Halloween and Christmas for Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSeptember in the U.S. has always marked the beginning of Fall, and for many kids an escalating anticipation of a spooky 6-to-8 weeks ahead, culminating in Halloween on October 31. But sometimes it feels like market participants haven’t grown out of their fears of this frightful time. As a case in point, the September-October window marks the weakest seasonal period for S&P 500 performance, based on returns going back 30 years, according to Bloomberg data as of October 17. And this Fall, the market has had ample reason to fear a “trick” instead of a “treat:” indeed, stagflation, demand destruction, soaring energy prices, the U.S. debt ceiling, a hawkish Federal Reserve, a weak Chinese property sector and elevated corporate profit warnings have taken turns in dominating the headlines. In the current commentary we hope to address this October’s unique market ghouls and further how we think resilient portfolios should be oriented around them.

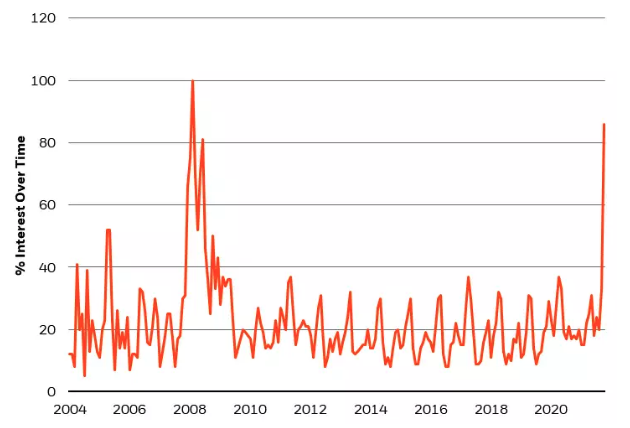

Figure 1: Google Trends: Worldwide Stagflation Queries

Source: Google Trends, data as of October 18, 2021

Ghoul # 1: Could “Stagflation” be Coming to our Doorsteps?

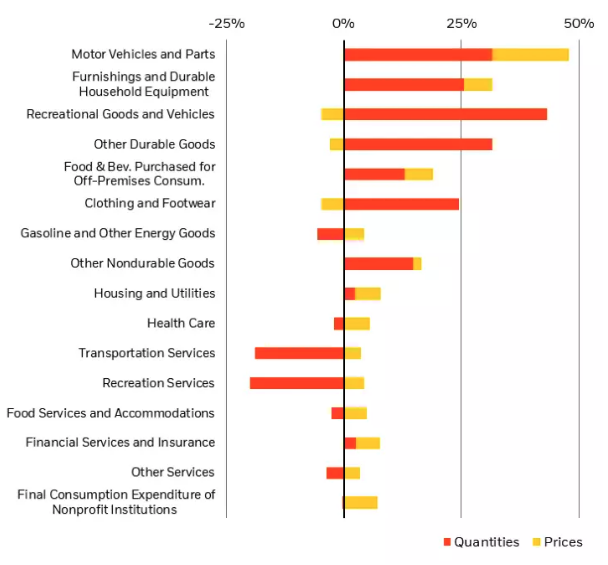

Perhaps there are so many Google queries about stagflation (see Figure 1) because nobody really knows what it means - which is helpful for stagflation prognosticators, since a very wide range of outcomes could then be considered “right.” The fact remains that predicting how the pandemic and policy response would ultimately influence consumption would have been near impossible, evidenced by the wild swings in prices and quantities over the last two years (see Figure 2). Smaller goods segments have been more volatile, while most services consumption trends can be explained by the nature of the pandemic (social distancing, curtailed mobility etc.). So, “stagflation” then becomes a one-word oversimplification of the complexity facing the global economic recovery today.

