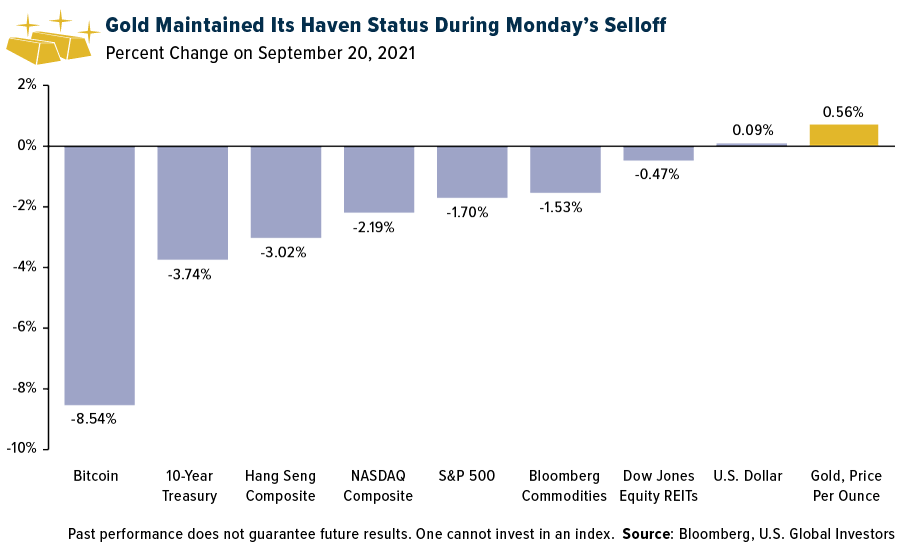

Gold Passed the Evergrande "Stress Test"

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIt’s the biggest company you’ve never heard of—until this past week, that is. Evergrande Group, the “too big to fail” Chinese property developer, rattled markets on Monday when it missed interest payments to at least two of its lenders. This gave more than a few investors flashbacks to Lehman Brothers’ demise in 2008, which helped trigger the global financial crisis.

The selloff spread to U.S. markets, and I was pleased to see that gold maintained its haven status. The yellow metal ended the day slightly up more than half a percent, passing an important “stress test” of its investment case in the age of Bitcoin.

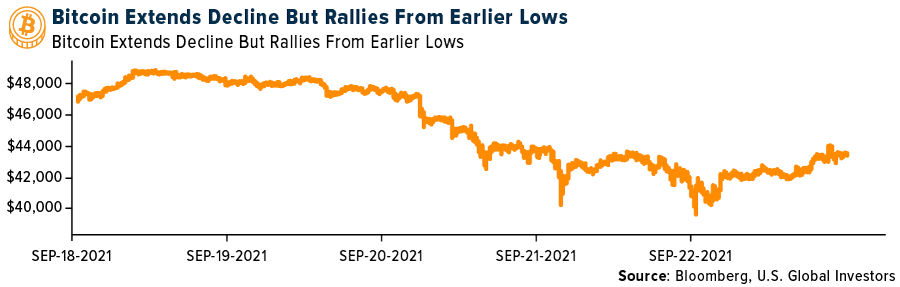

The world’s biggest cryptocurrency, believed by many to be “digital gold,” plunged 8.5% on Monday as investors dumped riskier assets. Indeed, Bitcoin is more than four times as volatile as gold. Those of you who attended HIVE Blockchain Technologies’ earnings webcast today know that gold bullion has a 10-day standard deviation of only ±3, while Bitcoin’s is ±14. Ether’s is even higher at ±19 over 10 trading days.

Bitcoin dipped further this week after the Chinese government banned all crypto transactions and crypto mining, prompting many to speculate that the People’s Bank of China (PBOC) is preparing to issue its own CBDC, or central bank digital currency.

I believe this crackdown is yet more proof that people need to own some Bitcoin, which is currently on sale as we await news on whether the Xi Jinping Administration will step in to prevent another pandemic, this one of the financial kind.

Gold and Bitcoin Looking More Attractive as Contagion Fears Mount

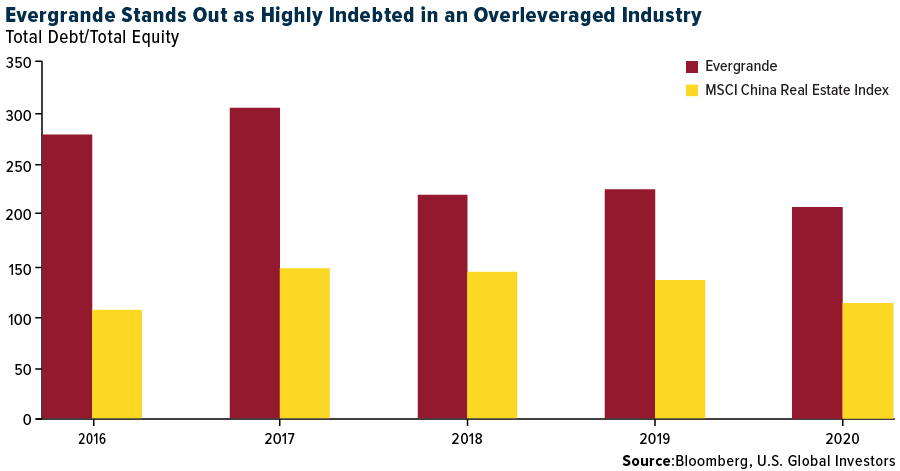

For the record, I find it hard to believe that President Xi will do nothing. Evergrande may not be a household name in the U.S., but it’s China’s second largest real estate company, with nearly 800 projects in 234 cities. It also offers financial products, invests in electric vehicles and is even building a theme park on an artificial island off the province of Hainan.

