Walmart Now Has Bitcoin ATMs? Five Bitcoin Developments from the Past Week

Membership required

Membership is now required to use this feature. To learn more:

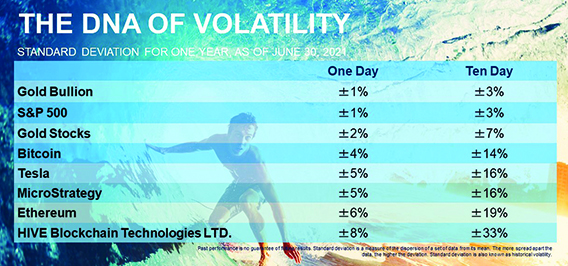

View Membership BenefitsBefore I get around to Walmart, I want to address the recent pullback in Bitcoin and Ether prices since Bitcoin hit a new record high. Shares of publicly listed crypto miners also fell this week. It’s important for investors to remember that the crypto ecosystem remains, and is expected to remain, highly volatile.

Whereas gold bullion and the S&P 500 have a standard deviation of ±1% over a single trading day, Bitcoin has one closer to ±4%. Ether’s is even higher at ±6%, and HIVE Blockchain Technologies can easily go up or down 8% during any given trading session.

Needless to say, the crypto ecosystem is high-risk and potentially high-reward, and it’s essential that investors who are thinking of participating manage their expectations.

There’s much more to cover from the week that was! Below are five Bitcoin developments you need to know.

1. The first Bitcoin ETF was also the fastest to $1 billion in assets

Many of you reading this may be aware that Wall Street finally got a Bitcoin-linked ETF. The ProShares Bitcoin Strategy ETF (BITO), which tracks the performance of Bitcoin futures contracts, was first out of the gate on Monday, mere days after the Securities and Exchange Commission (SEC) said it would no longer block the issuance of investment products related to the digital asset.

But that’s not the only record BITO now holds. The ETF attracted over $1 billion in as little as two days after its debut, making it the fastest ever to reach that milestone. The previous recordholder, appropriately enough, was State Street’s SPDR Gold Shares ETF (GLD), launched in 2004. It took the popular gold-backed ETF three days to reach $1 billion in assets.

BITO may be the first, but it will hardly be the last. A second Bitcoin futures fund, the actively managed Valkyrie Bitcoin Strategy ETF (BTF), became available for trading today.

Having said that, not everyone is jumping to buy a Bitcoin futures contract. Of the nearly 700 people who took a recent HIVE poll, more than three quarters said they were either “probably” or “absolutely” not interested in an ETF that tracks the futures market. Presumably they are holding out for a Bitcoin spot ETF, or they would prefer to own the crypto outright.

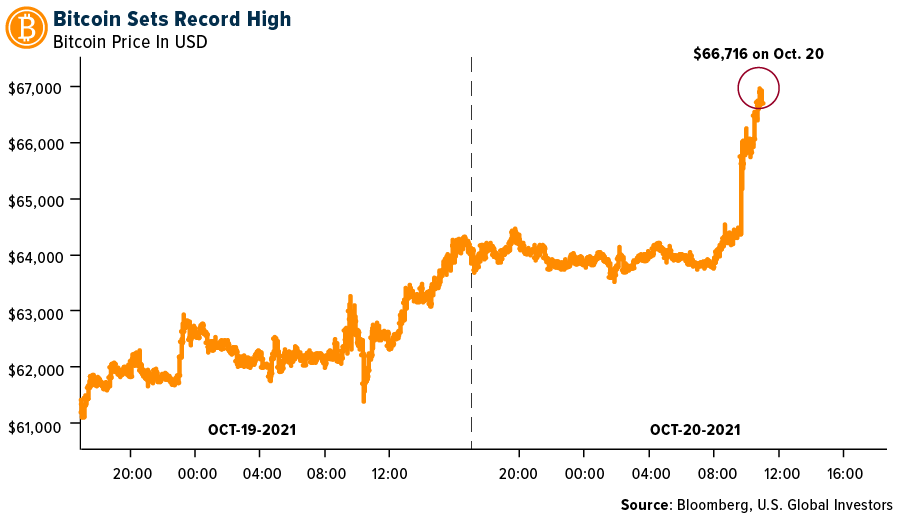

2. Bitcoin’s all-time high price has reignited speculations of $100,000

The price of Bitcoin topped $66,000 for the first time on Wednesday, pushing its market cap above an incredible $1.3 trillion. The surge was driven largely by the debut of BITO as well as the undeniable power of FOMO, or fear of missing out.

This has reawakened speculation that the crypto is headed for $100,000, perhaps as early as year’s end. Take a look at the logarithmic chart below. Each horizontal line represents a growth factor of 10.

Arithmetically, there are a lot of numbers in between $66,000 and $100,000, but geometrically, it’s a hop and a skip.

