong with Gold? No.

However, as long as the Federal Reserve is engaged in inflating asset prices and forcing investors to take on excess risk, gold will likely continue to underperform.

Will that eventually change? Absolutely.

When? As soon as the market participants realize the error of their ways.