This growth didn’t happen organically, though, and today Evergrande is believed to be the world’s most indebted developer, saddled with more than $300 billion in total liabilities. In November 2020, the Financial Times wrote that the Fortune 500 company “has enough land to house the entire population of Portugal and more debt than New Zealand.” At the end of last year, it had roughly twice as much debt as equity, putting it in a class well above other Chinese real estate firms.

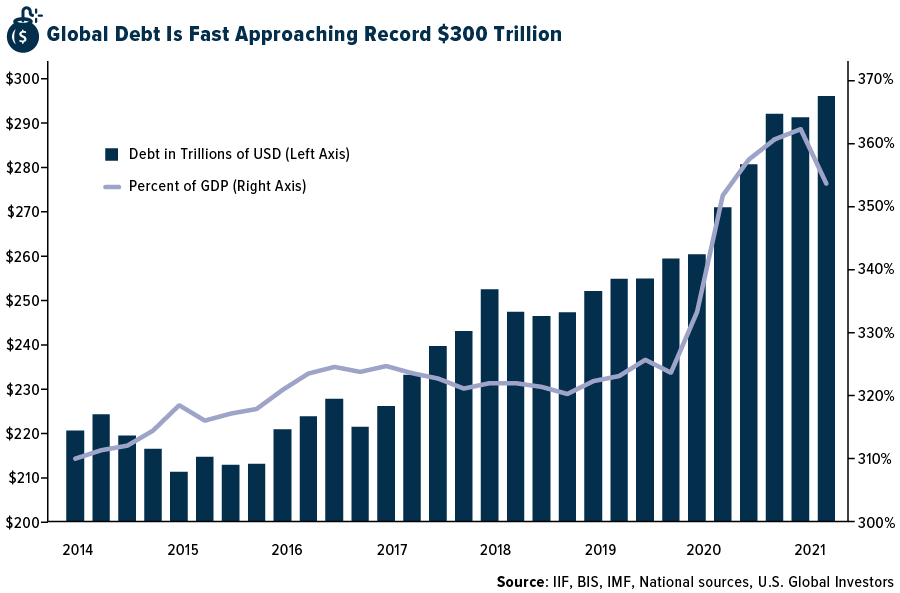

As “eye-popping” as Evergrande’s debt load is, it’s a “small drop in the ocean of debt that the world is swimming in,” CLSA’s Damian Kestel wrote today in a note to clients. Total global debt in the second quarter stood at just under $300 trillion, a new record, according to the Institute of International Finance’s (IFF) most recent Global Debt Monitor.

“The bigger they come, the harder they fall,” as the saying goes. If Evergrande were allowed to fail without any governmental intervention, it could spark a credit crisis that would make 2007-2008 look tame by comparison.

Against this backdrop, gold and Bitcoin look very attractive to me as stores of value, and both happen to be on sale right now. I’ve always recommended a 10% weighting in gold, with 5% in bullion and 5% in gold mining stocks and ETFs. I also believe it’s prudent to have between 1% and 2% in Bitcoin.

No, They’re Not Mutually Exclusive

As someone who’s involved in both gold and Bitcoin investing, I clearly don’t subscribe to the idea that one is better than the other in all cases. I agree with Bloomberg’s James Seyffart and Eric Balchunas, who said in a note this week that gold and Bitcoin “can complement each other in a portfolio.”

Although the two assets share obvious similarities and differences—one is thousands of years old while the other is brand spanking new; one is easily portable while the other isn’t—I think there are three important distinctions that investors need to be aware of: volatility, taxation and correlation to the market.

Volatility I’ve already talked about.

Looking at taxation, Bitcoin is taxed the same as a stock, with a long-term capital gains rate of between 0% and 20%, depending on income level. Gold, on the other hand, is taxed as a collectible, meaning it carries a higher fixed rate of 28%, regardless of income. Point: Bitcoin.

And then there’s correlation. Gold has no correlation to the S&P 500, making it suitable for someone who wants to hedge against market risk. As a risk-on asset, Bitcoin has a slight correlation to the S&P. Point: Gold.

When you add all of this up, I believe it shows that gold has a small advantage over Bitcoin as a diversifier and store of value—at least for now. This could change as the Bitcoin network matures and its price swings stabilize.

Bitcoin Man

|

I am thrilled and honored to be featured on October’s front cover of Real Assets Adviser, which is sent out to and read by thousands of registered investment advisors (RIAs). The fun photo was taken by U.S. Global Investors’ very own IT technician Rick Thompson, who moonlights as a photographer. You can see more of his amazing work on his Instagram page.

I want to thank Real Assets editor Mike Consol, who reached out with the idea to feature me. Our conversation covers a number of topics, including gold and Bitcoin (of course), my early career, the current state of the airlines industry and the San Antonio Spurs. The entire interview is posted here.

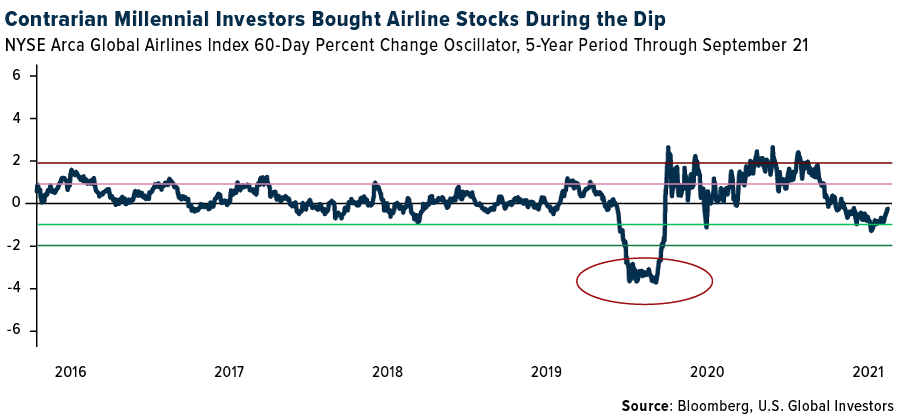

Airlines Webcast

Besides leading the HIVE earnings report this week, I also took part in a webcast on the airlines industry, co-hosted by ETF Trends Managing Editor Lara Crigger.