3. A public U.S. pension fund bought Bitcoin and Ether

BITO wasn’t the only love Bitcoin got from institutional investors this week. For the first time ever, a U.S. pension fund has invested in the space. On Thursday, the $5.5 billion Houston Firefighters’ Relief and Retirement Fund (HFRRF) announced that it had purchased $25 million in Bitcoin and Ether, representing a “watershed moment for Bitcoin and its place in public pensions,” according to Nate Conrad, Global Head of Asset Management at New York Digital Investment Group (NYDIG), which facilitated the purchase. “Fiduciaries are increasingly aware of how even a small allocation to digital assets can make a big impact over time,” Conrad went on.

Like BITO, this allocation may be the first of its kind, but I don’t believe it will be the last. Imagine what would happen to Bitcoin and Ether’s price if the approximately $440 billion California Public Employees’ Retirement System (CalPERS), the largest such fund in the U.S., got involved.

4. Walmart now has Bitcoin ATMs, with plans for thousands more

Bitcoin’s been called lots of things over the years. It’s “worse than tulips.” It’s a bubble. Warren Buffett described it as “rat poison squared.” More recently, JPMorgan CEO Jamie Dimon said it’s “worthless.”

Well, now nearly anyone will be able to convert their loose change into “worthless” Bitcoin at their neighborhood Walmart. This week, it was being reported that Walmart quietly began installing special Coinstar machines at select locations that give customers the option to buy Bitcoin.

Some 200 kiosks are currently available at the giant retailer, but according to Bloomberg, there are plans to install as many as 8,000 of them over time.

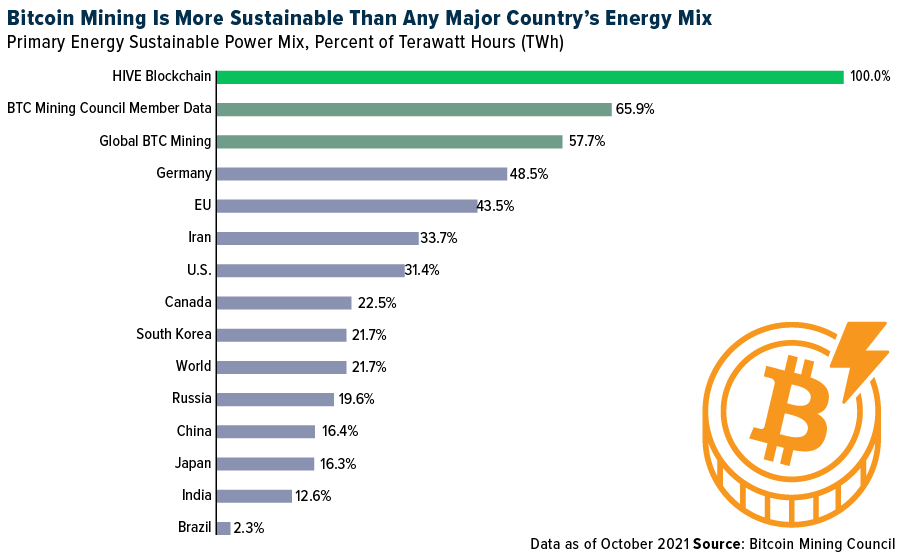

5. The global bitcoin network uses less energy than holiday lights

On a final note, the Bitcoin Mining Council (BMC) released its quarterly report this week, and it contained much to celebrate about Bitcoin. If you recall, this group came together during the summer in response to Elon Musk’s claims that Bitcoin mining consumed too much energy, and too much dirty energy. The Council’s findings, on the other hand, tell a very different story.

According to the group, which is headed by MicroStrategy CEO Michael Saylor, and of which HIVE is a member, Bitcoin mining uses a negligible amount of energy globally when stacked against any major country and even any major industry, gold mining included.

In fact, you may be surprised to learn that Bitcoin mining uses even less energy than holiday lights do every year.

And contrary to Elon Musk’s claims, the network uses a more sustainable energy mix than any major country on earth. Germany leads this list at nearly half renewable, whereas the global Bitcoin mining network is estimated to be 57.7%. The figure rises to almost 66% for the members of the BMC. And then there’s HIVE, which uses 100% green renewable energy to mine Bitcoin and Ether.

U.S. Global Honors Health Care Heroes

U.S. Global Investors is very proud to have been a sponsor of the 2021 Health Care Heroes, the annual event that celebrates the doctors, nurses, researchers and other health care professionals who serve our hometown of San Antonio. On behalf of everyone at the company, I tip my hat off to all of you! Thank you for keeping our community safe and healthy, particularly over this past year.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.08%. The S&P 500 Stock Index rose 1.67%, while the Nasdaq Composite climbed 1.29%. The Russell 2000 small capitalization index gained 1.08% this week.

- The Hang Seng Composite gained 3.07% this week; while Taiwan was up 0.64% and the KOSPI fell 0.30%.

- The 10-year Treasury bond yield rose 6 basis points to 1.64%.

Airline Sector

Strengths

- The best performing airline stock for the week was Bombardier, up 4.6%. Alaska Air’s third quarter update, posted this morning, provides $50 million USD higher revenue coupled with $20 million USD lower expenses, leading to $70 million USD total earnings and $0.50 better earnings per share (EPS) than consensus. The company highlighted improving corporate demand, noting that it recently had its best performing week for corporate volumes since the previous high just before the summer of this year. The company also observed an encouraging early response from corporate clients related to its codeshare with American Airlines and its Oneworld airline alliance partners.

