What Is Shadow Inflation? It Could Be More Prevalent Than You Realize

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe’re all familiar with inflation, whether it’s at the grocery store or gas pump. What cost you $10 last year might cost you $12 or more today, representing a hidden “tax” that steadily corrodes your purchasing power like rust on iron.

But did you realize there’s another form of inflation that’s just as corrosive and yet is nearly impossible to measure? Some economists call it “shadow inflation,” and it refers to instances when you pay the same price for a good or service one year to the next, but the quality or quantity has diminished.

Many companies, faced with paying higher prices for materials, labor and transportation, pass some or all of the extra costs on to customers. Others opt to charge the same as before but cut back on certain things.

Ever felt like you’re being gypped on potato chips in the bag you just bought? Or that your hotel room isn’t cleaned as well or as frequently as you once remembered? Granted, it could just be poor customer service. Or it could be shadow inflation.

CPI: Fact or FUD?

Shadow inflation is yet another indication that the traditional consumer price index (CPI), as provided by the U.S. Bureau of Labor Statistics (BLS), isn’t telling you the full story. Last year, I suggested the CPI might be fake news. I would also describe it as FUD, or fear, uncertainty and doubt.

This week the BLS reported that consumer prices rose 5.4% in September compared to the same month last year. That’s the highest such rate since 2008. But real inflation could be even higher if we measure it using the BLS’s methodology from 1980. According to that yardstick, consumer prices increased a whopping 13.4% in September. (Thank you, again, to John Williams’ Shadow Government Statistics for the data.)

And there could be even higher inflation on the way. Brent crude oil, the international benchmark, touched $85 a barrel today for the first time since October 2018, with Russian president Vladimir Putin saying $100 oil is “quite possible” before year end.

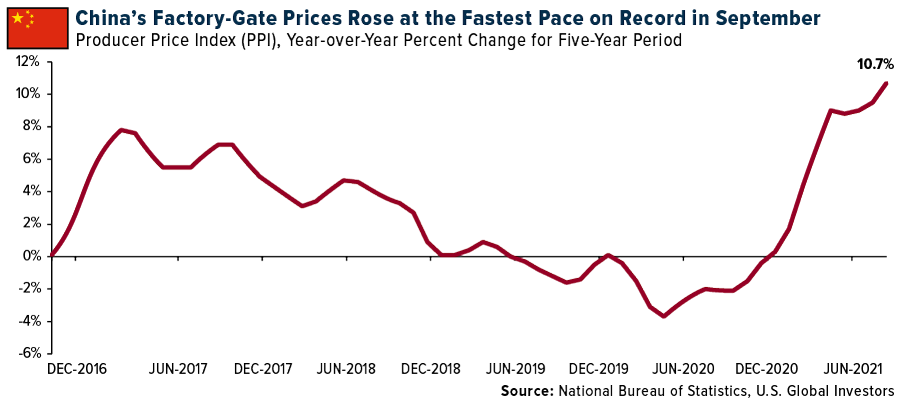

Meanwhile, factory-gate prices, or prices that distributors pay manufacturers for finished goods, rose at a record pace in China last month as worker shortages and shipping bottlenecks continued to gum up the global supply chain. Year-over-year, China’s producer price index (PPI) increased 10.7%, the fastest pace on record. These higher rates will most certainly spread across the globe, from wholesalers to retailers to end consumers.

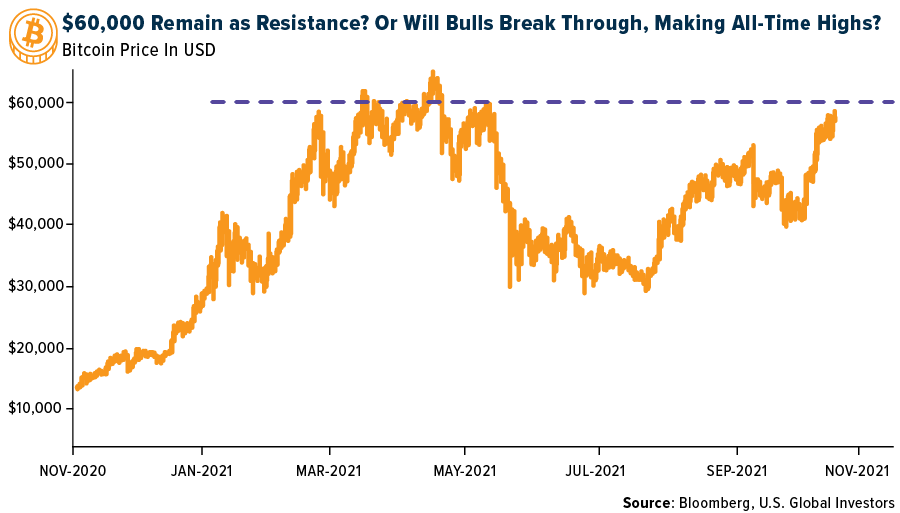

Gold Hit $1,800, Bitcoin at $61,000

No one can say for certain how long this current period of inflation will last, but I believe it’s only prudent to make sure you have exposure to gold and Bitcoin at this time. Both haven assets responded positively this week to news that inflation may not be so “transitory” as the Federal Reserve would have us believe.