As you might imagine, much of the discussion centered on when and to what extent the airlines industry will fully recover.

Below is a slide that seems to have resonated with attendees. It shows the 60-day standard deviation oscillator for the NYSE Arca Global Airlines Index, and if you notice, airline stocks were greatly oversold at the start of the pandemic. I bring this up because that’s when contrarian millennial Robinhood investors got in, at the same time that Warren Buffett and others panic sold.

You can find the on-demand replay of the webcast on ETF Trends’ website by clicking here. The webcast is titled “Can Airline Investors Finally Remove Their Seatbelts?”

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.62%. The S&P 500 Stock Index rose 0.61%, while the Nasdaq Composite climbed 0.02%. The Russell 2000 small capitalization index gained 0.79% this week.

- The Hang Seng Composite fell 2.84% this week; while Taiwan was down 0.10% and the KOSPI fell 0.49%.

- The 10-year Treasury bond yield rose 9 basis points to 1.455%.

Airline Sector

Strengths

- The best performing airline stock for the week was Air France, up 15.2%. The United States is officially making plans to lift the ban on international travel to the U.S., starting in November. Visitors from previously banned countries must be fully vaccinated to enter; those who remain unvaccinated will be allowed entry but will be subjected to strict COVID testing requirements. For 18 months, the only people allowed to visit the U.S. from the U.K., the EU, and several other countries have been U.S. citizens, their immediate family members, and those on a short list of exemptions.

- In the first half of September, China’s domestic air traffic recovered to 66% of 2019 levels (from 42% in the second half of August 2021) due to easing travel restrictions. Domestic capacity was back to 80% of normal levels in the first half of September. By contrast, Chinese international traffic stayed unchanged at 3% in the first half of September given strict border controls and flight restrictions. Domestic seat loads also rebounded to 69% in the first half of September, up from 63% in the second half of August. In addition, domestic yields recovered to 100% of 2019 levels in the first half of September.

- According to the Bank of America, its higher price target for Qantas is driven by assumptions regarding the reopening of international travel and by property monetization. The bank previously assumed a reopening of international travel to happen in June, however, given vaccination rates, it adjusted predictions to January. Qantas owns 14 hectares of mostly undeveloped land surrounding Sydney Airport. The company is in the process of exploring divestment options. As reported in recent press articles, Qantas has shortlisted parties for the auction's second round. Its valuation now assumes successful monetization of the land in 2022 at $550 million USD, aiding in balance sheet repair.

Weaknesses

- The worst performing airline stock for the week Aegean Air, down 4.0%. European airlines have had weak corporate demand, which led to a 1-point decrease in system-wide net sales for flights booked in Europe to -62% versus 2019 levels (versus -61% in the prior week). The lack of corporate travel demand, which is typical at this time of the year, could potentially weigh on the booking’s recovery.

- As comparisons normalize, the most recent week's data shows system net sales took a slight step back to -66.4% versus 2019 levels for the week, versus -63.9% during the last week. Domestic tickets sold took a similar step back to -34.4% versus -31.2% in the previous week. Domestic leisure tickets sold were -8.9% (versus -6.1% last week) while corporate demand was -61.2% (versus -59.2% last week).

- After seeing strong TSA throughput numbers around the Labor Day weekend (back above 80% of 2019 levels for six days), this week the TSA throughput trailing seven-day average took a sizable step back to -28.3% versus 2019. This is the lowest the TSA numbers have been since early June as corporate demand remains weak during the early part of September.

Opportunities

- Ryanair appears to have greater conviction in reaching the upper end of 90 to 100 million passengers in fiscal year (FY) 2022, with very strong bookings/pricing during the school mid-term break in October, over Christmas in December, and Easter in April. Likewise, Ryanair increased the long-term growth outlook from 33% to 50% of its five-year growth rate by FY2026. Slower fleet retirements/lease returns are expected to result in a FY2026 fleet of 620 versus 600 previously.

- Daily website visits for EU airlines were up by 4 points to -18% versus 2019 levels in the week (versus -22% in the prior week). easyJet showed the largest increase by 12 points, although this is likely related to its rights issue. Iberia, British Air and Wizz Air were up by 5 to 9 points, while Turkish Air, Lufthansa, Ryanair and KLM Royal Dutch Airlines grew by 1 to 3 points.

- Dr. Anthony Fauci, the nation's top infectious disease doctor, supports a vaccine mandate for air travel, but not all airlines are on board with this. Last week, Dr. Fauci told the Washington Post that he is supportive of a vaccine mandate for air travel but is not proposing it be enforced. However, if President Biden and his administration wanted to enforce vaccines for air travel, he would be supportive of it.

Threats

- According to Credit Suisse, following Lufthansa’s announced 2.1 billion euros equity raise, (at a 39% discount to the ex-rights price), this creates a doubling of the share count – halving the 2022 estimated-onward EPS forecasts. Net debt has now been reduced to 8.3 billion euros on a pro forma basis, versus 6.7 billion euros at FY2019, but may rise further over the winter, suggesting successful asset disposals may be necessary to further de-leverage before 2023.

