Ready or Not, the Transition to Net-Zero Carbon Emissions Will Be Highly Inflationary

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Policymakers can’t keep inflation at 2%, but they think they can keep the world’s temperature from rising 2° Celsius (or 3.6° Fahrenheit).

That’s how CLSA’s equity strategist Damian Kestel describes the goings-on at COP26, the United Nations’ climate change conference taking place now in Glasgow, Scotland. The attending leaders and policymakers may look like they’re in control, Kestel said in a note to clients today, but “a quick look at debt levels, inflation and yield movements suggest they are increasingly now mere passengers along for the ride and painted into a corner.”

Indeed, global debt is fast approaching a head-spinning $300 trillion. Here in the U.S., national debt will soon top $30 trillion, while debt-to-GDP currently stands at 126%.

Inflation is looking less and less “transitory,” and make no mistake: Transitioning to a zero-carbon energy mix as quickly as climate scientists are urging will be highly inflationary. Investment in fossil fuels is rapidly falling, which is driving up energy prices, and yet most economies are nowhere near ready to move to 100% renewables. That includes the U.S., which was one of a few large countries—the others being China, India, Japan and Australia—that did not sign the pledge this week to phase out the use of coal.

Vulnerable European Families Could Be Without Power this Winter

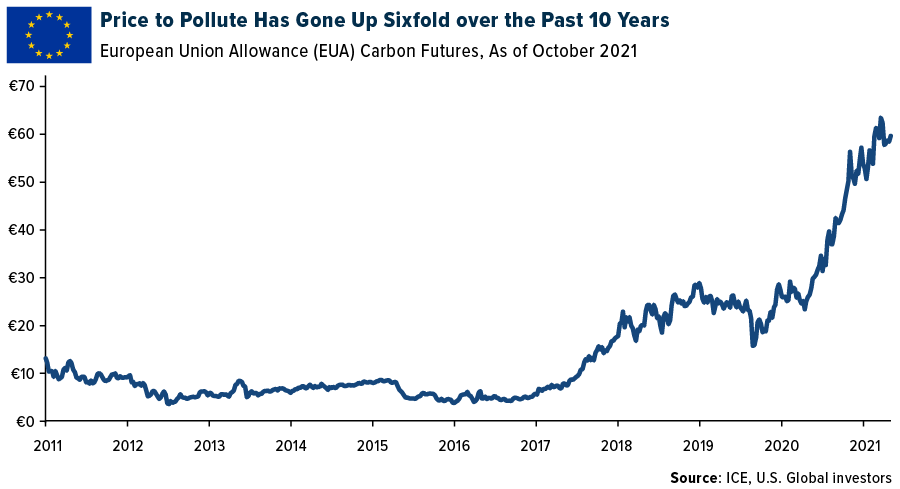

Europe is already feeling the pain of soaring energy costs. Under the European Union’s Emissions Trading System (ETS), companies must pay to emit carbon. This tax has gone up sixfold over the past 10 years, and it’s doubled in the past year alone. The bloc is now proposing so-called carbon border adjustment mechanisms (CBAMs), which are taxes on imported goods, such as steel and cement, that are produced in countries that lack tough climate laws.

These higher expenses on businesses will then be passed on to customers, and those that will suffer the most are poor households. Winter is right around the corner, and European governments fear that many families, who are still reeling from the economic impact of the pandemic, may be left in the cold.

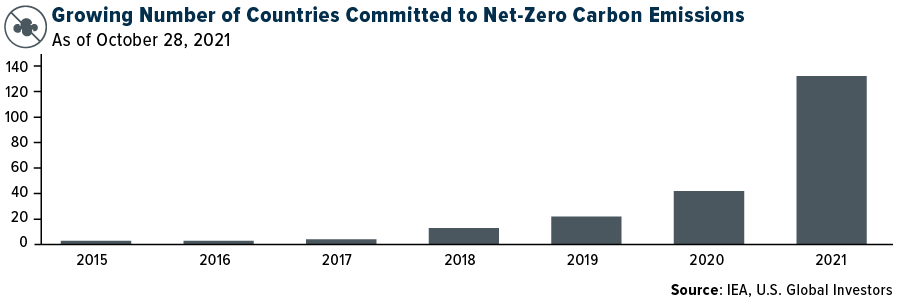

Nevertheless, a growing number of countries are now committed to net-zero carbon emissions. This is the reality, ready or not. Activists and policymakers say climate change is the number one threat of our time, and that doing nothing is not an option.

That may be the case, but we must acknowledge the impact this historic transition will have on inflation and debt levels. Whereas the former is a hidden tax on current economic growth, the latter is a tax on future growth.

And Yet We’ll Need to Continue Mining for Raw Materials

Guess what percent of a typical wind turbine is steel. Depending on the source, the answer is between 70% and 80%. As Wood Mackenzie’s Ed Crooks put it in a blog post this week, “Steel is one of the great paradoxes of the energy transition.” Although it’s essential for renewables technologies, the material “accounts for about 7% of total carbon dioxide emissions from energy use,” Crooks says.