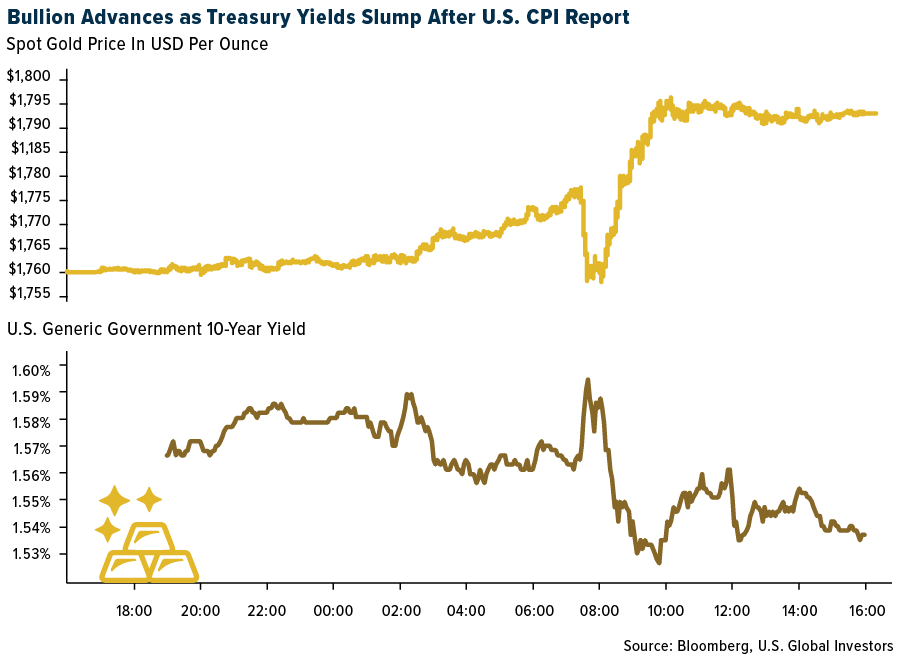

Following the CPI report, gold touched $1,800 an ounce in intraday trading, the first time we’ve seen that level in about a month.

As for Bitcoin, the crypto topped $61,000 on Friday on its quest to surpass its all-time high of $64,863, set in April 2021. Contributing to the price surge was news that the Securities and Exchange Commission (SEC) is finally set to allow Bitcoin futures ETFs to begin trading in the U.S., possibly as early as next week. Up until this point, the agency has blocked all efforts to launch such an ETF, despite incredible pent-up demand from investors. Bitcoin to $100,000 by Year End? On a final note, I returned this week from Dubai, where I attended and spoke at the AIM Summit, a gathering of some of the world’s leading investors and thought leaders on alternative assets. This year, a lot of the buzz was on crypto miners, including HIVE Blockchain Technologies.

Bitcoin to $100,000 by Year End?

On a final note, I returned this week from Dubai, where I attended and spoke at the AIM Summit, a gathering of some of the world’s leading investors and thought leaders on alternative assets. This year, a lot of the buzz was on crypto miners, including HIVE Blockchain Technologies.

I was extraordinarily impressed with Dubai, by the way. It’s right up there with Singapore and Hong Kong, perhaps even more so. Many of the city’s futuristic skyscrapers and other buildings are the work of Canadian infrastructure company Brookfield Properties.

To attract business and workers, the city has a tax-free zone that uses common law for corporate dealings. But across the street, they use Sharia law.

Unless you’re a big drinker, Dubai is relatively affordable, which is why many young people from Canada and elsewhere go there to find employment. That and, oh, income is entirely tax-free.

But back to crypto and the AIM Summit. Sentiment was very strong for Bitcoin, with some presenters and attendees talking about $100,000 by year end due to a number of reasons, including negative bond yields, rising inflation, institutional participation and general widespread adoption. Robinhood, PayPal and other platforms that allow you to buy fractional shares of coins have made investing in cryptos much more doable for a great number of people.

I can’t promise $100,000 Bitcoin by year end, but I can say it’s definitely plausible, mathematically. The crypto has a 10-day standard deviation of ±14, so a jump to $84,000 is possible by Halloween. After that, we could see $100,000 and beyond.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.58%. The S&P 500 Stock Index rose 1.81%, while the Nasdaq Composite climbed 2.18%. The Russell 2000 small capitalization index gained 1.58% this week.

