Jim Cielinski, Global Head of Fixed Income at Janus Henderson, considers the impact of nuance on bond markets.

Investing in bonds these days sometimes feels like being a lawyer – language seems to take on ever more importance. This is most evident with the way the market pores over every change in adjective or turn of phrase spoken by central bankers.

It is at its most acute when deciphering the statements and speeches of officials of the US Federal Reserve (Fed), where the responsibilities are all the greater given the influence of US monetary policy and US government bond yields as a marker for rates more globally.

Troubling bond markets in recent months has been the shift in language from the Fed towards tapering, ie, reducing the pace of purchases of securities it undertakes through its quantitative easing (QE) programme. The current round of QE was always billed as a policy tool to deal with the disruption caused by COVID-19. Successful vaccination programmes mean that the emergency has abated and economies have reopened. As such, markets have been trying to second guess when QE will end.

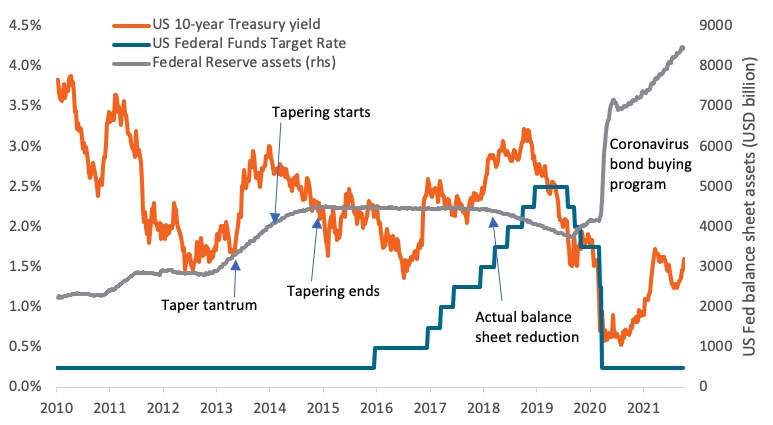

There are two things worth drawing attention to here. First, the Fed has learnt from the “taper tantrum” of 2013 that it needs to communicate clearly its intentions after the market (back then) misinterpreted tapering as immediately presaging a rise in interest rates. Jerome Powell, the current Fed Chairman, has been consistent in saying there will be a lag between the end of tapering and any rise in interest rates. In mid-October 2021, futures markets implied that rates would rise in December 20221, suggesting a six-month lag from the end of tapering (assuming it commences late 2021 and ends mid-20222). This compares with a lag of 14 months in 2014-15. The truncation can be explained by the relatively high inflation levels currently.

US monetary policy history

Source: Refinitiv Datastream, US Federal Funds Target Rate (current range 0.00-0.25%), US Benchmark 10-year government bond (redemption yield %), Federal Reserve Total Assets on balance sheet (USD billions), 01 January 2010 to 8 October 2021. Past performance is not a guide to future performance.

Second, a distinction should be made between tapering and outright balance sheet reduction. Tapering is still monetary policy accommodation. It is still injecting more money into the system, albeit in smaller doses. So the gradual tapering allows markets to adjust to the Fed not being a regular net purchaser of bonds. If the past is any guide – and it may not be – but we have not heard contrary from the Fed, they are likely to maintain their balance sheet around current levels for some time, as they did between late 2014 and early 2018.

Ultimately, tapering and the prospect of interest rate rises could have a calming effect on bond yields as it stamps down on inflation expectations. Breakeven inflation levels have been remarkably consistent, rangebound around 2.5% for much of 2021 for both 5-year and 10-year breakevens, although there has been some upward pressure recently.1

Back in 2014 the yield on the widely followed US 10-year government bond actually fell as tapering occurred and would carry on falling well beyond the first hike. It may be a stretch to expect the same to occur this time around when bond yields are at a lower starting point and inflation pressures abound. Supply chain disruptions are lasting longer than initially anticipated, with potential cost-push impacts across the economy. High prices may act as a drag on economic growth, essentially acting as a self-correcting force but there is a danger that higher prices begin to dislodge anchored inflation expectations. This could lead to a more persistent inflationary environment and ultimately higher bond yields.

1Source: Bloomberg, 25 October 2021.

2“While no decisions were made, participants generally view a gradual tapering process that concludes around the middle of next year is likely to be appropriate.” Powell, FOMC meeting, 22 September 2021.

The opinions and views expressed are those of the author(s) and are subject to change without notice. They do not necessarily reflect the views of others in Janus Henderson's organization and no forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes and are not an indication of trading intent. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector.

© Janus Henderson Investors

More Global Markets Topics >