And yet, for now, we need the stuff.

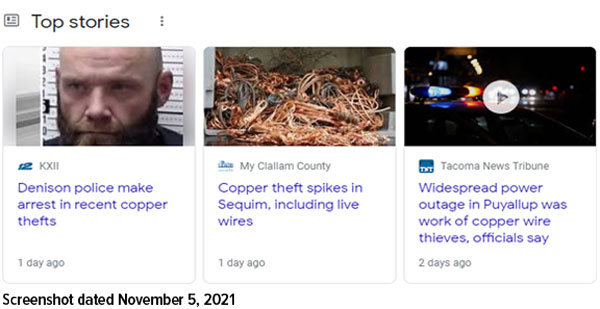

The same goes for copper, the global demand for which is expected to double this decade, from 2.1 million tonnes in 2020 to 4.3 million in 2030. Check out the informative infographic by Visual Capitalist by clicking here.

Copper is off its all-time high set in May, but it’s still going for double its price in March 2020. Many people expect the metal to continue increasing in value, which is why we’ve seen an increasing number of copper wire thefts lately.

We’re just as bullish on copper, but we prefer to get exposure with Ivanhoe Mines. The company, headed by billionaire Robert Friedland, recently reported a new daily production record of 729 tonnes of copper, bringing its year-to-date total production to 63,000 tonnes as of October 20.

Smart Money Preparing for Higher Inflation with Bitcoin

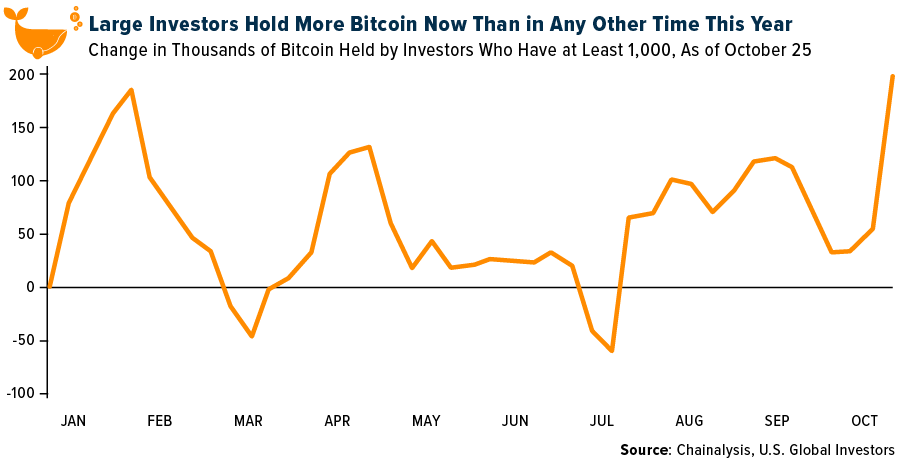

The smart money also appears to be preparing for higher inflation by loading up on Bitcoin. According to blockchain data provider Chainalysis, Bitcoin “whales,” or those that hold more than 1,000 BTC, added 185,000 BTC in the week ended October 25. This was enough to bring total holdings up to their highest levels so far in 2021.

Meanwhile, Bitcoin supply isn’t keeping up with demand, an imbalance that will only accelerate as more and more people participate and the mining difficulty increases.

Remember, Bitcoin supply is capped at 21 million coins, and there are 7.8 billion people. You do the math. Bitcoin may look overvalued at today’s prices, but I believe we’re still very early.

Wondering how you can buy Bitcoin? Check out these five easy-to-use apps in our latest video!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.42%. The S&P 500 Stock Index rose 1.99%, while the Nasdaq Composite climbed 3.05%. The Russell 2000 small capitalization index gained 6.08% this week.

- The Hang Seng Composite lost 2% this week; while Taiwan was up 1.82% and the KOSPI fell 0.05%.

- The 10-year Treasury bond yield fell 0.5 basis points to 6.62%.

Airline Sector

Strengths

- The best performing airline stock for the week was GOL Linhas Aereas Inteligentes SA, up 9%. Air France’s third quarter results exceeded consensus thanks to better-than-expected yields and a strong performance in Transavia, its low-cost subsidiary. The company plans to ramp-up to 70 to 75% of 2019 capacity in the winter quarter. Bookings were much better than the airline expected as well, and particularly strong for transatlantic routes, which are trending near 2019 levels.

- System net sales improved for the fourth straight week to down 43.6% versus 2019 for the week (versus last week’s level of -46.5%). Over the month of October, there was a steady acceleration in bookings, with pricing improving at a much slower rate, likely due to sale activity and heightened competition for the leisure traveler ahead of the holiday season. Domestic tickets sold stepped up to down 14.3% versus 2019 (and versus -17.8% last week), which is an improvement from the start of October. Domestic leisure (bookings through online channels) remained above 2019 levels at 11.8% versus 2019 (and versus 6.0% last week).