- The Hang Seng Composite gained 1.71% this week, while the KOSPI rose 1.99%.

- The 10-year Treasury bond yield fell 4 basis points to 1.57%.

Airline Sector

Strengths

- The best performing airline stock for the week was Norwegian Air Shuttle, up 9.4%.. Delta reported third quarter adjusted earnings per share (EPS) of $0.30, better than the consensus of $0.15. The best versus consensus was primarily due to a combination of higher than-expected revenue and better non-operating expenses.

- Global ticket sales are showing signs of accelerating. In the most recent data, international tickets finally showed life and improved to down -41.1% (versus -48.8% last week), which is a level only slightly behind the summer highs. Similarly, domestic tickets sold took a sizable step up to -27.6% versus 2019 levels compared to -36.4% last week but remains off its June/July average of -19% versus 2019 levels. Domestic leisure (bookings through online channels) and corporate (bookings through large travel agencies) both stepped up to -5.2% (versus -16.4% last week) and -54.6% (versus -60.3% last week), respectively.

- American Airlines published an investor update guiding third quarter revenue to the better end of its prior guidance range and adjusting its capacity outlook in addition to costs. The company now expects revenue to be down 25% versus 2019 levels, towards the better end of prior guidance of down 24% to down 28%.

Weaknesses

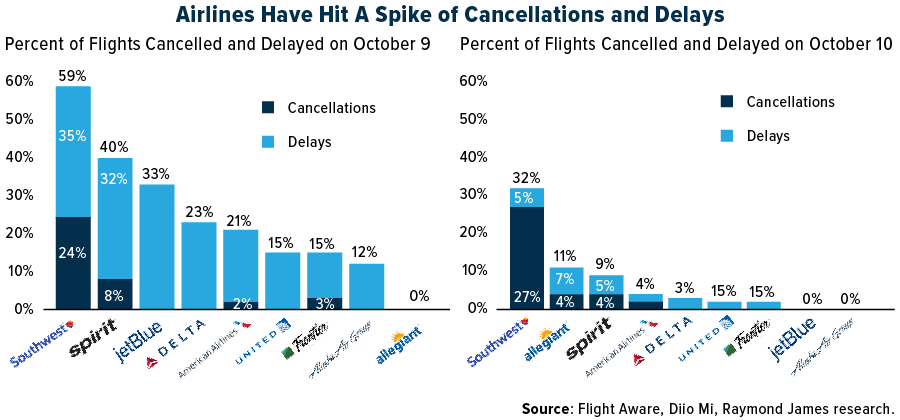

- The worst performing airline stock for the week was Sun Country, down 8.5%. Operational issues appear widespread across the industry, albeit more acute at Southwest with 59% of its Saturday flights either canceled or delayed. Spirit and JetBlue stood at 40% and 33%, respectively. Moreover, as of Sunday morning, operational issues lingered at Southwest to a much greater degree than any other U.S. airlines.

- A passenger who triggered a plane's emergency landing at LaGuardia Airport will not face charges as authorities characterized the incident as a "misunderstanding." Officials say the incident happened on American Eagle Flight 4817. According to Port Authority officials, passengers on Flight 4817 reported "suspicious behavior" from another passenger. Once the plane landed safely, passengers rushed to get off -- pushing each other down the slides. "We landed really hard and then out of nowhere people were screaming in the back of the airplane," the passenger said. "Some guy apparently may have had a bomb on him. It was a suspicion of a bomb and then everyone was just shoving and pushing, jumping out of the airplane".

- Airline shares declined on investor fears that a surge in oil prices will inflate the price of jet fuel over the coming winter months, undermining a recovery in air travel. Oil markets are tightening ahead of the Northern Hemisphere winter, with crude topping $80 a barrel for the first time since 2014. With shortages of natural gas and coal increasing the possibility of a full-blown energy crisis, analysts say it could go higher.

Opportunities

- The U.K. government removed 47 countries from its 'red list' in a boost to long-haul international travel. Travelers returning from red list countries need to quarantine in a hotel for 10 days. Only 7 countries remain on the list. Importantly, the U.K. has extended vaccine recognition for travel to a further 37 countries, which should encourage inbound travel.

- U.S. ticket sales stepped up this week to -56.4% versus 2019 levels for the week versus last week's level of -63.7%. Leisure demand showed a stronger improvement than corporate demand, which could point to a solid upcoming holiday season. Leisure consumers typically concentrate travel around Thanksgiving and Christmas.