- British Air abandoned plans for a new lower-cost unit at Gatwick given lack of union support. The company reports it will focus on long haul and consider alternative uses for many slots used for short haul, given historical losses.

- Airline pricing is worse than is being actively reported. With long-haul travel still down significantly more than short-haul travel and with fewer last minute higher priced business traveler fares, the overall average ticket price has fallen more dramatically than fare prices on specific routes. So, while average advertised fares decreased by 15% during the second half of 2020, the implied average ticket price was down closer to 30% over that same time period due to the change in mix.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Romania, gaining 1%. The best performing country in Asia this week was India, gaining 1.6%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 0.15%. The South Korean won was the best performing currency in Asia this week, gaining 0.17%.

- Consumer confidence in the euro-area rose to -4.0 in September, from -5.3 in August, and above the consensus expectation for a fall to -5.8. The improvement in the pandemic situation throughout the Eurozone is lifting sentiment among consumers.

Weaknesses

- The worst performing country in Asia this week was Hong Kong, losing 2.9%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 2.5%. The Philippine peso was the worst performing currency in Asia this week, losing 1.5%.

- AsiaMarkets.com reported that China’s property developer Evergrande is set to be restructured into three separate entities, making the company government owned. Investors are becoming nervous over the lack of communication from both the company as well as the government regarding a missing dollar payment. There are quite a few coupon payments coming up and investors are uncertain if Evergrande will be able to continue to fulfill its upcoming obligations.

Opportunities

- The European Central Bank (ECB) and Federal Reserve Bank balance sheets are both surging, which should provide a cushion for whatever fallout transpires from the Evergrande crisis, Ed Hyman wrote in his daily markets update. The two balance sheets together increased at a nearly $6 trillion annual rate last week to a total of $18.1 trillion. The balance sheet expansions are also keeping upward pressure on asset prices.

- China will likely continue to support its economy and protest domestic investors from Evergrande’s debt crisis. On Friday, the PBOC injected $18.6 billion into the financing system, the largest such injection of funds since the beginning of the year and the fifth consecutive business-day of net injections.

- TS Lombard said that the European gas shortage combined with higher energy prices is a good reason to refocus on Russia. Gazprom recently completed its North Stream 2 pipeline gas project connecting Russia with Germany and gas transports could start as soon as the certification procedures are completed. Russia is Europe’s biggest supplier of gas and accounts for about 40% of imports.

Threats

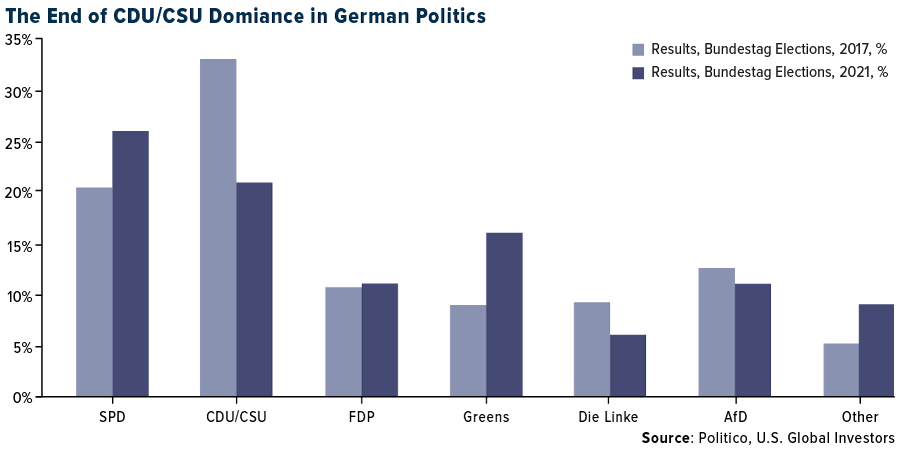

- This weekend Germany will hold parliamentary elections. After years of stability under the leadership of conservative Chancellor Merkel it is likely that the German government will be more fragmented. Pre-election polls have shown a fall in support for the Christian Democratic Union of Germany (CDU) and the Christian Social Union in Bavaria (CSU) coalition party led my Merkel, while the Social Democrats have gained momentum. A new collation will likely have to be formed.

- Eurozone preliminary PMI numbers are pointing to an economic slowdown in Europe. September Manufacturing PMI came in at 58.7 versus expected 60.3. The Service PMI came in at 56.3 versus expected 58.5, bringing the Composite PMI down to 56.1 in September from 59 in August.

- Eurozone confidence data, which is due to be released next week, will likely come in weaker. We have witnessed a slowdown in economic activity already and further corrections may follow. Europe has been handling the pandemic well during the summer and early fall, but winter usually brings additional sicknesses with its much colder weather.