Figure 2: U.S. Consumption: Q2 2019 – Q2 2021 Change

Source: Bureau of Economic Analysis, data as of June 30, 2021

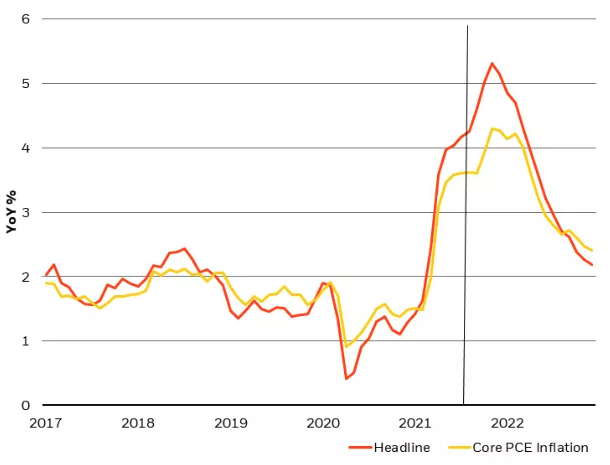

It is likely that in time pandemic distortions and extreme base effects will ease, though not immediately, pulling aggregate prices back toward a 2% rate of growth and allowing quantities to continue expanding once supply pressures alleviate. Nonetheless, this is not a normal set of historical patterns that can be easily modeled – many inflation factors are likely to stay sticky for a while, even as the aggregate PCE inflation metric may normalize in the year ahead (see Figure 3). Thus, in our view, owning inflation breakevens (TIPS) still makes sense, as do inflation sensitive sectors, which could serve as portfolio protection against more persistent inflation.

Figure 3: PCE Inflation Should Normalize in the Year Ahead

Sources: Bureau of Economic Analysis/Haver Analytics; forecast is from BlackRock, data as of October 1, 2021

Ghoul #2: The Terror of Demand Destruction

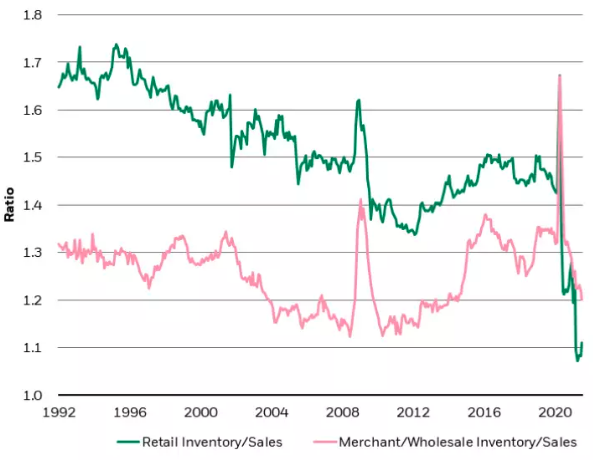

Closely related to the stagflation fear is the fear of demand destruction. How can we tell whether a decline in quantities consumed is due to a buyer’s decision not to make a purchase, or a seller’s inability to meet demand? Observing inventory levels and gauging spending power can tell much of the story. On the corporate side, capital expenditures (capex) have fully recovered and are setting new highs. Capex has recovered 4x faster than it did during the dotcom bust and twice as fast as it did after the Global Financial Crisis. That is itself an important source of current demand for goods and services, while at the same time creating future capacity that will fill future demand. Inventories, on the other hand, have struggled to keep up with sales (see Figure 4), confirming that demand is extremely strong, and that it is suppliers (especially retailers) who are unable to meet that demand.

Figure 4: Inventory/Sales Ratio

Source: U.S. Census Bureau, data as of July 1, 2021

In fact, retail sales, durable goods orders, building permits and home vacancy rates are at their strongest levels in decades (if not all-time). All these metrics suggest that aggregate demand is extremely robust, and that any apparent shortfall in demand has likely been delayed (until such time as inventories are available) rather than destroyed. Additionally, a study of income growth and savings lends further credibility to the theory that future consumption might remain robust even if today’s consumption is being truncated by supply constraints. During the pandemic, U.S. consumers “underspent,” relative to their disposable income, to the tune of about $700 billion. Added to that $2 trillion of Federal stimulus was delivered into the hands of consumers. This $2.7 trillion of dry powder is complemented by wages that are growing at about 5% a year, as well as a potential 4 to 5 million jobs that could be added over the next few years, as the U.S. labor market gravitates toward its pre-pandemic recovered health (data sourced from the Bureau of Economic Analysis, Bureau of Labor Statistics and BlackRock, as of September 30, 2021).

