Matters of money can pull at both our intellect and our emotions. And when markets get shaky, that’s when the internal tug-of-war kicks into high gear. Two investment pros share strategies for keeping calm and investing on.

It’s easy to focus on the negative. In fact, it’s the human tendency. We see some of this manifesting in markets today. After a swift and strong run for equities since the COVID-crisis lows, some investors are turning their attention to what can go wrong.

Yet there’s still plenty to go right. That’s according to international equity investor James Bristow and Morgan Housel, author of The Psychology of Money. The two recently got together for a robust conversation that not only considered the potential bright spots in the outlook, but also the lessons to be gleaned from the pandemic and how to balance the emotion and science of investing.

When it comes to maintaining perspective and ensuring your emotions don’t lead you astray when markets get choppy, they offer this advice:

Have a plan

All of us, whether individual or professional investors, should have a forward-looking plan, says Mr. Bristow. It should consider “here's what I'm trying to achieve, and here's what I would do in certain circumstances.” Having a well-thought-out plan should provide guardrails and offer some measure of solace, forestalling emotional reactions when markets get dicey.

Yet it’s also important to get comfortable with the idea that not every scenario can be foreseen or planned for. A once-in-a-century global pandemic is a prime example.

“Having plans is absolutely essential,” says Mr. Housel, “but the biggest news stories of the next year, of the next 10 years, over the course of the rest of our investing lives, are going to be things that you and I, and anyone else, cannot be discussing right now, because they're going to be surprises.”

How can investors manage around this grim reality? Incorporate a margin of error into your plan.

“If you have room for error in your analysis, in your allocations, in your budgets, you don't necessarily need to know exactly what's going to happen next,” Mr. Housel explains. “That to me is just a more realistic way to manage risk than assuming that we know exactly what's going to happen next.”

In the end, no one saw the COVID crisis coming, but neither could we have predicted the magnitude of the recovery. A margin of error leaves room to ride the waves, even the entirely unexpected ones.

Follow your playbook, not the crowd

As a participant in BlackRock’s behavioral finance project, Mr. Bristow has grown increasingly attuned to how individual psychology can affect investment decision-making.

“One of the things I and my team have done for many years is just to try to understand ourselves better. And it requires a willingness to be a little bit self-critical … to look back on your actions and find room for improvement.”

To “know thyself” is critical, yet there are popular undercurrents in markets that can lead to crowd mentality, causing some investors to set aside self-awareness and stray from their plan.

Mr. Housel’s advice: Realize that everyone is playing a different game. “If you assume that investing is one game, that everyone has the same time horizon, the same goals, [that] they want the same outcomes, then there should be one set of rules, and one strategy that's likely to work,” he says. “But people play completely different games.

“Does it make sense to dump your stocks if inflation rises by 10 basis points? If you're a long-term investor, no. If you're a day trader, maybe.”

Ultimately, what is “rational” depends on the game you’re in. Don’t assume you should be playing by others’ rules.

Be patient, but not stubborn

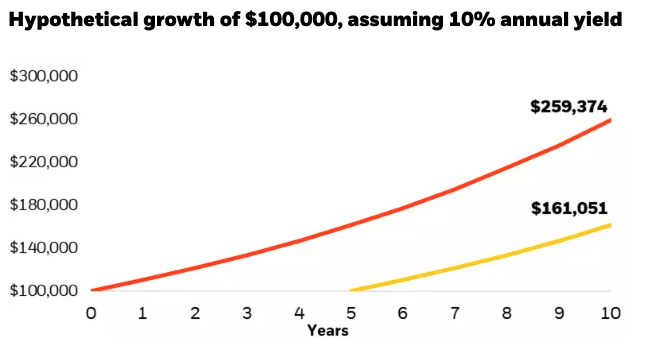

“The power of compounding,” Mr. Bristow asserts, is “clear, obvious and necessary for all of us.” And achieving greatest benefit from compound interest requires one critical element: time.

The hypothetical illustration below shows the profound impact of staying invested over 10 years versus five.

Hypothetical growth of $100,000, assuming 10% annual yield

Yet there can be a tension between having a long-term mindset and getting entrenched in a view that is fated for failure ― aka stubbornness.

The key to walking this fine line: Know that patience and compounding are the fundamental cornerstones of investing. But also know that the world is constantly changing ― and be willing to question your view.

Our two experts agree that it’s important to study the short term to understand if it may be important in the long run.

Mr. Bristow credits BlackRock for helping him to maintain this balance: a mentality and culture for long-term investing alongside the mechanisms needed to assess the short term and identify any threats to your long-term central thesis.

“It's not enough to just set the view, and then go away and hide in your bunker for 20 years and come out the other side,” he says. “You've always got to be reassessing it.”

This is a key virtue of active management― taking active, short-term steps in pursuit of long-term goals.

Mr. Housel sums it up well: Following and understanding what's going on in the short run is not counterproductive to long-term thinking. It's essential to long-term thinking and, ultimately, to enduring emotionally and financially across time.

© BlackRock

Read more commentaries by BlackRock