- European airline bookings stepped up in the week, with international and intra-Europe both up by 14% on a week-on-week basis. The continued strong bookings momentum resulted in total net sales exceeding 50% of 2019 levels for the first time. Intra-Europe net sales were up by 10 points to -27% versus 2019 (versus -37% in the prior week) and grew by 14% this week. International net sales increased by 6 points to -55% (versus -61% in prior week), with a similar 14% growth this week. This led to a 7-point increase in system-wide net sales for flights booked in Europe to -47% (versus -54% in the prior week).

- System net sales stepped up this week to down 50.9% versus 2019 for the week versus last week's level of -56.4%. Demand is building back the past two weeks after the threat from the Delta variant begins to pass as leisure bookings are once again back above 2019 levels for the first time in six weeks and corporate/international bookings are nearing summer levels. While domestic leisure (bookings through over-the-air (OTA) channels) showed stronger improvement sequentially than corporate for the second week in a row, corporate is nearing its highest levels on the year. Leisure tickets stepped up to 4.4% versus 2019 (versus -5.2% last week), though leisure continues to trail its peak summer bookings that averaged 13% versus 2019 in June through July. Tickets booked through small and large corporate channels improved to -23.5% (versus -30.5% last week) and -50.6% (versus -54.6% last week), respectively.

Weaknesses

- The worst performing airline stock for the week was GOL, down 17.2%. Following EasyJet’s update, which suggested revenue per seat was down 24% on pre-pandemic levels in its fourth quarter with seats down 42%, analysts cut their Ryanair 2022 net income from €308 million to €186 million, (to reflect revenue per seat down 28% with Ryanair seats down only 16%).

- European airline shares are down 8% on average year-to-date, underperforming the 7% rebound for U.S. peers. This largely reflects a slower recovery and greater uncertainty over travel restrictions as well as concerns over balance sheet restructuring and capital raises.

- For United Airlines, December quarter revenue guidance of down 25% to 30% versus 2019 is in line with investor expectations, but the cost outlook is worse-than-expected with cost per available seat mile (CASM) ex-fuel guided to be up 12% to 14%. Fuel costs are increasing as well. American Air and Southwest also reduced fourth quarter guidance for the same reasons.

Opportunities

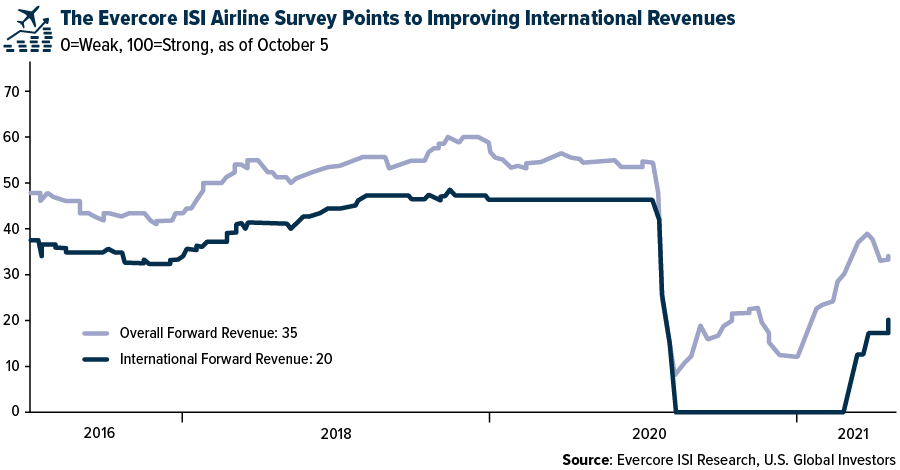

- The Evercore ISI Airline Survey of Overall Forward Revenue started to see signs of rising concerns over the COVID Delta variant in late July. Both leisure and business demand have been affected. While near-term travel plans have cooled, leisure demand for upcoming holidays remains strong. International demand has been slower to recover but has been improving as restrictions on foreign travel have eased. However, it should be noted that short-haul destinations remain solid, and long-haul demand has improved more gradually.

- The U.S. announced it will lift travel restrictions to fully vaccinated international travelers on November 8. The U.K. government will allow fully vaccinated travelers to take cheaper lateral flow tests from October 24, having previously required expensive PCR tests.

- According to Bank of America’s latest forward indicator, an improvement was seen from -19.8 to -16.9 last quarter, showing a continued rebound in industry domestic unit revenues into the new year. The uptick this quarter is much lower than last quarter as domestic revenues are likely beginning to flatten out after pent up leisure demand powered a strong summer.

Threats

- Bank of America surveyed 71 companies across their coverage in Latin America, with a particular focus on air travel. Data indicates that 82% of companies plan to reduce 2022-23 corporate air travel versus 2019 levels. For 75% of the respondents the latest technologies have been an effective replacement for business-to-business meetings, mitigating the travel restrictions problems.