- A new survey shows that significantly more people plan to travel during the holidays this year than in previous years. According to PWC's 2021 Holiday Outlook, 52% of respondents said they plan to travel during the holidays this year, which is far more than the historical one-third of respondents. The survey shows that the majority (72%) will travel by car, and 57% of those with household incomes above $150,000 plan to travel by airplane. Almost 60% of consumers stated they are concerned about the lingering effects of the pandemic and Covid variants, but consumers are still optimistic about holiday activities this year.

Threats

- Jet fuel has surged 20% versus the third quarter average. Fuel expense accounts for 25% of airlines’ expenses. If prices remained at October levels, this would on average imply a 4.5-point margin headwind.

- Southwest and American Airlines, both based out of Texas, said they’d still mandate COVID-19 vaccines a day after Gov. Greg Abbott signed an executive order banning any entity from requiring the vaccine. “We’re reviewing all guidance issued on the vaccine and are aware of the recent order by Governor Abbott. “According to the President’s Executive Order, federal action supersedes any state mandate or law, and we would be expected to comply with the President’s Order to remain compliant as a federal contractor,” Southwest spokesperson Brandy King said in a statement to Insider.

- Budget airline Ryanair has been accused of “outrageously” blocking customers from its flights unless they repay money previously refunded for canceled trips. Holidaymakers have said their plans were left in tatters after the airline informed them that they would be unable to fly unless they paid Ryanair money previously refunded via credit card “chargebacks.” It is believed thousands used the consumer credit rules after they were unsuccessful in getting money back directly from the airline for trips disrupted by the coronavirus.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Hungary, gaining 1.6%. The best performing country in Asia this week was the Philippines, gaining 4.0%.

- The Polish zloty was the best performing currency in emerging Europe this week, gaining 1.0%. The Thailand baht was the best performing currency in Asia this week, gaining 1.5%.

- China released stronger economic data this week. September’s trade balance increased to $66.67 billion from $53.3 billion in August versus the expected $45 billion. Exports rose and imports declined.The Money supply in China remains strong. Inflation increased by 0.7% versus the expected 0.8% and the prior 0.8%. The Producer Price Index, however, spiked to 10.7% in September versus the expected 10.5% and the prior 9.5%.

Weaknesses

- The worst performing country in emerging Europe for the week was Romania, losing 0.57%. The worst performing country in Asia this week was China, losing 0.40%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 2.6%. The Philippines peso was the worst performing currency in Asia this week, losing 0.21%.

- Industrial production in Turkey increased 5.4% month-over-month in August. On year-over-year basis, the industrial production increased by 13.8%, above the expected 10.5%.

Opportunities

- This week during the energy week in Russia, President Vladimir Putin has said that Russia will target carbon neutrality by 2060. He ordered the development of a carbon strategy in June and signed a climate law in July creating a framework for green projects. It will be a costly but necessary project to move energy producers heavily dependent on fossil fuels into more environment-friendly operations. Currently, Russia has been focused on putting extra money in its wealth fund from the sale of oil and gas for years. The government now predicts Russia’s wealth fund will break $300 billion in 2024, up from $190.5 billion now. These savings could be used for the energy transition into renewable energy sources.

- The Eurozone is set to become the largest player in green bonds. Bloomberg reported that the EU registered over €120 billion euros ($139.12 USD), starting with the sale of the first €12 billion out of the planned €250 billion in the next 15 years. UniCredit commented that the Eurozone will be the largest and most liquid green bond market.

- Higher energy prices and strong energy demand will support economic growth in Russia as most of the country’s revenue comes from the sale of oil and gas. This week, Russia held an energy summit during which President Putin said that his country is ready to transport more gas to Europe to ease the energy crunch. He also said the oil price could rise to $100 per barrel. Crude oil Brent trades at around $84 per barrel presently.

Threats

- The Turkish lira sank to a fresh record low against the dollar. President Erdogan fired three central bank policy makers who disagreed with his idea that cutting interest rates will bring inflation lower. Inflation in September spiked to 19.6% on an annual basis. The one-week repo rate was unexpectedly cut by 100 basis points to 18% at the last policy makers meeting. Next rate decision will take place on October 21. Most likely the one-week repo rate will be cut again by 100 basis points putting more downward pressure on the lira.

- Evergrande, the troubled Chinese property developer, which missed coupon payments in the past few weeks is due to pay $18.9 million on interests by October 19. The company has a 30-day grace period before any missed payment would constitute default, but next week Evergrande officially can be in default if there is no cash injection. Chinese property developers are responsible for about half of the world’s distressed dollar bonds. Of the $139 billion USD of dollar-denominated bonds trading at distressed prices, 46% were issued by companies in China’s real estate sector, according to data collected by Bloomberg.