- Air Canada’s third quarter results came in largely ahead of expectations, with the company reporting both capacity (60% below 2019 levels versus guidance for 65%) and net cash flow of $2 million USD per day, versus guidance of a cash burn of $3-$5 million USD. Keys from the quarter were the fourth quarter outlook, which was highlighted by a healthy sequential improvement in capacity. Going forward, the company indicated that it would no longer be providing cash flow guidance “in light of the transition towards a post-pandemic environment.”

Weaknesses

- The worst performing airline stock for the week was Cargo Jet, down 6.74%. Ryanair’s second quarter results came in below consensus. While the financial year 2022 (FY22) traffic outlook improved slightly, the FY22 loss guide was widened. However, it implies a second half of 2022 outlook in line with consensus. Ryanair has increased its FY22 traffic guidance to ‘just over 100 million passengers’ (from the upper end of 90-100 million previously), slightly ahead of consensus. The company now expects a loss of €100-200 million euros, worse than previous guidance of a small loss to breakeven, driven by challenging pricing and yields coupled with rising costs for unhedged fuel needs. This is below consensus, which has yet to adjust for higher fuel prices.

- According to Bank of America, Air France will need an estimated €2.1 billion euros more equity capital to achieve its 2x leverage target by 2023. This is lower than the previous €2.5 billion euros consensus estimate due to a higher 2023 EBITDA forecast. No update was given on the potential timing and size of an equity raise, but the company will wait until market conditions improve. Air France also needs to address its negative equity, which stood at €3.8 billion euro as of the first nine months of 2021. Additional hybrid instruments are likely, although the chief financial officer (CFO) acknowledged these would be transitory.

- Airline stocks underperformed in October, down 7.2% versus the S&P at a positive 6.9%, as a majority of U.S. airlines reported third quarter earnings. The positives during earnings are that airlines reported strong recent bookings trends after the Delta variant spread lessened, with a rebound in corporate and international demand on the horizon. But airline stocks underperformed given higher cost pressures (both operating and fuel related), leading many carriers to walk back longer-term unit cost targets. Furthermore, fourth quarter highlights include leisure seasonality with some leisure carriers guiding towards weaker sequential revenues versus 2019 levels.

Opportunities

- The U.K. government removed the last seven remaining South and Central American countries from its red list, although the red list and hotel quarantine policy remains in place. The U.K. also extended vaccine recognition for travel to an additional 30 countries, including Argentina, Tanzania, and Cambodia. The EU formally recognized the U.K.’s National Health Service (NHS) pass as proof of vaccination, making it easier for U.K. travelers to prove their status.

- Tickets booked through large and small corporate channels improved to -46.3% (versus -48.6% last week) and -16.4% (versus -19.1% last week), respectively. Both are now at their highest levels since the pandemic started, coinciding with the latest Transportation Security Administration (TSA) throughput data improvement. After stabilizing between down 20% to 25% versus 2019 following the summer peaks, the TSA throughput trailing seven-day average stepped up to down 16.7% this week (versus -21.5% last week) and is now near its summer peak of -14%.

- U.S. airlines’ trailing seven-day website visits are at 10% for the week compared to 7% last week. Low-cost airlines have the best website traffic with JetBlue at 28% versus 2019 (versus 13% last week), Allegiant at 34% (versus 20% last week) and Southwest at 23% (versus 7% last week). American Air at 23% had the best traffic out of the network carriers.

Threats

- European airline bookings stepped down in the week after showing strong momentum over the past few months. Intra-Europe net sales decreased by 19 points to -42% versus 2019 (versus -23% in prior week) and declined by 18% week-on-week. International net sales were down by 4 points to -54% versus 2019 (versus -50% in prior week), with a 5% fall this week. This drove an 8-point decline in system-wide net sales for flights booked in Europe to -51% (versus -43% in the prior week). The sharp decline in bookings is likely due to the later timing of October school holidays than in 2019 across Europe.

- American Air is making headline news for poor operations, with 2,100 flights canceled out of 22,000 scheduled. The airline reports 50-60 mph winds caused three runways to close at DFW, with delays and cancellations causing crews to be displaced and out of sequence, which then snowballed into the weekend. A good portion of the flight cancellations were due to flight attendant issues and, as of today, 1,800 flight attendants came off unpaid leave. Labor also points to IT underinvestment and staffing.