- The U.K. CAA is set to allow 50% increase in Heathrow charges price cap. The final decision will be taken in early 2022. The theme of infrastructure cost inflation continues to build across the sector.

- European airlines are far more exposed to the higher fuel prices than pre-pandemic as they have reduced hedging during the crisis. Historically, airlines have passed on fuel prices through ticket fares over time, but it may be more difficult for them to pass on higher costs this year given demand is still recovering. Prior to the pandemic, European airlines hedged 50-90% of their 12-month jet-fuel consumption. However, the grounding of fleets during the crisis has resulted in large hedging cash losses and most companies have reduced hedging levels as a result, meaning they are far more exposed than before to fluctuations in fuel prices.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 5%. The best performing country in Asia this week was Hong Kong, gaining 3%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 1%. The Chinese yuan was the best performing currency in Asia this week, gaining 0.83%.

- October preliminary Manufacturing PMI for the Eurozone was released at 58.5, above the expected reading of 57.1. However, Service PMI data declined to 54.7 versus the expected 55.4. Composite PMI corrected, primarily due to the weaker service sector, but remains well above the 50 level that separates expansion from contraction.

Weaknesses

- The worst performing country in emerging Europe for the week was the Czech Republic, losing 2.3%. The worst performing country in Asia this week was Indonesia, losing 0.75%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 3.72%. The Pakistani rupee was the worst performing currency in Asia this week, losing 1.64%.

- China reported slower economic growth in the third quarter. GDP was reported at 4.9% versus expected 5% and the 7.9% growth recorded in the second quarter. On a year-over-year basis, Chinese economic growth slowed to 9.8% versus the expected 10.1% and prior reading of 12.7%.

Opportunities

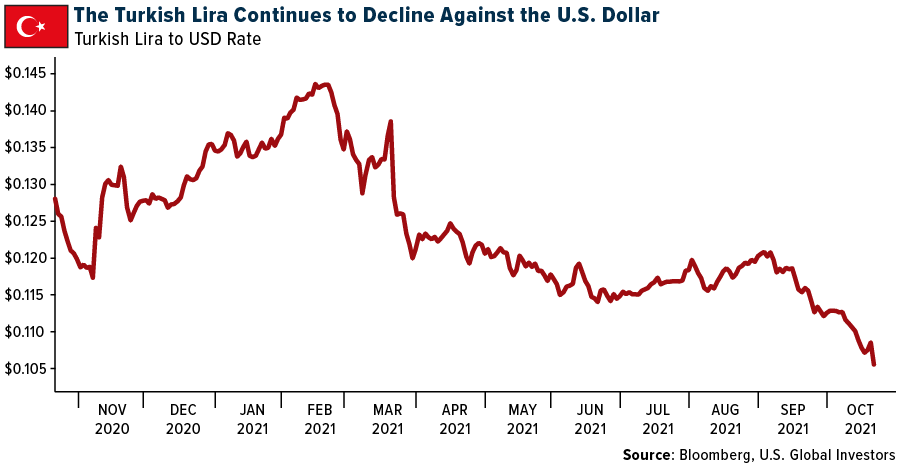

- As expected, the Turkish lira continues to slide against the U.S. dollar after the central bank unexpectedly cut its one-week repo rate from 18% to 16%. Last week, the president of Turkey fired three central bank members who opposed his idea of cutting rates. Bloomberg economists were only expecting a cut of 50 basis points. The lira may depreciate further on the news.

- Eastern emerging Europe is reporting a spike in COVID-19 cases. Some countries are experiencing the “fourth wave” of the pandemic. Latvia imposed a four-week lockdown while Russia is preparing for nationwide non-working day implementation from October 30 to November 7. Regions with serious levels of cases may introduce the stay-at-home measure starting this Sunday. Moscow’s mayor has asked unvaccinated people over 60 years old to stay home for next four months.

- UBS double upgraded China to overweight status. The UBS research team has been recommending underweighting Chinese equites since the summer of 2020 and now sees the recent sell-off as an opportunity to pick up more exposure to the Asian nation. UBS believes the tighter policy and regulatory concerns are now priced in and relative earnings, which have been very poor this year, should bounce in 2022.

Threats

- This week TS Lombard published a report titled “Slowing China, Slowing Europe,” saying that Europe is likely be significantly impacted by a slowdown in China in 2022. The report included a revised gross domestic product outlook for China of 4.7% year-over-year from 5.7%, saying the growth slowdown remains a major headwind for the euro currency.

- The president of China called for an increase in the property tax. China launched a pilot property tax program in Shanghai and Chongqing in 2011 and is now looking to introduce the pilot testing in the wealthy eastern province of Zhejiang. President Xi Jinping on Friday called for progress on a property tax that could help reduce the wealth inequality in order to achieve his goal of common prosperity by mid-century. Reuters commented that China has mulled introducing a property tax for over a decade. The Asian nation has faced resistance from stakeholders, including local governments, which rely on revenue from land sales and worry it would erode property values or trigger a market sell-off.