- Higher energy prices and high demand prompted by the Chinese government restricting some power usage. China’s main source of energy is coal and record high floods in China continue to keep supply tight. This week local media reported two large mines in Shaanxi province had been impacted by heavy rainfalls adding to closures already in place in neighboring Shanxi province where 60 of 682 mines were temporally closed.

Energy and Natural Resources Market

Strengths

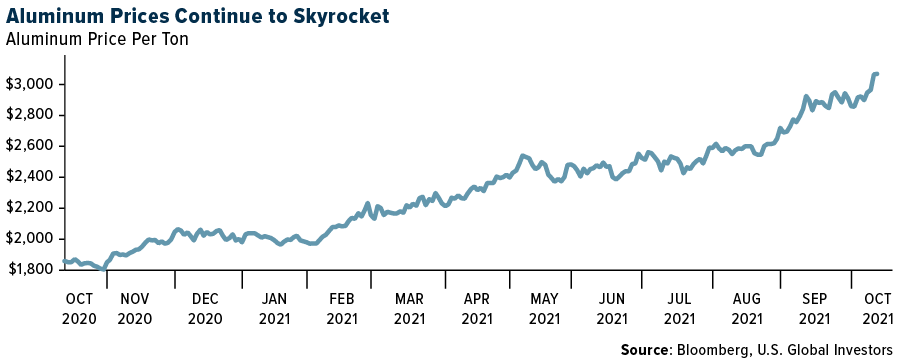

- The best performing commodity for the week was zinc, up 13.07% on power curtailments to refining more processed metal. Aluminum prices rose on Monday to their highest since 2008 due to increases in costs of energy and raw materials used to make the metal and output cuts by the biggest producer, China. China’s production, already curbed by a government anti-pollution drive, has been further hit by power shortages gripping the country.

- Crude topped $81 a barrel as the global power crunch boosts demand for oil ahead of winter. West Texas Intermediate futures climbed 2.7% to the highest level since October 2014. The prices of fuels such as coal and natural gas are soaring in Europe and Asia as stockpiles run low before the Northern Hemisphere winter, prompting a switch to oil products such as diesel and kerosene.

- Iron ore futures in Singapore have suddenly gone from commodity laggard to a top performer, with resurgent prices further fanning inflation fears that are rippling across the world. Futures have climbed 50% in just three weeks, joining gains in aluminum to energy as rising demand, stalled supply lines and climate policy send an index of raw materials to the highest ever.

Weaknesses

- The worst performing commodity was uranium, down 6.89% for the week. There has been little interest from generalist portfolio managers in recent weeks for oil and gas stocks. Most incremental buyers appear to be attracted to yields. As consensus earnings estimates market-to-market higher commodity prices, 2022 earnings numbers should still go higher. Consensus WTI is $67 per barrel in 2022. The forward curve is $74/barrel today. The consensus Henry Hub gas price is $3.70/Mcf and the forward curve for 2022 is $4.40/Mcf.

- California will soon ban the sale of new gas-powered leaf blowers and lawn mowers, a move aimed at curbing emissions from a category of small engines on pace to produce more pollution each year than passenger vehicles. Governor Gavin Newsom signed a new law on Saturday that orders state regulators to ban the sale of new gas-powered equipment using small off-road engines, a broad category that includes generators, lawn equipment and pressure washers. California has more than 16.7 million of these small engines in the state, about 3 million more than the number of passenger cars on the road.

- India will provide an additional 287 billion rupees ($3.8 billion USD) to fertilizer companies as compensation for selling products at lower than market prices to farmers, a government statement said. The proposal is also to partly offset the increase in international prices of DAP (18% Nitrogen and P2O5 46%) and nitrogen, phosphorus and potassium fertilizers. The increased fertilizer subsidy in the current financial year will boost spending to over 1 trillion rupees from 800 billion rupees allocated in the federal budget.

Opportunities

- Oil prices, around $80 a barrel, are once again spurring a revival of shale drilling in America’s biggest oil field, where production is expected to return to pre-pandemic highs within weeks. Only this time, the surge is being driven by private operators, rather than the publicly traded companies that fueled the previous booms. Increased access to financing and strong oil demand has created an opening for closely held producers, most of whom are backed by private equity, to ramp up output in West Texas and southeast New Mexico.

- Steel demand should climb again next year, even as a deepening energy crisis threatens the global economy’s recovery from the pandemic, according to the World Steel Association. Consumption will rise 2.2% to 1,896 million tons in 2022, a slower pace than this year’s 4.5% increase, the industry group said Thursday.

- The U.S. urea prices jumped from $63/mt sequentially to $683/ton (versus last year’s levels of $222/ton) as robust demand, plant closures, record-high gas costs in Europe, and expectations for further India tenders have buyers succumbing to strong prices. U.S. Midwest potash prices rose from $72/ton last week to $777/ton and Brazilian prices surged form $10/ton this week to $765/ton (versus last year’s levels of $239/ton).

Threats

- The British steel industry’s lobby group warned on Monday of an impending crisis due to soaring wholesale energy prices, which could force plants into expensive shutdowns, stoke emissions and sow chaos through supply chains. A shortage of natural gas in Europe had sent prices for electricity and gas soaring, triggering sharp rises in the prices paid by major heavy industrial plants smelting steel. “These extraordinary electricity prices are leading to smaller or wiped-out profits and thus to less reinvestment,” U.K. Steel, which lobbies on behalf of the British steel industry, said in a briefing document.

- The global energy crisis is casting a pall over copper, as investors who are bullish on its long-term prospects fret that power shortages and factory slowdowns could trigger a retreat in the near term. The chairman of the world’s top copper miner warned that the market may not scale new highs in the short term due to uncertainty over the macroeconomic outlook. “Most people are saying we could face some volatility in the very short term,” Codelco Chairman Juan Benavides said in an interview, listing concerns including inflation, energy prices and logistics bottlenecks. “A lot of people are talking about what central banks or government will be doing in the very short term.”

- Eyes will be on Washington throughout the reconciliation process. Investors’ attention will be on the potential for master limited partnerships (MLPs) to pay taxes. However, the Biden administration is potentially looking to expand the definition of MLPs to include renewables. If MLPs must pay taxes it would be a net negative from a cash flow perspective but could result in C-Corp conversions. Investors are also paying attention to potential changes to swap treatment. Should this come to fruition the net impact would likely be reduced liquidity.

Domestic Economy and Equities

Strengths

- Initial jobless claims dropped more than expected last week to 293,000 from an upwardly revised 329,000, continuing the downward trend that was overturned in September.

- Banks posted strong results this week. Bank of America reported earnings and revenue that exceeded Wall Street estimates. Wells Fargo & Co.’s quarterly profit spiked 59%, boosted by the release of money set aside for losses during the pandemic. Morgan Stanley booked stronger-than-expected results as its wealth management division added a record amount of assets.

- Freeport-McMoRan, global copper and gold producer, was the best performing S&P 500 stock for the week, increasing 13.45%. The company begun construction of the world’s biggest single-line smelter that could create 40,000 jobs in Indonesia. Analysts expect Freeport Indonesia to report higher revenue and net income due to surging copper prices.

Weaknesses

- Inflation increased to 5.4% in September from 5.3% in August. Producer-price inflation picked up to 8.6% last month from 8.3% on supply-chain woes, a little slower than expected.

- NY State Empire Manufacturing Index, which measures how the people who run companies in New York state feel towards the economy, dropped to 19.80 in October from 34.3 in September, whereas 25.0 was expected.

- Align Technology, s medical company, was the worst performing S&P 500 stock for the week, losing 8.68%. Its shares dropped 6.2% on Wednesday after Stifel analyst Jonathan Block warned about weaker revenue.

Opportunities

- This week’s stocks moved higher. Most likely, the recent pull back in equities is overdone, sparking the ‘buy at the dip’ investment strategy. Equities should rise on stronger economic data. Despite more talk about an upcoming taper, monetary policy is still supportive. The Federal Open Market Committee (FOMC) minutes said rates could hold near lower bound for the next several years.

- Bloomberg reported that the market cap of the Russell 3000 that comprises about 98% of the market — offering a proxy for the universe of U.S. stocks — is now around $47.7 trillion. That’s more than the combined gross domestic product of the U.S., China, Japan, Germany and the U.K. That means workers in the five biggest economies would have to combine all their output for a whole year just to buy every stock in the Russell 3000.

- The Manufacturing PMI should remain well above the 50 level that separates growth from contractions. Bloomberg economists predict the preliminary Manufacturing PMI to be released at 60.5, slightly lower than the August reading of 60.7.

Threats

- Federal Reserve officials broadly agreed they should start tapering in mid-November or December, according to the minutes from their September meeting. The program could then end by mid-2022. The inflation outlook was raised in the near term.

- Industrial production most likely will weaken. Bloomberg economists expect September industrial production to tick up only by 0.2%, down from 0.4% in August. Data will come out next week, on October 18.

- Amazon appealed a record 746 million-euros penalty for allegedly violating the European Union’s though data-protection rules. The company is being probed by the EU over its use of data from sellers on its platforms and whether it unfairly favors its own products. The EU law allows the fines to be as much as 4% of company’s annual global sales.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was GreenMoon (GRM), rising 460,763,129.80%.