Energy and Natural Resources Market

Strengths

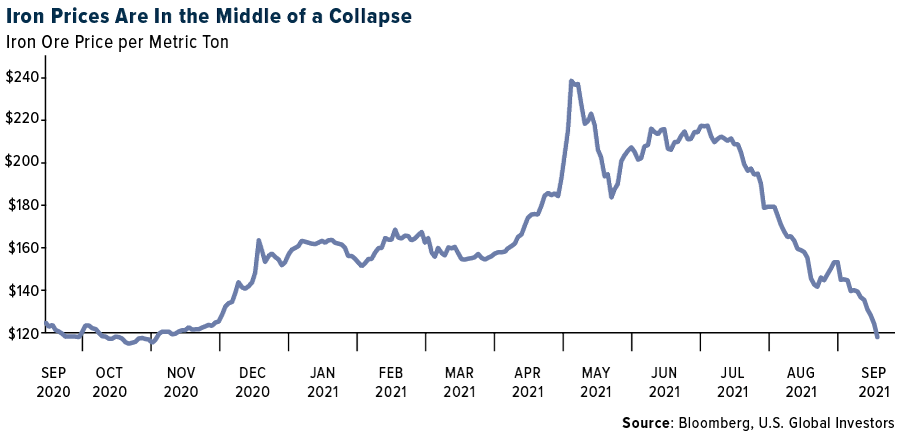

- The best performing commodity for the week was DCE iron ore futures, up 5.35%, after three-consecutive weekly drops on steel production curtailments in China. A perfect storm of events, from extreme weather and plant shutdowns to new government sanctions, has hit the chemical fertilizer market this year, slamming farmers already buckling under the strain of rising costs to produce food. Prices for urea, a popular nitrogen-based fertilizer, skyrocketed earlier this month to the highest since 2012. A common phosphate fertilizer known as DAP is the most expensive in that market since 2008, Bloomberg data reveals.

- A confluence of issues has lifted global natural gas prices, perhaps the latest example of unintended consequences of new energy policies shying away from fossil fuels in the fight against climate change. European natural gas storage heading into winter is 18% below five-year average levels. U.S. storage is below normal and tightened further by weather-adjusted supply/demand balance.

- Aluminum's recent rally has been helped partly by a sharp rise in European and Chinese power prices. Aluminum's high energy requirements, and its key role in transition technologies, leave it caught between rising input costs and higher demand.

Weaknesses

- The worst performing commodity for the week was uranium futures, down 5.41% after an almost 40% surge since September (as a possible carbon-free fuel for the future). Australia’s top three iron ore miners have shed a combined $109 billion USD in share value in less than two months – roughly equivalent to the market cap of General Electric Co. – following a record-breaking price rout. The three miners together account for more than 8% of Australia’s benchmark S&P/ASX 200 share index, which has slipped 2% over the period. The iron-ore demand squeeze could continue as China’s now mature steel sector faces further caps on production, which plunged to a 17-month low in August. Consequently, iron ore will come under more pressure, falling to $80 from $90 a ton heading into next year, said UBS Group AG strategist Wayne Gordon.

- Copper has been weakening in part due to a slowing housing market, which reduces demand for copper piping. The three-month copper price touched $9,052 per ton on Monday during early trading – its lowest since June 21. This is a 2.8% decrease from its closing price of $9,312 per ton last week.

- The U.S. refining sector began the year outperforming the S&P 500 by as much as 30% through March, driven largely by improving demand expectations. However, the sector's performance now lags both the S&P 500 and the broader XLE Energy Index. Winter Storm Uri, rising input prices and lower-than-expected capture rates were some of the headwinds faced by this sector.

Opportunities

- Lumber prices continue to climb. According to Random Lengths, the Framing Lumber Composite increased by $27 this week to $445, posting its third consecutive weekly increase. Lumber prices rose despite decreased demand overall. Boxboard prices increased again this month. Market participants noted that all markets remain tight from a supply-demand perspective, with most sellers on allocation.

- ConocoPhillips agreed to acquire Royal Dutch Shell Plc’s Permian Basin assets for $9.5 billion in cash, accelerating the consolidation of the largest U.S. oil patch. That will make ConocoPhillips one of the Permian’s biggest producers, rivaling Pioneer Natural Resources Co. and Chevron Corp. in terms of crude output. The Permian, which straddles West Texas and New Mexico, is the world’s busiest shale patch and accounts for nearly half the current activity in U.S. oil fields.

- According to UBS, European and U.S. integrated energy companies have risen an average of 25% this year, justifying their positive stance, but this is hardly stellar compared to crude oil's 46% rise and strong natural gas prices. The sector has stalled since April, up only 2.4%. However, 2022 estimated EV/FCF is 5.2X, which is 12% below the five-year average. This implies a 2022 free cash flow yield of 12.2% and a distribution yield of 9.4%.

Threats

- Oil resumed declines amid growing concerns over the health of China’s economy that have triggered massive losses in equities. The U.S. crude futures fell to the lowest in a week as worries mount over a possible implosion in the Chinese property sector that could impact the Asian giant’s appetite for crude.

- Surging energy costs are adding to pressure on global aluminum supply at a time when demand for the metal used in everything from cars to beer cans has already driven prices to a 13-year high. Just weeks ago, it looked like aluminum’s blistering rally might spark a worldwide rush to reopen mothballed smelters. However, the industry is massively energy intensive, writes Reuters. The spike in global electricity and coal prices will make restarts increasingly difficult and some producers may also soon be struggling to run their existing smelters profitably if the energy crunch worsens, particularly those not locked into long-term power contracts.

- Another European fertilizer producer is reducing output due to soaring natural gas prices, exacerbating already tight supply across the continent. Austria-based chemicals firm Borealis AG is curtailing its production of ammonia in Europe and will “further analyze the situation” regarding its plants in Austria, France, and the Netherlands.

Domestic Economy and Equities

Strengths

- August housing starts rose 3.9% month-over-month, beating estimates for a 1.9% gain and rebounding from last month's 6.2% decline. Gains were mostly driven by multifamily data, up 94,000 month-over-month and the best reading since 2019. Single family starts were down 31,000 month-over-month, the lowest since April. August building permits were reported higher as well, reaching the highest level since April. Permit gains were also driven heavily by multifamily homes.

- With the U.S. economy recovering from the negative effects of the pandemic, Federal Reserve Chairman Jerome Powell said that the central bank could begin scaling back asset purchases as soon as November and complete the process by mid-2022. The tapering will be a gradual process and the rate hikes may not happen soon.