- Southwest Airlines pilots’ request to block the vaccine mandate has been denied by a Federal Judge in Texas. According to CNBC, the Southwest Airlines Pilots Association, which represents almost 10,000 pilots, requested a temporary restraining order against the vaccine mandate, which was rejected by a federal judge in Texas last week. Because Southwest is a federal contractor, the airline is subject to a government mandate that requires staff to be vaccinated against COVID-19. However, the Southwest pilots union claimed that the airline violated the Railway Labor Act by changing work and pay rules without negotiating. U.S. District Judge Barbara Lynn denied this claim and stated that “requiring Southwest employees to be vaccinated against COVID-19 will likewise improve the safety of air transportation, efficiency of Southwest’s operations, and further the collective bargaining agreement’s goal of safe and reasonable working conditions for pilots.”

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 4.2%. The best performing country in Asia this week was Taiwan, gaining 0.82%.

- The Czech Koruna was the best performing currency in emerging Europe this week, gaining 1.6%. The Indian rupee was the best performing currency in Asia this week, gaining 1.0%.

- Manufacturing activity in Europe has been slowing down, but the PMI index remains well above the 50 level that separates growth from contraction. October’s final Manufacturing PMI was released at 58.3 versus the preliminary reading of 58.5. Italy’s Manufacturing PMI spiked to 61.1 in October from 59.7.

Weaknesses

- The worst relative performing country in emerging Europe for the week was Hungary, gaining 0.62%. The worst performing country in Asia this week was Malaysia, losing 2.6%.

- The Turkish lira was the worst performing currency in emerging Europe this week, losing 1.0%. The Indonesian rupiah was the worst performing currency in Asia this week, losing 1.0%.

- The China Manufacturing PMI fell deeper into the contraction area. The October Manufacturing index was released at 49.2 versus the 49.7 expected and the 49.6 in September. Service activity in China slowed down as well due to increased number of COVID infections and China’s zero tolerance policy.

Opportunities

- S. Lombard in a daily note said that China will most likely stick with its zero COVID tolerance policy for at least five more months. The investment strategy firm sees the country slowly staring to re-open after the vaccination rate reaches 90%, the winter flu season is over and the winter Olympics are finished. China has closed its border since the star of the pandemic and looser restrictions next year should contribute to pick up in economic activity.

- Investors are cautious with China due to the recent news about Xi Jinping’s plan for common prosperity and latest announcements by mostly Chinese property companies missing coupon payments on their debt obligations due to the lack of liquidity. However, Goldman Sachs says that there are opportunities in China despite the slew of negative news coverage. Broker published a list of 50 stocks that appear to be well positioned to benefit from Xi’s desire to focus on wealth distribution, recommending investors to focus on renewable energy and domestic technology production among few areas that are well positioned to benefit from changes taking place in the country and around the world.

- Europe has become the pandemic epicenter with infections increasing rapidly, but once the cold winter ends, the COVID situation will improve, and economic growth will bounce back supported by continued fiscal and monetary stimulus. The survey of economic growth for the eurozone will come out next week and we will most likely see a strong reading. The increase in COVID cases in Europe is seasonal. With Pfizer testing, use of a pill to fight COVID, and kids 5 to 11 years old being allowed to take the Pfizer, the COVID pandemic will ease, and growth will resume.

Threats

- China will possibly release a higher inflation next week when data comes out on November 11. Bloomberg economists predict inflation to increase 1.4% in October year-over-year versus 0.7% in September.

- The lira has reached a new record low this week and may weaken further against the dollar. Inflation in Turkey was reported at 19.89% in October below the expected 20.35%. Slightly weaker inflation than expected may give central bank a green light to cut rates again at the next meeting. President Erdogan believes that lower rates will eventually bring inflation down.

- While developed markets are keeping rates very low, emerging markets in Europe already started to hike rates in order to slow down inflation. This week, Poland and Czech Republic raised rates more than expected. Poland raised its rate to 1.25% from 0.50% and Czech Republic hiked to 2.75% from 1.5%. The Bank of England kept its rate unchanged this week, but Western Europe and the developed markets may soon be changing their monetary policy.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was the Bloomberg Powder River Basin 8800 Btu Coal Spot Fob/Gillette Wyoming, up 8.68% where the supply chain to get coal delivered id pushing up prices. Oil rose on the speculation that OPEC+ could spurn mounting pressure to boost production at a faster clip, even as consumption roars ahead of supply. Speaking at the Group of 20 (G20) summit on Sunday, U.S. President Joe Biden criticized the countries of Saudi Arabia and Russia for an inadequate response to the energy crunch, while declining to say what he’d do if producers don’t act. Crude oil has soared this year through increased consumption as economies recover from the pandemic. An energy squeeze marked by shortages of gas and coal has also stoked oil demand.

- Fertilizer prices continue to move higher. Urea prices were generally higher with limited supply due to China’s absence from the global market and India’s continued tendering activity. Ammonia prices moved up with the market remaining very tight, led by a big jump in the Tampa November contract settlement. Phosphate prices continued to move higher, although on a relatively smaller scale. Potash prices moved up again as well as demand remains supported by relatively strong crop prices and prolonged supply chain concerns.