- ETF giant Invesco partners with crypto billionaire Michael Novagratz’s Galaxy Digital holdings to bring two ETFs to market. Tickers SATO and BLKC began trading last Thursday on Cboe Global Markets. Both ETFs are among nearly a dozen of crypto-themed ETFs that issuers are seeking regulatory approval for, published Bloomberg in an article this week.

- The world’s largest digital currency, Bitcoin, rose about 3% this Friday – taking the rally to over 35% since this summer after Bloomberg reported that the SEC looks to allow the country’s first futures-base cryptocurrency ETF.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was StrikeCoin (STRIKE), down 99.45%.

- Jamie Dimon, CEO of the largest bank in the U.S. by market cap, JPMorgan Chase, calls Bitcoin futile. “I personally think that Bitcoin is worthless,” says Dimon during an Institute of International Finance (IIF) event reported by Bloomberg.

- Coinbase Global (Ticker: COIN) was rated underperformed with a $160 price target at Autonomous Research. An article by CoinDesk states that the reason for the underperformance rating is due to the lack of crypto innovation. Coinbase is losing market share to other exchanges wrote a research analyst at Autonomous Research.

Opportunities

- The U.S claims Bitcoin mining crown following China’s crackdown. According to Cambridge Centre for Alternative Finance, the U.S accounts for 35.4% of the global hashrate. The Chinese crackdown has driven firms to see the need to spread their operations around rather than having a centralized location, writes an article by CoinDesk.

- Bitcoin $60k resistance hits at ‘buy the dip’ opportunity before all-time highs. Order book data are repeating behaviors from August; in other words, more sellers are demanding higher prices for BTC, reports CoinTelegraph.

- A MakerDAO delegate is leading the charge to educate lawmakers about Decentralized Finance (or DeFi for short). Paper Imperium, the most powerful member of the DAO, controls 3% of the voting rights for the protocol and has been building a network of bankers, politicians and policymakers to educate and encourage adoption.

Threats

- Traders pilling into overvalued crypto funds risk a painful exit, writes Bloomberg Businessweek. It’s possible for a crypto trust to issue new shares, but it has no ability to redeem them – a key reason the trust’s prices stray away from the value of Bitcoin. “A pretty significant premium can quickly reverse and become a sizable discount when people begin selling” says Ben Johnson, Morningstar Inc’s global director of ETF research.

- Tether is crypto’s biggest danger, not China or the SEC. Tether’s biggest claim is that all USDT is back to a 1:1 ratio by the U.S dollar, however, Bloomberg Businessweek has shed some light in the charades Tether has been playing for years. Bitfinex has been taking hundreds of millions of Tether’s USD reserves for money it lost in shady deals. Tether has been investing their reserves in short-term Chinese loans, which experts describe as very dangerous. There’s also $1 billion lent to Celsius Network, a cryptocurrency lending company, that is being booted out of the U.S by regulators. The billions in profits go to Tether executives. But if there was ever to be a catastrophic loss resulting from such investments, it’s the USDT holders and the broader market that would feel the aftershock.

- Mexico rules out accepting crypto as legal tender. An article published by CoinTelegraph states that The Bank of Mexico and the National Banking and Securities commission warned financial institutions not to deal with digital assets. The President said the country is unlikely to follow in El Salvador’s footsteps by adopting Bitcoin as legal tender.

Gold Market

This week spot gold closed the week at $1,767.62, up $10.49 per ounce, or 0.60%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 6.28%. The S&P/TSX Venture Index came in up 6.86%. The U.S. Trade-Weighted Dollar fell 0.12%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-12 | Germany ZEW Survey Expectations | 23.5 | 22.3 | 26.5 |

| Oct-12 | Germany ZEW Survey Current Situation | 28.0 | 21.6 | 31.9 |

| Oct-13 | Germany CPI YoY | 4.1% | 4.1% | 4.1% |

| Oct-13 | CPI YoY | 5.3% | 5.4% | 5.3% |

| Oct-14 | Initial Jobless Claims | 320k | 293k | 326k |

| Oct-14 | PPI Final Demand YoY | 8.7% | 8.6% | 8.3% |

| Oct-17 | China Retail Sales YoY | 3.5% | -- | 2.5% |

| Oct-19 | Housing Starts | 1610k | -- | 1615k |

| Oct-20 | Eurozone CPI Core YoY | 1.9% | -- | 1.9% |

| Oct-21 | Initial Jobless Claims | 302k | -- | 293k |

Strengths

- The best performing precious metal for the week was platinum, up 2.92%, largely moving with the Thursday surge in precious metals. Palladium surged to the highest level in a month as industrial users took advantage of low prices even as the ongoing semiconductor crunch dampens the outlook for auto demand.

- Royal Gold streaming sales were 64,000 gold equivalent ounces, 8% higher than consensus. Outperformance versus consensus was attributable due to higher silver sales, where the company previously reported deferred ounces from Pueblo Viejo which would increase following recovery improvements at the operation.

- Gold rose to the highest in nearly a month as Treasury yields and the dollar slumped amid concerns rising prices may hinder a nascent economic recovery. The yield on the 10-year Treasury note fell after an initial increase following a U.S. inflation report that showed a faster-than-expected rise in consumer prices last month. The greenback dipped to a session low. Both movements are helping boost demand for non-interest-bearing bullion. However, profit taking on Friday trimmed the weekly gain.

Weaknesses

- The worst performing precious metal for the week was palladium, off 0.12% by the end of the week as Friday’s price action wipe away the potential weekly gain. Dundee Precious Metals reported preliminary production results for the third quarter, with consolidated gold output of 71,700 ounces, (missing the consensus of 77,800 ounces). Chelopech had sequentially lower production at 38,400 ounces because of lower grades.

- Top palladium producer MMC Norilsk Nickel PJSC further cut its outlook for the metal’s shortages as a semiconductor supply crunch weighs on demand in the key auto sector. Norilsk Nickel now sees palladium’s shortage totaling 200,000 to 300,000 ounces this year, down from a previous estimate of 400,000 to 500,000 ounces. For next year, the deficit may be 300,000 ounces, compared with the last outlook for a 700,000-ounce deficit.

- Exchange-traded funds (ETFs) cut 86,759 troy ounces of gold from their holdings in the last trading session, bringing this year's net sales to 8.3 million ounces, according to data compiled by Bloomberg. This was the eighth straight day of declines, the longest losing streak since August 26. Total gold held by ETFs fell 7.8% this year to 98.8 million ounces, the lowest level since May 15 of 2020

Opportunities

- Newcrest announced that the Newcrest Board has endorsed the Red Chris Block Cave Pre-Feasibility Study and approved its progression to the Feasibility Stage. The study confirms Newcrest's original investment thesis of unlocking the underground portion of this Tier 1 deposit by leveraging Newcrest's industry-leading block-caving expertise and developing the asset to become a mainstay of Newcrest's portfolio. The study is the first technical report issued by Newcrest on Red Chris since its acquisition of a 70% interest and operatorship in August 2019. The project is expected to average annual production of 316,000 ounces gold and 80,000 tons per year copper production from Macro Block 1 in the fiscal year 2029 to 2034. Capital cost to develop the project is estimated at $2.1 billion USD. Based on this production and cost profile, the company estimates a 17% internal rate of return (IRR) and $2.3 billion USD net present value (NPV) over a 31-year mine life. Longer mine lives versus short-term mines are becoming more desirable. Juniors controlling such assets are likely to attract the interest of majors.

- This morning Superior Gold released third quarter production that beat consensus estimates (19,400 ounces Au actual versus the consensus of 17,000 ounces Au). This sets up the company well for the upper half of 2021 production guidance. Open pit mining is progressing on schedule, with grades materially increasing sequentially. This should help the company reliably increase production.

- Aya Gold & Silver cited production of 338,624 ounces of silver in the third quarter, a 198% increase compared to 113,655 ounces silver in the third quarter of 2020. Aya Gold & Silver also increased 2021 production guidance to 1.55 million ounces silver, a 29% increase over initial guidance of 1.20 million ounces silver.

Threats

- According to Raymond James, they expect margin compression in the third quarter, as average gold, silver, and copper prices declined sequentially while inflationary pressures negatively impact operating costs. They expect the margin compression to be partially offset by improving production levels sequentially, particularly for the gold producers.

- Barrick Gold production of 1.09 million ounces was 3% below consensus. Weaker results reflect prior disclosed challenges at the Nevada operations (e.g., Carlin roaster repairs) and at Hemlo (e.g., COVID-19 concerns). The latest production report suggests third quarter earnings-per-share (EPS) could come in at $0.24/share, below the consensus of $0.31/share. National Bank Financial expressed concern that the share price could remain under pressure until operational performance is stabilized, which the market will want a couple quarters of proof before the shares could rerate.

- According to Goldman Sachs, palladium and platinum have corrected materially from their year-to-date highs due to the severe disruption in global auto production due to chip shortages. They now expect both metals to be in surplus in 2021-22. Beyond that, they think both markets are on their way to a structural rebalancing as the price differential leads to thrifting and the substitution of palladium and a greater use of platinum. In their base case of broadly balanced markets beyond 2022, they expect a large palladium premium over platinum to persist due to divergence in above-ground stock levels and the need to continue to incentivize substitution..

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All