- Expedia Group was the best performing S&P 500 stock for the week, increasing 13.05%. In Expedia Group’s ongoing bid to simplify its operations, the company decided to consolidate its current three loyalty programs into one globally. In addition, now members will be able to earn and burn rewards for vacation rentals.

Weaknesses

- Initial jobless claims came in at 351,000 for the week, up from the prior week's upwardly revised 335,000 and above consensus for 325,000. Continuing claims surprisingly increased, too. They were reported at 2,845,000, above the expected 2,600,000.

- September preliminary U.S. Manufacturing PMI data declined to 60.5 versus the expected reading of 61.0. Service PMI was reported at 54.4, slightly below the expected 54.9. Composite PMI registered 54.5, below August's 55.4 and the slowest pace of expansion since August 2020, with new-order growth also at 12-month lows.

- FedEx Corporation was the worst performing S&P 500 stock for the week, losing 11.06%. On Wednesday, FedEx shares dropped the most in 18 months on reports that the labor shortage is driving up company costs. FedEx is trying to attract workers by offering higher wages, which have increased more than 25% from a year earlier at some Express unit hubs.

Opportunities

- The United States will reopen in November to international travelers from 33 countries including China, India, Brazil and most of Europe who are fully vaccinated against the coronavirus, the White House said on Monday. This announcement will ease many of the tough pandemic-related travel restrictions that started early last year.

- Carnival, the world’s largest cruise operator, said it plans to have more than 50% of its fleet’s capacity operating by the end of next month. That amounts to 42 ships. Eight of the company’s nine cruise brands have resumed sailings following the shutdown last year due to the pandemic—the lone exception being P&O Cruises (Australia).

- Initial jobless claims picked up this week, but they should continue to come down over the longer term to reach pre-pandemic levels. The U.S. recorded nine consecutive weeks of claims below 400,000, a level last seen in May of 2021.

Threats

- Advisers to the Centers for Disease Control and Prevention have expressed concerns that ongoing resistance by many individuals to getting vaccinated against COVID-19 will prolong the pandemic, regardless of whether booster shots are offered, as they weighed the benefit of extra doses. More than 30% of the U.S. population has not taken the first shot yet.

- Chinese real estate developer Evergrande’s debt crisis has created a lot of noise in the global markets this week, causing selloffs at the beginning of the week. China most likely will not allow disorganized default of the company, but it is unknow if the heavily indebted firm will be able to pay its upcoming obligations. The Chinese government does not want Evergrande’s debt issue to turn into a large-scale problem potentially impacting the banking sector.

- U.S Treasury yields rose across the board on Thursday, with those on benchmark 10-year notes climbing to their highest levels in more than two months. U.S. 30-year yields also rose, on track for their largest gain in three months. Global central banks led by the Federal Reserve have turned more hawkish as the economic outlook around the world improved and inflation picked up.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Gravitoken, up over 1 million percentage points.

- Similar to apps like Coinbase, Cash App, and Venmo, Robinhood is testing out a new feature for its app in which costumers can send and receive digital currencies such as Bitcoin, reports Bloomberg News. Earlier this month, the company said it would roll out crypto recurring investments, allowing users to buy digital coins commission-free and with as little as $1 on a schedule of their choice. Retail shareholders and crypto enthusiasts alike are eagerly awaiting news of the future software update.

- On Wednesday, an economic free zone in Dubai made an agreement with the UAE’s Securities and Commodities Authority (SCA) to trade crypto assets. The agreement creates a framework for the Dubai World Trade Centre Authority (DWTCA) to license and acquire approvals for all cryptocurrency-related activities – including issuing, listing, licensing, and trading crypto – in the free zone. The oil-rich country has reported that cryptocurrency could be integral to its economy as more and more countries attempt to cut down carbon emissions.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Nerve Finance, down 83.07%. This week Bitcoin dropped below $40,000 for the first time since August, reports Bloomberg, before rallying as the mood in global markets improved. Although Bitcoin broke its three-day losing streak on Thursday, this price action “demonstrates that Bitcoin isn’t immune to the selloff in risk-on assets across traditional markets,” said Antoni Trenchev, co-founder of crypto lender Nexo.

- In a recent report from Bitcoin.com, founder of the Virgil Sigma Fund and the VQR Multistrategy Fund, Stefan Qin, was found guilty of securities fraud and sentenced by the Department of Justice (DOJ) to 7.5 years in prison. He is also expected to forfeit about $55 million. The DOJ says that Qin “engaged in a scheme to steal assets” from his hedge funds and defraud investors. “Rather than investing the fund’s assets in a cryptocurrency arbitrage trading strategy as advertised, Qin embezzled investor capital from Virgil Sigma and used the funds for purposes other than the purported arbitrage trading strategy,” details the DOJ last Friday.

- Bitcoin slid about 90% on the Pyth Network earlier this week after the company’s computers failed basic computations. Pyth Network said two unidentified firms that supply data to the platform encountered trouble dealing with decimals, causing them to report extremely low Bitcoin prices. Those incorrect numbers got averaged with Bitcoin prices from nine other Pyth contributors, leading to the inaccurate result, reported Bloomberg.

Opportunities

- Miami’s city commissioners voted to accept funds generated by a new cryptocurrency, MiamiCoin, which was launched in August by CityCoins, details CoinTelegraph. The coin was built on Stacks, an open-source network of decentralized applications and smart contracts that use the Bitcoin blockchain as a programmable base layer. In an interview with Fox Business, Miami Mayor Francis Suarez confirmed that the mining proceeds generated over $2,000 USD every 10 minutes and “over 5 million USD over the last 30 days.” Mayor Suarez praises the success of a recent initiative to fund community projects, like local climate change mitigation, programs for underprivileged communities, and investing in crypto education for tech entrepreneurs, through the earnings brought in by the MiamiCoin.