- Freeport Copper has announced that its Board has approved a new share repurchase program authorizing repurchases of up to $3 billion USD of common stock. The Board also approved the addition of a variable cash dividend on common stock for 2022 at an expected annual rate of $0.30 per share. The combined annual rate of the base dividend and the variable dividend is expected to total $0.60 per share. The Board intends to declare quarterly dividends for 2022 of $0.15 per share (including the $0.075 variable component), with the initial quarterly dividend expected to be paid on February 1, 2022.

Weaknesses

- The worst performing commodity was DCE Iron Ore Futures, down 14.25% for the week as it was reported steel output in China, the second largest economy, has fallen to its lowest level since March of 2020.Early indications are that October polyethylene prices in the U.S. are likely to settle at $0.05 per pound lower. This follows a significant rebound in domestic inventories and an over extended U.S. price backdrop. Given the spread and inventory levels, there is more weakness to come before year-end. How much remains a topic of debate, with consultants forecasting roughly $0.15 per pound of give back over the fourth quarter.

- According to Bank of America’s latest proprietary steel survey, demand worsened, and supply continues to decline, while price and margin trend down. Steel prices rose first in early October, then fell in mid-October and the decline accelerated in late October. Given market demand was worse than expected, traders were cautious and not motivated to take goods. Steel mills’ orders were also average as downstream purchases were mostly on-demand. Looking into November, steel mills and traders have a pessimistic sentiment for long steel as it enters the demand off-season, coupled with downward expectations of raw material prices.

- Chinese iron ore futures plunged as steel output in the world’s second-largest economy fell to its lowest level since March 2020 in late October. Futures for iron ore to be delivered in China in November fell more than 6% on Tuesday – down almost 20% in the last five days, as contracts for December delivery slipped 5.7%.

Opportunities

- The U.S. and European Union (E.U.) announced a deal this weekend that removes Section 232 tariffs on imports from the E.U. and replaces them with a tariff rate quota system. The agreement ends a dispute dating back to 2018 when President Trump imposed Section 232 tariffs on steel and aluminum imports, and it heads off retaliatory tariffs threatened by the E.U. Initial reaction to the truce between the U.S. and E.U. is generally positive, though trade groups in the U.S. call for strict enforcement of the quota limits to keep “unfair” imports from U.S. shores.

- Record free cash flow in the U.S. shale patch is boosting mergers and acquisitions among explorers, particularly as the private equity backed producers ramp up output and their owners seek exit options. Investors seeking consolidation have favored all-stock deals that don’t come with hefty premiums.

- Short-term copper contracts are once again trading at a huge premium to futures in London; this is a sign that last month’s unprecedented tightness in spot supplies is far from over. While futures prices are tumbling as the outlook for demand deteriorates, surging premiums for spot contracts point to a supply shortfall on the London Metal Exchange, with inventories near a multi-decade low. Premiums for spot contracts hit record levels last month, in a condition known as backwardation that signals spot demand is far outpacing supply.

Threats

- Japan’s biggest power generator holds higher inventory of liquefied natural gas (LNG) than last year, and has adequate stocks for the winter demand season, its official stated on Monday. “We have been securing supply quite heavily, which puts us taking on risk of holding excess fuel. But we are doing everything we can,” said Takashi Noguchi, executive officer. “At this stage, we think we are holding enough stock for this winter,” he told reporters. His comments confirm the industry’s ministry’s data that Japan’s LNG inventories held by major utilities as of mid-October were at the highest level in five years, as a wider energy crunch gripping many countries raised the prospect of a second winter of shortages. Electricity prices in Japan rose to their highest in nearly 10 months amid elevated global prices for LNG and coal — the main fuels that supply the country’s $150 billion power market.

- Chinese gas companies are finding ways to pass on high gas import costs to end-users amid soaring global energy prices and the country’s tight regulated price environment, which is largely designed to keeping a lid on inflation and keeping gas affordable for critical sectors like winter heating and residential use. At its third quarter results briefing on October 29, state-owned PetroChina’s chief financial officer Chai Shouping said it plans to pass the higher cost of spot LNG to buyers to help minimize losses. “For natural gas cargoes which have been sold, we will stick to the contract prices, while the spot cargoes will be sold based on market prices,” Chai said, but also noted that most of the national oil company’s gas supply was under term contracts both with domestic buyers and global suppliers.

- CME Group’s AUP Midwest aluminum premium futures forward curve moved lower during the week as the entire curve saw trader selling from December and throughout calendar year of 2022. The structure of the curve continued to tighten over the last week as all-in spot prices fell from record highs. Offers by traders have moved lower on some slightly bearish signals in the market and aggressive trader forward selling of AUP futures. The three-months aluminum price on the London Metal Exchange has fallen by 16% since October 8.

Domestic Economy & Equities

Strengths

- New jobless claims continued a downward trajectory for a fifth week, declining more than expected to 269,000 from a revised 288,000. It’s a new pandemic low. Continuing claims declined to 2,105,000 from last week’s 2,243,000. Unemployment rate declined to 4.6%, beating the 4.7% estimate.

- The October Manufacturing PMI weakened to 58.4 versus 59.2 in September. However, the Service PMI increased to 58.7 in October from 58.2 in September. Thanks to stronger service activity, the Composite PMI edged higher to 57.6 from 57.3.

- Arista Networks, a communication technology company, was the best performing S&P 500 stock for the week, increasing 29.5%. Shares soared on Tuesday after the company gave a fourth-quarter revenue forecast that was stronger than expected, declared a stock split, and boosted its plan for share buybacks.

Weaknesses

- A preliminary read showed third quarter productivity down 5.0% (versus consensus for a 3.1% drop) as output rose by 1.7% against a 7.0% increase in hours worked. It was the lowest rate of quarterly productivity growth since 1981.

- The Producer Price Index (PPI) increased 16% in September on year-over-year basis above expected 15.4%, and prior 13.4% pointing to more inflationary pressure.

- Moderna, a pharmaceutical company, was the worst performing S&P 500 stock for the week, losing 31.6%. Modena fell sharply on Pfizer’s COVID pill plan. Pfizer announced that the company’s currently experimental Covid pill reduces hospitalization and deaths in high-risk patients by 89%.

Opportunities

- U.S. authorities issued a federal rule mandating COVID vaccinations or at least weekly testing for workers at U.S. companies with 100 or more employees. Workers must be fully vaccinated by January 4 or submit to weekly testing. Merck’s oral antiviral pill was found to be safe and effective by U.K. drug regulators, making it the first COVID pill to be approved so far.

- Markets reacted calmly to the taper announcement. There is a perception that the central bank will shift slowly away from pandemic-related policy accommodation. The easy financial conditions most likely will stay for a while, consumer spending will remain strong pushing U.S. equites higher.

- Drugmaker Pfizer said its experimental pill designed to fight coronavirus reduced the risk of hospitalization and death for high-risk patients taking part in a trial of the drug. A so-called interim analysis – done before the trial was scheduled to end – showed an 89% reduction in the risk of hospitalization or death from Covid-19 if patients got it soon enough, CNN reported. Last week, Pfizer’s COVID vaccine was approved for kids ages 5 to 11 years old.

Threats

- Inflation will likely continue to rise. Bloomberg economists predict the CPI to spike to 5.8% in October on a year-over-year basis. The core inflation is expected to spike to 4.3% from 4% in September.

- Initial jobless claims will probably continue to drop as job markets continue to improve. Weekly new claims have fallen substantially from the 2020 peak of about 6.1 million new claims in a single week, and in recent weeks have inched closer to the 200,000 new claims per week seen before the pandemic.

- The central bank has been buying $120 billion in mortgage-backed securities and Treasury bonds each month to keep cash flowing through the financial system but will reduce that by $15 billion per month starting this month. That pace would bring the program to a close by the middle of 2022 if it is sustained.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Doge Universe (SPACEXDOGE), rising 511,160.61%.

- New York City Mayor-elect Eric Leroy Adams said he would take his first three paychecks in Bitcoin. He tweeted the news on Thursday and mentioned that “NYC is going to be the center of the cryptocurrency industry.”

- Compounding and saving in Bitcoin by using a dollar-cost averaging strategy helps reduce the impact of Bitcoin’s volatility. Bitcoin is a savings technology and a store of value when you save consistently, writes CoinDesk.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Squid Game (SQUID), down 98.88%.

- Riskier Bitcoin ETFs are proving to be too much for the SEC, says Bloomberg. According to the article, leveraged ETFs are getting rejected by the SEC and in some instances being withdrawn on the same day they are filed.

- According to a Harris Poll, 61% of people who have heard of cryptocurrencies don’t understand them. They have little to no understanding of how cryptocurrency works and only 14% of those familiar with cryptos reported that they understand them “very well,” writes Bloomberg in a recent report.

Opportunities

- Money managers risk falling behind and underperforming peers that own crypto assets. The chart shows a 200% outperformance of the Bloomberg Galaxy Crypto and DeFi indexes in 2021 versus the S&P 500. Selloffs in crypto assets appear to be attracting responsive buyers, which they could fall behind if they avoid crypto allocations, writes Bloomberg commodity strategist Mike McGlone.

- Global crypto exchange Binance is starting a $100 euro initiative to develop the blockchain and crypto ecosystems in France and Europe. An article written by Coin Telegraph stated that the Binance CEO announced the news when he spoke with the French Minister this past week.

- JPMorgan says Ethereum is a better bet than Bitcoin as interest rates rise due to the boom in DeFi and NFTs (non-fungible tokens). One JPMorgan analyst states that Bitcoin is like digital gold and likely to fare less well as interest rates and yields rise. Ethereum, on the other hand, is at the heart of decentralized finance and the market for NFTs.

Threats

- Cybercriminals are cashing out ransoms at Moscow’s tallest Tower, writes Bloomberg. The building is home to more than a dozen companies that convert cryptocurrencies to cash which enables criminals to cash out profits from digital crimes. Experts have linked four companies to money laundering according to the US Treasury Department.

- The grocery chain Kroger Company said that the press release that announced plans to accept Bitcoin cash was fraudulent. According to the Bloomberg article, a Kroger representative confirmed it to Bloomberg News that the company hadn’t issued that statement. A similar false statement was made about Walmart accepting Litecoin a few weeks ago on the same website.

- When the Fed starts to raise interest rates to cool the economy, it could have a negative impact on Bitcoin’s price. “To extend BTC is a hedge like gold, I think it could suffer,” says economist Claudia Sahm. Bitcoin has benefited over the past several months of quarter end from the belief that it’s an inflation hedge and smart money bought into it and profited. With the Biden administration unclear about Jerome Powell, a lot of uncertainty looms about the Fed’s actions starting in February 2022, writes CoinDesk.

Gold Market

This week spot gold closed the week at $1,818.36, up $34.98 per ounce, or 1.96%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.68%. The S&P/TSX Venture Index came in up 3.65%. The U.S. Trade-Weighted Dollar rose slightly up 0.10%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-31 | Caixin China PMI Mfg | 50.0 | 50.6 | 50.0 |

| Nov-1 | ISM Manufacturing | 60.5 | 60.8 | 61.1 |

| Nov-3 | ADP Employment Change | 400k | 571k | 523k |

| Nov-3 | Durable Goods Orders | -0.4% | -0.3% | -0.4% |

| Nov-3 | FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Nov-4 | Initial Jobless Claims | 275k | 269k | 283k |

| Nov-5 | Change in Nonfarm Payrolls | 450k | 531k | 312k |

| Nov-9 | Germany ZEW Survey Expectations | 20.0 | — | 22.3 |

| Nov-9 | Germany ZEW Survey Current Situation | 18.0 | — | 21.6 |

| Nov-9 | PPI Final Demand YoY | 8.6% | — | 8.6% |

| Nov-10 | Germany CPI YoY | 4.5% | — | 4.5% |

| Nov-10 | Initial Jobless Claims | 266k | — | 269k |

| Nov-10 | CPI YoY | 5.8% | — | 5.4% |

Strengths

- The best performing precious metal for the week was spot gold, up 1.96%. Nomad Royalty Company has entered a gold stream with respect to Orion’s 40% interest in Greenstone Gold Mines, which operates the Greenstone Gold Project located in Canada. The company will make cash payments totaling $95 million for 5.9% of gold production attributed to Orion’s 40% interest in Greenstone until 120,333 ounces have been delivered, and 4.0% thereafter. Nomad will make ongoing payments equal to 20% of the spot gold price and, in addition, will make payments of $30 per ounce to fund mine-level ESG (Environmental, Social and Governance) programs.

- Gold edged higher from a three-week low as the Federal Reserve signaled it will be patient on raising interest rates, after announcing it will start reducing bond purchases this month. Chair Jerome Powell on Wednesday stressed that the tapering – at a pace of $15 billion per month – doesn’t mean policymakers will hike rates any time soon for they want to see the labor market heal further first. A Federal Open Market Committee (FOMC) statement also included new language that inflation might not prove to be entirely transitory. Based on the market reaction, (equities up, gold up, cyclical commodities up), the market perceived it as dovish.

- Several gold companies reported better than expected earnings. Kirkland Lake reported earnings per share (EPS) of $0.91/share ahead of consensus at $0.81/share on production of 370,000 ounces better than consensus at 349,000 ounces. Fosterville and Detour drove the third quarter beat, with throughput at Detour at an annual high. Royal Gold reported third quarter results that exceeded consensus. EPS was $1.07, ahead of the consensus of $0.97, supported by total production of 97,000 ounces (5% ahead of consensus). The company increased second half 2021 stream guidance by 3%.

Weaknesses

- The worst performing precious metal for the week was silver, but still up 1.08%. Marathon is focused on the Valentine Gold Project, the largest gold project in Newfoundland with a resource base of 4.8 million ounces. Management announced the start of construction would be delayed after the province requested additional information for the Environmental Impact Study. Construction will commence in the third quarter of 2022 (previously 1Q 2022) with first gold production in third quarter 2024 (previously 1Q 2024).

- Pure Gold Mining reported third quarter production of 9,000 ounces of silver, 23% below the 12,000 consensus, largely due to significantly lower milled grades in September owing to inaccessibility of high-grade stopes as underground development rates lagged long hole production. Additionally, Pure Gold lowered its fourth quarter throughput and grade guidance to 600-700 tons per day and 5.5-6.5 grams/ton, respectively, while simultaneously postponing expectations to sustain 1,000 tons per day mill throughput.

- B2 Gold Headline reported EPS of $0.12, below the consensus of $0.13 because of higher income taxes and slightly higher cash costs. Total cash cost came in moderately above consensus. Total cash costs from the B2-operated mines came in at $572/ounce (versus consensus of $536/ounce). Wheaton Precious Metals reported third quarter EPS of $0.30, a miss vs. $0.34 consensus. Third quarter cash flow per share was $0.45, also a miss versus the $0.48 consensus. The EPS miss was driven fundamentally by lower revenue.

Opportunities

- This morning, Chifeng Jilong Gold Mining announced it is acquiring Golden Star Resources for $470 million in cash. Golden Star owns the Wassa Mine in Ghana. Chifeng Jilong tried to buy the Bibiani Mine in Ghana from Resolute Mining for $105 million earlier this year but ran into problems with the mining lease; Asante Gold ended up buying Bibiani for $90 million. In less than three years, nine producers/mines and ten pre-production companies/projects that have been acquired in the region.

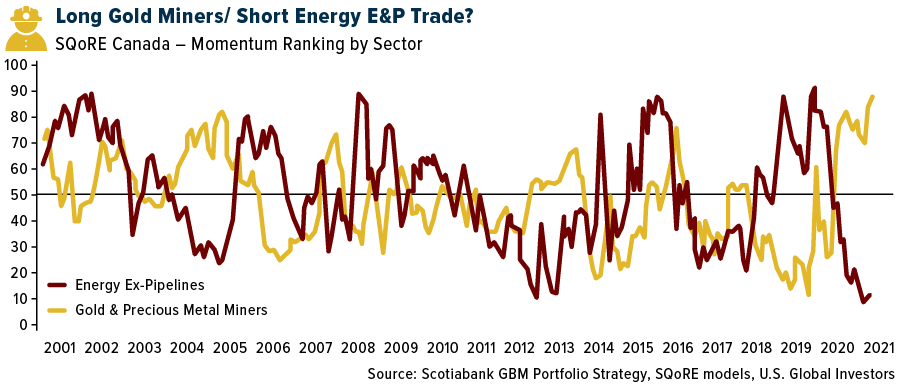

- According to Michael Letros at Scotiabank, he has been advocating for a Long Gold Miners / Short Energy E&P trade as the relative price momentum of the gold miners is at two-decade lows and the energy producers are at two-decade highs (both are relative to the S&P/TSX Composite). Based on Jean-Michel Gauthier’s (Scotiabank quant analyst) updated monthly report, the energy price momentum (red line) continues to break-out and the gold miner price momentum (yellow line) has only bounced a tiny bit off its lows.

- Indians flocked to jewelry stores on Tuesday on the biggest gold-buying day of the year, with a bumper sales period for precious metals that culminates during the festival of Diwali expected for the first time since the pandemic began. Dhanteras is traditionally seen as the most auspicious day in the Hindu calendar to buy gold, with many shops remaining open until midnight and jewelers offering discounts and gifts. Indians typically buy ornaments for marriage celebrations, and coins and bars for investment surge during a series of celebrations that culminates with Diwali, or the Festival of Lights, which fell on a Thursday this week.

Threats

- For Ghana, the gold disappears when you put a tax on it for small scale producers. Ghana introduced the levy in May of last year to boost revenue from its resource base. Before the tax went into effect, Ghana would export about 5 tonnes of gold a month from small miners, but that number is less than 1 and dropping now. Countries across West Africa are taking more steps to help formalize the artesian gold markets and Ghana announced they are reconsidering the implementation of the tax. In addition, Ghana’s first state-owned gold refinery is set to start operations in December with a process capacity of 400 kilograms a day with a goal of refining 30% of the country’s production.

- Chris Wood, global head of equity strategy at Jefferies, has upped his allocation to 10% from 5% for Bitcoin at the expense of gold bullion in his recent Greed and Fear report for his Asia ex-Japan portfolio. Chris cites the arrival of the Bitcoin ETF in America and the growing interest in crypto as a reason to pivot further to Bitcoin as a second lever to hedge a collapse of the U.S. dollar standard.

- Investors in Newfound Gold woke up to news released by the company of 30 selected samples of drill core that were re-assayed for gold content for quality control/quality verification analysis. The results showed the original core samples demonstrated a strong bias towards higher grades, particularly with the higher-grade samples in comparison to the new assays. Newfound Gold’s share price plunged as much as 27% during intraday trading to finish the day with its biggest 1-day loss in a year. The spectacular gold grades they were reporting had been a key driver of the share price. Historic event driven analysis done by CIBC World Markets on “Mining Stock Risks – Delays and Disappointments” showed that on average, a major exploration disappointment lowers the valuation of the company by about 45% and it takes 18-months to recover.

©_ US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All