In sum, utilizing a conservative assumption of 3% wage growth (we are running at 5%) and 200k monthly job gains (the 6-month average is 583k), coupled with the aforementioned $2.7 trillion of savings, would allow U.S. consumption to grow at a 6.5% annual rate, through 2025 (the 35-year average for consumption growth is only 5% per year). So, with the demand destruction ghoul dispelled, owning a portfolio of assets in housing, consumer and industrial-oriented sectors shouldn’t be that scary a prospect, even as interest rates move moderately higher in sympathy with economic conditions.

Ghoul #3: Energy Price Frights and Supply-driven Shocks

Fascinatingly, the lack of energy investment in recent years mirrors the over-investment in the sector during the 2012 to 2014 period. Energy sector capex as a share of the S&P 500 has declined from a peak of greater than 30% to recent lows of just 5% (CapitalIQ, data as of June 30, 2021). As such, energy prices around today’s levels may persist, or even get worse during a cold winter, but there isn’t a structural shortage of oil (like suggested by peak oil theory), rather what we’re witnessing is a seasonal, or perhaps a cyclical phenomenon. In other words, we are not in a “classic 1970s” oil shortage in the U.S., neither from the national nor individual perspective.

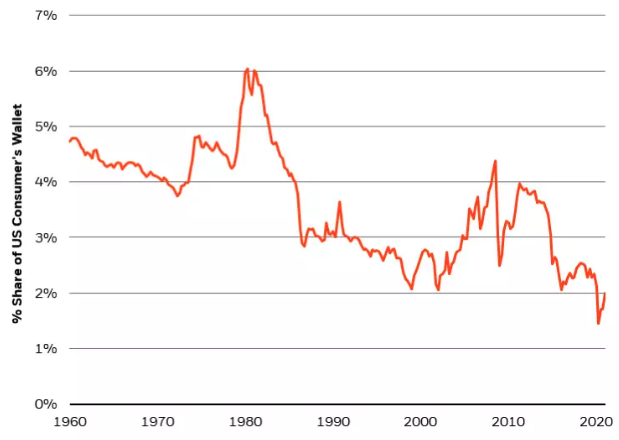

On the national front, domestic oil production has more than doubled in the last 20 years, and as such our reliance on imports has almost halved. Such an insulated domestic industry has a much higher ability to withstand, and dynamically respond to, price shocks than was the case in the 1970s. And from the standpoint of an individual, gasoline has become a very small share of the consumer’s wallet (see Figure 5), having simply returned to the same price as it was in 2014 (while the wallet has expanded since then). At just a 2% share of consumption, oil prices would need to approach $300/barrel in order to grab the same wallet share as was experienced in 1980.

Figure 5: Gasoline Share of U.S. Consumer’s Wallet

Source: Bureau of Economic Analysis, data as of June 30, 2021

Given that the oil rig count has already started ticking up in response to higher prices, and that productivity per rig is 50% higher than before the pandemic (due to cost-cutting innovations), it is unlikely that energy prices are as permanently damaging as they were many decades ago. Still, we think these dynamics make energy a reasonable part of portfolios as we head into the Winter months, since strong demand, enhanced productivity and higher prices should support corporate margins and profits in the sector.

While some will extrapolate the price patterns in commodities and apply them to the entire consumption basket, in truth there are very different pricing dynamics at play in each sector, such that each one needs to be assessed individually (semiconductors and automobiles being some other examples). Like energy, most of them end up looking quite unlike the 1970s, but still have long-tailed demand curves that warrant exposure in portfolios.