- AMC CEO Adam Aron announced via a tweet on September 15, after AMC’s second quarter earnings report released, that the company will accept Bitcoin for online ticket and concession payments by year-end 2021. Additionally, AMC “will accept Ethereum, Litecoin and Bitcoin Cash.” AMC's decision to accept cryptocurrencies as an alternative form of payment is part of a multistep plan to play offense after the company has narrowed its losses and boosted its total liquidity to a record high of more than $2 billion USD, reports Fox Business.

- According to Mike McGlone of Bloomberg Intelligence, Bitcoin is likely to surpass $100,000 by year-end. Despite Bitcoin price volatility and the recent dip in value this week, Bloomberg analyst and commodity strategist McGlone says Bitcoin could make a “significant advance in 2021” as more and more people in the mainstream begin to participate in the world’s largest cryptocurrency.

Threats

- The Nasdaq-listed cryptocurrency exchange Coinbase has dropped its plan to launch a lending program after the U.S. Securities and Exchange Commission (SEC) threatened to sue the company, report Bitcoin.com on Tuesday. The announcement came last Friday stating “Our goal is to create great products for our customers and to advance our mission to increase economic freedom in the world. As we continue our work to seek regulatory clarity for the crypto industry, we’ve made the difficult decision not to launch the USDC APY program.” In the meantime, Coinbase plans to grow its business in other ways to include filing an application with the National Futures Association (NFA) to offer futures and derivatives trading on its platform, raising $2 billion USD by selling bonds, and building Coinbase Prime, a comprehensive platform for institutional investors.

- Bitcoin.org, one of the first websites on Bitcoin (BTC), has been hacked by online scammers and down as of Thursday morning, reported Coinbase later the same day. Cobra, Bitcoin.org’s anonymous curator, announced on September 23 that Bitcoin.org was compromised and that hackers managed to put up a scam notice on the site. After disabling the website, Cobra suggested that the hackers exploited a flaw in the DNS, stating that Bitcoin.org’s Cloudflare accounts and servers were not compromised.

- Nikil Rathi, CEO of the Financial Conduct Authority (FCA) reiterated the regulator’s firm stance on cryptocurrencies during a speech in London on Wednesday. “If consumers invest in these types of products, they should be prepared to lose all their money,” he said. The FCA issued a list of five concerns consumers should keep in mind when dealing with cryptocurrencies which include consumer protection, price volatility, product complexity, charges and fees, and misleading marketing material. Additionally, the regulator told Decrypt its ban against Binance, a cryptocurrency exchange, was based on the firm’s approach (or lack of approach) to appropriate anti-money laundering standards.

Gold Market

This week spot gold closed the week at $1,750.42, down $3.92 per ounce, or 0.22%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.04%. The S&P/TSX Venture Index came in off 1.21%. The U.S. Trade-Weighted Dollar rose just 0.10%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-21 | Housing Starts | 1550k | 1615k | 1554k |

| Sep-22 | FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Sep-23 | Initial Jobless Cliams | 320k | 351k | 335k |

| Sep-24 | New Home Sales | 715k | 740k | 729k |

| Sep-27 | Durable Goods Orders | 0.7% | -- | -0.1% |

| Sep-28 | Hong Kong Exports YoY | -- | -- | 26.9% |

| Sep-29 | Conf. Board Consumer Confidence | 115.0 | -- | 113.8 |

| Sep-30 | Caixin China PMI Mfg | 49.5 | -- | 49.2 |

| Sep-30 | Germany CPI YoY | 4.2% | -- | 3.9% |

| Sep-30 | Initial Jobless Claims | 325k | -- | 351k |

| Sep-30 | GDP Annualized QoQ | 6.6% | -- | 6.6% |

| Sep-30 | Eurozone CPI Core YoY | 1.9% | -- | 1.6% |

| Sep-30 | ISM Manufacturing | 59.5 | -- | 59.9 |

Strengths

- The best performing precious metal for the week was platinum, up 4.52%. This is more related to speculation and, perhaps, to the minting of the $1 trillion coin. According to Raymond James, Wheaton Precious Metals’ investor day highlighted the company’s portfolio of assets. It has a diversified asset base (24 operating sites) with over 70% of the company’s production coming from assets that fall in the lowest cost quartile. The portfolio has over 30 years of mine life based only on reserves. The company has no debt and has a dividend linked to operating cash flows, whereby 30% of the average of the previous four quarters’ operating cash flows are distributed to shareholders.

- Uranium spot prices are blasting upward with no sign of slowing. The spot price hit $50 per pound, a 64.5% increase from $30.4 per pound on August 13, according to S&P Global Platts. Most uranium analysts point to a flurry of spot market purchases by Sprott Asset Management LP, which launched a uranium trust in July to scoop up material and give investors exposure to the price of physical uranium. "We have a uranium market completely driven by a single financial player," said Matt Zabloski, managing director of Delbrook Capital Advisors, who intends to short uranium. "Kudos to them, they've figured out a way to get people excited about the market."

- Gold shipments from Europe’s key refining hub rose to 116.4 tonnes last month from 94.1 tonnes in July, according to data on the website of the Swiss Federal Customs Administration. Sales to India climbed 93% to 70.3 tonnes and shipments to China fell 9% to 18.2 tonnes.

Weaknesses

- The worst performing precious metal for the week was palladium, down 2.18% on further prospects of delays in new car production with the ongoing chip shortage. Exchange-traded funds continued to sell, bringing this year's net sales to 7.18 million ounces, according to data compiled by Bloomberg. The sales were equivalent to $19.2 million. Total gold held by ETFs fell 6.7% this year to 99.9 million ounces.