- Chinese Evergrande, the world’s most indebted property developer, made a missed coupon payment on its offshore bond on Thursday, avoiding the formal default that some were expecting on October 23. Evergrande missed its first coupon payment on September 23, and the 30-day grace period would put the formal default on October 23. This weekend’s default has been avoided, but there are additional missing payments that the company will need to make.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was wheat futures, up 3.30% on tight supplies. This high protein grain is the latest food product price to be impacted as drought scorched North American production, cutting Canada’s production by nearly half while the U.S. harvest was the lowest in 50 years.

- Nickel has done well this year, rallying above $20,000 per ton to the highest intraday level since 2014. At this juncture, the critical cash-three-month gap is backward and has the scope to widen further. It was last at $83 per ton, the biggest in two years.

- The London copper market remains in a historic squeeze, as a critical shortfall in available inventories drives prices to near-record levels and leaves buyers paying huge premiums for spot metal. The 88% drop in available stockpiles this month has been driven by a steady flow of orders to take metal out of European depots. The squeeze has helped underpin a surge in prices – benchmark futures have jumped 10% in the past week

Weaknesses

- The worst performing commodity was lumber futures, down 12.15% for the week as the housing backdrop becomes cloudier with rising mortgage rates and affordability wanes. The rapid growth of the U.S. solar industry risks being knocked off course as a “perfect storm” of events causes project costs to rise for the first time in 14 years. This year marks the first time solar costs have increased since 2007. “This year is a perfect storm,” said Xiaojing Sun, head of solar research at Wood Mackenzie, pointing to a triple whammy of contributing factors: a sharp rise in component prices, tariffs and sanctions, and soaring shipping costs. Polysilicon, an essential component for solar panels, has tripled in price since January, with increased demand and power shortages in China largely responsible for the rise.

- Preferential electricity prices for primary aluminum smelters will end by January 1, 2022, in several provinces and regions in China, increasing production costs and adding further upward pressure to domestic aluminum prices. The move comes as many Chinese smelters are already grappling with rising electricity prices due to a power shortage. The cost of electricity comprised 35.1% of the cost of primary aluminum production in September.

- Union members at Exxon Mobil’s Beaumont refinery on the Texas Gulf Coast voted down the company’s contract offer Tuesday, which means a nearly six-month lockout will continue, according to two people familiar with the vote outcome. United Steelworkers Local 13-243, which represents about 650 Exxon workers, voted against a new labor agreement that the union had urged members to reject. The union contends that the contract offered by Exxon would eliminate some jobs in the next three years.

Opportunities

- Leading indicators continue to signal year-to-year improvements in U.S. long steel demand. Non-residential construction represents the largest consumer of steel, where project starts lead steel demand by 6 to 12 months. On a national basis, U.S. non-residential building construction starts were up 9% year-to-year, although U.S. infrastructure construction starts were down 17% year-to-year. Construction represents roughly 40% of U.S. steel demand.

- According to Bank of America, the 12-month moving average of their proprietary Petrochemical Sentiment Indicator just hit a high of 67%. This marks the 12th month since the indicator flashed a bullish signal back in late September 2020. However, they suspect much of the bullishness is being driven by weather-related outages, high turnaround activity, and rising energy/electricity prices, the aggregation of which is quite unique and likely to moderate in coming months/quarters.

- NanoXplore recently updated investors on their growing confidence in the graphene market. Graphen has properties that can help recycle plastics, reduce the weight of vehicles, and strengthen concrete thus lowering the amount required. Producing a tonne of graphene also yields less carbon dioxide (CO2); 0.4 tonnes versus 3 tonnes for producing carbon black. NanoXplore recently received U.S. Environmental Protection Agency approval for their GraphenBlackTM to be used as an additive without limitation on volumes in the U.S. and they are the only company that has such approval to sell graphene in the U.S. Perhaps the biggest use of graphene could be its use as a concrete additive where it can increase the strength of material which allows the weight to be reduced. Gerdau Grafeno LTDA has entered into a multi-year supply and distribution agreement with NanoXplore for their graphene supply. NanoXplore is the global leader in in graphene production with about 40% of the market.

Threats

- Europe is facing a magnesium shortage that could shut down industrial operations where the metal is a critical for hardening aluminum alloys to a wide range of products from power tools and laptops. China supplies Europe with 95% of their magnesium but exports have been halted or curtailed drastically. European manufactures may only have enough metal to carry them through November, according to Bloomberg.

- Iron ore has been demonstrating unexpected resilience so far this week. Still, a retracement in prices has likely been postponed, not avoided. China’s steel industry – the top buyer of seaborne ore supplies – saw a record drop in output in September as authorities sought to cut emissions and save power. During the third quarter this year, its mills produced 37 million tons less steel than in the same period of 2020. For iron ore, that’s a major demand shock.

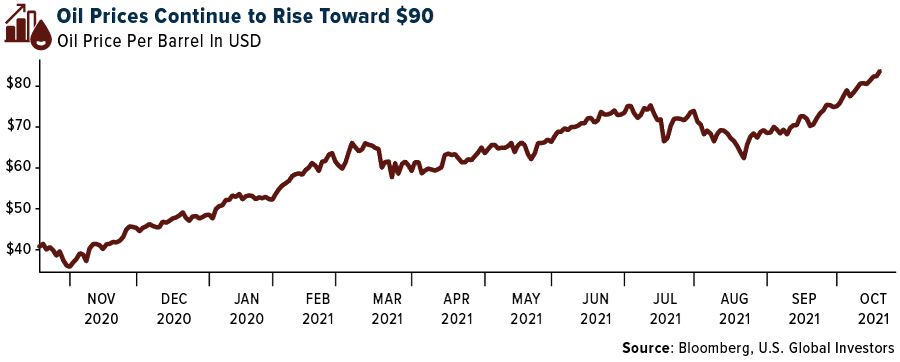

- President Joe Biden said Thursday night that Americans should expect high gasoline prices to continue into next year because of policies by OPEC and other foreign oil producers. “My guess is you’ll start to see gas prices come down as we get by, and going into the winter…into next year, in 2022,” the President said. “I don’t see anything that’s going to happen in the meantime that’s going to significantly reduce gas prices.” The president added that prices will “ultimately” decline as the country shifts to renewable energy over the next few years.

Domestic Economy and Equities

Strengths

- Initial jobless claims dropped to 290,000, a fresh pandemic low and the second week below 300,000. This week’s reading is also down from the prior week's upwardly revised 296,000 and below the consensus of 299,000. Continuing claims came in at 2,481,000 which is a new low since March 20, and below last week's upwardly revised 2,603,000.

- October preliminary Manufacturing PMI was released at 59.2, which is slightly lower than the prior month’s 60.7. Service PMI jumped to 58.2 from 54.9, bringing the Composite PMI to 57.3 from 55.0.

- Pool Corporation was the best performing S&P 500 stock for the week, increasing 11.28%. Shares gained after the company announced a revenue beat. Strong consumer spending is lifting the swimming pool industry.

Weaknesses

- Industrial production declined in September by 1.3% month-over-month while Bloomberg economists were predicting an increase of 0.1%. Housing starts and building permits also weakened in the month of September.

- The Consumer Confidence Index, which measures Americans' perceptions on three important variables: the state of the economy, personal finances and whether it's a good time to buy needed goods or services, decreased by 0.2% from 0.9%. Bloomberg economists were expecting the index to decline, but only by 0.4%.

- International Business Machines Corporation (IBM) was the worst performing S&P 500 stock for the week, losing 11.57%. Shares dropped as the company reported weaker revenue. Analysts are predicting that IBM may struggle to show significant sales gains until the spinoff of its lower-growth infrastructure outsourcing unit, Kyndryl, is complete.

Opportunities

- Federal Reserve officials have seemingly made a heightened effort to distinguish between tapering and tightening. Monetary policy can remain a tailwind for risk assets but even with the Fed reducing asset purchases by $15 billion a month, it will end up adding about $400 billion in liquid assets to the financial system through mid-2022, FactSet reported.

- Stocks are at record high as Democrats try to move closer to a deal on infrastructure stimulus, now expected in the $1.7 - $1.9 trillion range. The White House may be pushing for votes on both the stimulus package and the $1 trillion bipartisan infrastructure bill next week.

- China Evergrande Group made an overdue interest payment on dollar denominated bonds just a few days before October 23 when it would formally enter a default if the payment was not made. The coupon payment this week from Evergrande was a positive surprise suggesting that Evergrande is treating the onshore and offshore bond creditors the same for the time being.

Threats

- As of Thursday, five-year yields climbed above 1.2%, the highest since February 2020. The 10-year yields rose to around 1.68%.

- Bloomberg reported that record imports and labor shortages are creating problems for supply-chain companies. There are long lines of cargo ships waiting to be unloaded in the United States as Americans continue making purchases from abroad. It now costs as much as $25,000 to import a 40-foot container from Asia, up from less than $2,000 two years ago. This supply crunch will lead to higher and prolonged inflation.

- Investors are stepping up bets that the world’s key central banks will raise interest rates sooner than they had planned, and faster than they would like. Policymakers now sound more worried that pandemic inflation will stick around -- and more willing to boost borrowing costs in order to bring it down.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was BlowUP (BLOW), rising 88,848,931%.

- Tom Lee from Fundstrat says he could see the newly launched Bitcoin Futures ETF attract $50 billion. As reported by Bloomberg, Lee added that demand could even exceed inflows for QQQ. Lee’s team has a year-end $100,000 price target on Bitcoin, though he says the coin’s price could rise even higher to $168,000.

- Bitcoin climbed to record highs this week after the debut of the futures-based ETF. According to data compiled by Bloomberg, the ProShares ETF traded more than 24 million shares on Tuesday, which is the second-most traded shares at a launch.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Spain National Fan (SNFT), down 98.17%.

- In an interview with CNBC, Larry Fink, Chairman and CEO of Blackrock, agreed with JPMorgan CEO Jamie Dimon on Bitcoin’s true worth. Fink said, “I can’t tell if Bitcoin is going to $80,000 or zero,” wrote CoinTelegraph. He did add that he sees a huge role for digitized currency and its potential to help people and the economy.

- Crypto bull Cathie Wood did not buy the new Bitcoin ETF (BITO). In an interview at the Milken Institute Global Conference this week, Wood stated that her team is looking at this very carefully before making any decisions to invest. She stated that there are tax ramifications the ARK Invest team would like to understand first, specifically having to do with contango.

Opportunities

- ProShares Bitcoin Strategy ETF (BITO) launched this week after getting its blessing from the U.S. Securities and Exchange Commission (SEC). It’s the first U.S Bitcoin-linked ETF that offers investors an opportunity to gain exposure to Bitcoin returns. The funds seeks capital appreciation through managing exposure to Bitcoin futures contracts.

- Grayscale Investment and the NYSE filed to turn the biggest Bitcoin fund into an ETF, reports Bloomberg. The application to flip the $40 billion Grayscale Bitcoin Trust (GBTC) landed on the same day the ProShares Bitcoin Strategy ETF debuted. The SEC has allowed the derivatives-based product to launch but has yet to permit the kind of structure used by Grayscale, which holds the actual cryptocurrency.

- The pension fund for Texas firefighters has allocated part of its $4 billion portfolio towards cryptocurrency, reports CoinTelegraph. The Houston Firefighters’ Relief and Retirement Fund used the New York Digital Investment Group to execute the purchase of $25 million in both Bitcoin and Ether.

Threats

- Hackers have exploited a simple computer tool to steal 17.5 million euros, reports Science Techniz. The botnet, called MyKings, apparently hijacks the function on infected machines and redirects the payments to the attackers’ wallets, the article continues.

- JPMorgan is warning that a boom for Bitcoin futures ETFs may come at a cost, reports Bloomberg. The problem here is the cost of continually rolling over contracts held by the fund, known as a “carry.” JPMorgan strategists Bram Kaplan and Marko Kolanovic note that the new BITO ETF accounts for a quarter of open interest in October and November. This means that the carry cost could be several times larger than the management fees, the article continues.

- The Bitcoin price flash crashed by 87% to $8,000 on Binance.US, reports CoinTelegraph. On October 21, BTC crashed to just $8,100 only on Binance’s U.S. platform. Traders are calling this a “scam wick” and have vocally criticized the terrible exchange protocols that Binance.US has to offer, CoinTelegraph explains.

Gold Market

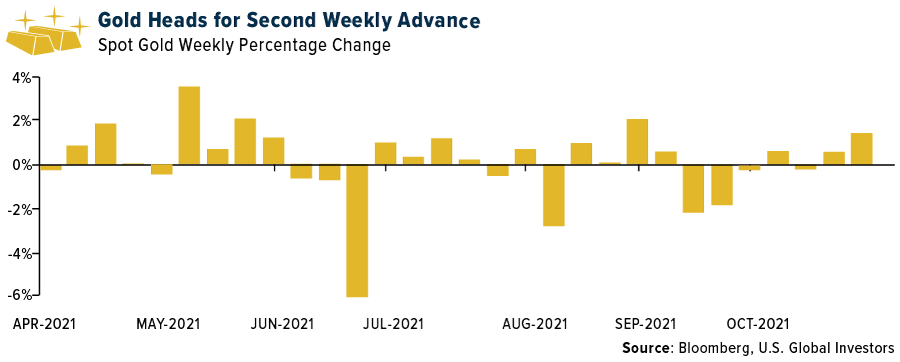

This week spot gold closed at $1,792.65, up $25.03 per ounce, or 1.42%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.31%. The S&P/TSX Venture Index came in up 1.19%. The U.S. Trade-Weighted Dollar fell 0.33%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-17 | China Retail Sales YoY | 3.5% | 4.4% | 2.5% |

| Oct-19 | Housing Starts | 1,615k | 1,555k | 1,580k |

| Oct-20 | Eurozone CPI Core YoY | 1.9% | 1.9% | 1.9% |

| Oct-21 | Initial Jobless Claims | 297k | 290k | 296k |

| Oct-26 | Hong Kong Exports | -- | -- | 25.9% |

| Oct-26 | New Home Sales | 756k | -- | 740k |

| Oct-26 | Conf. Board Consumer Confidence | 108.5 | -- | 109.3 |

| Oct-27 | Durable Goods Orders | -10.0% | -- | 1.8% |

| Oct-28 | ECB Main Refinancing Rate | 0.000% | -- | 0.000% |

| Oct-28 | Germany CPI YoY | 4.4% | -- | 4.1% |

| Oct-28 | Initial Jobless Claims | 292k | -- | 290k |

| Oct-28 | GDP Annualized QoQ | 2.7% | -- | 6.7% |

| Oct-29 | CPI Core YoY | 1.9% | -- | 1.9% |

Strengths

- The best performing precious metal for the week was silver, up 4.35%. Gold steadied after a two-day advance as investors weighed comments from Federal Reserve officials indicating that interest-rate hikes aren’t imminent. Increases to U.S. interest rates aren’t coming “anytime soon,” Cleveland Fed President Loretta Mester said Wednesday – though the central bank will act if warranted by inflation expectations. Bullion has fluctuated recently as traders attempt to gauge the pace at which pandemic-era stimulus will be reined in by central banks. Rising energy and commodities costs and disrupted supply chains are creating inflation headaches for the global economy, boosting expectations for earlier rate hikes that can curb the allure of non-interest-bearing gold.

- Russia's gold reserves have been increasing in the last few years, but it seems that inflationary woes in particular have the nation stocking up on the yellow metal again. The Russian central bank has been raising interest rates to try and combat the issue. This now means that the Russians are hedging against this problem by increasing the amount of gold it holds. Serbia plans to boost its gold reserves from an already record-high 37 tons to prepare for challenges such as the energy crisis rattling Europe, President Aleksandar Vucic said.

- Maverix Metals is increasing and expanding its royalty interest in the Omolon hub. The increased royalty is expected to more than double current gold equivalent ounces received from Polymetal's Omolon operation to 5,000 ounces per year (an incremental 3,000 ounces). The new 2.5% royalty will now cover 13 of Omolon's licenses, up from the previous 2% on 2 licenses (in essence, the royalty now covers all production from Omolon versus previous royalty interest on a portion of production covering certain deposits). Total cash consideration for the increased and expanded royalty is $23.5 million.

Weaknesses

- The worst performing precious metal for the week was palladium, down 2.73%. K92 Mining reported third quarter production of 24.1 gold ounces from its Kainantu Mine in Papua New Guinea. This was 4% below consensus. COVID-19 travel restrictions are still impacting the operations. Current guidance is 115,000-135,000 ounces. To hit the low end of guidance will require production of a record 47,000 ounces (the current record is 29,800 ounces in the last quarter of 2020).

- More than $10 billion USD has been pulled from the biggest gold exchange traded fund (ETF) this year and pension funds physical gold hoards have also been selling down, according to Bloomberg data. The price of gold has declined 6.1% this year to $1,782 a troy ounce on Wednesday. Bitcoin has meanwhile doubled in price to a record high of more than $67,000 this week. Some investors have begun to view it and other cryptocurrencies as an inflation hedge, even if none existed during the world’s last serious bout of inflation. Veteran gold traders acknowledged times are changing. “There is zero interest in our strategy right now,” said John Hathaway, senior portfolio manager at Sprott Asset Management, a precious metals investment group. More than half the hedge funds surveyed in Europe and the U.S. said that rising inflation was a main driver of their attraction to digital assets, with nearly eight in 10 of the surveyed investors stating that cryptocurrencies have a place in a portfolio.

- Metals and mining fundraising increased 31% month-over-month in September to $1.77 billion in 160 financings. The number of financings completed fell for the third consecutive month, however, and is at its lowest since April 2020 when 136 financings were recorded during the peak of lockdowns due to the COVID-19 pandemic. The number of financings declined, however, with 1,843 financings completed compared with 2,106 in the same period of 2020.

Opportunities

- Silvercorp Metals reported operating results for its fiscal second quarter. Second quarter production results were modestly weaker than consensus due to lower grades at both mines. Silver grades at the Ying Mining District were 283 grams per tonne, compared to consensus of 303 grams per tonne. However, Silvercorp also mentioned it won an auction to acquire the Kuanping Project with is 33km from their Ying Mine. What is interesting is Silvercorp has rarely been able to secure new opportunities in China.

- Current financial metrics being demonstrated by gold mining companies present a great opportunity for generalist investors to take notice. Dividend yields for Newmont Mining and Barrick Gold are north of 3% while the indicated yield on the S&P 500 Index is just 1.3%. With inflation becoming more mainstream generalist investors will be looking to protect their wealth and gold miners need to take this opportunity of scarcity to raise investor awareness. Perhaps some gold miners should withhold a portion of their production; HODLing the supply chain as gold is too cheap to sell at these prices.

- Silver miner Hochschild PLC plans to spin off the rare earths project it bought two years ago and list the new company in Canada. Hochschild, which mines silver and gold in Peru and Argentina, bought the Chilean project in 2019 for about $56 million. Hochschild will keep a 20% stake in the business. Rare earths companies have come into play with China being the world’s largest producer of rare earth metals with other countries trying to secure stable supply chains.

Threats

- The U.S. Forest Service is being sued by an environmental group that asserts it unlawfully fast-traced approval for a land exploration drilling project on public lands. In September, the government agency had given approval of the permit to KORE Mining.

- Gold demand in India is likely to face challenges from a declining household savings rate and lower agricultural wages, according to the World Gold Council. Rising income is one of the biggest drivers of gold demand, suggesting that as India’s economy grows, sales of the precious metal should increase. However, “households are saving proportionately less than they used to, which may reduce the amount of capital they allocate to gold,” it said.

- Vale announced that copper concentrate production has been suspended at its Salobo operation as a fire has partially affected a conveyor belt at the mill. Due to the timing of concentrate shipments/refining, the shutdown is largely expected to impact first quarter 2022 gold deliveries to Wheaton's 75% gold stream on the operation.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All