Ghoul #4: Earnings Scares (or a wave of Profit Warnings)

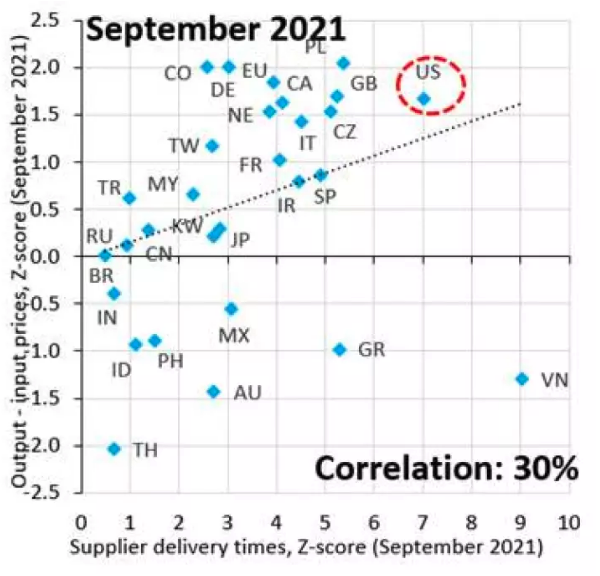

Over the past five quarters (ending Q2-2021), S&P 500 ex-Financials earnings have beaten forecasts by 18%, compared to a 4% average beat over the prior 25 years. That is suggestive of how companies with pricing power and operating leverage can survive, and indeed even thrive, in an inflationary environment. We believe that equities, particularly those with tangible pricing power (such as in the U.S. where pricing power is strong, as displayed in Figure 6), can be part of a diversified mix of real assets that is designed to build portfolio convexity against a longer bout of inflation pressure that today’s nominal assets fail to defend against. There is unquestionably some substantial philosophical evolution from Capital to Labor today, but in the coming years we think capital can still perform quite nicely in a very supportive economic environment.

Figure 6: Longer Delivery Times can Lead to Higher Margins for Those with Pricing Power

Source: IIF, data as of September 2021

Ghoul #5: Frightful Headlines From China

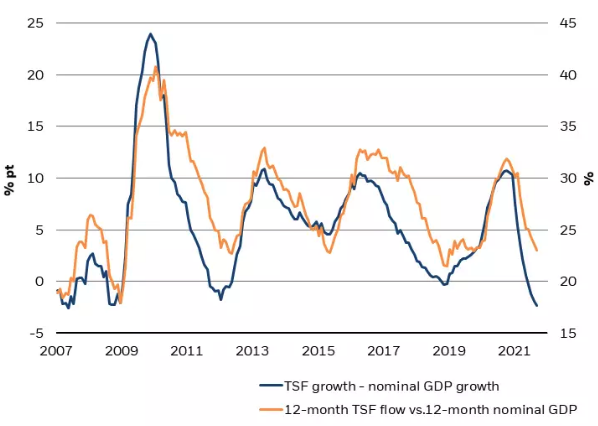

A slew of spooky headlines out of China, ranging from property prices to energy prices to regulatory crackdowns, have created some consternation among investors recently. Yet we would argue that volatile property prices and energy prices, which have led to some demand destruction, are near-term issues. While emissions and antitrust regulation are likely here to stay, largely supported by the Party’s renewed commitment to “Common Prosperity,” while defaults have increased, and credit creation has indeed slowed in response (see Figure 7). This is certainly one of the risks to the global economic and investment system, perhaps even the most profound set of risks. Yet, even so, there will still be investments to make in China, albeit well-scaled ones and in areas that are generally government-aligned and technology-oriented.

Figure 7: China’s credit impulse has slowed

Source: JP Morgan, data as of September 15, 2021

And if all That Wasn’t Spooky Enough, We Still have the Fear of Higher Rates, the Fed Tapering, etc.

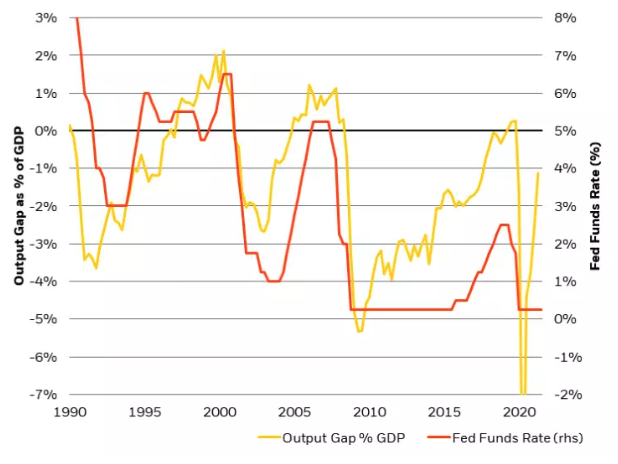

The markets have done a lot of heavy lifting to reprice the yield curve in the last few weeks (and rightly so). Looking at the labor market from a long-term perspective, and through the lens of the monetary policy path, the Fed can continue to evolve to a higher policy rate, and hence the front-end has room to price in a bit more policy normalization, in our view (see Figure 8). After the GFC, it took nearly six years to get back to the pre-GFC employment peak, but post-Covid, it’s taken just 18 months to get back to levels seen as recently as December 2017. Every time we’ve seen this level of employment, relative to the working age population, the Fed was already in the midst of a hiking cycle (at much lower levels of employment, in fact). Hence, the Fed should feel confident in normalizing policy, especially as more labor tailwinds emerge, catalyzed by extended unemployment benefits rolling off and a decline in new Covid cases.

Figure 8: The Front-End has Space to Rise More, in Sympathy with Unemployment and Output

Source: Congressional Budget Office, data as of September 30, 2021

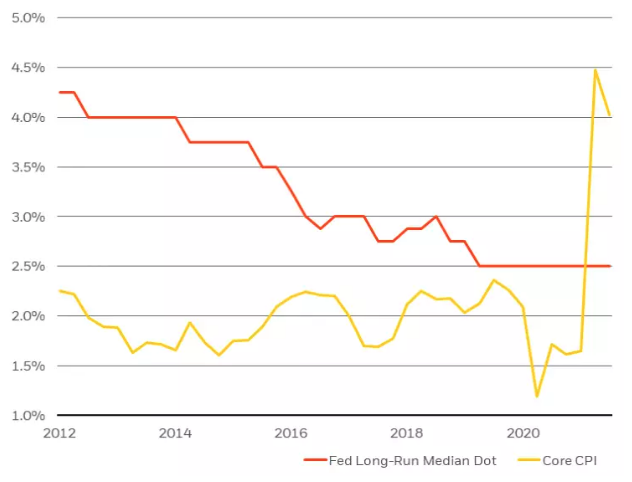

In the context of policy normalization, rising rates should not be too much of a concern for investors because the existing stock of liquidity is still historically high, and likely to keep yields contained (if moderately higher), even as the flow of new liquidity slows in the months ahead. We also suspect higher U.S. yields will strengthen the USD, amplifying any intended policy tightening, and lowering the terminal policy rate indefinitely. The Fed is also likely to be very mindful of not letting the all-in cost of credit exceed the potential growth rate, as evidenced by the Fed’s own long-run median “dot” having declined to 2.5%, the lowest in history (see Figure 9). That also means that negative real rates are likely to be a common feature, if not a possible permanent feature, of financial markets going forward.

Figure 9: Negative Real Front-End Rates are Likely to be a Persistent Phenomenon

Sources: Federal Reserve and Bureau of Labor Statistics, data as of September 30, 2021

Moving away from “emergency policy” means that global policy rates and real rates are likely to diverge. For example, the Bank of England (BOE) is guiding to the potential for earlier rate hikes than expected, while the European Central Bank has pushed back against the market discounting of rate hikes. More than 70 basis points (bps) of additional hikes have been priced one year out for the BOE since the start of September, while only 32 bps of additional hikes have been priced three years out for the ECB (also since Sept. 1). And while the emerging markets (EM) countries have their own challenges, there might be a good story down the road. With peak central bank rate hikes largely being priced in, EM may be able to attract capital early next year, once developed market (DM) inflation fears have peaked. So, while it may be a bit too early to be overweight high quality fixed income, which in turn leaves parts of EM vulnerable, the back end of the U.S. yield curve has at least returned to levels that may provide some hedging value in the event of an extreme systemic shock, and hence some duration exposure can again be justified.

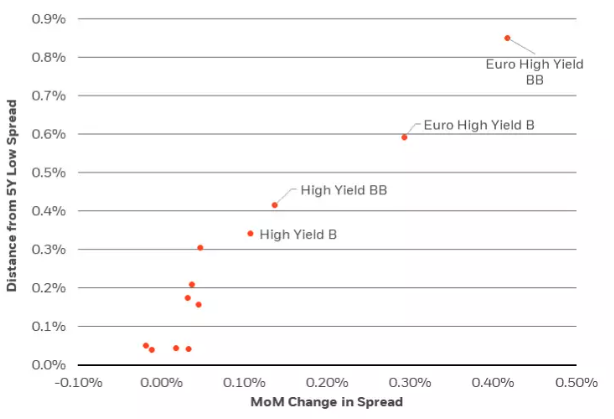

This spooky period for markets has also caused a minor shakeup lower down the capital stack (see Figure 10). High yield has cheapened up enough to justify the “scary” risks that will be with us for a while, and offers a much better technical entry point for owning risk today. And the return on equity continues to stand out as being one of the highest “yields” in major asset classes today, and large enough to withstand the shakeup in yields at the other end of the capital stack, we believe, as we wrote about extensively in last month’s commentary (There’s More Than Just an Underwater Beach Ball in Today’s Investment Pool)

Figure 10: Lower Quality Fixed Income is at a More Reasonable Entry Point

Source: Bloomberg, data as of October 16, 2021

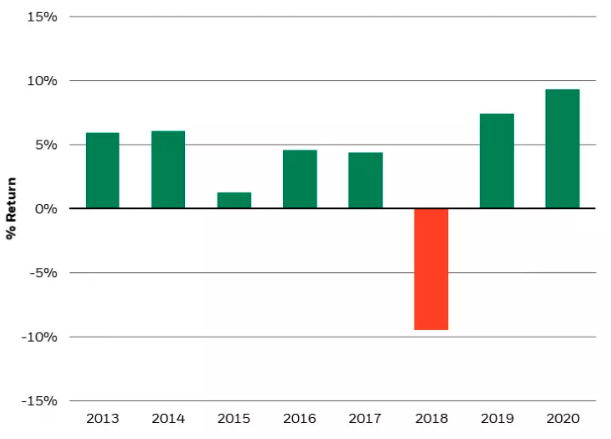

In fact, as we leave the spookiness of Halloween in the rear-view mirror, market seasonals quickly home in on Christmas and the traditional “Santa Claus” rally (so known for its timing, see Figure 11). The last two months of the year are often the best two months of the year for risk assets. We continue to like equities, European high yield, and commercial and residential real estate, as part of our diversified portfolio of real assets, in a world of still-negative real yields and of rising nominal yields.

Figure 11: The “Santa Claus” Rally

Source: Bloomberg, data as of October 19, 2021 Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

Rick Rieder, Managing Director, is BlackRock’s Chief Investment Officer of Global Fixed Income and is Head of the Global Allocation Investment Team.

Investing involves risks, including possible loss of principal. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. It is not possible to invest directly in an index.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic, or other developments. These risks may be heightened for investments in emerging markets. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks may be heightened for investments in emerging markets.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of October 29, 2021 and may change as subsequent conditions vary. The information and opinions contained in this commentary are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees, or agents. This commentary may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Prepared by BlackRock Investments, LLC, member FINRA

©2021 BlackRock, Inc. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

USRRMH1121U/S-1893895-1/20

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All