- Spot palladium hit a 52-week low at $1,931.48 per ounce, a 4.2% decrease from the previous close. The previous low was on September 14. Spot prices declined 21% year-to-date. This is driven by the slowdown in auto demand, which reduces the demand for catalytic converters that use palladium.

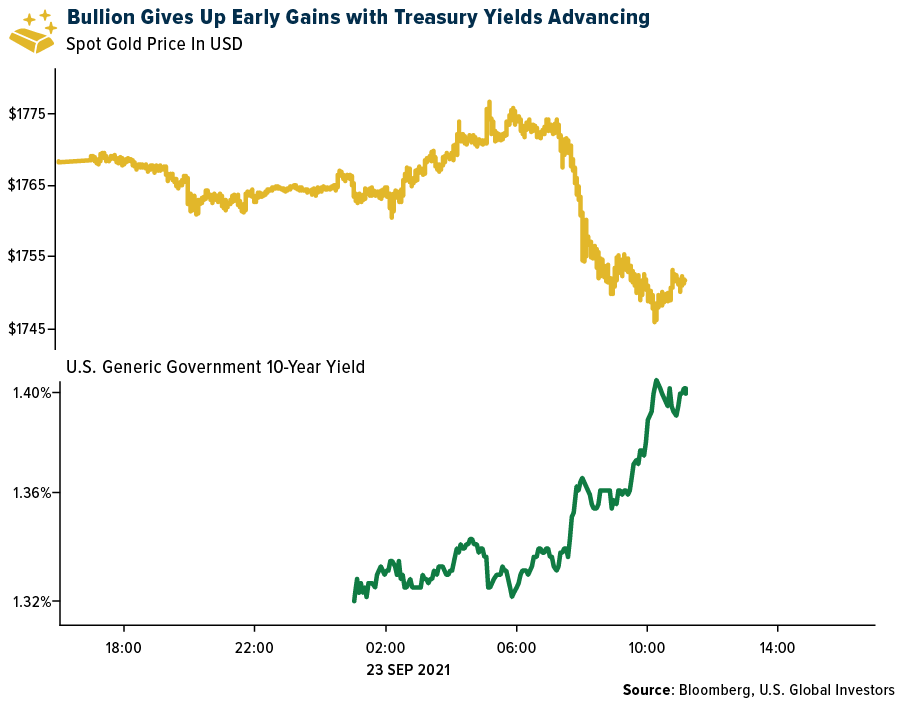

- Gold gave up early gains as Treasury yields advanced after the Federal Reserve signaled it could soon begin scaling back asset purchases. The yield on 10-year Treasuries advanced six basis points, reducing bullion’s appeal because it doesn’t offer interest. Gold also fell as rising U.S. stocks dented demand for the metal as a haven, with analysts saying the Fed outlook indicates a strong economy. Bullion has fallen more than 7% this year as the global economic recovery has raised the prospect of central banks reining in their stimulus. Traders are balancing that view against economic concerns over the resurgent pandemic and possible fallout from China Evergrande Group’s debt crisis, giving some support to gold.

Opportunities

- Red Pine Exploration said exploration drilling at its Wawa gold project in Ontario showed some high-grade gold mineralization. The company said its best results from drilling into the Jubilee shear zone on the property included 25.73 grams per ton of gold over 4.78 meters of core and 8.76 grams per ton of gold over 0.87 meters.

- With regards to platinum, one way to address the U.S. debt ceiling, would be the nuclear option. The steps as outlined by Bloomberg would go as follows: 1) The U.S. Treasury mints a platinum coin of, say, $1 trillion USD notional value. 2) The U.S. Treasury then deposits that coin into its account at the Federal Reserve. 3) With the account at the Fed now credited up to $1 trillion, the Treasury would then buy back U.S. Treasury bonds to prevent the debt ceiling from being breached. 4) This would be the equivalent of quantitative easing, with the Treasury in the role of easer -- essentially swapping reserve balances, which are not counted toward the debt ceiling, for U.S. Treasury bonds, which are. A Freedom of Information Act request showed that the Obama Administration investigated this option but did not go forward with the plan.

- Asante Gold announced a strategic investment of $5 million in Roscan Gold this past week. The management team of Asante last sold its prior gold discovery in Ghana, Cardinal Resources, to Shandong Gold and is currently bringing the Bibiani Mine back into production. Roscan has a very strategic board chaired by Sir Samuel Esson Jonah and its CEO is Nana Sangmuah, a native Ghanian. Roscan has a strategic land position in a prolific gold camp in southwestern Mali and has delivered some impressive grades and intercepts.

Threats

- South African courts recently set aside mining regulations that govern black ownership targets for companies. In 2018, it was ruled that the ownership target of 26% should remain in perpetuity. If the government decides to appeal the decision, then that would reintroduce uncertainty for investors while the status is a big plus.

- Sibanye Stillwater expects South African output of rhodium to decline 9% to 690,000 ounces by 2030, the company says in a presentation on its website. Sibanye says platinum output from South Africa, the world’s No. 1 producer, may drop to 5.7 million ounces in 2030 from 6 million ounces in 2019.

- Mining companies in South Africa are considering spending as much as 40 billion rand ($2.7 billion) to construct 2,000 megawatts of power generation capacity, said Roger Baxter, chief executive officer of Minerals Council South Africa. Mining companies have been pushing to develop their own power plants because of persistent power cuts imposed by state power utility Eskom Holdings SOC Ltd. They are also keen to move away from total reliance on the mainly coal-fired power supplied by Eskom as their investors pay more attention to climate change issues.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits